Enjoy complimentary customisation on priority with our Enterprise License!

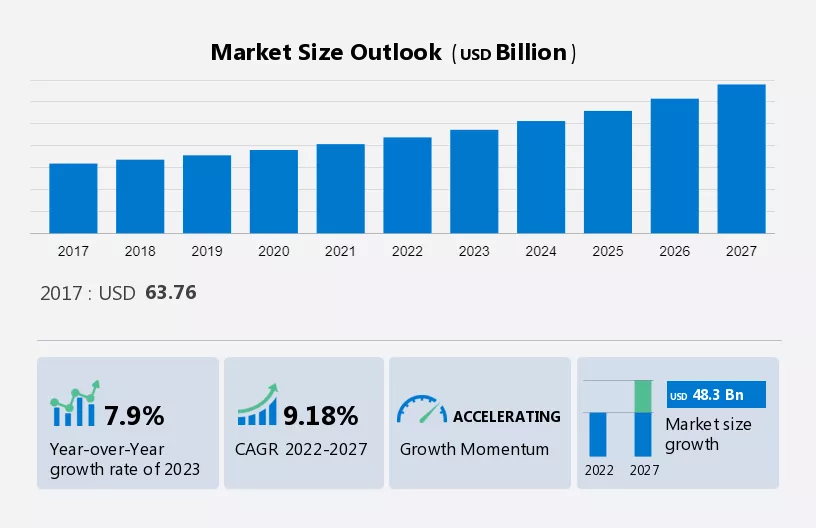

The in-vitro diagnostics instruments market size is estimated to increase by USD 48.3 billion, at a CAGR of 9.18% between 2022 and 2027. The growth of the market depends on several factors, including the growing geriatric population, demand for personalized medicines, and product launches.

To learn more about this report, Download Report Sample

Our researchers analyzed the data with 2022 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The growing geriatric population is the key factor driving the global market growth. Owing to the absence of physical activity and improper diet, people across the world are experiencing adverse effects on their health, which leads to major medical problems. These medical problems are more prevalent among the geriatric population than in the younger population. The geriatric population is increasing significantly across the world.

The rise in the aging population has resulted in increased expenditure on healthcare, including health check-ups, disease diagnosis, and treatment. The common health problems affecting older adults include Alzheimer’s disease, CVDs, bone and joint diseases, and diabetes. The elderly population requires diagnostic testing regularly due to their low immunity and metabolism. These factors have increased the demand for in-vitro diagnostic (IVD) instruments, as these instruments assist in disease diagnosis.

The potential opportunities for physician office laboratories (POLs) will fuel the global IVD instruments market growth. Across the world, there is no uniformity or support for the use of decentralized IVD testing in primary and outpatient care. This testing is more often performed in POLs. Reimbursement organizations, regulators, and healthcare administrators need to address the importance of POL testing, as the technical capabilities of portable IVD instruments are rising. This situation presents clinicians with several options for in-house testing.

The POL test segment is related to actionable infectious disease markers, cardiovascular diseases, and diabetes care. Testing for the most common infectious diseases has enabled the use of molecular diagnostic instruments in POLs. While Clinical Laboratory Improvement Amendments (CLIA)-approved testing using molecular assays will drive market growth, certain regulatory aspects of CLIA-waived testing will affect its growth. The overall growth of POL testing is expected to propel the average growth of the market during the forecast period.

Limited laboratory budgets and declining reimbursements that affect instrument sales are major challenges to the global IVD instruments market growth. Reimbursement policies for diagnostic testing are not the same across different geographic regions, and they are witnessing a downward trend. Hospitals and diagnostic laboratories that are the primary end-users of IVD instruments have been compelled to reduce their expenditure on IVD instruments to ensure that they can break even or earn profits.

End-users like clinical laboratories are facing workforce shortages as well as frequent visits to the doctor by patients who have lost their health insurance cards. These factors have led clinical laboratories to find alternative ways to maintain revenue despite limited casualty and testing volumes. IVD instrument manufacturing companies have recognized slow growth in developed nations, which has led them to focus on emerging markets and opt for strategies according to the market scenario. Such factors are likely to restrict the growth of the global IVD instruments market during the forecast period.

The report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates?in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Global In-vitro Diagnostics Instruments Market Customer Landscape

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Abbott Laboratories - The company offers in-vitro diagnostics instruments that can detect diseases, conditions, and infections from samples such as blood or tissue that have been taken from the human body.

The market report also includes detailed analyses of the competitive landscape of the market and information about 15 market companies, including:

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

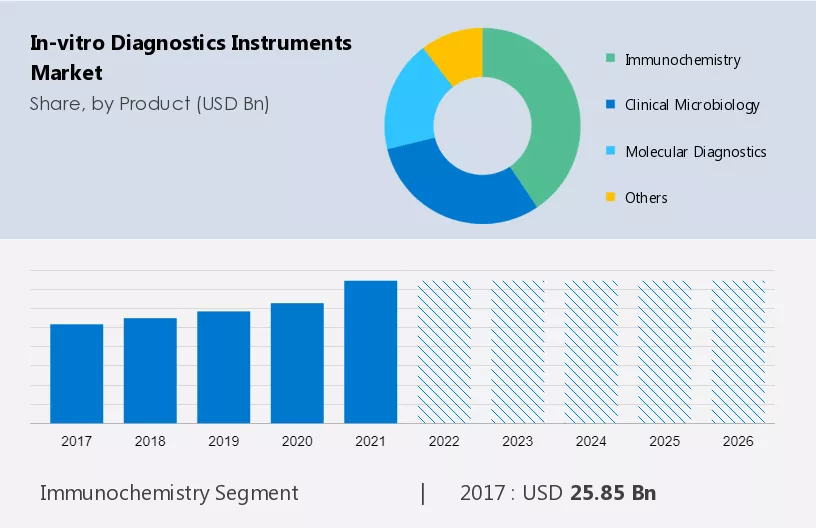

The market share growth by the immunochemistry segment will be significant during the forecast period. This segment is a highly automated segment in clinical laboratories and accounts for the highest test volume when compared with the other types of IVD testing instruments. The demand for immunochemistry analyzers is declining in the US and, to a certain extent, in Europe. The consolidation of laboratories in France and late reimbursements, especially in Italy, Spain, and Portugal, are some of the factors responsible for the low demand for immunochemistry analyzers in Europe. Despite the increasing number of patients with Type II diabetes, significant reductions in expenditure have been noted, not only in the UK but also in France and Germany.

Get a glance at the market contribution of various segments View PDF Sample

The immunochemistry segment showed a gradual increase in market share from USD 25.85 billion in 2017 and continued to grow by 2021. In China and India, there has been a rise in the number of rural hospitals that lack basic diagnostics laboratory infrastructure. This represents a growth opportunity for affordable immunochemistry analyzers. More than 80 different models of immunoassay analyzers are available in the market, which provides end-users with various options as per their requirements. To face and survive in the intensely competitive market, manufacturers reduce product cycles with new product launches or upgrade their existing analyzers.

For more insights on the market share of various regions View PDF Sample now!

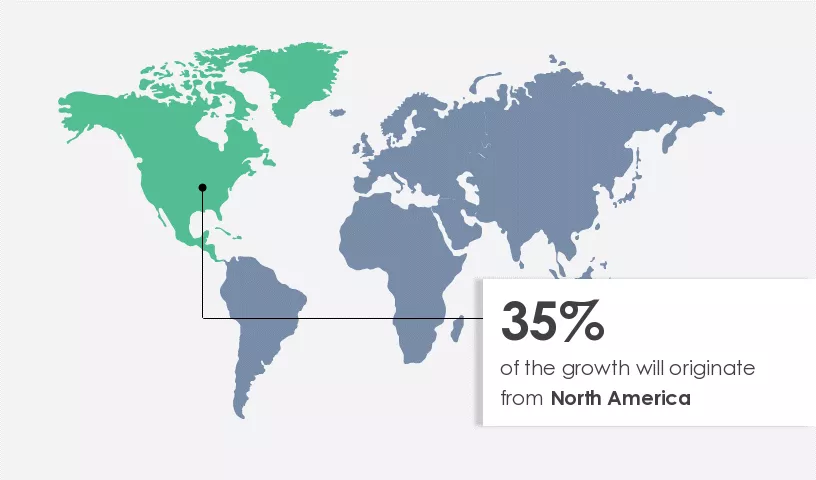

North America is projected to contribute 35% by 2027. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The US has the largest market share in terms of the sales of IVD instruments in North America. The IVD instruments market in North America is witnessing significant growth, primarily because of the growing aging population as well as the high prevalence of chronic and infectious diseases. This has raised the demand for diagnostic products and services in this region.

The Market report forecasts have a detailed analysis of growth by revenue at global, regional & country levels and provide an analysis of the market growth and trends opportunities from 2017 to 2027.

The market plays a crucial role in the healthcare industry, providing essential medical devices for diagnosing diseases and monitoring patient health. These instruments encompass a wide range of diagnostic tests and laboratory equipment, including clinical chemistry analyzers, immunoassay systems, hematology analyzers, and microbiology instruments. Additionally, point-of-care testing devices offer rapid and convenient diagnostics at the patient's bedside. Advanced technologies such as molecular diagnostics instruments enable precise genetic testing and personalized medicine. Other instruments like blood gas analyzers, urinalysis instruments, and coagulation analyzers provide critical data for patient management. With innovations in microplate readers, flow cytometers, and electrophoresis instruments, the market continues to evolve, supporting advancements in histology, cytology, and pathology.

|

In-vitro Diagnostics Instruments Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

180 |

|

Base year |

2022 |

|

Historic period |

2017-2021 |

|

Forecast period |

2023-2027 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 9.18% |

|

Market growth 2023-2027 |

USD 48.3 billion |

|

Market structure |

Fragmented |

|

YoY growth (%) |

7.9 |

|

Regional analysis |

North America, Europe, Asia, and Rest of World (ROW) |

|

Performing market contribution |

North America at 35% |

|

Key countries |

US, Canada, Germany, UK, and China |

|

Competitive landscape |

Leading companies, Market Positioning of companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Abbott Laboratories, Beijing Leadman Biochemistry Technology Co. Ltd., bioMerieux SA, Biosino Bio Technology and Science Inc., CPC Diagnostics Pvt Ltd., DAAN Gene Co. Ltd., Danaher Corp., F. Hoffmann La Roche Ltd., Guangzhou Wondfo Biotech Co. Ltd., Myriad Genetics Inc., Ortho Clinical Diagnostics, Shanghai Kehua Bio Engineering Co. Ltd., Shenzhen Mindray BioMedical Electronics, Siemens AG, and Thermo Fisher Scientific Inc. |

|

Market dynamics |

Parent market analysis, Market Forecasting, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for the forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this report to meet your requirements. Get in touch

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Product

7 Market Segmentation by End-user

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights