Enjoy complimentary customisation on priority with our Enterprise License!

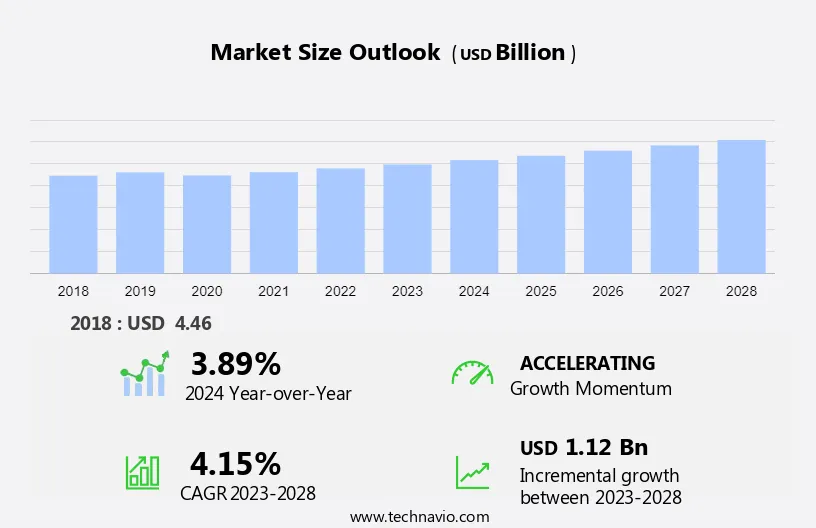

The Automotive Aftermarket Shock Absorbers Market size is forecast to increase by USD 1.12 billion, at a CAGR of 4.15% between 2023 and 2028. Market expansion is propelled by multiple factors, chief among them being the aging vehicle fleet with a substantial number of in-use vehicles, necessitating replacements and upgrades. Moreover, there is a notable surge in vehicle miles driven, indicating heightened mobility requirements and driving the demand for automotive products and services. Additionally, the uptick in sales of luxury vehicles further fuels market growth, reflecting evolving consumer preferences and increasing purchasing power. These combined factors create a conducive environment for market acceleration, presenting opportunities for industry players to capitalize on the growing demand and cater to diverse customer needs in the automotive sector. The report provides market size, historical data spanning from 2018-2022, and future projections, all presented in terms of value in USD billion for each of the mentioned segments.

For More Highlights About this Report, Download Free Sample in a Minute

In the realm of vehicle handling and seating, automotive shock absorbers are pivotal components, ensuring optimal aerodynamics and ride comfort. Employed by automakers worldwide, they mitigate the impact of bumps or speed breakers encountered by passenger cars and light trucks. Operating through a hydraulic system comprising valves and springs, shock absorbers regulate bounce and roll, enhancing suspension and tire contact with the road. Essential across various sectors, from motorcycles to industrial machinery, these components play a vital role in vehicle performance and contribute to advancements in automotive engineering and materials science. Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

An increase in vehicle miles driven is the key factor driving the market. The average vehicle miles driven has been witnessing an upsurge since the start of the current decade. The emergence of shared mobility services, the increase in commercial vehicle traveling due to the rise in trade volume and growth of the e-commerce sector, and consumer tendency to travel are the key factors driving the average vehicle miles driven per year. Enhanced accessibility of shared mobility services and low cost of vehicle users compared with vehicle ownership are shifting consumer preference from vehicle ownership to shared mobility services. Automakers utilize hydraulic fluid in their machinery to ensure smooth operation and efficient performance, contributing to the reliability and functionality of their production processes.

The wear and tear of vehicles increases with the rise in vehicle miles driven. Tires, suspension systems, and hydraulic system components are some of the major components hampered by the increase in vehicle miles driven. In a suspension system, shock absorbers are continuously subjected to vibrations and movement of components, which are attributed to uneven road surfaces. The components of automotive shock absorbers are operated under cyclic thermal and mechanical loading. In some cases, due to loss of shock-absorbing capability, bounce and roll roads and uneven road surfaces can lead to the bending of the piston rod. In such scenarios, vehicle shock absorbers are replaced, thus fueling the global automotive aftermarket shock absorbers market during the forecast period.

