Enjoy complimentary customisation on priority with our Enterprise License!

The absorption chillers market size is forecast to increase by USD 741.07 million, at a CAGR of 4.32% between 2022 and 2027. The market's expansion hinges on several factors, notably the increasing utilization of absorption chillers spanning diverse industries, the rising embrace of district heating and cooling infrastructures, and the strict regulations governing refrigerant usage. These elements collectively propel the market forward, with absorption chillers gaining prominence due to their energy-efficient and environmentally friendly operation. The adoption of district heating and cooling systems reflects a broader trend towards sustainable infrastructure solutions. However, challenges persist, particularly in navigating complex regulatory frameworks and ensuring compliance with evolving environmental standards, driving innovation and adaptation within the industry.

To learn more about this report, Download Report Sample

This report extensively covers market segmentation by application (industrial and HVAC), type (lithium bromide and ammonia), and geography (APAC, Europe, North America, Middle East and Africa, and South America). It also includes an in-depth analysis of drivers, trends, and challenges. Furthermore, the report includes historic market data from 2017 to 2021.

The market is driven by the need for efficient refrigeration systems that utilize various heat sources such as waste heat or natural gas to power the cooling process. Unlike conventional vapor compression chillers that rely solely on mechanical energy, absorption refrigeration systems use refrigerant vapor absorption into a liquid solution. This technology is gaining traction, especially in developing nations and the industrial sector, due to its higher Coefficient of Performance (COP) and reduced reliance on ozone-depleting chlorofluorocarbons (CFCs). However, challenges such as fluctuating electricity rates and the ongoing transition away from CFCs remain significant. Our researchers analyzed the data with 2022 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The growing use of absorption chillers across various industries is the key factor driving the global market growth. These chillers lodge a vital position in a heating, ventilation, air conditioning, and refrigeration (HVAC and R) system. It offers numerous benefits over conventional cooler, which majorly include the ability to integrate with combined heat and power (CHP) generation and district cooling infrastructure, low noise levels, and improved efficiency.

Moreover, these advantages have accelerated the adoption of these coolers among various industrial end-users. They help them to reduce their overall costs and enable them to meet their environmental targets. These factors make these coolers an appealing option in the industrial sector and allow many industrial users to meet their environmental and regulatory targets.

The availability of substitute chiller technologies is the primary trend in the global market growth. The competition from alternative chiller technologies will remain the biggest challenge for the market during the forecast period. Although conventional chiller technologies are not much energy efficient as these coolers which are used in conjunction with CHP, cogeneration, or waste heat, they have several other advantages, which are encouraging their adoption over these coolers.

Moreover, chiller manufacturers are also investing in the development of new chiller technologies, which enhance efficiency and reduce the environmental footprint of conventional coolers, to boost product adoption. The introduction of coolers, which can meet stringent environmental regulations, is expected to impact the market negatively during the forecast period.

High capital and maintenance costs are a major challenge to global market growth. Most of the energy-efficient HVAC and R technologies, including these coolers, are considerably more expensive than their conventional counterparts. Although they provide significant energy savings, the breakeven period for the return on initial investment can be significantly longer. The high cost of absorption coolers may be a major challenge for price-sensitive customers, especially in emerging economies.

Moreover, most of the industries and commercial businesses in developing countries, such as India and China, are extremely price-sensitive; therefore, they are more concerned about the initial cost of purchase. The annual cost of maintenance of these chillers is 20%-35% higher than the conventional coolers, which can add up to a significant amount over many years. Therefore, the relatively higher cost of these chillers is one of the key reasons that is expected to affect the market growth during the forecast period.

The report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Global Market Customer Landscape

Market players are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

BROAD Group - The company offers absorption chillers such as BDH Model, BDE Model, BDS Model.

The report also includes detailed analyses of the competitive landscape of the market and information about 15 market market players, including:

Qualitative and quantitative analysis of market players has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize market players as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize market players as dominant, leading, strong, tentative, and weak.

The market is segmented based on various factors such as the heat source utilized, the cooling process involved, and the type of refrigerant used. Refrigeration systems employing absorption refrigeration technology are preferred for their ability to utilize waste heat or natural gas as a primary heat source, unlike conventional vapor compression chillers that rely on mechanical energy. Industries in developing nations and those focusing on sustainability are increasingly adopting absorption chillers due to their higher Coefficient of Performance (COP), reduced greenhouse gas emissions, and the elimination of ozone-depleting chlorofluorocarbons (CFCs). These chillers find significant application in sectors such as the food and beverages industry, petrochemical industry, and various industrial processes. However, challenges persist in terms of fluctuating electricity rates and the need for efficient wastewater management in industrial sectors utilizing these chillers.

The market share growth by the industrial segment will be significant during the forecast period. Industrial Absorption chillers are deployed in the industrial sector to maintain the temperature of process equipment and refrigeration of chemicals, food, beverages, and other materials that need to be maintained at a low temperature. Industries such as plastic, chemical, pharmaceutical, oil and gas, food and beverages, and printing are some of the major industrial consumers that use chillers. These chillers can be directly integrated with the processes and can utilize the waste heat generated by the equipment.

Get a glance at the market contribution of various segments Request a PDF Sample

The industrial segment was valued at USD 2.08 billion in 2017 and continue to grow by 2021. The food and beverages industry is also expected to be a significant contributor to the demand for industrial absorption chillers. Factors such as the growth in global population, rise in per capita income, and changing consumer habits have played a significant role in increasing the demand for processed and packaged food products such as frozen foods, carbonated drinks, packed juices, alcoholic beverages, and bottled water. Absorption chillers are used for flash freezing, cooling, and chilling of food, food additives, beverages, and other chemicals in the food and beverages industry. Therefore, the growing consumption of processed foods, especially in developing countries, will drive the demand for industrial absorption chillers. Hence, such factors are fuelling the growth of this segment which in turn drives the market during the forecast period.

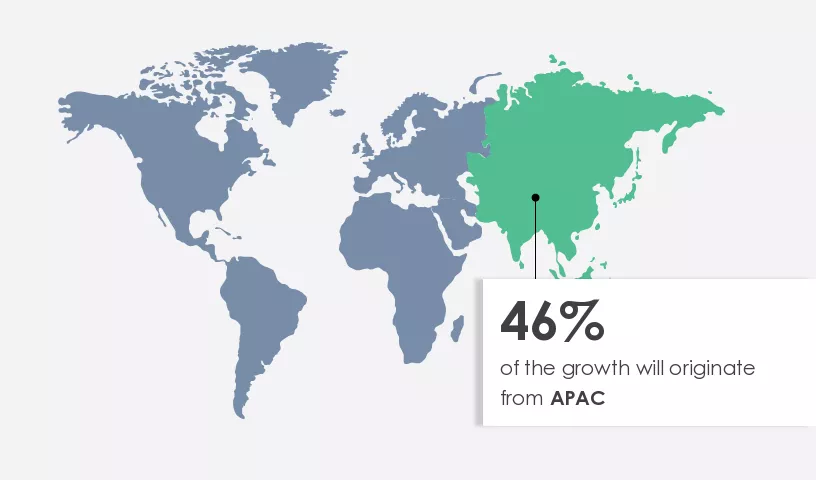

For more insights on the market share of various regions Request PDF Sample now!

APAC is estimated to contribute 46% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period. APAC is the largest market for absorption chillers due to huge demand from countries such as China, Japan, India, and several countries in Southeast Asia. Factors such as the rapid growth in population, rise in industrialization, growth in urbanization, and expansion in the number of large commercial establishments are driving the market growth in the region. The growth in commercial and residential constructions is a key driver for the demand for medium to large-scale heating, ventilation, air conditioning, and refrigeration (HVAC and R) systems in the region, which also drives the growth of the market. The adoption of green building initiatives in some countries, such as China and India, will be another factor that will drive the demand for absorption chillers in APAC.

The report forecasts market growth by revenue at global, regional & country levels and provides a market growth analysis of the latest market trends and growth opportunities from 2017 to 2027.

The market is influenced by a range of critical factors. As industries seek sustainable cooling solutions, absorption chillers gain traction due to their efficiency and eco-friendly operation, especially when powered by renewable energy sources like solar thermal energy and cogeneration systems. These chillers utilize low-grade heat sources and offer an alternative to conventional vapor compression chillers, significantly reducing greenhouse gas emissions and minimizing environmental impact. The rising demand for cooling in sectors such as the food and beverage industry, pharmaceuticals, and metal fabrication is driving the adoption of absorption refrigeration technologies.

Moreover, stringent energy efficiency regulations, coupled with sustainability initiatives and concerns about climate change, are encouraging industries to shift towards absorption refrigeration solutions. These systems leverage heat recovery and district cooling systems to optimize energy consumption and reduce electricity rates. Additionally, advancements in solar-powered absorption chillers and direct-fired absorption chillers are enhancing their efficiency and reliability in various applications, including commercial buildings, industrial facilities, and data centers. As the focus on carbon neutrality grows, absorption chillers play a pivotal role in achieving energy sustainability across diverse sectors, including power plants and the petrochemical industry.

Furthermore, the market is witnessing significant growth driven by various key factors. These chillers play a crucial role in refrigeration systems by utilizing mechanical energy or natural gas combustion to facilitate the cooling process. They operate by absorbing refrigerant vapor into a liquid solution, making them suitable for various industrial processes and applications in sectors like the pharmaceuticals industry, petrochemical industries, and metal fabrication industries. One of the standout features of absorption chillers is their use of non-ozone-depleting refrigerants, aligning with global efforts to reduce greenhouse gases and mitigate global warming potential (GWP) and ozone depletion potential (ODP). This makes them highly favored within the HVAC sector and among organizations striving for environmental sustainability.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

164 |

|

Base year |

2022 |

|

Historic period |

2017-2021 |

|

Forecast period |

2023-2027 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.32% |

|

Market growth 2023-2027 |

USD 741.07 million |

|

Market structure |

Fragmented |

|

YoY growth 2022-2023(%) |

3.78 |

|

Regional analysis |

APAC, Europe, North America, Middle East and Africa, and South America |

|

Performing market contribution |

APAC at 46% |

|

Key countries |

US, China, Japan, Germany, and UK |

|

Competitive landscape |

Leading market players, Market Positioning of market players, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

BROAD Group, Carrier Global Corp., Century Corp., CNIM SA, Daikin Industries Ltd., EAW Energieanlagenbau GmbH, Ebara Corp., Helioclim, Johnson Controls International Plc., Kirloskar Pneumatic Co. Ltd., LG Electronics Inc., Mitsubishi Heavy Industries Ltd., Robur Spa, Shuangliang Eco-Energy Systems Co. Ltd., THE PAR GROUP, Thermax Ltd., Trane Technologies plc, World Energy Co. Ltd., Yazaki Corp., and Berg Chilling Systems Inc. |

|

Market dynamics |

Parent market analysis, market research and growth, Market forecasting, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, and Market condition analysis for the forecast period. |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this report to meet your requirements. Get in touch

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Application

7 Market Segmentation by Type

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights