Enjoy complimentary customisation on priority with our Enterprise License!

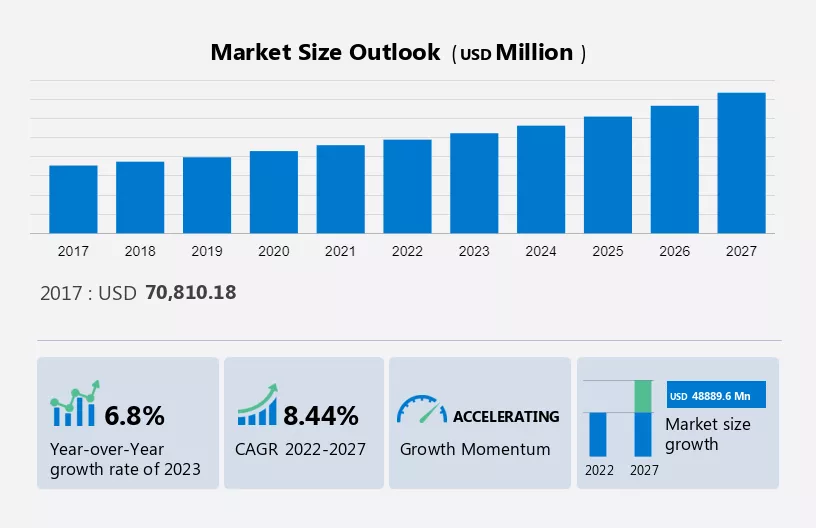

The Pharmaceutical Packaging Market size is estimated to grow by USD 48,889.6 million between 2022 and 2027 accelerating at a CAGR of 8.44% during the forecast period. Primary factors boosting the growth of the market are the increase in R&D spending in the pharmaceutical industry, growing sales of pharmaceuticals globally, and the increasing demand for convenience in pharmaceutical packaging.

This pharmaceutical packaging market research report extensively covers market segmentation by material (rigid plastic, flexible plastic, glass, and others), product (plastic bottles, caps and closures, blister packs, pre-fillable syringes, and others), and geography (North America, Europe, APAC, Middle East and Africa, and South America). It also includes an in-depth analysis of drivers, trends, and challenges.

Manufacturers in the global pharmaceutical packaging market provide different types of packaging, such as primary and secondary packaging for various pharmaceutical products. Pharmaceutical products that are available in solid, semisolid, liquid, and powder form are packed in plastic bottles, blister packs, parenteral containers, pouches, and others.

Our researchers analyzed the data with 2022 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers, trends, and challenges will help companies refine their marketing strategies to gain a competitive advantage.

An increase in R and D spending in the pharmaceutical industry is a major pharmaceutical packaging market driver. Pharmaceutical companies are investing heavily in research and development (R&D), allocating approximately 15%-20% of their revenue for this purpose. In 2020, companies like Biogen and F. Hoffmann-La Roche spent around 18%-20% and 20% of their revenue on R&D, respectively. This increased R&D expenditure is anticipated to lead to more pharmaceutical products in the market, thus driving the need for pharmaceutical packaging. By outsourcing packaging operations to third-party providers, pharmaceutical manufacturers can reduce capital expenditure and operating costs associated with packaging machinery, space, and labor. This allows them to focus on their core business. As a result of the growing R&D spending, there is an expected rise in demand for innovative packaging that offers convenience and product differentiation.

Expansion of manufacturing facilities is an ongoing pharmaceutical packaging market trend. Due to the increasing demand for pharmaceutical products such as drugs, vaccines, and others, pharmaceutical glass packaging companies are expanding their manufacturing facilities to meet the demand. Some of the instances of expansion by the companies include:

Thus, the growing expansion of manufacturing facilities by the companies will drive the market to focus during the forecast period.

The risk of counterfeiting in pharmaceutical packaging is a major pharmaceutical packaging market challenge. Counterfeiting poses a higher risk in the pharmaceutical supply chain, endangering consumer safety and causing financial harm to both pharmaceutical and packaging companies. It also has the potential to damage brand reputation due to the negative effects of counterfeit drugs. The complexity of the global pharmaceutical supply chain, with its many intermediaries, increases the likelihood of original products being stolen or replaced with fake ones before reaching consumers.

To mitigate the risk of counterfeiting, the US government implemented the Drug Quality and Security Act in 2013. This act aims to establish complete traceability for pharmaceutical products by 2023. Serialization will be implemented across the supply chain to enhance the efficiency of the traceability system, enabling pharmaceutical manufacturers, hospitals, and pharmacies to track prescription drugs throughout the supply chain. Still, instances of fake or counterfeit products entering the supply chain during reverse logistics operations have been reported, which may impact market growth in the forecast period.

The market share growth by the rigid plastic segment will be significant during the forecast period. Rigid plastic bottles are commonly made from polyethylene polymer and can be customized to various specifications. Rigid plastic packaging products are mainly used for packaging over-the-counter drugs such as oral drugs and tablets. Such factors will increase segment growth during the forecast period.

Get a glance at the market contribution of the End User segment Request Free Sample

The rigid plastic segment was valued at USD 27,276.09 million in 2017 and continued to grow by 2021. Rigid plastic packaging includes plastic bottles, caps, closures, and other uses. Plastic bottles can protect the medicinal properties of the packaged product when it is exposed to the outside environment in the supply chain. Moreover, countries in APAC are expected to witness significant growth in terms of over-the-counter drug sales due to rising self-medication knowledge among the population. For example, over-the-counter drug sales in India are expected to reach USD 6 billion by 2023. Rising sales of over-the-counter drugs are expected to boost the demand for rigid pharmaceutical plastic packaging during the forecast period.

Based on the product analysis, plastic bottles hold the largest market share. Pharmaceutical products are commonly packaged in plastic bottles made of polyethylene and polypropylene. These bottles serve as primary packaging for solid, liquid, and semi-liquid medications. The demand for plastic bottles is rising because they eliminate the need for additional packaging layers and ensure the safety of pharmaceutical products throughout the supply chain.

The increasing demand for syrups, ophthalmic, and nasal medicines, which are commonly packaged in plastic bottles, drives the demand for pharmaceutical packaging using this material. This is attributed to the growing prevalence of dry eye caused by prolonged exposure to smart devices like laptops and smartphones. However, the segment's growth may be hindered by environmental concerns as plastic materials are non-degradable. To address sustainability concerns, pharmaceutical manufacturers are increasingly focusing on adopting alternative packaging solutions that are more environmentally friendly, moving away from plastic materials.

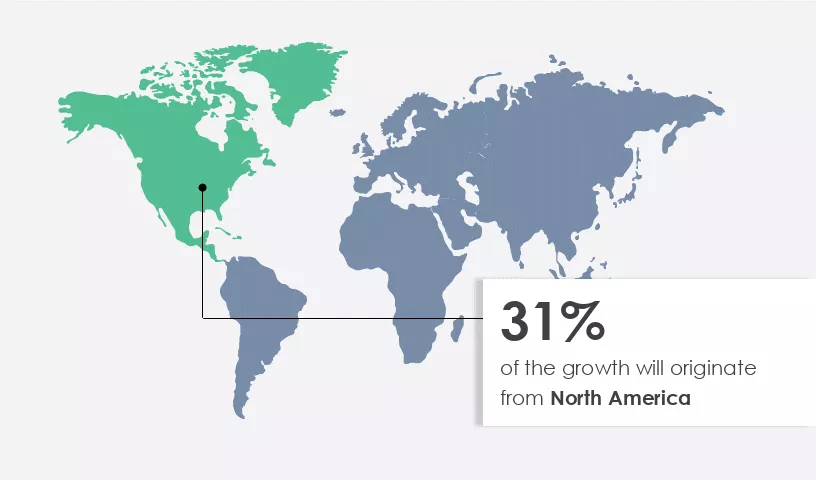

North America is estimated to contribute 31% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The US is the major contributor to the North American pharmaceutical packaging market, driven by factors such as growing healthcare spending, a rising aging population, and the increasing value of pharmaceutical exports. Established players like Johnson & Johnson, Pfizer, Abbot Laboratories, and Bristol Myers Squibb dominate the US pharmaceutical industry. Government healthcare insurance programs and the intellectual property system supporting sales of patented drugs attract venture capital investments. The region's demand for pharmaceutical packaging is also fueled by regulatory standards for senior-friendly packaging and the shift towards alternative materials like metal and glass. The growing elderly population further propels the market, with projections indicating over 78 million elderly individuals in the US by 2035.

The COVID-19 outbreak positively impacted the demand for pharmaceutical packaging in North America, as the pharmaceutical supply chain experienced increased demand due to the pandemic. The need for high-quality medical facilities and medicines boosted the demand for pharmaceutical packaging in the region. This trend is expected to continue, driven by the rising number of COVID-19 deaths and the initiation of vaccination drives, leading to increased production activities and demand for pharmaceutical packaging solutions.

Companies are implementing various strategies by analyzing factors such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product or service launches, to enhance their presence in the market.

Winpak- The company offers pharmaceutical packaging solutions such as Injectapak.

The report also includes detailed analyses of the competitive landscape of the market and information about 15 market companies, including:

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

The pharmaceutical packaging market research report forecasts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and growth opportunities from 2017 to 2027.

|

Pharmaceutical Packaging Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

182 |

|

Base year |

2022 |

|

Historic period |

2017-2021 |

|

Forecast period |

2023-2027 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.44% |

|

Market growth 2023-2027 |

USD 48,889.6 million |

|

Market structure |

Fragmented |

|

YoY growth 2022-2023(%) |

6.8 |

|

Regional analysis |

North America, Europe, APAC, Middle East and Africa, and South America |

|

Performing market contribution |

North America at 31% |

|

Key countries |

US, Canada, China, UK, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Amcor Plc, AptarGroup Inc., Ball Corp., Berry Global Inc., Becton Dickinson and Co., Constantia Flexibles Group GmbH, Datwyler Holding Inc., Gerresheimer AG, International Paper Co., Jabil Inc., James Alexander Corp., KP Holding GmbH and Co. KG, Nipro Corp., O I Glass Inc., SCHOTT AG, Vitro S.A.B. de C.V., West Pharmaceutical Services Inc., WestRock Co., Winpak Ltd., and Catalent Inc. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID 19 impact and recovery analysis and future consumer dynamics, Market condition analysis for forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this report to meet your requirements. Get in touch

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Material

7 Market Segmentation by Product

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights