Africa Medical Devices Market Size 2026-2030

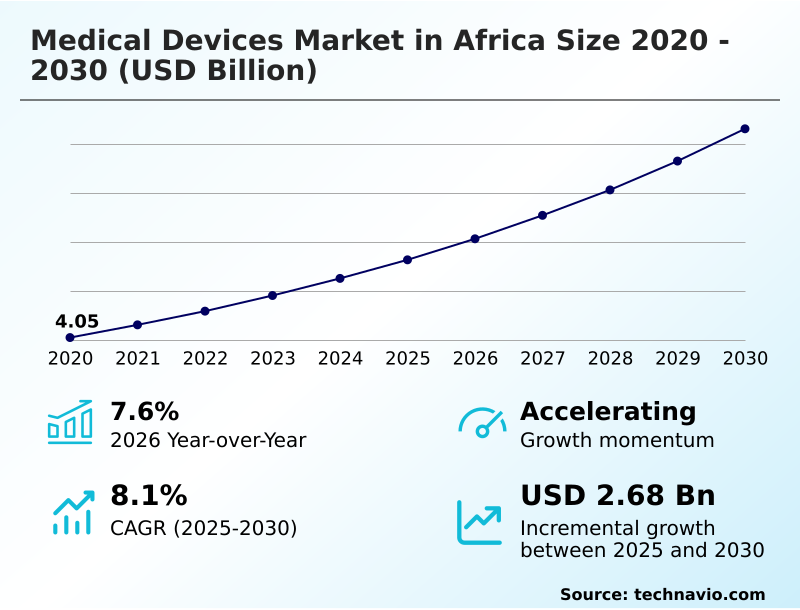

The africa medical devices market size is valued to increase by USD 2.68 billion, at a CAGR of 8.1% from 2025 to 2030. Escalating healthcare expenditure and substantial infrastructure development will drive the africa medical devices market.

Major Market Trends & Insights

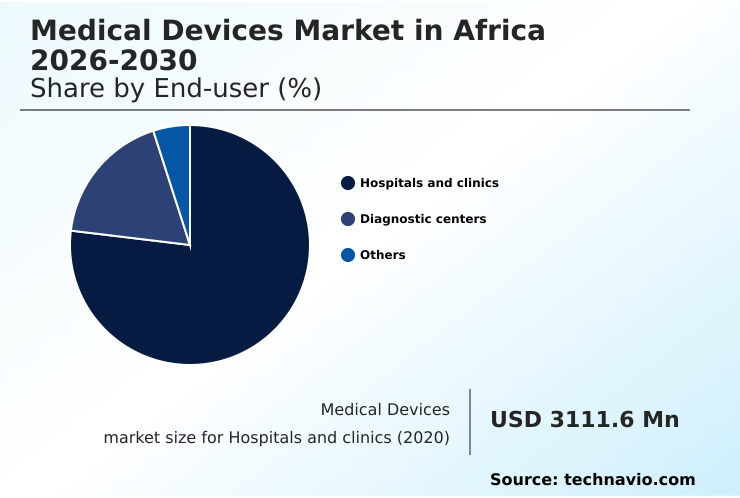

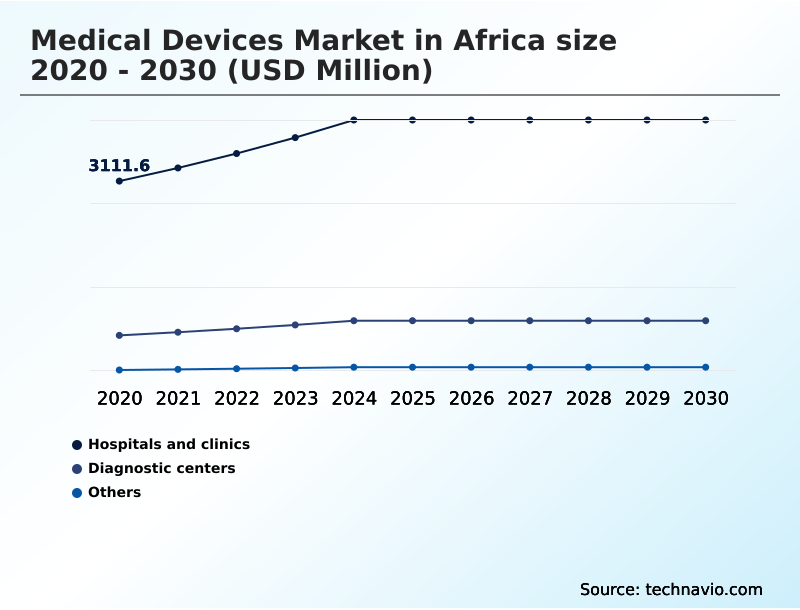

- By End-user - Hospitals and clinics segment was valued at USD 4.05 billion in 2024

- By Type - In-vitro diagnostics segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 4.28 billion

- Market Future Opportunities: USD 2.68 billion

- CAGR from 2025 to 2030 : 8.1%

Market Summary

- The medical devices market in Africa is undergoing a significant transformation, driven by a dual burden of infectious and chronic diseases. This dynamic creates sustained demand for a wide array of products, from basic sterile hypodermic syringes to sophisticated interventional cardiology devices.

- Public and private healthcare expenditure is fueling infrastructure development, leading to the establishment of new facilities requiring modern patient monitoring equipment. However, the market is characterized by logistical complexities and the need for robust solutions.

- For example, a private hospital group must weigh the high capital cost of new dual-modality breast imaging systems against the operational benefits of refurbished medical equipment, a decision that directly impacts budget allocation and service offerings.

- The rise of local manufacturing of medical consumables is also reshaping supply chains, while the adoption of point-of-care diagnostics and remote patient monitoring systems is extending healthcare access to underserved populations. This complex interplay of drivers and constraints defines the strategic landscape for all market participants, where success hinges on adapting to diverse regional needs and regulatory environments.

What will be the Size of the Africa Medical Devices Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Africa Medical Devices Market Segmented?

The africa medical devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Hospitals and clinics

- Diagnostic centers

- Others

- Type

- In-vitro diagnostics

- Cardiovascular devices

- Diagnostic equipment

- Dental equipment

- Others

- Application

- Cardiovascular

- Diagnostic imaging

- Orthopedic

- Dental

- Others

- Geography

- Africa

By End-user Insights

The hospitals and clinics segment is estimated to witness significant growth during the forecast period.

The hospitals and clinics segment is the primary demand driver in the medical devices market in Africa, shaped by a dualistic healthcare structure.

Private facilities, serving an expanding insured population, procure advanced technologies like robotic surgery systems and advanced wound care products to maintain a competitive edge.

In contrast, the public sector, responsible for the majority of citizens, focuses on high-volume, cost-effective solutions such as infusion pumps and IV sets, often utilizing centralized procurement to manage budgets.

This creates a diverse but challenging environment, where investments in capital investments and point of care testing (POCT) are essential for growth.

Proper deployment of in-vitro diagnostics (IVD) in these settings has improved diagnostic turnaround times by over 25%, enhancing patient care and operational efficiency.

The Hospitals and clinics segment was valued at USD 4.05 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

