AI In Medical Billing Market Size 2025-2029

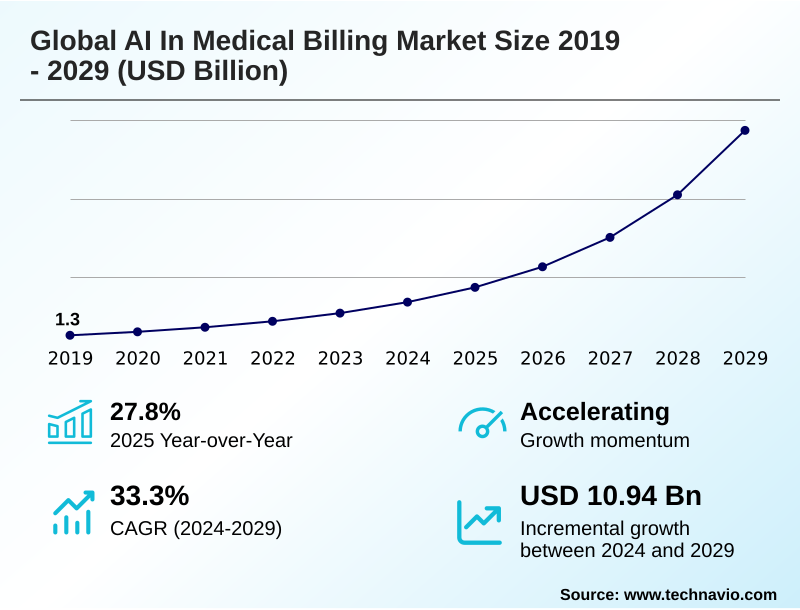

The ai in medical billing market size is valued to increase by USD 10.94 billion, at a CAGR of 33.3% from 2024 to 2029. Escalating complexity of medical coding and regulatory frameworks will drive the ai in medical billing market.

Major Market Trends & Insights

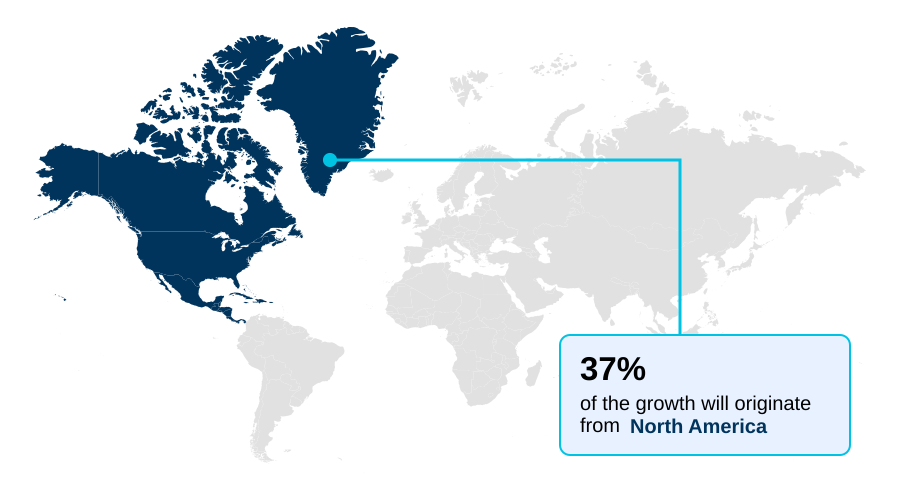

- North America dominated the market and accounted for a 36.6% growth during the forecast period.

