Enjoy complimentary customisation on priority with our Enterprise License!

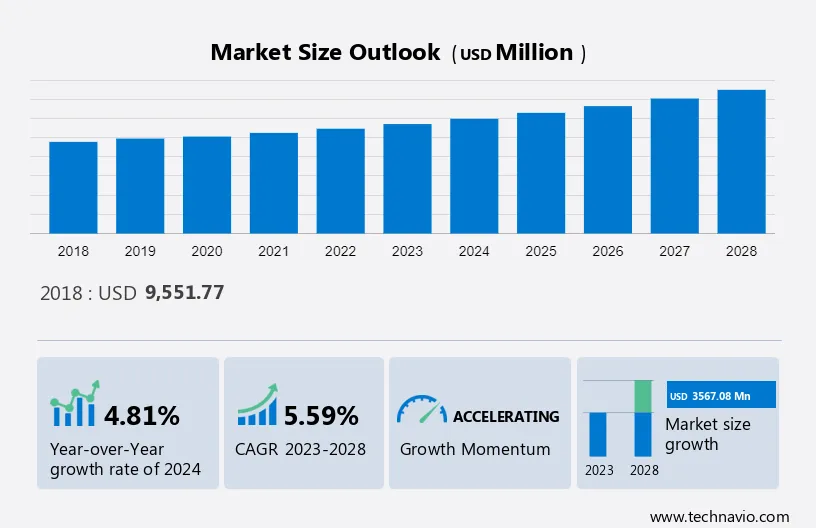

The global spinal implants market is estimated to grow by USD 3.57 billion at a CAGR of 5.59% between 2023 and 2027.

A favorable reimbursement scenario will lead to a raised demand for spinal implant procedures, which will, in turn, drive the growth of the market. Various reforms, such as the Affordable Care Act (Obamacare) in the US healthcare system, provide medical insurance coverage for more people. This has allowed patients with back pain to receive the best treatment with spinal implants. In addition, Europe, too, has well-established reimbursement policies for spine pain management procedures and implants. In APAC, countries such as Japan, Australia, and China have structured nationalizing policies for the minimally invasive interventional spine. The Japanese government has also started giving reimbursement coverage for spinal implants. The promising reimbursement scenario, along with the boost in the elderly population, is anticipated to drive the adoption rates in Asia. Thus, increasing reimbursements for spinal implants will drive the growth of the market during the forecast period.

Technavio has segmented the market into End-user, Product, and Geography

It also includes an in-depth analysis of drivers, trends, and challenges. Our report examines historical data from 2018-2022, besides analyzing the current market scenario.

To learn more about this report, Request Free Sample

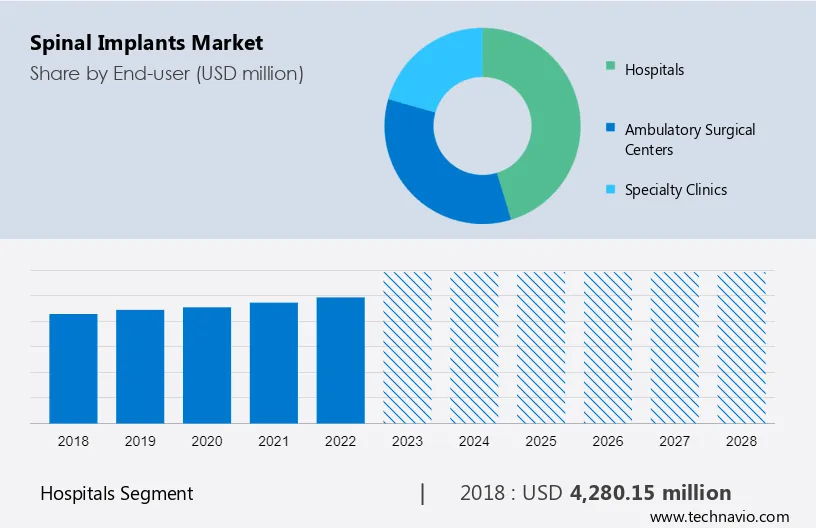

The market share growth by the hospitals segment will be significant during the forecast period. Hospitals typically use spinal implants for spinal fusion procedures. In spinal fusion surgery, two or more vertebrae are linked together to make stability in the spine. Spinal implants such as screws, rods, plates, and interbody cages, are used to secure the spine in the desired position, preventing movement between the fused vertebrae.

Get a glance at the market contribution of various segments Download PDF Sample

The hospitals segment was valued at USD 4.28 billion in 2018. Hospitals employ spinal implants, including interspinous process devices, in surgeries to address spinal stenosis, a condition characterized by narrowing of the spinal canal and compression of the spinal cord or nerves. Moreover, hospitals utilize spinal implants in surgeries to remove spinal tumors. These implants provide spinal stability after tumor resection. Thus, these uses of spinal implants will propel the growth of the hospitals segment and drive the market in focus during the forecast period.

Spinal fusion implants are medical devices used in surgical procedures to treat different spinal disorders that induce instability, pain, or neurological symptoms. Spinal fusion is a surgical technique that aims to join two or more adjacent vertebrae, creating a solid, immobile bridge between them. In addition, spinal fusion with implants can restore stability and correct the slippage. Moreover, spinal fusion may be used to treat herniated or ruptured discs that are causing severe pain, especially when other non-surgical treatments have been unsuccessful. Therefore, these factors will drive the growth of the spinal fusion implants segment of the market during the forecast period.

The non-fusion spinal implants segment includes artificial discs, dynamic stabilization devices, annulus repair devices, and nuclear disc prostheses. Non-fusion implants can be used to treat lumbar spinal stenosis, a condition where the spinal canal narrows and puts pressure on the spinal cord or nerves. Non-fusion implants can be used to stabilize the facet joints in the spine, which can become painful due to arthritis or degeneration. The demand for spine surgery in ambulatory surgical centers (ASCs) is increasing as payers are more willing to reimburse for spine procedures in the outpatient setting. Thus, such factors will drive the demand for the non-fusion spinal implants segment and enhance the market in focus during the forecast period.

For more insights about the market share of various regions Download PDF Sample now!

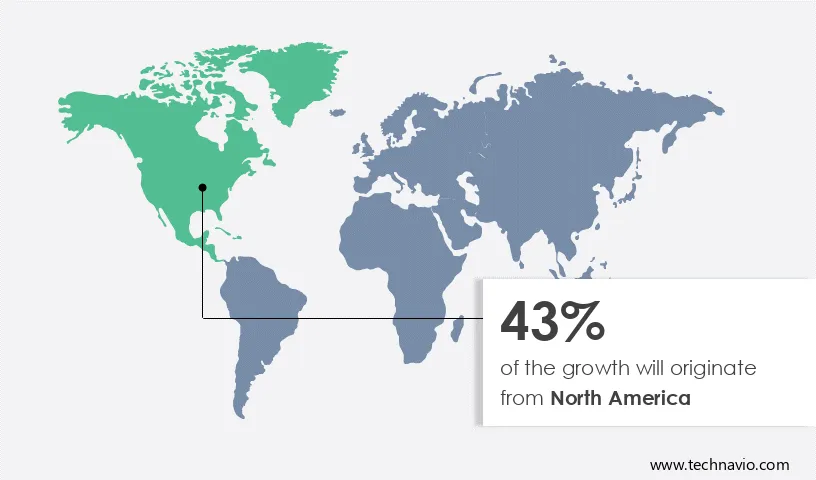

North America is estimated to contribute 43% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that will shape the market during the forecast period. There is an increasing prevalence of spine-related disorders in North America, including degenerative disc disease, herniated discs, spinal stenosis, and scoliosis. These conditions are becoming more common as the population ages, driving demand for spinal implant procedures.

Furthermore, North America has some of the world's most advanced and well-funded healthcare systems. In addition to that, North America has a highly skilled workforce of orthopedic surgeons, neurosurgeons, and spine specialists with expertise in complex spinal surgeries and the latest implant technologies. Thus, these factors will drive the growth of the market in North America during the forecast period.

In 2020, the outbreak of COVID-19 restricted the growth of the spinal implants market in North America. However, in 2021, the initiation of large-scale vaccination drives?lifted the lockdown and travel restrictions, which led to the resumption of supply chain activities. Furthermore, the region is home to various R&D centers and medical device companies focused on spinal implant innovations and technologies. Continuous investment in R&D leads to the introduction of advanced implants and surgical techniques. Hence, such factors will drive the growth of the market in North America during the forecast period.

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market. The report also includes detailed analyses of the competitive landscape of the market and information about 20 market companies, including:

B.Braun SE: The company offers spinal implants such as S4 spinal system, and lumbar fusion implants.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

There are multiple factors influencing market growth. Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges.

Growing focus on developing custom implants is the key factor driving market growth. The anatomically challenging 3D printing of implants for the spine needs expertise. The advancements in medical imaging and instrumentation have made the 3D approach a globally acknowledged method for repairing spine defects. The advanced techniques are either used alone or in conjunction with conventional techniques for better results. 3D printing, also called additive manufacturing technology, is achieving prominence and becoming increasingly popular in the medical devices industry.

Moreover, 3D-printed implants provide precise anatomical fit, minimal chances of error, and reduced hospitalization time and cost. Due to these advantages, surgeons have started using 3D printing to treat several spine diseases. The growing demand for 3D-printed implants encourages manufacturers to offer such implants that cater to the needs of modern medicine. Hence, the growing demand for 3D printing technology in the manufacturing of spinal implants will drive the growth of the global spinal implants market during the forecast period.

Rising minimally invasive procedures are the primary trend shaping market growth. Minimally invasive procedures usually need specialized implants designed for these procedures. These implants are generally smaller and designed to fit through the smaller incisions used in minimally invasive spine surgery (MISS). Patients who undergo minimally invasive procedures often experience less postoperative pain and discomfort compared to traditional open surgeries. This can improve patient satisfaction.

Moreover, many patients prefer minimally invasive procedures due to the smaller incisions, reduced scarring, and faster recovery. This patient preference can influence the choice of surgical approach and implants. Thus, rising minimally invasive procedures will boost the growth of the global spinal implants market during the forecast period.

High costs of spinal implants and procedures is a challenge that affects market growth. Spinal implants are used for the cure of spinal disorders such as spinal deformities, scoliosis, spinal fractures, and spinal stenosis. The cost of spinal implants depends on factors such as the brand and type of implants. The cost of spinal implants varies based on their type.

Moreover, the cost of spinal procedures, such as surgery, includes the cost of spinal implants, implantation procedures and consultation, medications, and consumables. The cost of spinal surgeries varies according to the type of procedure. In addition, the cost of spinal surgery treatment can also vary depending on healthcare infrastructure. Thus, such factors are expected to impede the growth of the global spinal implants market during the forecast period.

The market report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Global Spinal Implants Market Customer Landscape

The spinal implants market report forecasts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and growth opportunities from 2018 to 2028.

|

Spinal Implants Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

163 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.59% |

|

Market Growth 2024-2028 |

USD 3.57 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.81 |

|

Regional analysis |

North America, Europe, Asia, and Rest of World (ROW) |

|

Performing market contribution |

North America at 43% |

|

Key countries |

US, Germany, UK, Japan, and China |

|

Competitive landscape |

Leading Vendors, Market Positioning of Vendors, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

B.Braun SE, Globus Medical Inc., icotec AG, Implanet SA, Inion Oy, Innovasis Inc., JAYON IMPLANTS Pvt. Ltd., Johnson and Johnson, Medacta International SA, Medtronic Plc, MicroPort Scientific Corp., Orthofix Medical Inc., OrthoPediatrics Corp., Precision Spine Inc., RTI Surgical Inc., Stryker Corp., ulrich GmbH and Co. KG, Xtant Medical Holdings Inc., ZAVATION, and Zimmer Biomet Holdings Inc. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for the forecast period. |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

Download Sample PDF at your Fingertips

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by End-user

7 Market Segmentation by Product

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights

- US, Germany, UK, Japan, China - Size and Forecast 2024-2028")