Enjoy complimentary customisation on priority with our Enterprise License!

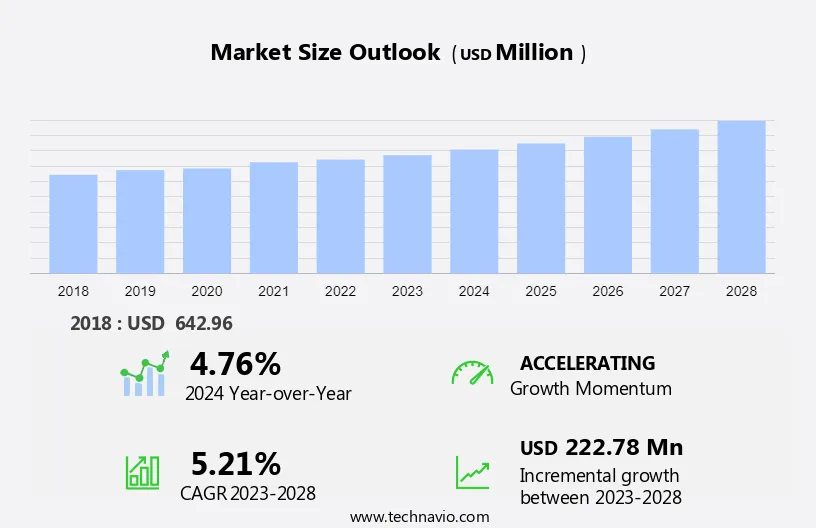

The anti-fog lidding films market size is forecast to increase by USD 222.78 million, at a CAGR of 5.21% between 2023 and 2028. Market growth is propelled by factors such as heightened demand for packaged F&B, increased use of anti-fog lidding films in expanding retail sectors, and widespread adoption of barrier films. The market analysis delves into drivers, trends, and challenges, offering insights into industry growth and development. By examining these elements, stakeholders gain a comprehensive understanding of the market dynamics influencing industry evolution. Our report examines historical data from 2018 - 2022, besides analyzing the current market scenario.

Anti-fog lidding films are specialty plastic films that provide modified atmosphere packaging, which prevents the formation of moisture inside the packaged food container. It also helps enhance the shelf-life of perishable food products such as meats, seafood, dairy products, fresh produce, ready-to-eat food items, bakery and confectionery items, and frozen food products.

To Know more about the market report Request Free Sample

The market is witnessing a surge in demand driven by the increased focus on food preservation and packaging. Consumers and industries alike are adopting advanced packaging solutions like Anti-fog films to enhance product visibility and ensure longer shelf life. The market trends include the rising popularity of high-barrier films for optimal protection against moisture, contamination, and spoilage. However, challenges lie in balancing the need for heat resistance with environmental concerns, pushing the industry towards sustainable packaging solutions. The market reflects the ongoing quest for innovative materials addressing diverse packaging needs, particularly in the dairy and frozen foods sectors. Our researchers analyzed the market research and growth data with 2023 as the base year, along with the key market growth analysis, trends, and challenges. A holistic analysis of drivers, trends, and challenges will help companies refine their marketing strategies to gain a competitive advantage.

Increasing demand for anti-fog lidding films from the growing retail sector is notably driving the market. Continuous advancements in the global retail industry are set to fuel the expansion of the market. Modern consumers, with their busy lifestyles, increasingly seek comfort and convenience. Major and well-organized retail establishments offer a diverse array of products, including household items, consumer appliances, furnishings, personal care products, and home decor items, representing various brands all under one roof with longer shelf life. The surging brand consciousness among consumers has heightened the significance of organized retailers providing an extensive selection of branded and packaged goods.

Additionally, polyethylene (PE), polyethylene terephthalate (PET), polyamide, and polypropylene (PP) polymers are used in the anti-fog lidding films. E-commerce and online retailing stand out as pivotal sectors within the retail industry. The growing prevalence of the Internet and smart devices is enhancing accessibility to online shopping platforms. Retailers and companies leverage these platforms to extend their reach and connect with a broader consumer base. The expansion of the e-commerce consumer base and the high barrier film penetration in e-commerce companies are expected to drive the demand globally, which will further drive the global market during the forecast period.

Integration of smart packaging technologies is an emerging trend in the market. The global market is undergoing an increase with the incorporation of smart packaging technologies, most notably quick response (QR) codes and Near Field Communication (NFC) tags. In addition, this movement underscores the industry's overall commitment to improving traceability, encouraging information exchange, and increasing consumer participation.

