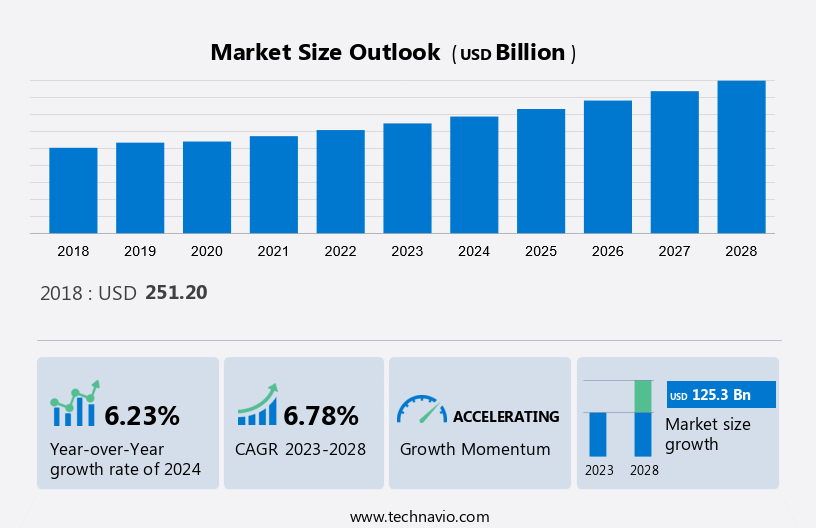

Active Electronic Components Market Size 2024-2028

The active electronic components market size is forecast to increase by USD 125.3 billion at a CAGR of 6.78% between 2023 and 2028. The market's growth is influenced by various factors, such as the rising demand for IoT devices, which drives the growth of semiconductors. Additionally, there's a growing need for renewable energy sources, further stimulating market expansion. These factors collectively contribute to the market's upward trajectory, reflecting the increasing reliance on IoT technologies and the shift towards sustainable energy solutions. Moreover, the proliferation of connected devices and the Internet of Things (IoT) has significantly increased the demand for semiconductor devices. This trend is expected to continue as more industries and applications adopt IoT platforms. Additionally, the growing focus on renewable energy sources to mitigate environmental concerns is driving the demand for energy-efficient semiconductor devices, further propelling market growth.

What will be the Size of the Active Electronic Components Market During the Forecast Period?

To learn more about this market report, View Report Sample

Active Electronic Components Market Segmentation

The market research report provides comprehensive data (region wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018 - 2022 for the following segments.

- End-user Outlook

- Consumer electronics

- Networking and telecommunications

- Automotive

- Manufacturing

- Others

- Product Outlook

- Semiconductor

- Vacuum tube

- Display devices

- Region Outlook

- North America

- The U.S.

- Canada

- Europe

- U.K.

- Germany

- France

- Rest of Europe

- APAC

- China

- India

- Middle East & Africa

- Saudi Arabia

- South Africa

- Rest of the Middle East & Africa

- North America

By End-User

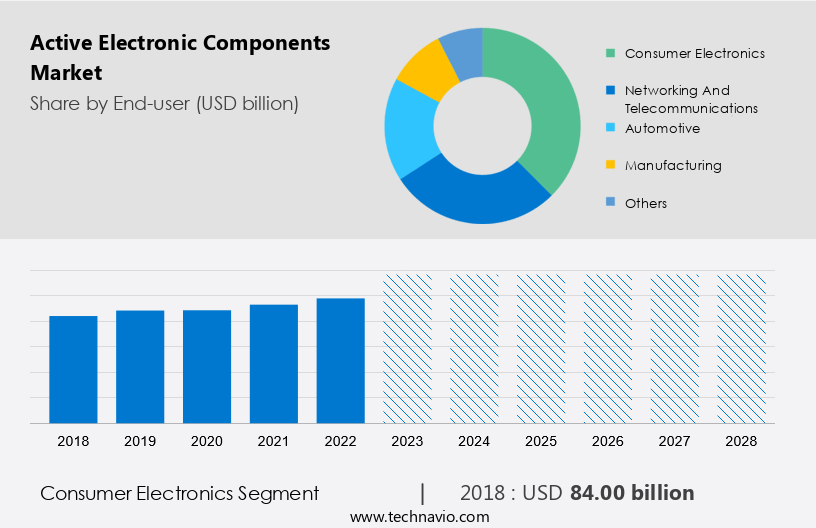

The market share growth by the consumer electronics segment will be significant during the forecast period. The market encompasses circuits that convert electrical input signals into functional outputs, utilizing electricity as an energy source. This market caters to various applications, including AC circuits and DC circuit in connected devices such as laptops, wearable devices, and industrial automation services. The healthcare industry and MEMS technology also benefit from these components, with semiconductors, diodes, transistors, and integrated circuits (ICs) being key players.

Get a glance at the market contribution of various segments. View PDF Sample

The consumer electronics segment was valued at USD 84 billion in 2018. In the automotive sector, ICs are integral to electric vehicles, autonomous vehicle technologies, parking assistance, safety airbags, telematics, navigation, and 5G infrastructure. The semiconductor segment, including electric insulators, conductors, and current flow, is essential for the functioning of electrical devices, solid-state storage, resistors, capacitors, and other electronic components. The market's growth is driven by consumer smartphone use, 5G services, and the increasing demand for advanced technologies in various industries. This, in turn, is likely to drive market expansion in the consumer electronics segment throughout the forecast period.

Regional Analysis

For more insights on the market share of various regions, Download PDF Sample now!

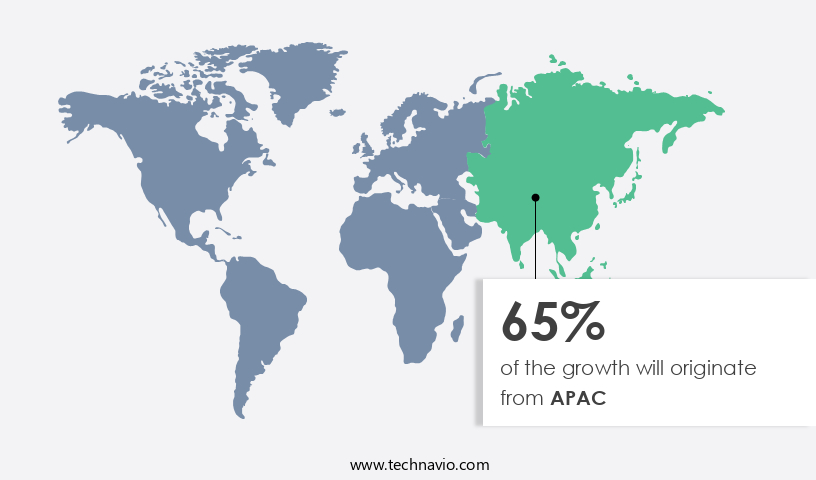

APAC is estimated to contribute 65% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period. The market in the Asia Pacific region is projected to experience significant growth, driven by increasing demand from industries such as consumer electronics & computing, automotive, aerospace, medical, industrial, and communications. Key end-use products include mobile phones, audio players, wireless routers, and various electronic equipment. NXP Semiconductors and other semiconductor companies are major contributors to this market. The growth is fueled by the expanding consumer base and rising disposable income in developing countries like China and India. This leads to increased demand for electronic devices, including computing components, ICs, amplifiers, and other components like vacuum tubes, inductors, and sensing devices.

Key raw materials include silicon, iron, nickel, molybdenum, and precious metals like palladium and ruthenium. The market is also influenced by digitalization, connectivity, mobility, and miniaturization trends. However, raw materials prices, supply chain issues, and the availability of alternative technologies may pose challenges. Additionally, advancements in technology bring innovations like electrochemical transistors, modular architecture, and amplifiers, further expanding the market scope. Throughout the projected period, APAC is expected to further improve its position in global automobile manufacturing, which is expected to fuel market expansion in the region.

Active Electronic Components Market Dynamics

The market encompasses a wide range of electrical devices that convert electrical input signals into various forms of energy or power. These are essential in AC and DC circuits, powering connected devices such as laptops, wearable devices, and autonomous vehicle development platforms. The electricity source can be derived from various energy sources, including 5G infrastructure and semiconductor segments like ICs. They include insulators, conductors, and electronic components like ICs, which facilitate current flow and enable the functioning of electrical devices. These are integral to numerous applications, including parking assistance, safety airbags, telematics, navigation, and consumer smartphone use. Solid-state storage technologies like mobile phones and audio players also rely on active electronic components for their operation. The market is expected to grow significantly due to the increasing demand for advanced electrical devices and the development of new technologies like 5G infrastructure and autonomous vehicles.

Our researchers analyzed the data with 2022 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Key Market Driver

The growth of the semiconductor industry is notably driving the demand for active electronic components. The Market encompasses circuits that respond to electrical input signals and convert electricity into various forms, such as AC and DC circuits. IoT devices, including laptops, wearable gadgets, and industrial automation systems, rely on these components for power and voltage regulation. MEMS technology, semiconductors, diodes, transistors, and integrated circuits (ICs) are integral to this market.

In the healthcare industry, ICs power medical equipment, while in the automotive sector, they enable features like parking assistance, safety airbags, telematics, navigation, and autonomous vehicle technologies. The semiconductor segment, including insulators, conductors, and current flow components like resistors and capacitors, plays a crucial role in this market's growth. The consumer electronics sector, including smartphones, and 5G infrastructure development further fuel the demand for these components. Automotive manufacturers and smart connected automobiles are significant consumers of ICs in the automotive industry. Thus, these factors drive the growth of the market during the forecast period.

Significant Market Trend

The growing investments in smart city projects are a new trend in the market. The electrical components market encompasses various technologies, including circuits, that facilitate the efficient flow of electricity in AC and DC circuits. These components are integral to powering connected devices, such as laptops, wearable devices, and industrial automation systems, in the smart city landscape. MEMS technology, semiconductors, diodes, transistors, and integrated circuits (ICs) are key components in this market.

The semiconductor segment, specifically ICs, plays a significant role in powering applications in the healthcare industry, electric vehicles, and autonomous vehicle technologies, such as parking assistance, safety airbags, telematics, navigation, and consumer smartphone use. The 5G infrastructure expansion fuels the demand for these components in the automotive industry, driving the development of smart connected automobiles. Resistors, capacitors, and other passive components, such as insulators and conductors, are also essential in managing current flow and energy storage in electrical devices. Furthermore, developing countries have made major investments in smart city projects, which further drive the demand for active electronic components. Thus, these factors drive the growth of the market during the forecast period.

Major Market Challenge

Increases in design complexity due to miniaturization are the major challenges that may hinder market growth during the forecast period. In the dynamic electronic components market, manufacturers face intense price competition due to the abundance of suppliers offering comparable products. This pressure to set competitive prices while maintaining long-term profitability necessitates careful consideration of various factors, including raw material costs, research and development expenses, marketing budgets, and overheads.

Furthermore, pricing components too low can result in unsustainable profit margins, while failing to price competitively may lead to lost business. Key players in this market include components used in circuits that process electrical input signals, such as AC and DC circuits, which power connected devices like laptops, wearable devices, and industrial automation systems. The healthcare industry, semiconductor segment, and automotive sector heavily rely on these components, including MEMS technology, diodes, transistors, integrated circuits, and insulators or conductors. Current flow is facilitated through various electrical devices, such as resistors, capacitors, and Integrated Circuits (ICs). The market encompasses components for various applications, including electric vehicles, autonomous vehicle technologies, parking assistance, safety airbags, telematics, navigation, consumer smartphone use, 5G infrastructure, and smart connected automobiles. Semiconductor segment components, such as ICs, are essential for solid-state storage and various applications, including insulators, conductors, current flow, and electrical devices. This challenge is expected to hinder the growth of the market focus during the forecast period.

Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market growth analysis report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth and forecasting strategies.

Market Customer Landscape

Key Active Electronic Components Market Companies

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Advanced Micro Devices Inc.- The company offers active electronic components such as microprocessors, motherboard chipsets, embedded processors, and graphics processors.

The market research and growth report also includes detailed analyses of the competitive landscape of the market and information about 15 market companies, including:

- Analog Devices Inc.

- Broadcom Inc.

- Diotec Semiconductor AG

- Everlight Electronics Co. Ltd.

