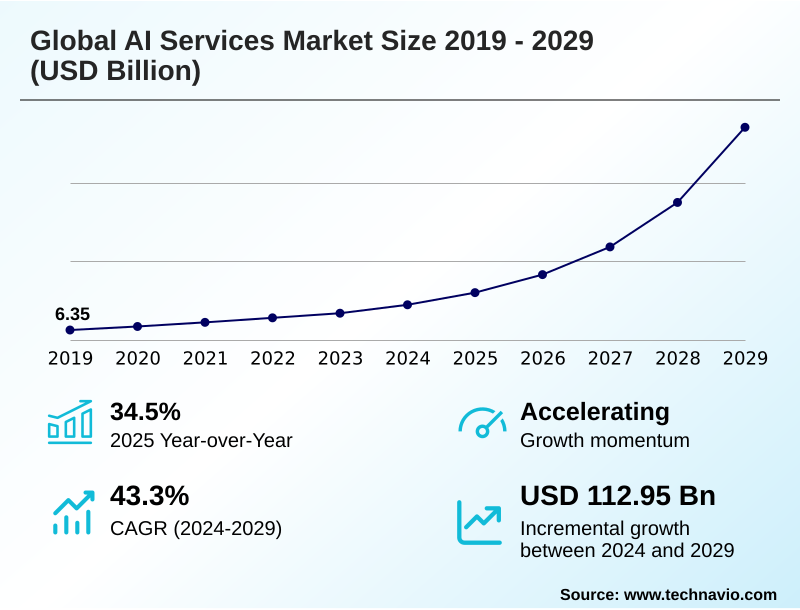

AI Services Market Size 2025-2029

The ai services market size is valued to increase by USD 112.95 billion, at a CAGR of 43.3% from 2024 to 2029. Proliferation of generative AI and large language models will drive the ai services market.

Major Market Trends & Insights

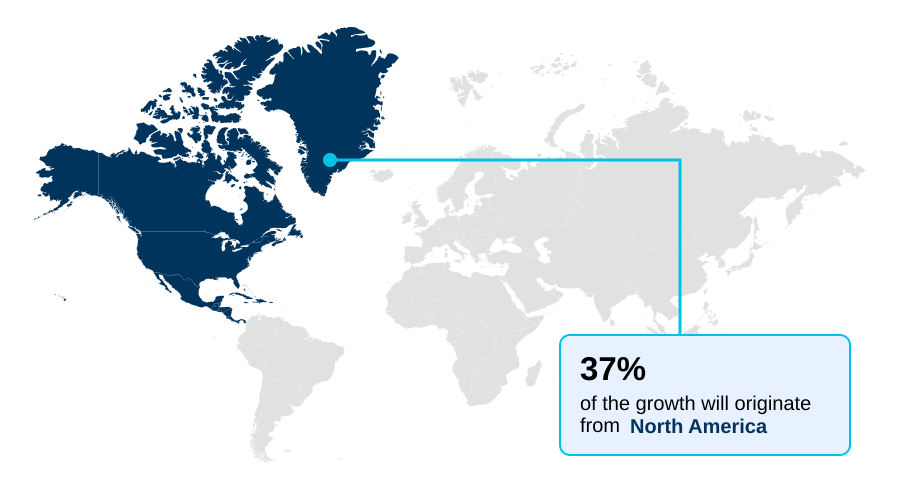

- North America dominated the market and accounted for a 37.2% growth during the forecast period.

