AI Kitchen Market Size 2025-2029

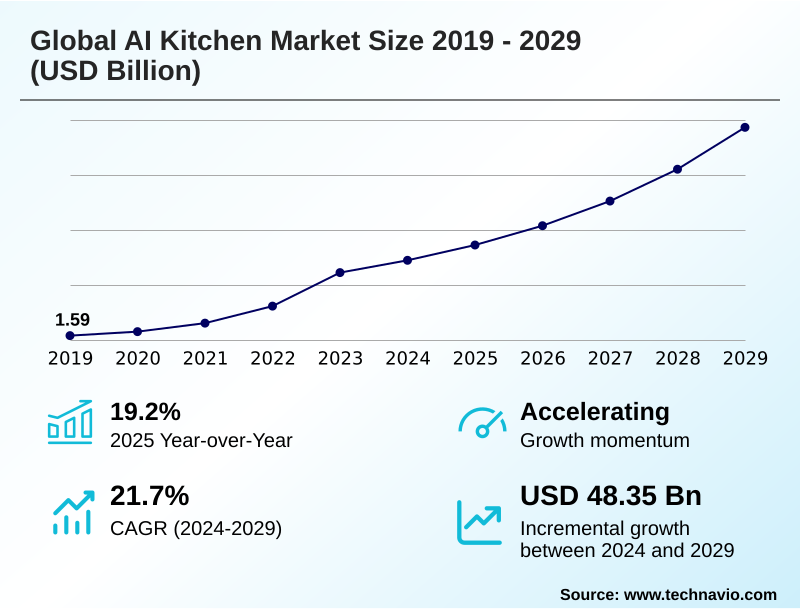

The ai kitchen market size is valued to increase by USD 48.35 billion, at a CAGR of 21.7% from 2024 to 2029. Increasing consumer demand for convenience and automation will drive the ai kitchen market.

Major Market Trends & Insights

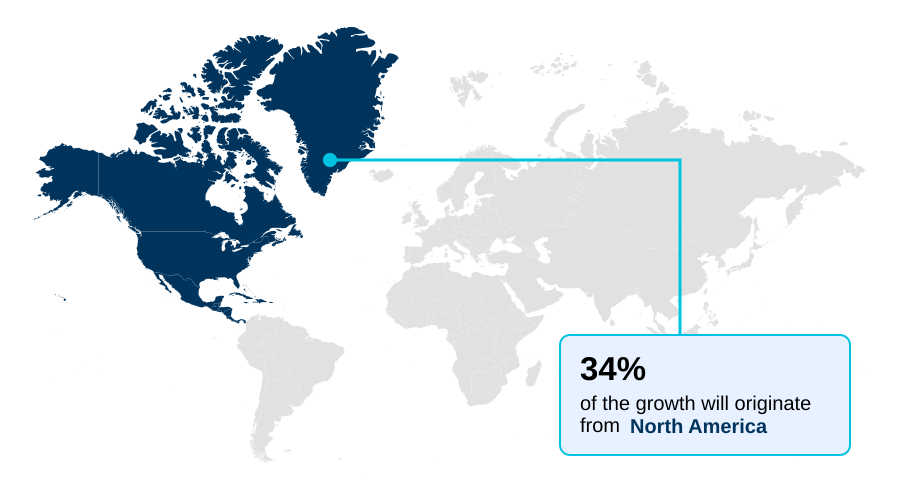

- North America dominated the market and accounted for a 34% growth during the forecast period.

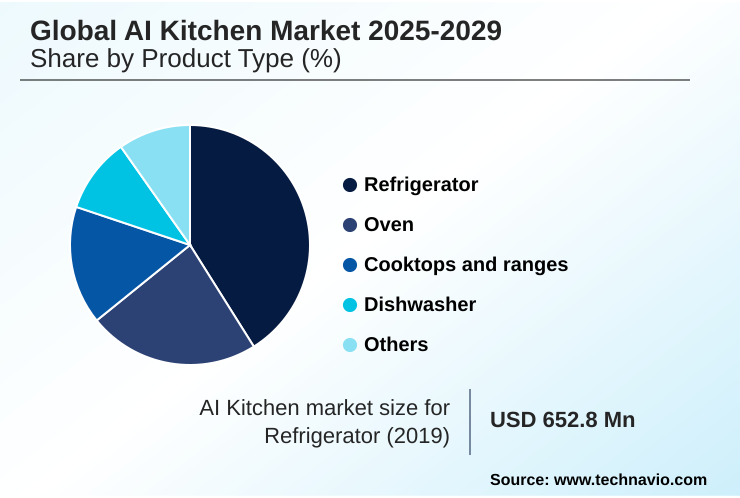

- By Product Type - Refrigerator segment was valued at USD 9.87 billion in 2023

- By Application - Residential segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 75.74 billion