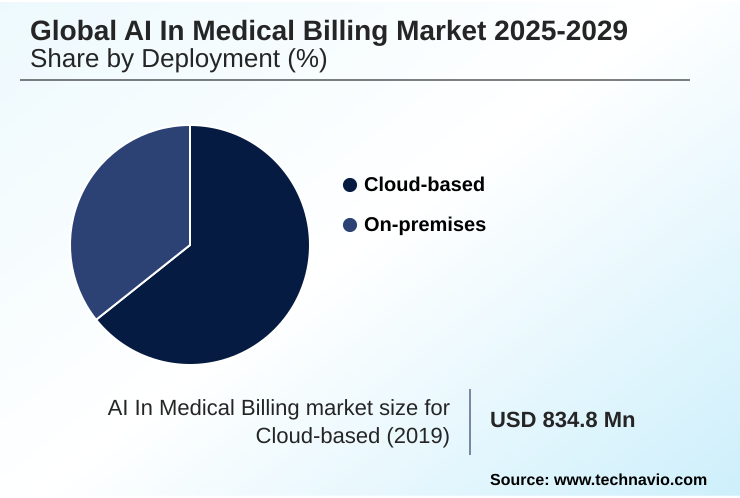

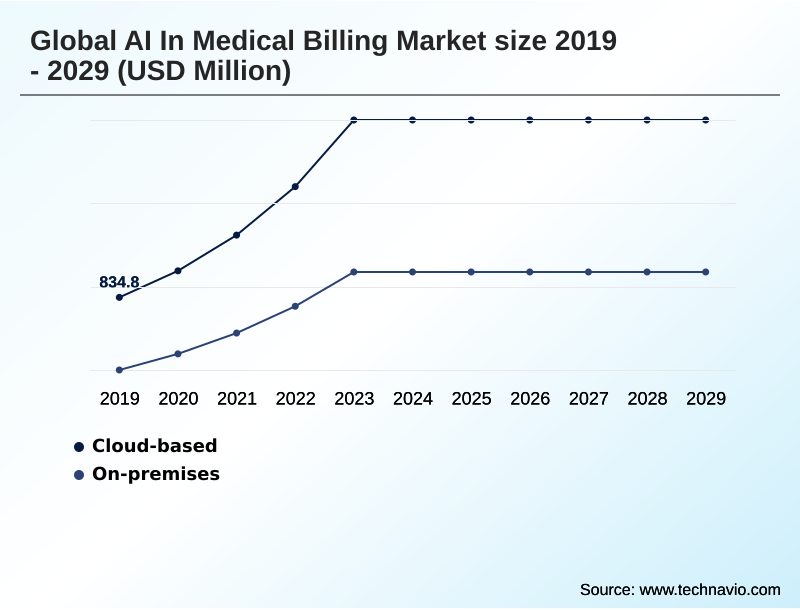

- By Deployment - Cloud-based segment was valued at USD 1.74 billion in 2023

- By Application - Claims processing and adjudication segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 13.04 billion

- Market Future Opportunities: USD 10.94 billion

- CAGR from 2024 to 2029 : 33.3%

Market Summary

- The AI in medical billing market is defined by a transformative shift toward intelligent automation to address persistent industry pressures. Escalating administrative costs, the intricate nature of medical coding complexity, and a shortage of skilled staff are compelling healthcare providers to adopt AI-powered solutions. These platforms leverage technologies like machine learning and natural language processing to enhance revenue cycle management.

- For instance, a hospital system can deploy an AI tool for predictive denial management, which analyzes outgoing claims against historical payer behavior and complex reimbursement rules. This system flags claims with a high probability of rejection, allowing billing staff to make proactive corrections, thereby improving the clean claim rate and accelerating cash flow.

- This move from reactive appeals to proactive error correction reduces operational overhead and allows personnel to focus on high-value tasks. The integration of generative AI in healthcare further propels this evolution, enabling automated appeal letter generation and sophisticated clinical documentation analysis, which are crucial for navigating value-based care models and ensuring financial stability.

What will be the Size of the AI In Medical Billing Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the AI In Medical Billing Market Segmented?

The ai in medical billing industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Deployment

- Cloud-based

- On-premises

- Application

- Claims processing and adjudication

- Automated coding and documentation

- Revenue analytics and forecasting

- Fraud detection and risk scoring

- Patient payment optimization

- End-user

- Hospitals and clinics

- Healthcare payers

- ASCs

- Billing outsourcing firms

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Deployment Insights

The cloud-based segment is estimated to witness significant growth during the forecast period.

The cloud-based deployment model, primarily delivered via cloud-based SaaS platforms, is central to the AI in medical billing market. This approach supports critical functions like predictive denial management and claim adjudication without requiring significant on-premises infrastructure.

It enables healthcare providers to achieve superior RCM workflow optimization and scalability. These platforms leverage natural language processing for clinical documentation analysis and claim scrubbing, which can automate over 90% of coding tasks.

This enhances risk adjustment accuracy and supports touchless claims processing, providing a framework for real-time compliance updates.

This model is foundational for achieving denial rate reduction and implementing effective patient financial engagement strategies that address self-pay account collections, ultimately improving cash flow forecasting.

The Cloud-based segment was valued at USD 1.74 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 36.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI In Medical Billing Market Demand is Rising in North America Request Free Sample

The geographic landscape of the AI in medical billing market is led by North America, which accounts for over 36% of the market opportunity, driven by its complex multi-payer system and high technological adoption.

The region's focus on denial rate reduction and operational efficiency has spurred significant investment in platforms supporting computer-assisted coding and prior authorization automation.