Moreover, smart packaging, powered by QR codes and near-field communication (NFC) tags, provides a dynamic interaction between the product and the consumer. In addition, QR codes, when scanned with a smartphone, allow fast access to detailed product information such as sourcing, nutritional statistics, and usage instructions. Furthermore, this transparency not only meets the growing consumer demand for information but also fosters trust in the company. Hence, such factors are driving the market during the forecast period.

Evolving consumer demands for alternative packaging materials is a major challenge hindering the market. The global market is witnessing medium competition from several conventional packaging films and paper and aluminum films. In addition, the increasing consumer tastes and requests for alternative packaging materials have a significant impact on the global market.

Moreover, as consumer awareness of environmental sustainability and eco-friendly options rises, there is a greater demand for packaging solutions that reflect these ideals. In addition, this rise in demand for ecologically friendly products puts the market under pressure to respond quickly to changing consumer needs. Furthermore, consumers increasingly want packaging materials that are biodegradable, recyclable, or derived from renewable resources. Hence, such factors are hindering the market during the forecast period.

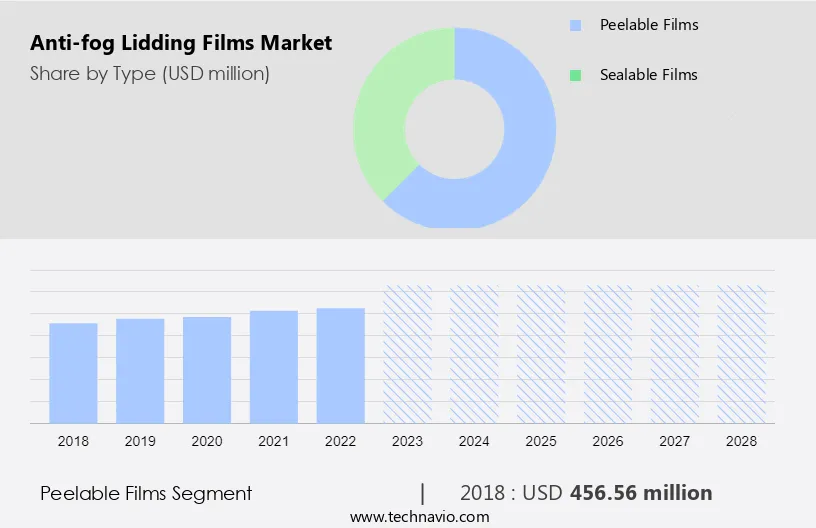

The peelable films segment is estimated to witness significant growth during the forecast period. The peelable films segment emerged as a major type in the global market as the peelable segment offers handy and easy-to-open package options, improving consumer experience and product accessibility. In addition, the peelable segment is growing in popularity due to the food industry's need for user-friendly packaging, notably for ready-to-eat meals and snacks.

Get a glance at the market contribution of the End User segment Request Free Sample

The peelable films segment was the largest segment and was valued at USD 456.56 million in 2018. Moreover, manufacturers are working to create upgraded peelable films with stronger seals and better barrier qualities. For example, Amcor plc (Amcor) offers peelable lidding films to meet the requirement for secure yet accessible packaging. In addition, peelable films are also growing in popularity in the pharmaceutical industry since they are commonly used to package medical devices and pharmaceutical products. Furthermore, companies such as Uflex Ltd. (Uflex) provide peelable films for pharmaceutical packaging, ensuring product safety and convenience of use. Hence, such factors are fuelling the growth of this segment which in turn drives the market during the forecast period.

Based on the material, the market has been segmented into PE, PP, PET, EVOH, and others. The PE segment will account for the largest share of this segment. The polyethylene (PE) segment has superior resistance to most solvents. Therefore, it is the most prevalent plastic material used to manufacture anti-fog lidding films. In addition, other factors leading to the high adoption of PE include its low cost, conformability, and sealing ability. Furthermore, PE is a viable option for use with other materials, such as polypropylene ( PP) and ethylene vinyl alcohol (EVOH), to enhance the performance characteristics of the anti-fog lidding films. Hence, such factors are fuelling the growth of this segment which in turn drives the market during the forecast period.

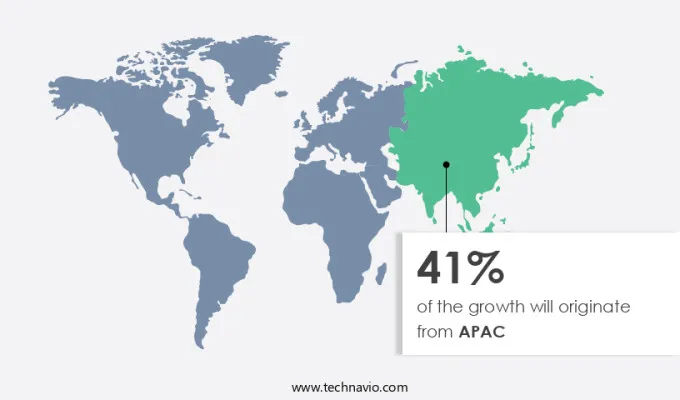

APAC is estimated to contribute 41% to the growth of the global market during the projection period. Technavio's analysts have provided extensive insight into the market forecasting, detailing the regional trends and drivers influencing the market's trajectory throughout the projection period.

For more insights on the market share of various regions Request Free Sample

The market in APAC will have a higher growth rate compared with other regions due to the increasing demand for anti-fog lidding films from the packaged food industry in the region. In addition, the packaged food industry in APAC is expected to expand in the coming years. Moreover, rapid urbanization in India and China has led to an increase in the number of working people who are the major consumers of packaged food products. In addition, according to the World Bank Group, the gross national income (GNI) per capita in China was around 17 trillion in 2022. Therefore, economic growth and the consumer demand for packaged food drive the need to ensure food safety and quality throughout the food supply chain. Hence, such factors are driving the market in APAC during the forecast period.

Companies are implementing various market growth and forecasting strategies by analyzing factors such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product or service launches to enhance their presence in the market.

The report also includes detailed analyses of the competitive landscape of the market and information about 15 market companies, including:

Effegidi International S.p.A., Ester Industries Ltd., FLEXOPACK SA, KP Holding GmbH and Co. KG, Mondi Plc, Plastopil Hazorea Co. Ltd., ProAmpac Holdings Inc., Sappi Rockwell Solutions Limited, Sealed Air Corp., Toray Industries Inc., Transcendia Inc., UFlex Ltd., Vishakha Polyfab Pvt. Ltd., Wipak Group, Amcor plc, Berry Global Inc., FLAIR Flexible Packaging Corp., and Garware Hi Tech Films Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

The market report predicts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and growth opportunities from 2018 to 2028.

The market is witnessing significant growth driven by the increasing demand for anti-fog film and high-barrier film solutions. These films effectively prevent fogging on containers and trays, ensuring a longer shelf life for various food products. With the rise in consumer awareness about food wastage and food contamination, there's a growing need for packaging materials that offer superior protection against spoilage.

Moreover, manufactured using materials like polyethylene terephthalate (PET) and polyamide, these films cater to diverse applications in the food industry, including packaging for frozen foods, meat, poultry, and ready-to-eat products in bakeries. By minimizing the formation of water droplets, they enhance the appearance of packaged goods, crucial for maintaining product freshness during long-distance transportation. The antifog lidding film market addresses the demand for packaging solutions that provide both heat resistance and tensile strength while ensuring UV and temperature stability.

However, the major players in the industry continually innovate and launch new products to capitalize on emerging trends. With a focus on resealable films for meat, poultry, and seafood, the market presents lucrative growth opportunities, especially in the fresh produce segment and home delivery services for high-moisture foods. In-depth market trend analysis and segmentation highlight the growing significance of anti-fog lidding films across confectionery, bakery, and meat poultry product industries.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

178 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.21% |

|

Market Growth 2024-2028 |

USD 222.78 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.76 |

|

Regional analysis |

APAC, Europe, North America, Middle East and Africa, and South America |

|

Performing market contribution |

APAC at 41% |

|

Key countries |

US, China, India, South Korea, Germany, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Coveris Management GmbH, Effegidi International S.p.A., Ester Industries Ltd., FLEXOPACK SA, KP Holding GmbH and Co. KG, Mondi Plc, Plastopil Hazorea Co. Ltd., ProAmpac Holdings Inc., Sappi Rockwell Solutions Limited, Sealed Air Corp., Toray Industries Inc., Transcendia Inc., UFlex Ltd., Vishakha Polyfab Pvt. Ltd., Wipak Group, Amcor plc, Berry Global Inc., FLAIR Flexible Packaging Corp., and Garware Hi-Tech Films Ltd. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, and Market condition analysis for the forecast period. |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Type

7 Market Segmentation by Material

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights