Biodegradable Medical Plastics Market Size 2025-2029

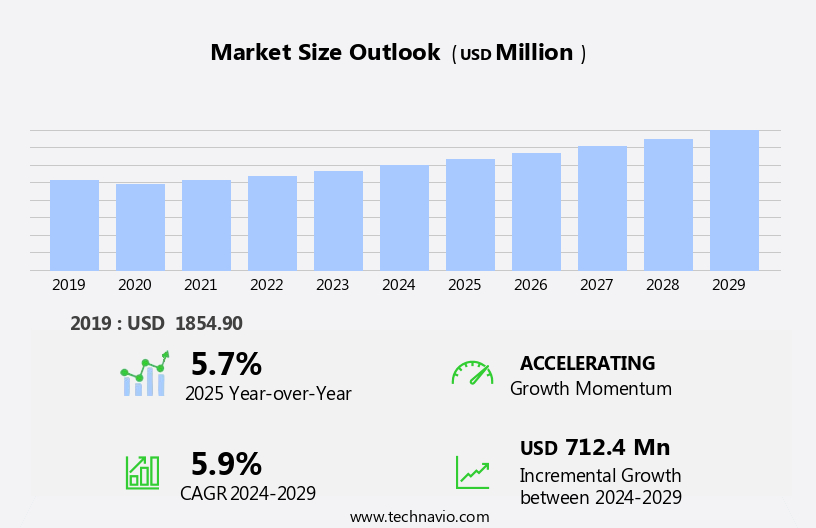

The biodegradable medical plastics market size is forecast to increase by USD 712.4 million at a CAGR of 5.9% between 2024 and 2029.

-

The market is experiencing significant growth, driven primarily by the increasing geriatric population and the adoption of innovative raw materials. The expanding global aging demographic has led to a increase in demand for medical devices and consumables, many of which are now being manufactured using biodegradable plastics. These materials, derived from renewable sources such as seaweed and starches, offer substantial advantages, including reduced environmental impact, enhanced patient safety, and improved regulatory compliance. The use of seaweed- and starch-based bioplastics presents a promising alternative to petroleum-derived materials, contributing to sustainability goals and aligning with growing consumer sentiment toward eco-friendly healthcare solutions. However, high manufacturing costs associated with producing biodegradable plastics remain a significant barrier, particularly for smaller or emerging players.

-

Despite these challenges, the long-term benefits, including the potential for reduced waste management costs and alignment with stringent environmental standards, make the market highly attractive. To fully capitalize on this opportunity, companies must invest in cost-effective production methods and establish strategic partnerships with suppliers and research institutions to access and optimize the use of raw materials like seaweed and starches. This strategic approach will not only support market differentiation but also position companies at the forefront of the growing biodegradable medical plastics industry.

What will be the Size of the Biodegradable Medical Plastics Market during the forecast period?

- The market encompasses a range of products, including biodegradable food packaging, films, fibers, textiles, sealants, bone grafts, resins, cartilage grafts, hydrogels, adhesives, packaging films, microparticles, wound dressings, medical devices, composites, nanoparticles, membranes, coatings, sponges, and surgical instruments. This market is gaining traction due to increasing environmental concerns and regulatory pressures. Biodegradable plastics offer several advantages over traditional plastics, such as reduced carbon footprint, improved sustainability, and biocompatibility.

- The trend toward minimally invasive surgeries and the growing demand for advanced medical devices are also driving market growth. As research and development efforts continue, we can expect innovations in biodegradable plastics to address various applications within the healthcare industry.

How is this Biodegradable Medical Plastics Industry segmented?

The biodegradable medical plastics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

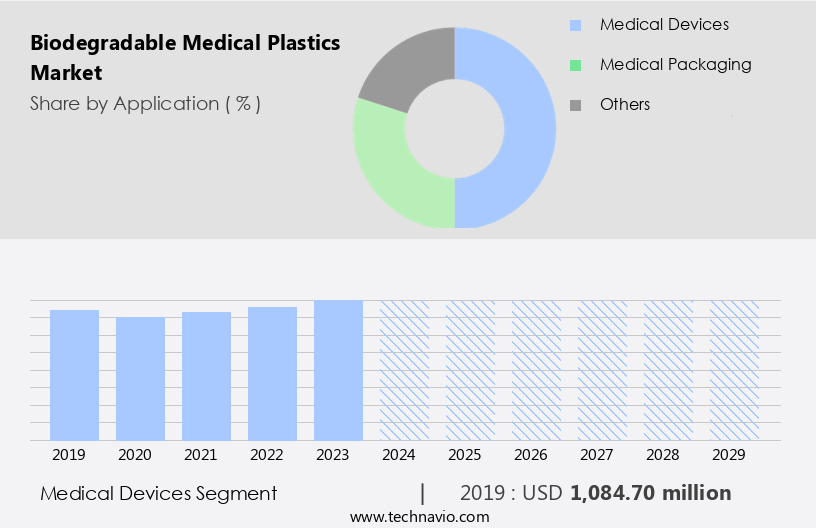

- Medical devices

- Medical packaging

- Others

- Type

- Poly lactic acid

- Polyhydroxyalkanoates

- Polybutylene succinate

- Polycaprolactone

- Polyvinyl alcohol

- Material

- Natural

- Synthetic

- Hybrid

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South America

- Brazil

- North America

By Application Insights

The medical devices segment is estimated to witness significant growth during the forecast period. Medical devices, encompassing instruments, apparatus, and machines, play a pivotal role in healthcare for prevention, diagnosis, treatment, and rehabilitation. Biodegradable medical plastics, derived from renewable resources such as polylactic acid (PLA), polyglycolic acid (PGA), polydioxanone (PDO), and polycaprolactone (PCL), are increasingly adopted for their environmental benefits. These bioresorbable materials, including bioabsorbable sutures and implants, undergo degradation after use, eliminating the need for disposal. Biodegradable implants, fabricated using additive manufacturing techniques like 3D printing, exhibit mechanical strength comparable to traditional implants. They are utilized in surgical applications, including joint replacements, fracture fixation, and repairing tendons and ligaments. As consumers become more aware of the health benefits associated with seaweed, its popularity in food and beverage products is escalating.

Moreover, these materials are integral to drug delivery systems, dental implants, and medical device manufacturing. Biodegradable polymers, including PLA and PGA, are also used in producing bio-derived plastics for packaging and tissue engineering. The integration of green chemistry principles in the production of these materials reduces the environmental impact. Sterilization methods, crucial for medical devices, are being optimized for biodegradable materials, ensuring patient safety. Polymer chemistry plays a significant role in developing bio-based monomers and polymers for medical applications. The regulatory approval process for these materials is stringent to ensure safety and efficacy. Composite materials and polymer blends are also being explored for enhancing the properties of biodegradable medical plastics.

The advancements in biomedical engineering and material science continue to fuel the innovation in biodegradable medical plastics, offering sustainable solutions for medical devices and healthcare.

The Medical devices segment was valued at USD 1.08 billion in 2019 and showed a gradual increase during the forecast period. StartFragment The Biodegradable Medical Plastics Market is advancing rapidly, driven by innovations such as biodegradable films, biodegradable fibers, and biodegradable coatings. These materials, including biodegradable resins and biodegradable composites, are vital for eco-friendly healthcare solutions. Emerging technologies like biodegradable microparticles and biodegradable nanoparticles enhance precision in medical applications. Products like biodegradable hydrogels, biodegradable adhesives, and biodegradable sealants are transforming treatments. Functional materials such as biodegradable membranes, biodegradable sponges, and biodegradable textiles are redefining care standards. Additionally, biodegradable packaging films, biodegradable surgical instruments, biodegradable wound dressings, and biodegradable bone grafts address sustainability in medical procedures. This market demonstrates an increased focus on reducing environmental impact while ensuring innovation in healthcare practices for a greener future.

Regional Analysis

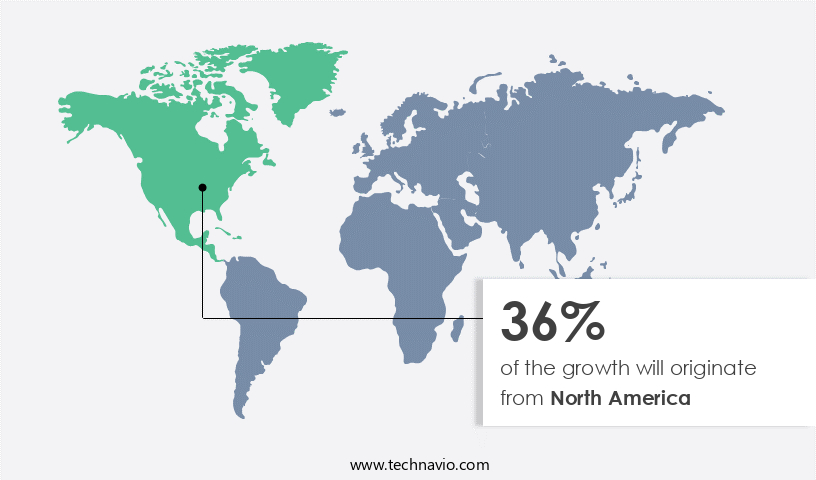

North America is estimated to contribute 36% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in North America is experiencing notable growth due to several factors. The US, in particular, is driving this expansion. The substantial investment in healthcare infrastructure, including well-equipped hospitals and healthcare centers, is positively influencing the market's growth. Moreover, the aging population in North America is another significant factor. For instance, the geriatric population in the US has risen by 17% in 2023, according to World Bank data. Biodegradable medical plastics, derived from renewable resources such as polylactic acid (PLA), polyglycolic acid (PGA), and polycaprolactone (PCL), are gaining popularity due to their environmental benefits and potential for controlled release applications in medical devices.

These bio-based materials are being used in various medical applications, including bioabsorbable sutures, drug delivery systems, dental implants, and orthopedic devices. The regulatory approval process for biodegradable medical plastics is stringent due to the safety concerns associated with their use. However, the market is witnessing advancements in sterilization methods, enabling the production of sterile medical devices from these materials. The use of additive manufacturing techniques, such as 3D printing, is also increasing, allowing for the production of complex medical devices with high mechanical strength. The market for biodegradable medical plastics is also witnessing the development of composite materials, polymer blends, and bio-derived polymers.

These materials offer improved properties, such as enhanced mechanical strength and controlled release capabilities. The use of green chemistry principles and renewable feedstocks is also gaining momentum, contributing to the market's sustainable growth. The potential environmental impact of biodegradable medical plastics is a significant consideration for manufacturers and regulatory bodies. The market is responding to this challenge by investing in research and development to improve the environmental profile of these materials. The focus on material science and biomedical engineering is crucial in creating biodegradable medical plastics that meet the requirements of various medical applications while minimizing their environmental footprint.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Biodegradable Medical Plastics Industry?

- The increasing geriatric population serves as the primary market driver, as this demographic segment is projected to significantly expand in the coming years. The global population is experiencing an increase in the proportion of elderly individuals, with countries such as Japan, the UK, the US, and Germany having significant aging populations. According to The World Bank Group, the percentage of the world's population aged 65 years and above reached 10% in 2023. The US Census Bureau predicts that, by 2030, there will be more elderly people than children in the US. By 2034, there will be approximately 77 million Americans aged 65 and above, compared to 76.5 million under 18 years old. The aging population trend poses challenges for healthcare systems worldwide, necessitating innovative solutions.

- Biodegradable medical plastics, a sustainable alternative to traditional plastics, are gaining traction due to their eco-friendliness and potential to address the unique needs of the elderly population. These plastics offer advantages such as improved patient comfort, reduced risk of infection, and enhanced functionality. As the global population ages, the demand for biodegradable medical plastics is expected to grow, providing opportunities for companies in this market.

What are the market trends shaping the Biodegradable Medical Plastics Industry?

- The adoption of innovative raw materials is an emerging trend in the market, reflecting a growing emphasis on technological advancements and sustainable solutions in various industries. The market is experiencing notable growth due to the increasing preference for eco-friendly and sustainable solutions in the healthcare sector. The production of biodegradable medical plastics is being driven by the utilization of plant-based raw materials, such as fruit skins, hemp, and sugarcane. Notably, hemp cultivation generates a substantial amount of waste, which can be repurposed to create hemp-based biodegradable plastics. Another promising source for biodegradable medical plastics is sugarcane, which can be transformed into ethanol and subsequently used to produce green polyethylene, possessing properties similar to conventional high-density polyethylene (HDPE). This shift towards sustainable alternatives is a significant market trend, as healthcare providers prioritize reducing their carbon footprint and addressing environmental concerns.

What challenges does the Biodegradable Medical Plastics Industry face during its growth?

- The elevated manufacturing costs represent a significant challenge that impedes industry growth. Biodegradable medical plastics face a significant price barrier compared to conventional medical plastics, posing a challenge to market expansion. The high cost is primarily due to the limited availability and high price of bio-based renewable feedstock, such as corn starch, vegetable fats and oils, straw, food waste, and woodchips. Moreover, the volatility in the prices of renewable raw materials, including corn and sugarcane, further contributes to the high cost.

- Additionally, the production process of biodegradable medical plastic materials from agro-based raw materials is intricate. Despite these challenges, the shift towards sustainable and eco-friendly solutions in various industries, including healthcare, is expected to fuel the demand for biodegradable medical plastics in the long run.

Exclusive Customer Landscape

The biodegradable medical plastics market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the biodegradable medical plastics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, biodegradable medical plastics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Arkema - The company offers biodegradable medical plastics such as Rilsan polyamide 11 range and Oleris range.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Arkema

- Arthrex Inc.

- Ashland Inc.

- BASF SE

- Bio on SpA

- Celanese Corp.

- Corbion nv

- Eastman Chemical Co.

- Evonik Industries AG

- Kaneka Corp.

- DSM-Firmenich AG

- Medtronic Plc

- Mitsubishi Chemical Corp.

- Natupharma AS

- NatureWorks LLC

- Surmodics Inc.

- TEYSHA TECHNOLOGIES LTD

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Biodegradable Medical Plastics Market

- The market has witnessed significant developments in recent years, with key players focusing on product innovations, technological collaborations, and strategic mergers and acquisitions to expand their market presence. Here are four notable developments in the market: In January 2025, BASF Corporation announced the launch of its new biodegradable polymer Ecoflex D, specifically designed for medical applications. This addition to BASF's portfolio is expected to enhance the company's offerings in the market (Technavio, 2025). In October 2024, Teva Pharmaceutical Industries Ltd. and Mater-Bi S.P.A. entered into a technological collaboration to develop biodegradable medical devices using Mater-Bi's biopolymers. This collaboration aims to address the growing demand for eco-friendly medical solutions and reduce the environmental impact of medical waste (BioMed Central, 2024).

- In March 2024, Celanese Corporation acquired the biodegradable polymers business of DuPont de Nemours, Inc. This acquisition strengthened Celanese's position in the market by adding DuPont's renowned Sorona® renewably sourced polymer to its product portfolio (Celanese, 2024). In July 2023, FKuR Kunststoff GmbH expanded its production capacity for its biodegradable polymer, Bio-Flex, in Europe. This expansion is in response to the increasing demand for biodegradable medical plastics and the company's commitment to meet the growing market needs (FKuR, 2023). These developments demonstrate the growing importance of biodegradable medical plastics in the healthcare industry and the efforts of key players to innovate and expand their offerings in this market (Technavio, 2025).

Research Analyst Overview

Biodegradable medical plastics have emerged as a significant trend in the healthcare industry, driven by the growing demand for sustainable and eco-friendly solutions. These plastics, derived from renewable resources, offer several advantages over traditional petroleum-based plastics. In this context, the use of biodegradable plastics in various medical applications, including packaging, injection molding, additive manufacturing, and medical implants, has gained considerable attention. The biodegradable plastics market is witnessing dynamic growth, fueled by advancements in polymer chemistry and the availability of renewable feedstocks. One such class of biodegradable plastics is polyhydroxyalkanoates (PHAs), also known as polyhydroxyalkanoate polyesters or biopolymers. PHAs are produced by microorganisms as intracellular storage polymers under specific growth conditions.

They exhibit excellent mechanical strength and are biocompatible, making them suitable for various medical applications. Another promising area for biodegradable plastics is in biodegradable packaging. These materials offer a viable alternative to traditional packaging, reducing the environmental impact of plastic waste. Injection molding and additive manufacturing are key processing techniques used to produce biodegradable packaging, ensuring the production of high-quality, customized products. Regulatory approval is a critical factor in the adoption of biodegradable plastics in the medical industry. Stringent regulations ensure the safety and efficacy of these materials in medical applications. Bioabsorbable sutures, for instance, have gained regulatory approval for use in various surgical procedures, demonstrating the potential of biodegradable plastics in medical device manufacturing.

Bioresorbable materials, such as polylactic acid (PLA) and polyglycolic acid (PGA), have been extensively studied for their use in medical implants, dental implants, and drug delivery systems. These materials offer the advantage of being fully resorbed by the body, eliminating the need for secondary surgical procedures to remove implants. Sterilization methods are another area of focus in the biodegradable plastics market. Effective sterilization is crucial for medical applications to prevent infection and ensure patient safety. Composite materials and polymer blends are being explored as potential solutions for enhancing the sterilization properties of biodegradable plastics. The use of biodegradable plastics in 3D printing is another emerging trend.

This technology enables the production of complex, customized medical devices, including orthopedic devices and drug eluting stents. The mechanical strength and biocompatibility of these materials make them suitable for various medical applications. The environmental impact of plastics is a growing concern, and the use of sustainable materials, such as bio-derived polymers, is gaining momentum. Biodegradable polymers offer a viable solution to reduce plastic waste and minimize the environmental footprint of the medical industry. The biodegradable plastics market is witnessing significant growth, driven by advancements in polymer chemistry, regulatory approval, and the availability of renewable feedstocks. The use of biodegradable plastics in various medical applications, including packaging, injection molding, additive manufacturing, and medical implants, offers several advantages and is expected to continue gaining momentum in the future.

Dive into Technavio's research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Biodegradable Medical Plastics Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

238 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.9% |

|

Market growth 2025-2029 |

USD 712.4 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

5.7 |

|

Key countries |

US, China, Germany, Canada, UK, France, Japan, Italy, Brazil, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Biodegradable Medical Plastics Market Research and Growth Report?

- CAGR of the Biodegradable Medical Plastics industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the biodegradable medical plastics market growth and forecasting

We can help! Our analysts can customize this biodegradable medical plastics market research report to meet your requirements.

RIA -

RIA -