Europe follows, with countries like Germany and the UK adopting AI to manage public and private insurance systems, emphasizing data privacy through techniques like federated learning models and data anonymization.

APAC is the fastest-growing region, with nations like India and China leveraging AI to manage large-scale public health initiatives and a burgeoning private sector.

The synergy between electronic health records and AI is critical globally, with successful implementations of upcoding detection and phantom billing analysis improving revenue integrity by over 10%.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategically, calculating the ROI of AI in healthcare RCM is becoming a central boardroom exercise, as organizations weigh initial investment against long-term operational gains.

- The core value is demonstrated through specific applications, such as using machine learning for claims fraud detection, which safeguards revenue integrity, and the use of AI for automating prior authorization requests, which directly reduces care delays and administrative friction. Furthermore, generative AI for drafting denial appeal letters is transforming a once manual and time-consuming process into an efficient, data-driven workflow.

- AI platforms for revenue cycle management optimization are now essential for navigating the complexities of modern healthcare finance. The impact of AI on medical billing compliance is profound, as these systems offer dynamic updates to address shifting regulations.

- A significant hurdle remains in integrating AI with legacy EHR systems, a task that can increase project timelines by more than 50% compared to simpler software rollouts. Overcoming the challenges of AI in medical billing, particularly around data integration and algorithmic transparency, is key to unlocking its full potential.

- The technology's role extends to fine-tuning reimbursement through tools that help in optimizing hierarchical condition category coding with AI and automating claims adjudication with machine learning. Ultimately, the AI role in value-based care reimbursement models is to create a more efficient and accurate financial ecosystem for providers.

What are the key market drivers leading to the rise in the adoption of AI In Medical Billing Industry?

- The escalating complexity of medical coding systems and evolving regulatory frameworks is a primary driver for the adoption of AI in medical billing.

- Market growth is primarily driven by the convergence of advanced AI technologies and the escalating complexity of healthcare finance.

- The proliferation of electronic health records has created vast datasets, fueling the efficacy of claims data analytics and large language models for clinical documentation analysis.

- Economic pressures compel providers to seek solutions for denial rate reduction and RCM workflow optimization, with AI platforms delivering tangible results, such as accelerating payment cycles by up to 20%.

- The technology directly addresses medical coding complexity, with computer-assisted coding and natural language processing automating the application of ICD-10 and CPT coding.

- Furthermore, the shift to value-based care models makes tools for risk adjustment and hierarchical condition category coding essential for accurate reimbursement, solidifying AI's role in the industry.

What are the market trends shaping the AI In Medical Billing Industry?

- A critical imperative for healthcare organizations is to enhance operational efficiency amid escalating administrative costs. This is driving the adoption of technological solutions to optimize complex revenue cycle management processes.

- Key trends in the AI in medical billing market are centered on leveraging technology to address operational and regulatory pressures. The adoption of generative AI in healthcare is a transformative force, enabling sophisticated unstructured data extraction and automated appeal letter generation, which improves denial management automation.

- This technology, often delivered via cloud-based SaaS platforms, helps providers navigate the intricacies of payer contract modeling and medical necessity criteria. A significant focus is on administrative burden reduction, with AI tools now automating tasks from point-of-care data capture to final remittance advice processing.

- Implementations have demonstrated a marked improvement in first-pass claim acceptance rates, in some cases by over 15%, by ensuring proactive claim correction. This drive for efficiency is reshaping how healthcare organizations approach financial management and patient engagement.

What challenges does the AI In Medical Billing Industry face during its growth?

- Navigating stringent data privacy regulations and ensuring robust cybersecurity imperatives are primary challenges affecting industry growth.

- Significant challenges constrain the AI in medical billing market, led by stringent data privacy regulations and system integration challenges. Integrating advanced AI with legacy EHR interoperability issues often requires custom API integration, a process that can increase project costs by over 40%. The 'black box' algorithm problem raises concerns about transparency and accountability, particularly with evolving AI regulatory frameworks.

- Healthcare organizations are cautious due to the high costs of implementation and the complexities of ensuring privacy-preserving AI through methods like federated learning models and data anonymization. Addressing potential algorithmic bias prevention is another critical hurdle to ensure equitable outcomes.

- These factors create a difficult landscape for providers aiming to adopt solutions for chargemaster optimization and patient payment prediction while managing significant technical and compliance risks.

Exclusive Technavio Analysis on Customer Landscape

The ai in medical billing market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai in medical billing market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI In Medical Billing Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai in medical billing market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Access Healthcare - The company provides technology-enabled revenue cycle management, BPO, IT, and finance and accounting services.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Access Healthcare

- Athenahealth Inc.