The emergence of additive manufacturing is the primary trend in the market. Additive manufacturing technology, also known as 3D printing, is a manufacturing technology used to manufacture 3D objects from computer-aided design models. The automotive industry is one of the significant contributors to the additive manufacturing industry. The increasing manufacturing cost, especially for the products that have a complex design and are manufactured in low volumes, offers immense potential for additive manufacturing. Manufacturers are adopting additive manufacturing technologies to manufacture complex and advanced automotive components.

Furthermore, technology helps develop and manufacture intricate designs for products. This has resulted in opportunities to develop with advanced design and material composition. It also helps develop lightweight and effective shock absorbers. Due to the advantages associated with manufacturing, additive manufacturing technology is anticipated to witness rapid adoption by auto component manufacturers in the future. This technological advancement will boost the market during the forecast period.

Availability of inexpensive and low-quality products is the major challenge that affects market expansion. Price is a key factor when purchasing automotive components in the aftermarket. Consumers from low-income economies such as India, China, and Egypt, as well as countries from Africa and South America, are more inclined toward low-cost automotive components. These low-cost components have low quality and performance characteristics compared with OEM standard aftermarket products; however, their lower cost attracts numerous consumers toward them. India and China are the leading global hubs for automotive components manufacturing and sales.

Consequently, the shift of consumers from these countries toward low-cost aftermarket products hampers the revenue and profit margins of well-established OEM quality auto component manufacturers. Furthermore, counterfeiting of auto components is also a major challenge faced by organized players. Counterfeit products are disrupting the automotive shock absorber aftermarket and creating a bottleneck for the growth of organized players operating in the market. Thus, such factors may impede market growth during the forecast period.

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report also includes detailed analyses of the competitive landscape of the market and information about 20 market companies, including:

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

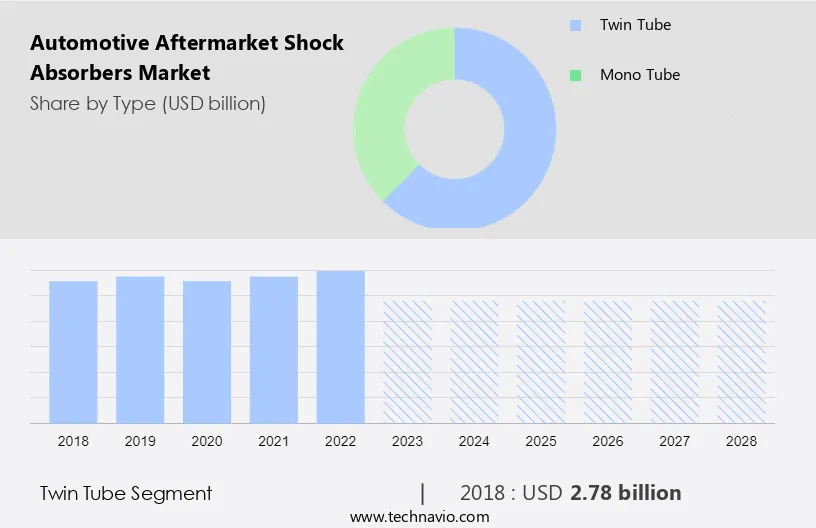

The twin tube segment is estimated to witness significant growth during the forecast period. Twin-tube shock absorber type of shock absorber consists of two tubes, an inner and an outer tube, with a piston and oil-filled chamber in between. The inner tube is where the piston moves up and down, while the outer tube serves as a reservoir for the oil. This design allows for better heat dissipation and improved performance, making twin-tube shock absorbers a preferred choice for many vehicle owners.

Get a glance at the market contribution of various segments Download the PDF Sample

The twin tubes segment was the largest segment and was valued at USD 2.78 billion in 2018. Additionally, the market is witnessing significant growth, driven by the increasing demand for high-performance and customizable products. The popularity of twin-tube shock absorbers, with companies like Gabriel India and KYB leading the way, is a testament to the importance of innovation and quality in this market. As the automotive industry continues to evolve, the segment is expected to grow. Thus, the market will witness growth during the forecast period.

For more insights on the market share of various regions Download PDF Sample now!