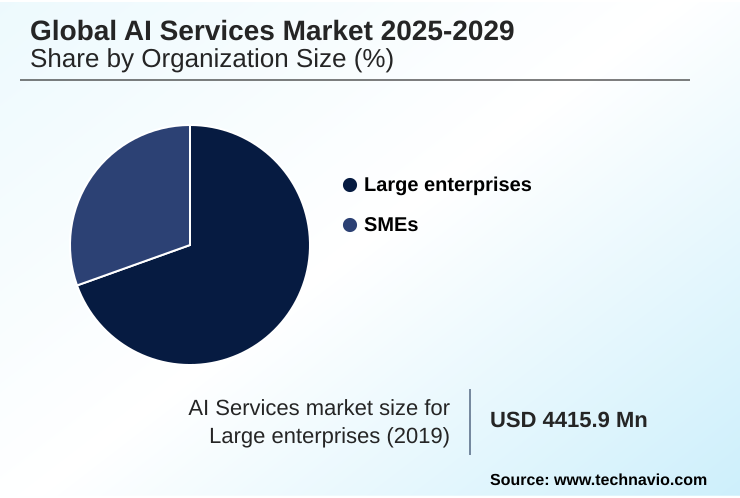

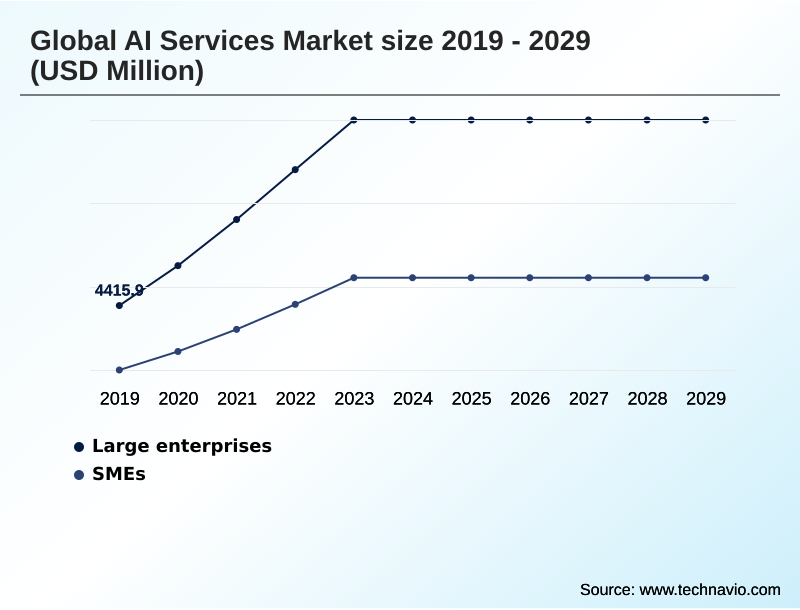

- By Organization Size - Large enterprises segment was valued at USD 11.56 billion in 2023

- By Type - Software as a service segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 129.01 billion

- Market Future Opportunities: USD 112.95 billion

- CAGR from 2024 to 2029 : 43.3%

Market Summary

- The AI services market is undergoing a period of unprecedented and transformative growth, moving beyond niche applications and into the core of mainstream enterprise strategy. This expansion is largely propelled by the maturation and widespread accessibility of artificial intelligence technologies.

- Following a period of intense research and development, the market has reached an inflection point where the practical, commercial application of large language models and other generative systems is not only viable but essential for competitive positioning.

- Businesses across diverse sectors are actively seeking ai services for enterprise workflows to enhance operational efficiency, personalize customer experiences, and unlock new revenue streams. The prevailing trend is a decisive shift from experimental pilot programs to full-scale strategic integration of AI into fundamental business processes, such as ai-powered supply chain route optimization.

- This dynamic is illustrated by the strategies of major technology corporations and a maturing enterprise ai strategy for smes. The market is focused on practical, domain-specific applications that enhance human capability and automate routine tasks across all major business functions, from finance to human resources, requiring a blend of technical AI knowledge and deep domain expertise.

What will be the Size of the AI Services Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the AI Services Market Segmented?

The ai services industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Organization size

- Large enterprises

- SMEs

- Type

- Software as a service

- Platform as a service

- Infrastructure as a service

- End-user

- Healthcare

- BFSI

- Retail

- Manufacturing

- Transportation

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Organization Size Insights

The large enterprises segment is estimated to witness significant growth during the forecast period.

Large enterprises are the primary drivers of market revenue, pursuing strategic ai implementation of enterprise-grade ai solutions to secure competitive advantages. Their adoption extends beyond experimentation, focusing on ai for operational efficiency and the deployment of large language models (llms).

These organizations engage in complex projects, including bespoke ai model development and autonomous systems integration, which necessitates a thorough ai implementation cost analysis.

They leverage ai infrastructure as a service (iaas) for scalability and require robust ai governance frameworks for compliance. This commitment is evidenced by initiatives in ai in financial risk management where firms report a 25% improvement in threat detection accuracy.

The focus is on transformative programs involving ai readiness assessment and mlops platform integration for ai-powered workflow automation.

The Large enterprises segment was valued at USD 11.56 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 37.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI Services Market Demand is Rising in North America Get Free Sample

The geographic landscape is led by North America, where a mature enterprise ai adoption strategy prioritizes ai workload optimization and cloud ai service integration.

Enterprises in this region heavily invest in computer vision systems and ai-driven supply chain optimization, achieving up to a 15% reduction in logistics costs.

The APAC region is the fastest-growing market, with government initiatives accelerating the adoption of federated learning models and custom silicon accelerators.

In Europe, the focus is on regulatory alignment and ai model security, driving demand for solutions that address data poisoning mitigation.

Across all regions, ai systems integration with legacy platforms is a key service requirement, alongside managed ai infrastructure and ai model fine-tuning to create tools like stateful ai assistants for ai for retail personalization.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- As organizations advance their digital transformation journeys, the focus shifts to deploying ai services for enterprise workflows. A central consideration is the cost of implementing large language models, which requires a careful analysis of both infrastructural spend and talent acquisition.

- A critical priority is building secure generative ai applications, which involves a secure ai model lifecycle management approach to protect against emerging threats. The demand for specialized expertise is evident in sectors like healthcare, with a significant increase in projects for ai model development for healthcare.

- Many developers are realizing the benefits of paas for ai development, as it accelerates timelines and simplifies the process of optimizing ai workloads on cloud. The complexities of managing ai infrastructure as a service are driving many to seek specialized partners. Developing a cohesive enterprise ai strategy for smes is becoming crucial for smaller players to remain competitive.

- For larger retailers, scaling ai services for retail is key to enabling ai-driven personalization in e-commerce. Similarly, there are notable generative ai use cases in finance, from automated reporting to client interaction.

- The verticalized ai for manufacturing sector is driving ai predictive maintenance for industry 4.0, where digitally mature factories are now resolving potential equipment failures twice as fast as those using traditional methods. The debate over comparing open-source and commercial llms continues, while regulatory challenges in ai deployment shape implementation choices.

- The use of generative ai for software development is boosting productivity, guided by ethical ai implementation best practices. Finally, ai-powered supply chain route optimization and developing human-centric conversational ai are delivering tangible operational efficiencies and improved customer satisfaction.

What are the key market drivers leading to the rise in the adoption of AI Services Industry?

- The proliferation of generative AI and powerful large language models is a key driver propelling growth and investment in the AI services market.

- The democratization of ai supercomputing access through cloud-based ai platforms is a significant market driver.

- These platforms, often structured as ai platform as a service (paas), enable organizations to leverage powerful natural language processing (nlp) and develop domain-specific ai models without massive upfront investment.

- This trend is fueling data monetization with ai, as companies can now process vast datasets to create verticalized ai solutions. For instance, ai in healthcare diagnostics has shown the ability to analyze medical images 40% faster than manual methods.

- The rise of powerful open-source ai models further spurs innovation, though it also increases the need for model evasion defense and secure ai development.

- This ecosystem is supported by advances in ai-specific semiconductors and allows for greater ai solution customization in tools like conversational ai platforms.

What are the market trends shaping the AI Services Industry?

- A primary trend influencing the market is the proliferation of generative AI, coupled with its accelerating adoption across enterprises for strategic implementation and business process optimization.

- A primary trend is the infusion of generative ai systems into mainstream enterprise software, delivered through accessible ai software as a service (saas) models. This facilitates ai for business process optimization, with firms reporting up to a 30% reduction in cycle times for content creation.

- Concurrently, the demand for predictive analytics models is surging, especially for ai for predictive maintenance in industrial settings, where deployments have cut unplanned downtime by 18%. The pursuit of scalable ai deployment is fueling innovation in machine learning operations (mlops) and the use of ai application development apis.

- This trend emphasizes human-centric ai design and advanced prompt engineering techniques, enabling more intuitive interaction with complex systems like ai-powered digital twins for ai for logistics optimization and algorithmic trading systems which rely on precise data-driven decision making.

What challenges does the AI Services Industry face during its growth?

- Navigating the complex, fragmented, and rapidly evolving regulatory landscape presents a key challenge to the seamless growth of the AI services industry.

- A key challenge is ensuring ai ethics and compliance, as fragmented ai regulatory compliance frameworks create operational hurdles. Enterprises are increasingly demanding trustworthy ai systems and explainable ai (xai), making responsible ai deployment a prerequisite for adoption.

- The scarcity of expertise in areas like ai infrastructure management and ai model lifecycle management inflates costs, with specialist salaries being 50% higher than traditional IT roles. These hurdles are compounded by the technical complexity of establishing data lakehouse architecture needed for ai in smart manufacturing and ai-powered drug discovery.

