Green Data Center (GDC) Market Size 2026-2030

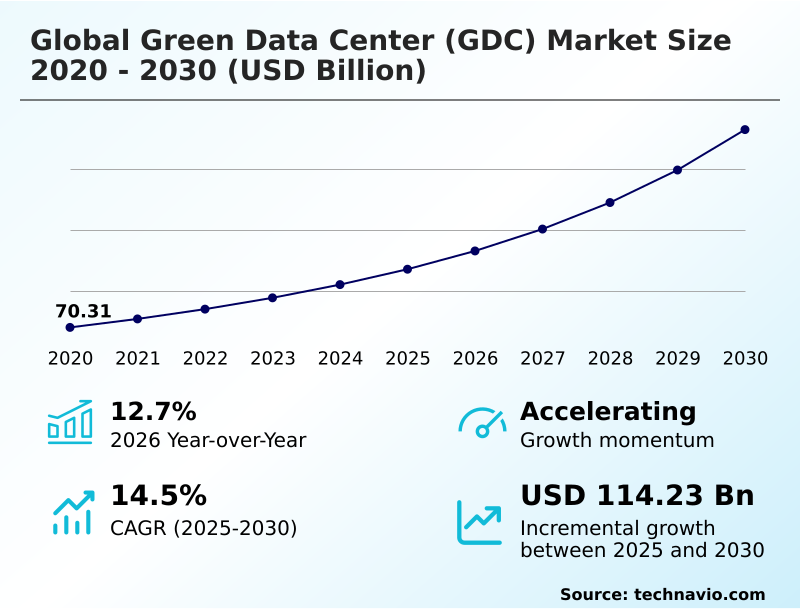

The green data center (gdc) market size is valued to increase by USD 114.23 billion, at a CAGR of 14.5% from 2025 to 2030. Increase in electricity consumption is augmenting market growth will drive the green data center (gdc) market.

Major Market Trends & Insights

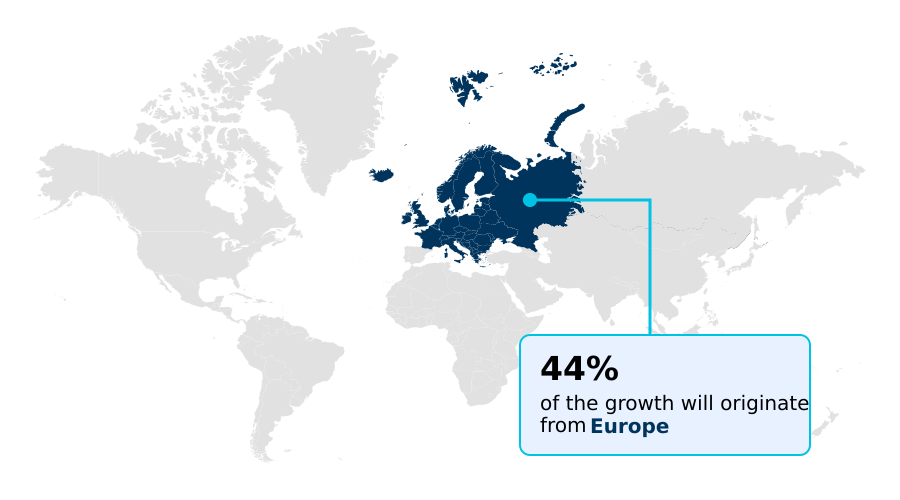

- Europe dominated the market and accounted for a 44.4% growth during the forecast period.

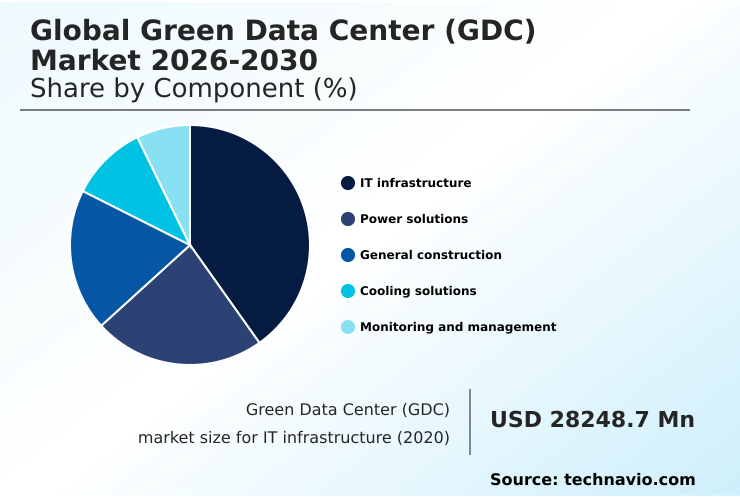

- By Component - IT infrastructure segment was valued at USD 43.51 billion in 2024

- By End-user - BFSI segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 161.83 billion

- Market Future Opportunities: USD 114.23 billion

- CAGR from 2025 to 2030 : 14.5%

Market Summary

- The green data center (GDC) market is expanding as organizations prioritize sustainability and energy efficiency in their digital infrastructure. This market focuses on developing and operating data centers that minimize environmental impact through optimized energy consumption, reduced carbon emissions, and the use of renewable energy sources.

- The rising demand for cloud computing, big data analytics, and digital services has accelerated the need for efficient data storage and processing solutions, positioning green data centers as a key alternative to conventional facilities. A key driver is the growing emphasis on environmental responsibility, with regulatory frameworks encouraging the adoption of energy efficient servers, advanced cooling systems, and intelligent power management technologies.

- For example, a financial services firm migrating to a green data center can meet its ESG targets while reducing operational expenses through lower energy bills and improved power usage effectiveness (PUE). Technological advancements, including virtualization and AI-driven energy optimization, are further enhancing resource utilization.

- Despite challenges like high initial investment, the market is set to play a crucial role in supporting sustainable digital growth.

What will be the Size of the Green Data Center (GDC) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Green Data Center (GDC) Market Segmented?

The green data center (gdc) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

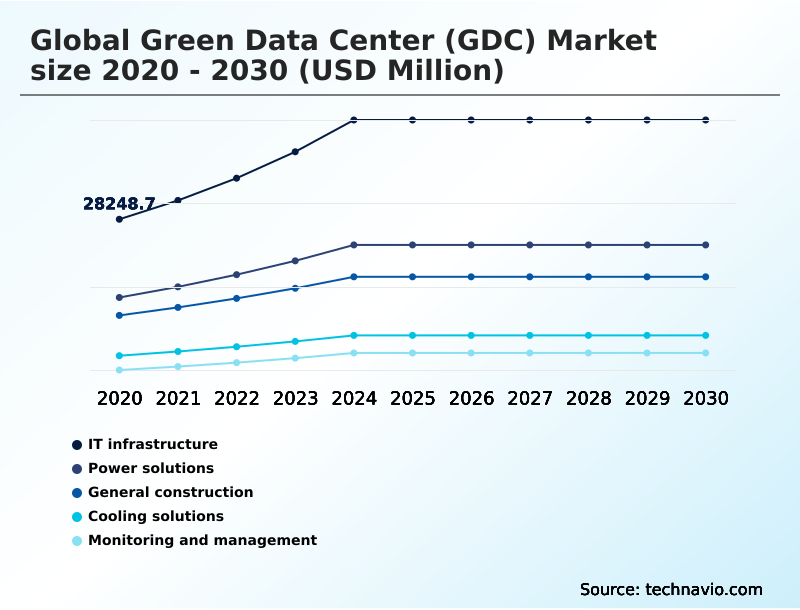

- IT infrastructure

- Power solutions

- General construction

- Cooling solutions

- Monitoring and management

- End-user

- BFSI

- Energy

- IT and telecom

- Others

- Type

- Hyperscale data centers

- Colocation data centers

- Enterprise data centers

- Geography

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- Europe

By Component Insights

The it infrastructure segment is estimated to witness significant growth during the forecast period.

The IT infrastructure segment is fundamental to the green data center market, focusing on hardware that minimizes energy consumption. This includes high-efficiency servers, advanced storage arrays, and low-power networking equipment, which are crucial for achieving ambitious sustainability goals.

The adoption of energy-efficient infrastructure and high-density computing designs allows operators to handle complex workloads, such as AI and big data analytics, without a proportional increase in electricity demand, improving performance per watt by up to 25%.

Key elements like high-voltage direct current (HVDC) power distribution, solid-state drives, and intelligent energy management are becoming standard.

This shift toward sustainable materials and ecofriendly building designs supports the broader goal of creating a resilient and low-carbon digital economy by addressing both operational and embodied carbon reduction.

The IT infrastructure segment was valued at USD 43.51 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

Europe is estimated to contribute 44.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Green Data Center (GDC) Market Demand is Rising in Europe Get Free Sample

The market's geographic landscape is characterized by distinct regional priorities. Europe leads in regulatory-driven adoption, with its focus on circular economy principles and waste heat reuse.

In contrast, North America's expansion is fueled by hyperscalers investing in large-scale renewable energy integration and high-performance computing (HPC). APAC is a high-growth region where climate-adapted infrastructure is essential for operating in tropical environments, driving innovation in advanced cooling technologies.

Operators in this region are achieving PUE ratings as low as 1.2 by deploying specialized thermal management systems.

The market in Europe is expanding at a rate approximately 15% higher than in the Middle East and Africa, driven by stringent energy intensity reporting mandates.

The adoption of modular construction and rainwater harvesting systems is also gaining traction globally to enhance sustainability.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Achieving sustainability in the digital age requires a multifaceted approach, starting with reducing the embodied carbon of the digital backbone through sustainable procurement. A key focus is managing heat loads from high-density computing, where optimizing cooling and energy efficiency becomes paramount. For facilities operating data centers in tropical climates, specialized designs are crucial.

- Success hinges on balancing workloads for improved efficiency, which directly contributes to achieving low power usage effectiveness ratings. Forward-thinking operators are reusing waste heat for district heating, creating a circular energy model. Many are deploying AI for facility operations management to automate and refine performance, including using AI for predictive energy adjustments.

- In water-scarce areas, managing water stress in arid regions is a critical operational constraint, often addressed by minimizing water consumption with closed-loop cooling. Retrofitting legacy sites for energy efficiency offers a path to modernization, while new builds are implementing modular data center designs and implementing sustainable building materials in construction.

- Integrating on-site renewable energy generation is a core strategy, complemented by using AI-driven workload management. A key metric of success is aligning data center operations with compliance, which can reduce risks. Furthermore, reducing transmission losses with HVDC and improving power usage with virtualization are vital technical tactics.

- Finally, tracking environmental metrics with DCIM software provides the necessary data for continuous improvement, with some facilities reporting a 15% greater workload density compared to traditional designs.

What are the key market drivers leading to the rise in the adoption of Green Data Center (GDC) Industry?

- The increase in electricity consumption is a key driver augmenting market growth by accelerating the shift toward energy-efficient infrastructure.

- Market growth is fundamentally driven by the rising need for energy-optimized systems to counteract increasing electricity consumption and costs. As digital services expand, the demand for sustainable infrastructure that meets stringent carbon reduction targets is intensifying.

- A surge in data center standards is compelling organizations to adopt low-emission operations and energy-efficient technologies, with adherence to new standards often reducing carbon-related fees by over 10%.

- This push for compliance-driven infrastructure is accelerating investment in renewable energy and carbon accounting tools.

- The rising need for high computational performance without a corresponding increase in environmental impact is making technologies like free cooling and efficient chiller systems essential for new builds and retrofits, supporting long-term sustainability goals.

What are the market trends shaping the Green Data Center (GDC) Industry?

- The increased use of data center infrastructure management (DCIM) and automation is an emerging trend. It enables real-time monitoring and optimization of energy and operational performance.

- Key trends are reshaping operational models, with a strong emphasis on automation and resource management. The increased use of predictive control systems and AI-driven thermal optimization enables facilities to dynamically adjust to workloads, improving energy utilization by up to 20%.

- As high-density hardware becomes common, rising water consumption from traditional water-based cooling methods is a significant concern, driving the adoption of more sustainable alternatives. Innovations in rear door heat exchangers and closed-loop liquid cooling are becoming critical. Furthermore, the expansion of operations into tropical climates is fostering innovation in climate-adapted infrastructure, where specialized cooling solutions are necessary to maintain performance.

- This trend pushes the industry toward more efficient and resilient designs tailored to challenging environmental conditions, ensuring both sustainability and operational continuity.

What challenges does the Green Data Center (GDC) Industry face during its growth?

- The high cost associated with constructing green data centers is a key challenge affecting industry growth.

- Significant challenges persist, primarily centered on high upfront costs and the need for specialized expertise. The capital expenditure for building green data centers can be 15-25% higher than for traditional facilities, creating a barrier for many organizations.

- This is compounded by the high operational expenses and complexity involved in retrofitting existing data centers with modern technologies like flexible loads or district heating programs. A lack of expertise in areas such as grid frequency regulation and sustainable infrastructure design slows adoption and can lead to suboptimal performance.

- Overcoming these hurdles requires not only financial investment but also a commitment to developing a skilled workforce capable of managing sophisticated, energy-efficient systems.

Exclusive Technavio Analysis on Customer Landscape

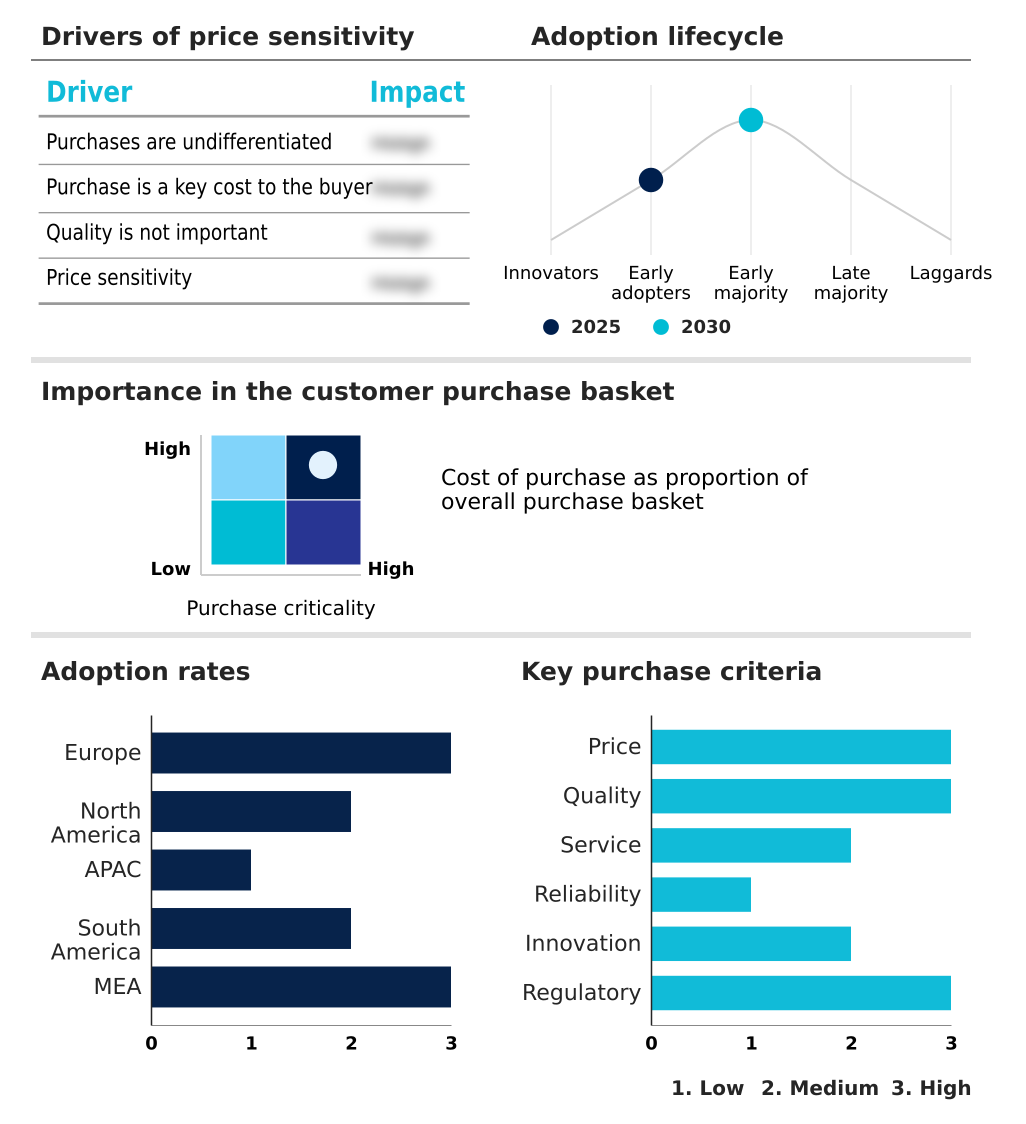

The green data center (gdc) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the green data center (gdc) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Green Data Center (GDC) Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, green data center (gdc) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - Delivering GDC solutions with energy-efficient power distribution and digital management to cut electrical losses and carbon emissions for hyperscale facilities.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Amazon.com Inc.