- Infineon Technologies AG

- Intel Corp.

- KYOCERA Corp.

- Microchip Technology Inc.

- Monolithic Power Systems Inc.

- Murata Manufacturing Co. Ltd.

- NXP Semiconductors NV

- ON Semiconductor Corp.

- Panasonic Holdings Corp.

- Qualcomm Inc.

- Renesas Electronics Corp.

- STMicroelectronics International N.V.

- Texas Instruments Inc.

- Toshiba Corp.

- Vishay Intertechnology Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Latest Market Developments and News

-

In November 2024, Texas Instruments introduced a new series of active electronic components designed to improve the performance of electric vehicles (EVs). These components focus on enhancing power management and battery efficiency, addressing the growing demand for energy-efficient solutions in the automotive sector.

-

In October 2024, Analog Devices launched a next-generation power amplifier aimed at 5G applications. The new component features advanced signal processing capabilities to support the high-speed data transmission required for 5G networks, catering to the increasing demand for efficient active components in telecommunications.

-

In September 2024, Infineon Technologies unveiled a new range of microcontrollers designed for industrial automation systems. These active components focus on improving processing power and connectivity, responding to the growing demand for smarter and more efficient automation solutions in various industries.

-

In August 2024, NXP Semiconductors introduced a new series of integrated circuits (ICs) optimized for automotive safety applications. These ICs are designed to enhance in-vehicle electronics systems, meeting the rising demand for advanced safety features in modern vehicles.

Market Analyst Overview

The market is a significant segment in the electronics industry, featuring various types of components such as circuits, integrated circuits (ICs), resistors, capacitors, diodes, and transistors. These components play a crucial role in converting, regulating, and transmitting electrical energy into various forms. The market is driven by the increasing demand for advanced technology in various sectors like telecommunications, automotive, consumer electronics, and industrial automation. The semiconductor industry, in particular, is experiencing rapid growth due to the development of microelectromechanical systems (MEMS) and the Internet of Things (IoT). Power electronics, a sub-segment of active electronic components, is gaining popularity due to the rising demand for energy-efficient solutions.

Furthermore, the market is expected to grow significantly due to the increasing adoption of renewable energy sources and electric vehicles. The market for active electronic components is competitive, with key players including Texas Instruments, Infineon Technologies, STMicroelectronics, and Analog Devices. These companies invest heavily in research and development to stay ahead of the competition and meet the evolving demands of their customers. In conclusion, the market is a dynamic and growing industry driven by advancements in technology and the increasing demand for energy-efficient solutions. The market is competitive, with key players investing heavily in research and development to meet the evolving demands of their customers.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

193 |

|

Base year |

2023 |

|

Historic period |

2018 - 2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.78% |

|

Market growth 2024-2028 |

USD 125.3 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.23 |

|

Regional analysis |

APAC, North America, Europe, South America, and Middle East and Africa |

|

Performing market contribution |

APAC at 65% |

|

Key countries |

China, US, Japan, South Korea, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Advanced Micro Devices Inc., Analog Devices Inc., Broadcom Inc., Diotec Semiconductor AG, Everlight Electronics Co. Ltd., Infineon Technologies AG, Intel Corp., KYOCERA Corp., Microchip Technology Inc., Monolithic Power Systems Inc., Murata Manufacturing Co. Ltd., NXP Semiconductors NV, ON Semiconductor Corp., Panasonic Holdings Corp., Qualcomm Inc., Renesas Electronics Corp., STMicroelectronics International N.V., Texas Instruments Inc., Toshiba Corp., and Vishay Intertechnology Inc. |

|

Market dynamics |

Parent market analysis, market trends , market growth analysis , Market forecast, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID 19 impact and recovery analysis and future consumer dynamics, Market condition analysis for forecast period |

|

Customization purview |

If our market forecast report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Active Electronic Components Market Research and Growth Report?

- CAGR of the market report during the forecast period

- Detailed information of market analysis and report on factors that will drive the growth of the market between 2024 and 2028

- Precise estimation of the size of the market and its contribution in focus to the parent market

- Accurate predictions about upcoming trends and changes in consumer behavior

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements.

RIA -

RIA -