- Market Future Opportunities: USD 48.35 billion

- CAGR from 2024 to 2029 : 21.7%

Market Summary

- The AI kitchen market is redefining culinary spaces by transforming them from areas of manual labor into highly efficient, automated environments. This shift is propelled by the integration of technologies like natural language processing and smart sensor technology, which enable a new class of appliances to offer proactive assistance and hyper-personalization.

- For instance, commercial kitchens are leveraging AI for intelligent inventory tracking and automated cooking cycles, which not only ensures meal consistency but also drives significant food waste reduction. This data-driven food management leads to better resource consumption optimization.

- However, the path to mass adoption involves addressing the high initial cost of robotic cooking systems and ensuring seamless smart appliance interoperability between different brands. The evolution toward a cohesive smart home ecosystem, where the kitchen acts as a central hub, depends on robust IoT connectivity protocols and intuitive conversational interfaces that simplify the user experience.

- The ultimate goal is a kitchen that provides personalized nutritional guidance and predictive maintenance alerts, making daily routines more convenient.

What will be the Size of the AI Kitchen Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the AI Kitchen Market Segmented?

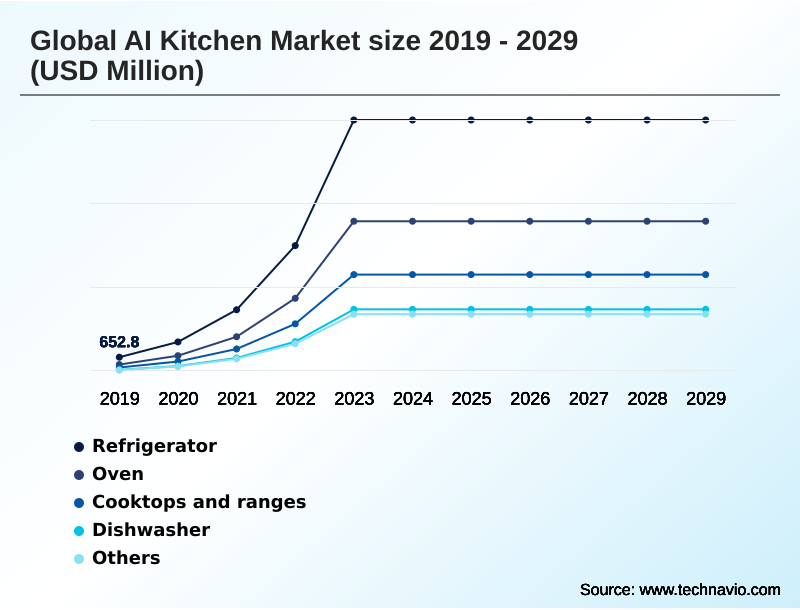

The ai kitchen industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product type

- Refrigerator

- Oven

- Cooktops and ranges

- Dishwasher

- Others

- Application

- Residential

- Commercial

- Distribution channel

- Specialty stores

- Online channels

- Hypermarkets and supermarkets

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- APAC

- China

- South Korea

- Japan

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- South Africa

- UAE

- Israel

- Rest of World (ROW)

- North America

By Product Type Insights

The refrigerator segment is estimated to witness significant growth during the forecast period.

The refrigerator segment is evolving into an intelligent food management hub, central to the AI kitchen. This transformation leverages computer vision cameras and advanced machine learning algorithms for intelligent inventory tracking and AI-enhanced food preservation.

Key functions include data-driven food management and automated grocery list creation, which are pivotal for food waste reduction. Systems offering a personalized cooking experience and connected oven recipe suggestions are becoming standard.

This adaptive user preference learning, which can identify over 33 different food items with 95% accuracy, optimizes resource consumption and enhances AI-guided culinary techniques.

The integration within a broader smart home ecosystem is critical, enabling proactive assistance and seamless communication through established IoT connectivity protocols and advanced AI kitchen appliance integration for a cohesive user experience.

The Refrigerator segment was valued at USD 9.87 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 34% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI Kitchen Market Demand is Rising in North America Get Free Sample

The geographic landscape of the market is diverse, with regional priorities shaping technology adoption.

In North America, which accounts for nearly 34% of the incremental growth, demand is driven by convenience, leading to a focus on seamless grocery ordering and smart home automation kitchen features.

Europe prioritizes sustainability and kitchen energy optimization AI, with regulations compelling efficiency gains; certain AI-driven appliances have achieved a 15% reduction in energy use.

The APAC region, led by innovation hubs in South Korea and China, is a nexus for advanced development in AI-powered food pairing and sophisticated smart kitchen user interface design.

This region pioneers concepts like the smart home AI agent, setting global benchmarks for what is technologically feasible in the market.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The AI kitchen market presents a multifaceted value proposition, with the benefits of AI in commercial kitchens being particularly compelling. Commercial kitchen automation using AI robotics is already improving efficiency and consistency, with AI-driven cooking for consistent results leading to operational gains of over 15% compared to manual methods.

- In the residential sector, a key driver is how AI reduces household food waste through intelligent tracking and alerts. As consumers evaluate options, comparing AI kitchen platform ecosystems becomes critical, as does understanding the user data security in connected kitchen appliances. The future of generative AI in cooking promises creative recipe modification and more natural interactions.

- However, this raises privacy concerns with AI kitchen cameras, which must be addressed to build trust. Furthermore, AI-powered nutritional tracking in smart kitchens, especially when integrating health trackers with AI kitchens, offers significant wellness benefits. Interoperability challenges in smart kitchens remain a hurdle, but the role of IoT in AI kitchen development is key to creating unified experiences.

- For an aging population, AI kitchen technology for elderly assistance is an important emerging application. Innovations like the smart oven with food recognition technology, smart refrigerator automated food ordering, and AI-based predictive maintenance for appliances are making kitchens more autonomous.

- The technology enables AI for personalized dietary plan generation, moving beyond simple AI kitchen voice assistant query examples to create truly helpful systems.

What are the key market drivers leading to the rise in the adoption of AI Kitchen Industry?

- The primary driver for market expansion is the escalating consumer demand for convenience and automated solutions that streamline household management.

- Growing consumer demand for convenience is a primary market driver, with features like automated recipe personalization and proactive appliance alerts simplifying daily routines.

- The focus on health and wellness is also significant, as AI-driven nutritional analysis and integration with fitness trackers are enabling personalized cooking experiences; meal plans generated by these systems show a 15% higher adherence rate than traditional methods.

- Relentless technological advancement, particularly in smart sensor technology and voice-activated cooking capabilities, underpins this growth.

- The ability to perform remote appliance monitoring and receive predictive appliance diagnostics adds a layer of practicality and long-term value for consumers, making the AI kitchen an increasingly attractive investment.

What are the market trends shaping the AI Kitchen Industry?

- The market is witnessing a definitive shift from basic automation toward hyper-personalization and proactive assistance. This evolution transforms appliances into intelligent partners that anticipate user needs and tailor experiences accordingly.

- A defining trend is the shift toward hyper-personalization and proactive assistance, transforming appliances into intelligent partners. The integration of generative AI is creating more intuitive conversational interfaces, with some platforms generating custom recipes 50% faster than manual methods. This AI-powered meal planning is central to the modern smart kitchen.

- Another key trend is the emphasis on sustainability, with intelligent food management and AI-enhanced food preservation features helping to reduce household food spoilage by up to 40%. The development of comprehensive connected cooking platforms and robotic cooking systems enables a more seamless intelligent cooking workflow, supported by smart appliance firmware updates that continuously improve functionality and the smart kitchen experience.

What challenges does the AI Kitchen Industry face during its growth?

- A significant challenge affecting widespread market adoption is the high initial cost of AI-enabled appliances and the difficulty in conveying a clear value proposition to mass-market consumers.

- A major challenge is the high initial cost, with the price premium for AI-enabled appliances often 40-60% higher than standard models, creating a significant barrier for mass adoption. Data privacy and security are also critical concerns, as the collection of sensitive user information heightens the need for robust smart kitchen data privacy protocols.

- Furthermore, ecosystem fragmentation due to a lack of smart appliance interoperability complicates the user experience, with over 70% of households using mixed-brand appliances reporting integration issues. Overcoming these hurdles, which include addressing smart kitchen safety features and ensuring reliable automated cooking parameter adjustment, is essential for future market expansion and building consumer trust in AI-optimized energy consumption claims.