- While managed ai services can mitigate some of this burden, the industry-wide push for ai talent development is critical for long-term growth and effective implementation of automated quality control and ai-powered customer service systems.

Exclusive Technavio Analysis on Customer Landscape

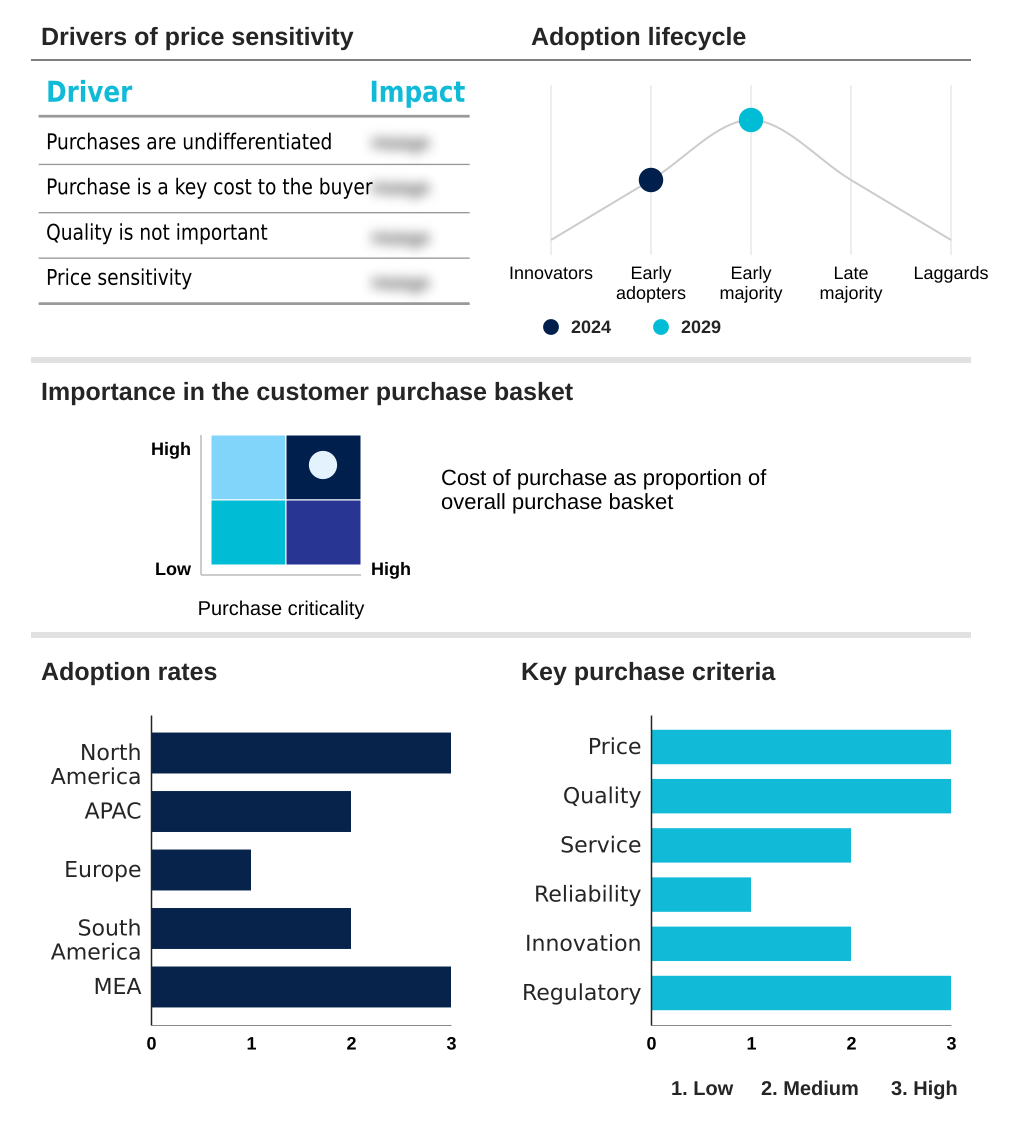

The ai services market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai services market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI Services Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai services market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amazon.com Inc. - Key offerings include managed services, custom model development, and access to scalable AI platforms and APIs for integration into enterprise workflows.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amazon.com Inc.

- Anthropic

- Apple Inc.

- Baidu Inc.

- Cohere

- Crusoe Energy Systems LLC

- Databricks Inc.