- Daikin Industries Ltd.

- Delta Electronics Inc.

- Digital Realty Trust Inc.

- Eaton Corp. Plc

- Equinix Inc.

- GE Vernova Inc.

- Google LLC

- Green Revolution Cooling Inc.

- Hitachi Energy Ltd.

- Iron Mountain Inc.

- LiquidStack BV

- LITE ON Technology Corp.

- Meta Platforms Inc.

- Microsoft Corp.

- Mitsubishi Heavy Industries

- Schneider Electric SE

- Submer Technologies SL

- Vertiv Holdings Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Green data center (gdc) market

- In June 2025, Google LLC announced an expansion of its next-generation data center facilities, focusing on advanced energy-efficient architecture and carbon-free energy sourcing across multiple operational regions.

- In May 2025, Dell Technologies is scheduled to release an expanded line of servers featuring modular, circular design components that utilize 50% recycled content, significantly reducing the embodied carbon of the digital backbone.

- In February 2025, Schneider Electric announced the widespread deployment of its new dielectric immersion cooling pods, which allow for the operation of high-density hardware without the need for massive mechanical chillers.

- In January 2025, Vertiv introduced an upgraded modular power platform designed for sustainable facilities, utilizing lithium-ion battery storage to provide better energy density and longer lifecycles than traditional lead-acid alternatives.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Green Data Center (GDC) Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 318 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 14.5% |

| Market growth 2026-2030 | USD 114228.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 12.7% |

| Key countries | Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The green data center (GDC) market is defined by a continuous evolution toward greater efficiency and environmental stewardship, driven by technological innovation. Core to this transformation is the widespread adoption of virtualization and advanced cooling technologies to manage escalating thermal management challenges.

- The integration of data center infrastructure management (DCIM) software has become standard for AI-based energy monitoring and optimizing performance. Boardroom decisions increasingly center on the CAPEX of deploying technologies like liquid immersion cooling versus the long-term OPEX savings from enhanced power usage effectiveness. The use of high-efficiency power supply units and modular power platforms with lithium-ion battery storage is critical.

- Facilities are also leveraging digital twin technology to model and de-risk changes. Implementing high-voltage direct current (HVDC) distribution can reduce power conversion losses by over 5%, a significant factor in large-scale operations. This focus on intelligent energy management and workload consolidation is reshaping infrastructure strategy.

What are the Key Data Covered in this Green Data Center (GDC) Market Research and Growth Report?

-

What is the expected growth of the Green Data Center (GDC) Market between 2026 and 2030?

-

USD 114.23 billion, at a CAGR of 14.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (IT infrastructure, Power solutions, General construction, Cooling solutions, and Monitoring and management), End-user (BFSI, Energy, IT and telecom, and Others), Type (Hyperscale data centers, Colocation data centers, and Enterprise data centers) and Geography (Europe, North America, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

Europe, North America, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increase in electricity consumption is augmenting market growth, High cost of building green data center

-

-

Who are the major players in the Green Data Center (GDC) Market?

-

ABB Ltd., Amazon.com Inc., Daikin Industries Ltd., Delta Electronics Inc., Digital Realty Trust Inc., Eaton Corp. Plc, Equinix Inc., GE Vernova Inc., Google LLC, Green Revolution Cooling Inc., Hitachi Energy Ltd., Iron Mountain Inc., LiquidStack BV, LITE ON Technology Corp., Meta Platforms Inc., Microsoft Corp., Mitsubishi Heavy Industries, Schneider Electric SE, Submer Technologies SL and Vertiv Holdings Co.

-

Market Research Insights

- The market dynamics are increasingly shaped by the push for sustainable digital infrastructure, where AI-driven thermal optimization is critical for managing heat loads. Enterprises adopting compliance-driven infrastructure report a 10% improvement in audit readiness. The shift toward carbon-free energy sourcing is becoming a competitive differentiator, with early adopters seeing enhanced brand reputation.

- Organizations leveraging intelligent software platforms for workload balancing achieve up to a 15% reduction in wasted compute cycles. As sovereign AI models become more prevalent, the need for localized, efficient data processing powered by on-site renewable energy grows. This strategic alignment with carbon reduction targets and data sovereignty principles is redefining operational and investment priorities across the industry.

We can help! Our analysts can customize this green data center (gdc) market research report to meet your requirements.

RIA -

RIA -