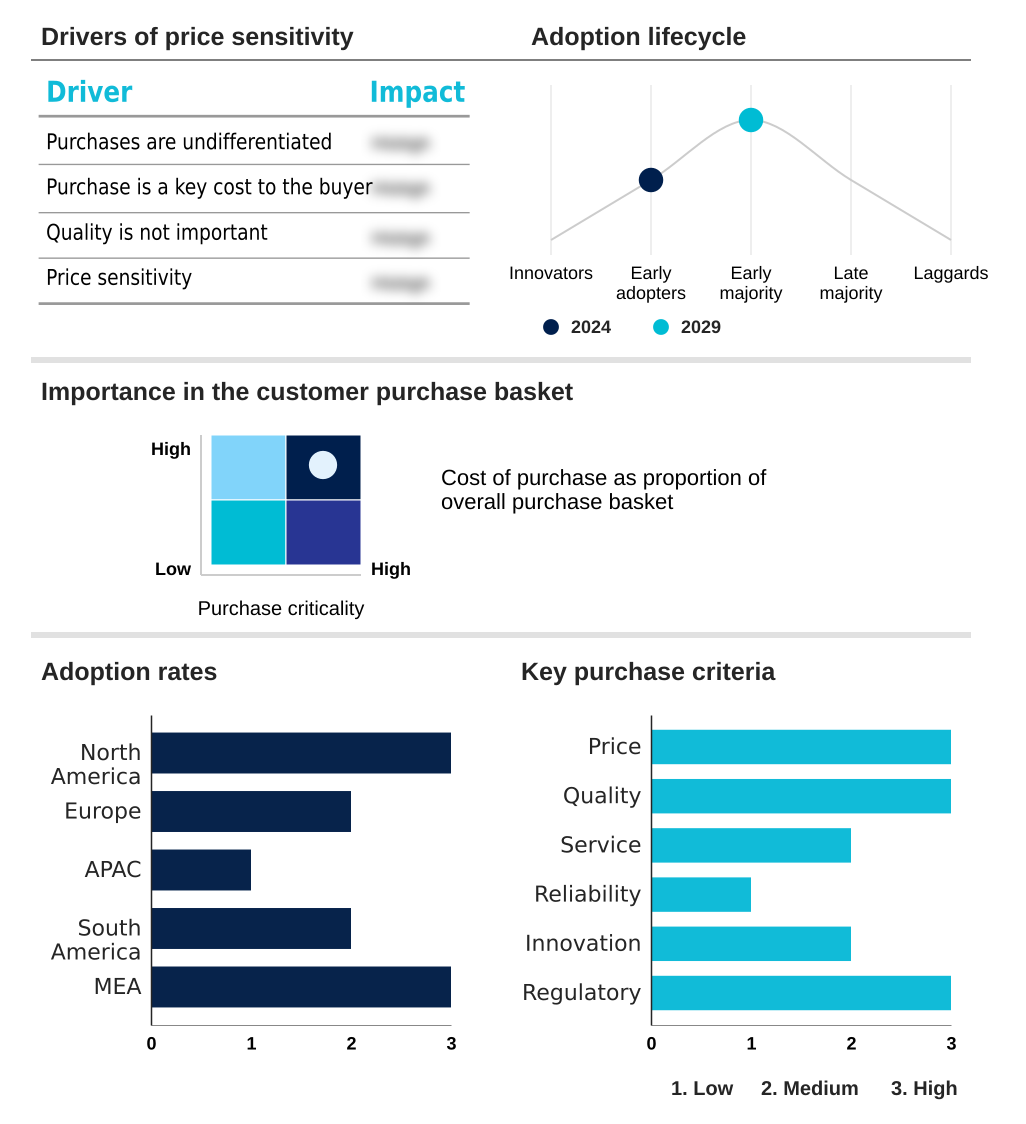

Exclusive Technavio Analysis on Customer Landscape

The ai kitchen market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai kitchen market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI Kitchen Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai kitchen market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AB Electrolux - Key offerings focus on embedding intelligence across appliance lines, creating interconnected ecosystems that provide predictive assistance, automated cooking, and personalized user experiences.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AB Electrolux

- Breville Group Ltd.

- BSH Home Appliances Ltd.

- Fisher and Paykel Appliances Ltd.

- FRIGIDAIRE

- General Electric Co.

- Haier Smart Home Co. Ltd.

- Hisense International Co. Ltd.

- Koninklijke Philips NV

- LG Electronics Inc.

- Miele and Cie. KG

- Panasonic Holdings Corp.

- Robert Bosch GmbH

- Samsung Electronics Co. Ltd.

- Sharp Consumer Electronics Poland sp. z o.o.

- Siemens AG

- THERMADOR

- Toshiba Corp.

- Whirlpool Corp.

- Zhuhai Gree Electric Appliances Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai kitchen market

- In August, 2024, Samsung Electronics launched its Samsung Food platform, an AI-powered application for personalized meal planning and recipe discovery that integrates with its smart appliances.

- In September, 2024, GE Appliances introduced its Profile Smart Mixer with Auto Sense, a product that embeds AI to automatically adjust mixing speed and duration for optimal consistency.

- In January, 2025, LG Electronics announced its development of a multi-modal generative AI smart home agent designed to power its future appliances with advanced conversational capabilities.

- In February, 2025, GE Appliances announced a strategic partnership with Instacart, enabling users to facilitate direct grocery ordering from their smart refrigerators to create a seamless procurement process.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI Kitchen Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 299 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 21.7% |

| Market growth 2025-2029 | USD 48354.8 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 19.2% |

| Key countries | US, Canada, Mexico, Germany, UK, Italy, The Netherlands, France, Spain, China, South Korea, Japan, India, Australia, Indonesia, Brazil, Argentina, Colombia, South Africa, UAE, Israel, Saudi Arabia and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI kitchen market is rapidly evolving from a collection of standalone smart devices to a fully integrated smart home ecosystem. This transition is powered by core technologies including computer vision cameras and sophisticated machine learning algorithms that enable features like intelligent inventory tracking, automated cooking cycles, and personalized nutritional guidance.

- The implementation of AI Pro Cooking technology and adaptive cooking algorithms delivers consistent culinary results, a key factor driving consumer adoption. Boardroom-level strategy is now focused on developing proprietary platforms versus embracing open IoT connectivity protocols to capture market share.

- Innovations such as generative AI integration for AI-driven recipe generation and multi-modal AI agents with conversational interfaces are redefining the user experience. Features like guided cooking modes and proactive assistance for food waste reduction are becoming standard. Moreover, AI-assisted cooking has demonstrated a capacity to reduce food preparation errors by up to 20%, providing a quantifiable return on investment.

- The inclusion of predictive maintenance capabilities further enhances the value proposition, solidifying the kitchen's role as an intelligent, responsive environment.

What are the Key Data Covered in this AI Kitchen Market Research and Growth Report?

-

What is the expected growth of the AI Kitchen Market between 2025 and 2029?

-

USD 48.35 billion, at a CAGR of 21.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product Type (Refrigerator, Oven, Cooktops and ranges, Dishwasher, Others), Application (Residential, Commercial), Distribution Channel (Specialty stores, Online channels, Hypermarkets and supermarkets) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing consumer demand for convenience and automation, High initial cost and perceived value proposition

-

-

Who are the major players in the AI Kitchen Market?

-

AB Electrolux, Breville Group Ltd., BSH Home Appliances Ltd., Fisher and Paykel Appliances Ltd., FRIGIDAIRE, General Electric Co., Haier Smart Home Co. Ltd., Hisense International Co. Ltd., Koninklijke Philips NV, LG Electronics Inc., Miele and Cie. KG, Panasonic Holdings Corp., Robert Bosch GmbH, Samsung Electronics Co. Ltd., Sharp Consumer Electronics Poland sp. z o.o., Siemens AG, THERMADOR, Toshiba Corp., Whirlpool Corp. and Zhuhai Gree Electric Appliances Co. Ltd.

-

Market Research Insights

- Market dynamics are shaped by a push toward holistic AI kitchen appliance integration and enhanced smart kitchen resource management. The focus is on delivering tangible outcomes through context-aware kitchen automation and AI for dietary management, which drives consumer adoption. For instance, systems featuring AI-based food spoilage detection have demonstrated the ability to reduce household food waste by up to 30%.

- Similarly, intelligent dishwasher cycles that utilize real-time sensor data can lower water consumption by 20% compared to conventional models, addressing both economic and environmental concerns.

- This emphasis on performance is further evident in AI cooking precision control, where automated parameter adjustments ensure consistent results, strengthening the value proposition beyond basic connectivity and making the voice-controlled kitchen environment more practical and efficient.

We can help! Our analysts can customize this ai kitchen market research report to meet your requirements.

RIA -

RIA -