- DeepL SE

- Eleven Labs Inc.

- Glean Technologies Inc.

- Google LLC

- Hugging Face

- IBM Corp.

- Lambda Inc.

- Microsoft Corp.

- Mistral AI

- OpenAI

- Stability AI

- Tencent Holdings Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai services market

- In September, 2024, Databricks announced its plan to acquire Tabular, a data management startup, to enhance data lakehouse architectures for large-scale AI.

- In November, 2024, Microsoft announced the general availability of its Security Copilot, an AI assistant designed to augment cybersecurity professionals' capabilities in threat detection and response.

- In January, 2025, the Indian government approved the IndiaAI Mission, a national program with a substantial budget to build a robust domestic AI ecosystem through public-private partnerships.

- In March, 2025, NVIDIA announced its Blackwell architecture, a next-generation platform promising a significant performance increase for AI training and inference workloads, driving the next wave of infrastructure upgrades.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI Services Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 295 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 43.3% |

| Market growth 2025-2029 | USD 112948.6 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 34.5% |

| Key countries | US, Canada, Mexico, China, Japan, India, Australia, South Korea, Indonesia, Germany, UK, France, The Netherlands, Italy, Spain, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI services market is defined by a rapid shift from theoretical applications to practical, value-driven deployments. The proliferation of generative ai systems and large language models (llms) is compelling boardrooms to re-evaluate digital strategies, moving beyond simple ai-driven process automation to full-scale transformation.

- A key boardroom focus is on ai governance frameworks and ai ethics and compliance to navigate risks. This evolution is enabled by a tiered technology stack, starting with ai infrastructure management and the choice between ai infrastructure as a service (iaas) and building on custom silicon accelerators.

- On top of this, cloud-based ai platforms offer ai platform as a service (paas) for bespoke ai model development and ai model fine-tuning. Machine learning operations (mlops) are critical for managing the lifecycle of predictive analytics models and natural language processing (nlp) applications.

- End-user solutions, delivered as ai software as a service (saas), range from conversational ai platforms to verticalized ai solutions for ai-powered drug discovery and algorithmic trading systems. Businesses are implementing ai-driven hyper-personalization and automated quality control using computer vision systems. This creates a need for managed ai services, ai readiness assessment, and prompt engineering techniques to build stateful ai assistants.

- Security, addressed through data poisoning mitigation and model evasion defense, is paramount, as is the demand for explainable ai (xai). This integration, seen in ai-powered digital twins and ai-driven supply chain optimization, leads to tangible outcomes, with some firms achieving a 20% improvement in forecast accuracy.

- The market is maturing towards autonomous systems integration supported by federated learning models and data lakehouse architecture for ai workload optimization.

What are the Key Data Covered in this AI Services Market Research and Growth Report?

-

What is the expected growth of the AI Services Market between 2025 and 2029?

-

USD 112.95 billion, at a CAGR of 43.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Organization Size (Large enterprises, SMEs), Type (Software as a service, Platform as a service, Infrastructure as a service), End-user (Healthcare, BFSI, Retail, Manufacturing, Transportation) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Proliferation of generative AI and large language models, Navigating evolving and fragmented regulatory landscape

-

-

Who are the major players in the AI Services Market?

-

Amazon.com Inc., Anthropic, Apple Inc., Baidu Inc., Cohere, Crusoe Energy Systems LLC, Databricks Inc., DeepL SE, Eleven Labs Inc., Glean Technologies Inc., Google LLC, Hugging Face, IBM Corp., Lambda Inc., Microsoft Corp., Mistral AI, OpenAI, Stability AI and Tencent Holdings Ltd.

-

Market Research Insights

- The AI services market is characterized by a rapid shift toward strategic ai implementation that delivers measurable business outcomes. A focus on ai for operational efficiency is paramount, with deployments in manufacturing yielding an 18% reduction in unplanned downtime through predictive maintenance.

- Enterprises are increasingly adopting a human-centric ai design for ai-powered customer service solutions, which has improved customer satisfaction scores by over 25%. Data monetization with ai is another key dynamic, where data-driven decision making is enhanced by sophisticated analytical models.

- The move toward responsible ai deployment is shaping procurement criteria, as organizations seek trustworthy ai systems that comply with emerging regulations. This is driving demand for ai solution customization and cloud ai service integration to ensure both performance and governance.

We can help! Our analysts can customize this ai services market research report to meet your requirements.

RIA -

RIA -