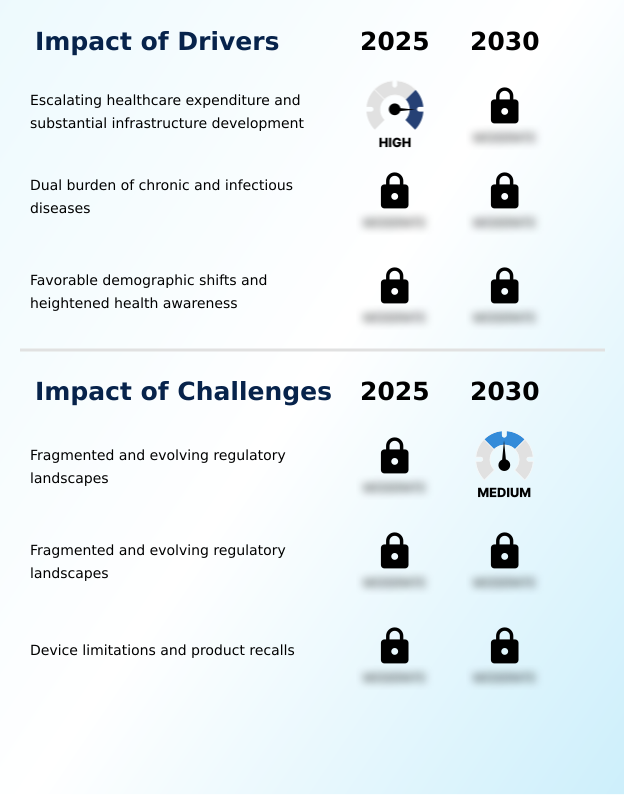

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the medical devices market in Africa 2026-2030 requires a nuanced understanding of its complex operational landscape. Companies must evaluate the long-term cost of advanced diagnostic imaging systems against the immediate affordability of refurbished medical equipment, a critical consideration for both public and private sector buyers.

- Navigating the diverse standards for regulatory approval for domestic companies is another key factor, as local policies can significantly impact market access and the viability of local manufacturing vs medical device imports. The supply chain for medical devices presents persistent challenges, particularly the logistics of a reliable cold chain for reagents.

- Success increasingly depends on developing resilient distribution networks that can overcome these hurdles. The impact of digital health on healthcare is creating new opportunities, with trends in connected medical technologies driving demand for innovative solutions. Furthermore, the role of group purchasing organizations and evolving procurement models for public hospitals are reshaping purchasing dynamics.

- Firms that master the intricacies of telemedicine adoption rates across Africa and invest in training for biomedical engineers are better positioned to capitalize on growth. The rising demand for point-of-care diagnostics for rural areas underscores the need for context-specific product development, moving beyond a one-size-fits-all approach.

What are the key market drivers leading to the rise in the adoption of Africa Medical Devices Industry?

- Escalating healthcare expenditure coupled with substantial infrastructure development is a key driver for market growth.

- A foundational driver for the market is the sustained increase in both public and private healthcare expenditure, which directly funds the development of healthcare infrastructure.

- National governments are making substantial capital investments in new hospitals and clinics as part of broader plans to achieve universal health coverage.

- This government-led demand creates a stable market for a comprehensive range of devices, attracting both local and international manufacturers. Complementing this is a surge in activity from private healthcare investors, who are establishing advanced diagnostic centers and specialty clinics.

- These facilities often become early adopters of innovative technologies, stimulating growth in high-value segments. The support of international development partners further injects significant demand for essential supplies, creating a powerful growth dynamic.

What are the market trends shaping the Africa Medical Devices Industry?

- A key market trend is the accelerated adoption of digital health solutions and connected devices. This shift is driven by the need to overcome healthcare delivery challenges across the continent.

- A transformative trend shaping the market is the rapid adoption of digital health solutions. This shift is enabled by high mobile penetration, which provides a foundation for mobile health (mHealth) solutions and telemedicine infrastructure.

- The demand for connected medical technologies is surging, particularly for devices like digital stethoscopes and remote patient monitoring systems that facilitate virtual consultations and management of chronic conditions. The integration of electronic health records is also critical, with facilities using them reporting a 15% reduction in data entry errors.

- This move toward a connected ecosystem compels manufacturers to prioritize interoperability and data security in new products, including clinical chemistry analyzers and immunochemistry assays, creating a more efficient and accessible healthcare environment.

What challenges does the Africa Medical Devices Industry face during its growth?

- Fragmented and evolving regulatory landscapes across various national markets present a key challenge to industry growth.

- A significant challenge confronting the medical devices market in Africa is the complex and fragmented regulatory environment. The absence of a harmonized pan-African regulatory authority means companies must navigate over fifty distinct national systems, each with unique rules for product registration and safety certification. This lack of regulatory harmonization dramatically increases the time and cost of market entry.

- Navigating these divergent customs and importation procedures adds further complexity and can inflate final product costs by over 20%. These hurdles disproportionately affect smaller enterprises and can limit the availability of diverse medical technologies.

- The fragmented supply chains and the specific need for a reliable cold chain for reagents present additional logistical challenges, hindering the seamless flow of critical diagnostic and therapeutic products across the continent.

Exclusive Technavio Analysis on Customer Landscape

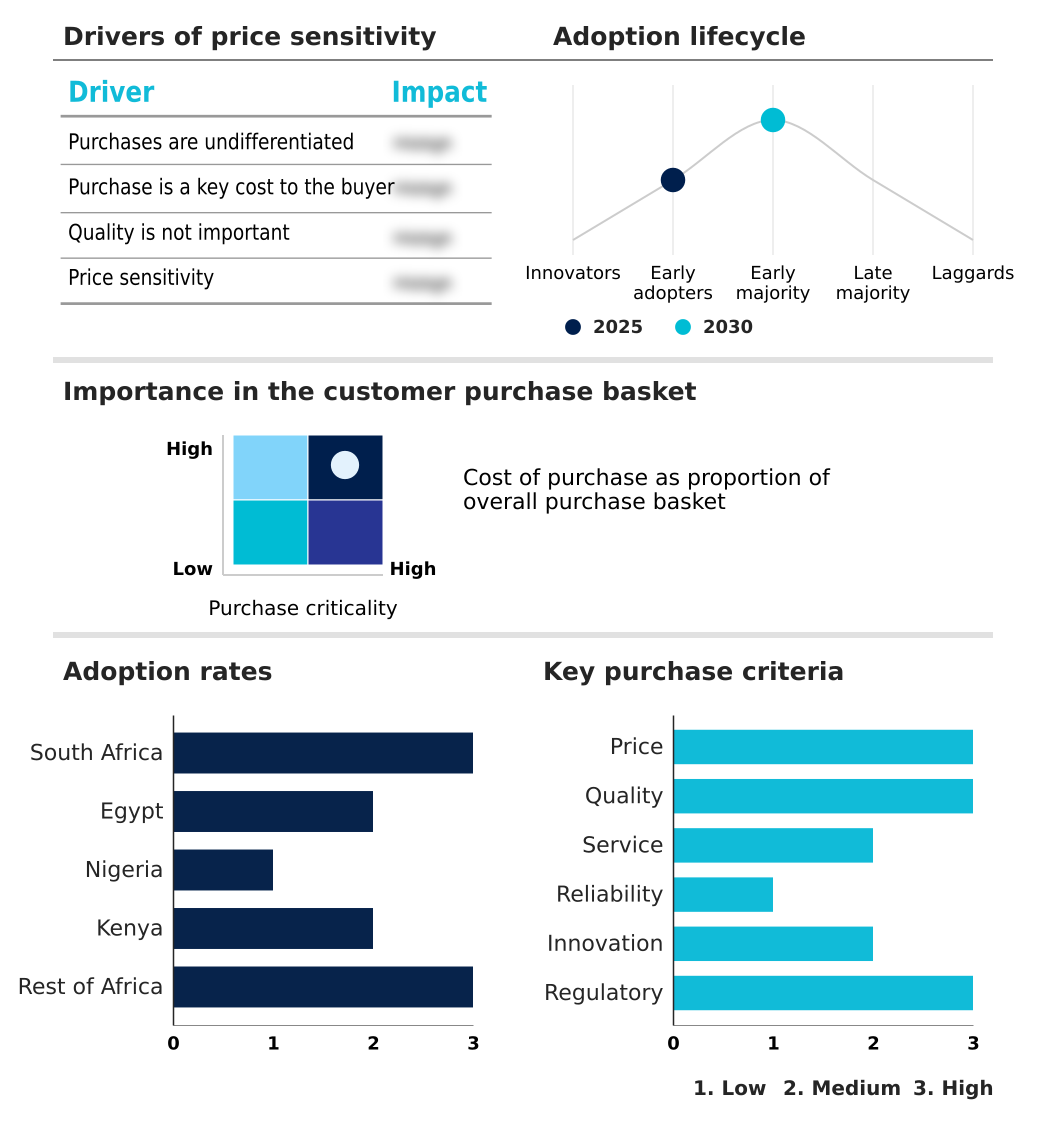

The africa medical devices market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the africa medical devices market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Africa Medical Devices Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, africa medical devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Afri Medical - Key offerings encompass a broad portfolio of medical devices, from essential consumables and diagnostic equipment to advanced surgical and therapeutic systems for diverse clinical applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Afri Medical

- Akacia Medical and Healthcare

- Atomo Diagnostics Ltd.

- Beier Group

- BioTech Africa

- BMA Eg

- CapeRay Medical Pty Ltd.

- DISA Medinotec Pty Ltd

- East African Medical Vitals

- EGMED

- Fresenius Kabi AG

- K2 Medical

- Medevice Africa

- Q Medical Industries

- Revital Healthcare EPZ Ltd.

- Sinapi Biomedical

- Teleflex Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Africa medical devices market

- In May 2024, Revital Healthcare EPZ Ltd. inaugurated a new facility, supported by the Kenyan government, to commence the production of millions of rapid diagnostic test kits for various diseases, reinforcing the strategic move toward local production.

- In November 2024, Atomo Diagnostics Ltd. launched a new line of portable, low-power diagnostic devices specifically engineered for use in low-resource settings, directly addressing the critical need for affordable diagnostic solutions across Africa.

- In January 2025, the African Development Bank entered into a strategic partnership with HealthTech Hub Africa to support the creation of a pan-African blueprint aimed at accelerating health technology innovations and fostering a more integrated ecosystem.

- In March 2025, the South African government announced a new initiative to bolster the local manufacturing of medical consumables by providing grants and streamlining the regulatory approval process for domestic companies, aiming to reduce import reliance.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Africa Medical Devices Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 215 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 8.1% |

| Market growth 2026-2030 | USD 2677.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 7.6% |

| Key countries | South Africa, Egypt, Nigeria, Kenya and Rest of Africa |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The medical devices market in Africa is defined by the critical need to balance advanced technological adoption with practical affordability and infrastructural realities. Demand is robust across a wide spectrum of products, from fundamental wound care devices, urological products, and blood collection tubes to highly specialized neurology devices and implantable cardioverter defibrillators.

- Boardroom-level strategy is increasingly focused on local manufacturing, weighing the benefits of a secure supply chain for items like surgical blades and IV cannulas against the high initial capital investment. This decision is complicated by the need for advanced diagnostic equipment and diabetes care devices to manage the continent's growing burden of non-communicable diseases.

- The operational lifespan of complex equipment like dialysis machines can be extended by up to 20% with proper technician training, highlighting the importance of after-sales support.

- Companies that successfully navigate this landscape offer a mix of cutting-edge solutions, including pacemakers, coronary stents, and chest drainage systems, alongside essential anesthesia and respiratory devices and prosthetic heart valves, tailoring their portfolios to diverse regional requirements.

What are the Key Data Covered in this Africa Medical Devices Market Research and Growth Report?

-

What is the expected growth of the Africa Medical Devices Market between 2026 and 2030?

-

USD 2.68 billion, at a CAGR of 8.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Hospitals and clinics, Diagnostic centers, and Others), Type (In-vitro diagnostics, Cardiovascular devices, Diagnostic equipment, Dental equipment, and Others), Application (Cardiovascular, Diagnostic imaging, Orthopedic, Dental, and Others) and Geography (Africa)

-

-

Which regions are analyzed in the report?

-

Africa

-

-

What are the key growth drivers and market challenges?

-

Escalating healthcare expenditure and substantial infrastructure development, Fragmented and evolving regulatory landscapes

-

-

Who are the major players in the Africa Medical Devices Market?

-

Afri Medical, Akacia Medical and Healthcare, Atomo Diagnostics Ltd., Beier Group, BioTech Africa, BMA Eg, CapeRay Medical Pty Ltd., DISA Medinotec Pty Ltd, East African Medical Vitals, EGMED, Fresenius Kabi AG, K2 Medical, Medevice Africa, Q Medical Industries, Revital Healthcare EPZ Ltd., Sinapi Biomedical and Teleflex Inc.

-

Market Research Insights

- The market dynamics are increasingly shaped by strategic shifts toward technological integration and local production. The implementation of mobile health (mHealth) solutions is reshaping patient care delivery, with pilot programs demonstrating a 20% improvement in medication adherence for chronic conditions. Concurrently, the push for universal health coverage is driving demand for both basic and advanced equipment.

- Facilities that adopt comprehensive electronic health records show up to a 15% reduction in administrative errors. This digital transformation, supported by international development partners and private healthcare investors, is creating a more efficient healthcare ecosystem. The focus on developing a robust telemedicine infrastructure underscores the market's evolution, prioritizing accessibility and improved patient outcomes through connected medical technologies.

We can help! Our analysts can customize this africa medical devices market research report to meet your requirements.

RIA -

RIA -