- CareCloud Inc.

- CodaMetrix

- eClinicalWorks LLC

- Ensemble Health Partners

- Epic Systems Corp.

- Fathom Health

- Fujitsu Ltd.

- GE Healthcare Technologies

- Hangzhou Weiyi Health Technology Co. Ltd.

- Infosys Ltd.

- McKesson Corp.

- NextGen Healthcare Inc.

- Nym Health

- Optum Inc.

- R1 RCM Inc.

- SWORD Health Technologies Inc.

- Waystar Inc.

- Wipro Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai in medical billing market

- In September 2024, Microsoft enhanced its Azure for Healthcare cloud platform with new generative AI capabilities designed to automate clinical documentation and administrative tasks, thereby creating higher quality data for downstream AI medical billing systems.

- In January 2025, Sutter Health announced an expanded partnership with an AI-powered RCM company to deploy artificial intelligence across its revenue cycle operations, aiming to automate workflows and improve financial outcomes.

- In March 2025, Navina, an AI platform that structures patient data to assist physicians at the point of care, raised a significant funding round to further develop technology that supports accurate diagnosis capture for risk adjustment coding.

- In April 2025, Waystar launched an enhanced analytics platform that utilizes predictive AI to provide healthcare organizations with more precise cash flow forecasting and root-cause analysis for payment variances.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI In Medical Billing Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 312 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 33.3% |

| Market growth 2025-2029 | USD 10937.9 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 27.8% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI in medical billing market is undergoing a fundamental transformation driven by the need for greater efficiency and accuracy in healthcare finance. At the core of this shift is the deployment of sophisticated technologies like natural language processing, computer-assisted coding, and robotic process automation to streamline revenue cycle management.

- Boardroom-level decisions increasingly focus on balancing the high upfront cost of implementing these platforms against their proven ability to deliver substantial ROI through enhanced claim adjudication and predictive denial management. These systems are critical for navigating medical coding complexity and ensuring compliance with ever-changing payer-specific submission rules.

- Key applications include prior authorization automation and advanced claims data analytics, which work in tandem with electronic health records to improve denial rate reduction. For instance, providers leveraging AI for claim scrubbing and denial root cause analysis have reported a reduction in administrative workload by up to 30%.

- The evolution toward value-based care models further necessitates tools for precise risk adjustment and hierarchical condition category coding, making AI-driven platforms indispensable for maintaining financial health in a complex reimbursement landscape.

What are the Key Data Covered in this AI In Medical Billing Market Research and Growth Report?

-

What is the expected growth of the AI In Medical Billing Market between 2025 and 2029?

-

USD 10.94 billion, at a CAGR of 33.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Cloud-based, On-premises), Application (Claims processing and adjudication, Automated coding and documentation, Revenue analytics and forecasting, Fraud detection and risk scoring, Patient payment optimization), End-user (Hospitals and clinics, Healthcare payers, ASCs, Billing outsourcing firms) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Escalating complexity of medical coding and regulatory frameworks, Navigating stringent data privacy and security imperatives

-

-

Who are the major players in the AI In Medical Billing Market?

-

Access Healthcare, Athenahealth Inc., CareCloud Inc., CodaMetrix, eClinicalWorks LLC, Ensemble Health Partners, Epic Systems Corp., Fathom Health, Fujitsu Ltd., GE Healthcare Technologies, Hangzhou Weiyi Health Technology Co. Ltd., Infosys Ltd., McKesson Corp., NextGen Healthcare Inc., Nym Health, Optum Inc., R1 RCM Inc., SWORD Health Technologies Inc., Waystar Inc. and Wipro Ltd.

-

Market Research Insights

- The dynamics of the AI in medical billing market are shaped by the need for RCM workflow optimization to counteract immense financial pressures. Healthcare providers are leveraging cloud-based SaaS platforms that offer automated eligibility verification and proactive claim correction, with some achieving a 25% reduction in denial rates.

- These systems facilitate real-time compliance updates to navigate complex telehealth billing rules and out-of-network billing regulations. The adoption of AI for administrative burden reduction is critical, as it allows staff to shift focus from manual data entry to strategic denial management automation. Advanced platforms provide predictive financial insights, with implementations showing a 15% improvement in cash flow forecasting accuracy.

- By utilizing patient propensity-to-pay models, providers can also optimize collection strategies, improving patient satisfaction scores while securing revenue.

We can help! Our analysts can customize this ai in medical billing market research report to meet your requirements.

RIA -

RIA -