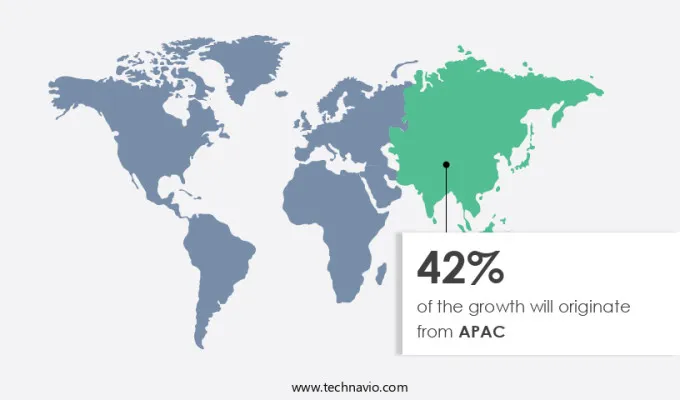

APAC is estimated to contribute 42% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period. The improved and stabilized socioeconomic conditions in APAC countries, especially China and India, are contributing to the growth of the automotive industry in this region. A large consumer base with increasing per capita income and the ease of availing of financing services have been fueling the demand for passenger and commercial vehicles in the region.

Further, China, Japan, and India are the global leaders in automobile manufacturing. The low cost of vehicles due to the presence of vehicle manufacturers, coupled with the increasing per capita income of individuals across the region, is fueling the demand for vehicles. Furthermore, APAC accounts for about half of the vehicle production in the world. A large number of vehicles produced in APAC are exported to various countries across the globe. Low labor costs, availability of skilled labor, and a large consumer base across the region are likely to boost the production of vehicles in APAC during the forecast period.

The market report forecasts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and growth opportunities from 2018 to 2028.

The market plays a critical role in enhancing vehicle performance and ensuring a comfortable ride for cars, light trucks, and motorcycles. These components are vital for automotive engineering, managing the impact of bumps or speed breakers and maintaining stability on roads and off-road terrains. Utilizing advanced materials science, modern shock absorbers employ innovative designs with pistons, springs, and valves to regulate hydraulic fluid flow within the suspension system. As a result, they optimize handling, seating comfort, and aerodynamics, contributing to overall vehicle safety and performance.

Further, the market is witnessing significant growth driven by the increasing demand for balanced rides and enhanced vehicle control across various segments including passenger cars, SUV trucks, heavy vehicles, and E-vehicles. Advanced suspension systems with features like damping control, air springs system, and electronic control unit (ECU) are becoming more prevalent to address challenges such as brake dive and acceleration squat. Manufacturers are incorporating air shock absorbers, hydraulic shock absorbers, and gas-charged shock absorbers to optimize vertical loads and ensure a smoother driving experience. Additionally, the market is witnessing innovations in smart shock absorbers with actuators, sensors, and microprocessors for self-regulating performance and improved vehicle handling.

Furthermore, the market is evolving rapidly with the surge in demand for E-vehicles, pickup trucks, and vans. Transmissions and powertrain parts play crucial roles in optimizing vehicle performance, while OEM suppliers ensure quality components. Tires remain integral for a balanced ride and effective braking, while innovations like air dumpers and automatic auxiliary suspensions enhance control. Raw materials such as rubber, carbon, and silicon are essential for manufacturing, along with plastic and activated carbon for advanced applications. Off-road vehicles and commercial trucks benefit from variable damping systems, leveraging technologies like data analytics and machine learning for improved performance and reduced CO2 emissions.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

167 |

|

Base year |

2023 |

|

Historic period |

2018 - 2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.15% |

|

Market growth 2024-2028 |

USD 1.12 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.89 |

|

Regional analysis |

APAC, Europe, North America, South America, and Middle East and Africa |

|

Performing market contribution |

APAC at 42% |

|

Key countries |

US, China, Japan, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

ADD Industry Zhejiang Co Ltd, AL-KO Vehicle Technology Group, ANAND Group, Arnott LLC, Dorman Products Inc., DRiV Inc., Festo SE and Co. KG, Hangzhou Smart Mfg Group Co. Ltd., Hitachi Ltd., KAVO B.V., KYB Corp., MAPCO Autotechnik GmbH, MEYLE AG, Roberto Nuti Group, Skyjacker Ltd., SUSPA GmbH, Taylor Devices Inc., Tenneco Inc., thyssenkrupp AG, and ZF Friedrichshafen AG |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for the forecast period. |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this market research report to meet your requirements.

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Type

7 Market Segmentation by Vehicle Type

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights