Biopolymer Packaging Market Size 2026-2030

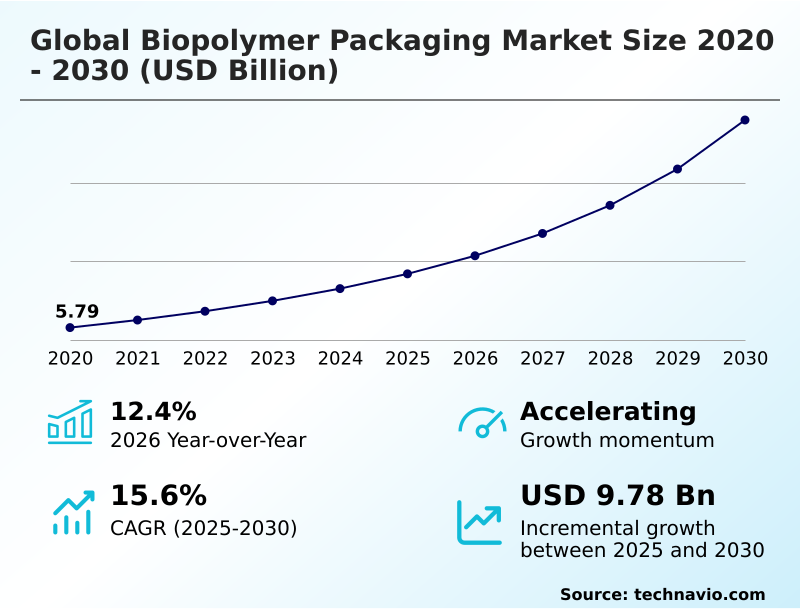

The biopolymer packaging market size is valued to increase by USD 9.78 billion, at a CAGR of 15.6% from 2025 to 2030. Increasingly stringent government regulations and policies will drive the biopolymer packaging market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 64.2% growth during the forecast period.

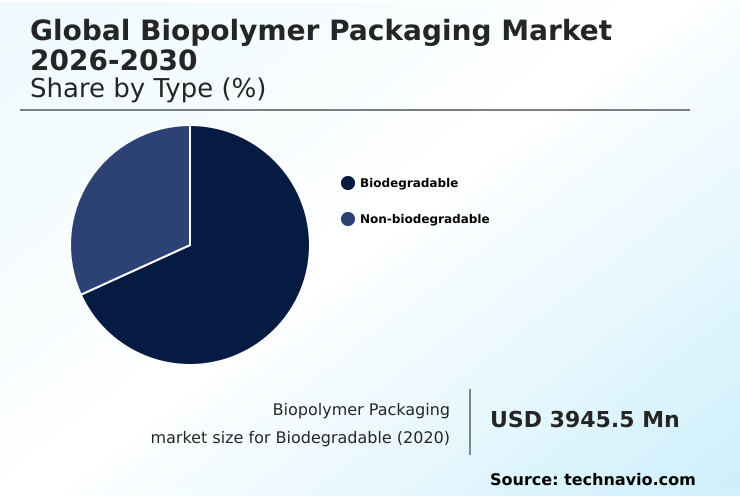

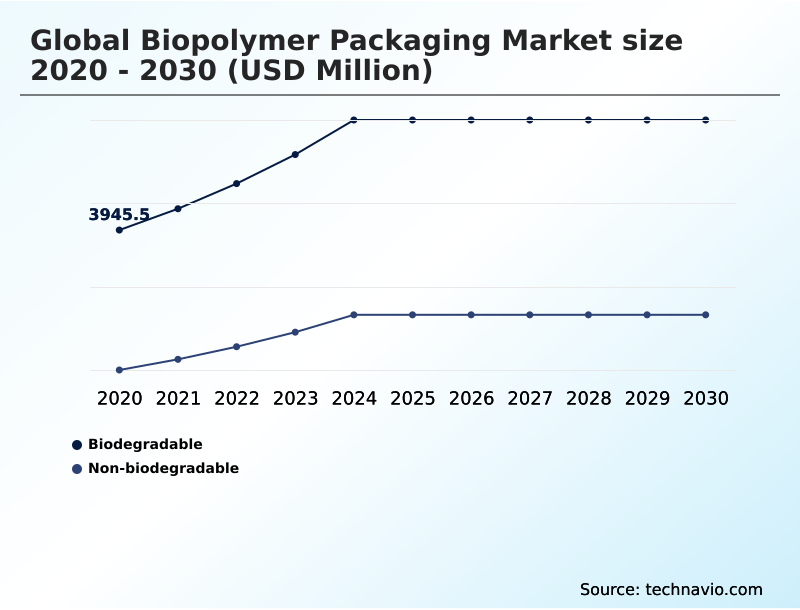

- By Type - Biodegradable segment was valued at USD 5.60 billion in 2024

- By Material Type - Polylactic acid (PLA) segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 13.21 billion

- Market Future Opportunities: USD 9.78 billion

- CAGR from 2025 to 2030 : 15.6%

Market Summary

- The biopolymer packaging market is undergoing a significant transformation, moving from a niche category to a strategic imperative for industries worldwide. This evolution is driven by a convergence of regulatory pressures against single-use plastics and a consumer-led demand for sustainable packaging solutions. At its core, the market revolves around the development and application of bioplastic resins derived from renewable resources.

- Innovations in the polymerization process and bio-based feedstock sourcing are continuously improving the performance of these materials, making them viable single-use plastic alternatives for food, beverage, and consumer goods. A critical business scenario involves supply chain re-engineering, where companies are adopting circular economy principles.

- This requires a shift in procurement to prioritize materials with viable end-of-life options, such as industrial composting or anaerobic digestion. Firms are now evaluating the entire sustainable product lifecycle, from feedstock sourcing to packaging waste management, to meet corporate ESG goals and differentiate their brands.

- Success hinges on balancing material performance, such as barrier properties, with cost-effectiveness and the availability of appropriate disposal infrastructure, which remains a key variable in achieving widespread adoption and ensuring the environmental benefits of these material science innovations are fully realized.

What will be the Size of the Biopolymer Packaging Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Biopolymer Packaging Market Segmented?

The biopolymer packaging industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Biodegradable

- Non-biodegradable

- Material type

- Polylactic acid (PLA)

- Polyhydroxyalkanoates (PHA)

- Others

- End-user

- Food and beverages

- Consumer goods

- Personal care

- Others

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Type Insights

The biodegradable segment is estimated to witness significant growth during the forecast period.

The biodegradable segment is advancing rapidly, driven by the demand for sustainable alternatives to conventional plastics. These materials, including biodegradable polymers like polylactic acid (PLA), polyhydroxyalkanoates (PHA), and thermoplastic starch, are engineered for specific end-of-life options.

Their adoption is critical for mitigating waste from single-use items, especially in food service with products like biodegradable food containers and compostable cutlery.

The value of these sustainable packaging solutions is entirely dependent on correct disposal, requiring access to facilities for home and industrial composting.

A key focus is on material innovation, which has improved the processability of these plant-based plastics by over 15% on standard converting equipment, making them more viable for applications like flexible packaging laminates and rigid containers.

The Biodegradable segment was valued at USD 5.60 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 64.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Biopolymer Packaging Market Demand is Rising in APAC Get Free Sample

The geographic landscape is led by the APAC region, which accounts for over 64% of the market's incremental growth, driven by aggressive government policies aimed at plastic pollution reduction and a robust manufacturing base.

This region is a hub for bio-based material sourcing and innovations in biopolymer compounding. In contrast, North America and Europe are focusing on a value-driven approach, emphasizing material science innovation to develop high-performance rigid bioplastics and flexible films.

European regulations, which are some of the world's strictest, have accelerated the adoption of materials designed for marine degradation.

This has incentivized investments in the sustainable supply chain, with companies achieving up to a 20% carbon footprint reduction by localizing feedstock sourcing.

The development of food grade biopolymers with advanced sustainable coatings is a key competitive differentiator in these mature markets.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- A primary consideration for businesses evaluating a switch to sustainable materials is the cost of biopolymer vs plastic, a gap that continues to narrow due to advancements in pha bioplastic production technology and economies of scale. While pla plastic heat resistance issues have historically limited its use, new formulations are expanding its viability.

- The most significant adoption is seen with biopolymers in food packaging applications, where brand owners leverage sustainability claims to appeal to consumers. However, this introduces complexity in operational planning, as material choice must align with performance needs. For example, improving barrier properties of pla films is crucial for extending the shelf life of moisture-sensitive products.

- For brands in coastal markets, marine biodegradable packaging standards compliance is becoming a non-negotiable aspect of risk management. Strategic decisions also revolve around the supply chain, particularly regarding the ethics and stability of feedstock sourcing for bioplastic manufacturing. Ultimately, the return on investment is tied to the end-of-life options for biopolymers.

- Regions with well-developed composting infrastructure see adoption rates nearly double those without, underscoring the critical link between material choice and available waste management systems.

What are the key market drivers leading to the rise in the adoption of Biopolymer Packaging Industry?

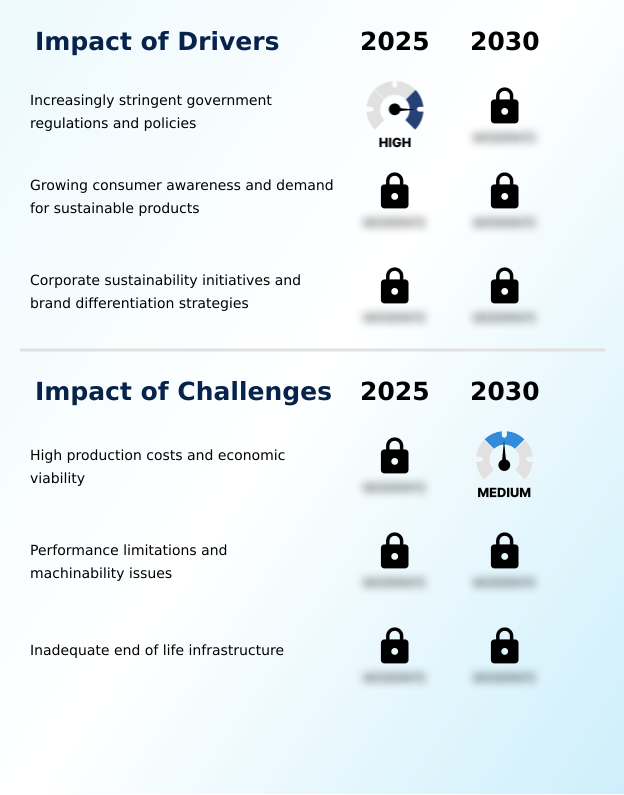

- The proliferation of stringent government regulations and supportive policies aimed at reducing plastic pollution serves as a primary driver for the market.

- Stringent environmental packaging regulations are a primary driver, compelling organizations to adopt sustainable alternatives and redesign their sustainable supply chain.

- These policies have accelerated the market for bioplastic resins derived from renewable resources, with adoption in regulated regions growing 25% faster than in unregulated ones.

- The push for carbon footprint reduction is another significant force, leading to innovations in the polymerization process and bio-based material sourcing. Companies are increasingly turning to plant-based materials to develop rigid packaging solutions that align with consumer demand for sustainability.

- This transition has led to a 20% improvement in resource efficiency for some manufacturers by optimizing feedstock sourcing. The demand for viable single-use plastic alternatives is reshaping product portfolios and forcing improvements in packaging waste management infrastructure.

What are the market trends shaping the Biopolymer Packaging Industry?

- A prominent market trend is the strategic prioritization of biopolymers engineered for degradation in marine and soil environments. This focus aims to address plastic leakage into natural ecosystems.

- A key market trend is the evolution of circular packaging design, moving beyond basic recyclability to embrace advanced biopolymer materials with verified end-of-life options. The focus on materials demonstrating soil biodegradability is intensifying, with research investment in this area increasing by over 40% in recent years.

- This shift fosters the development of green packaging solutions like compostable flexible films and heat-sealable films that do not persist in the environment. Another significant development is the integration of certified recycled polymers into bio-based products, a hybrid approach that improves resource efficiency. Companies adopting these single-use plastic alternatives have seen a 15% increase in consumer trust metrics.

- Innovations in bio-based barrier materials are enabling these eco-friendly bags and films to replace conventional plastics without compromising product integrity.

What challenges does the Biopolymer Packaging Industry face during its growth?

- Significant production costs and the challenge of achieving economic viability compared to conventional plastics represent a key restraint on market growth.

- The primary market challenge remains the cost and performance gap between compostable plastics and their conventional counterparts. While demand for eco-friendly packaging materials is high, achieving competitive pricing for bio-based rigid packaging and biodegradable films is difficult.

- The barrier properties of materials like thermoplastic aliphatic polyester often do not match traditional plastics, a performance deficit that can reduce shelf life by up to 10% in some applications.

- Furthermore, the efficacy of these materials is constrained by a lack of infrastructure; less than 15% of communities have access to the industrial composting facilities required for proper disposal of compostable bags. This creates confusion around home and industrial composting standards, hindering widespread adoption.

- Biopolymer compounding efforts are focused on creating high-performance biopolymers, but these advanced compostable resins carry a significant cost premium.

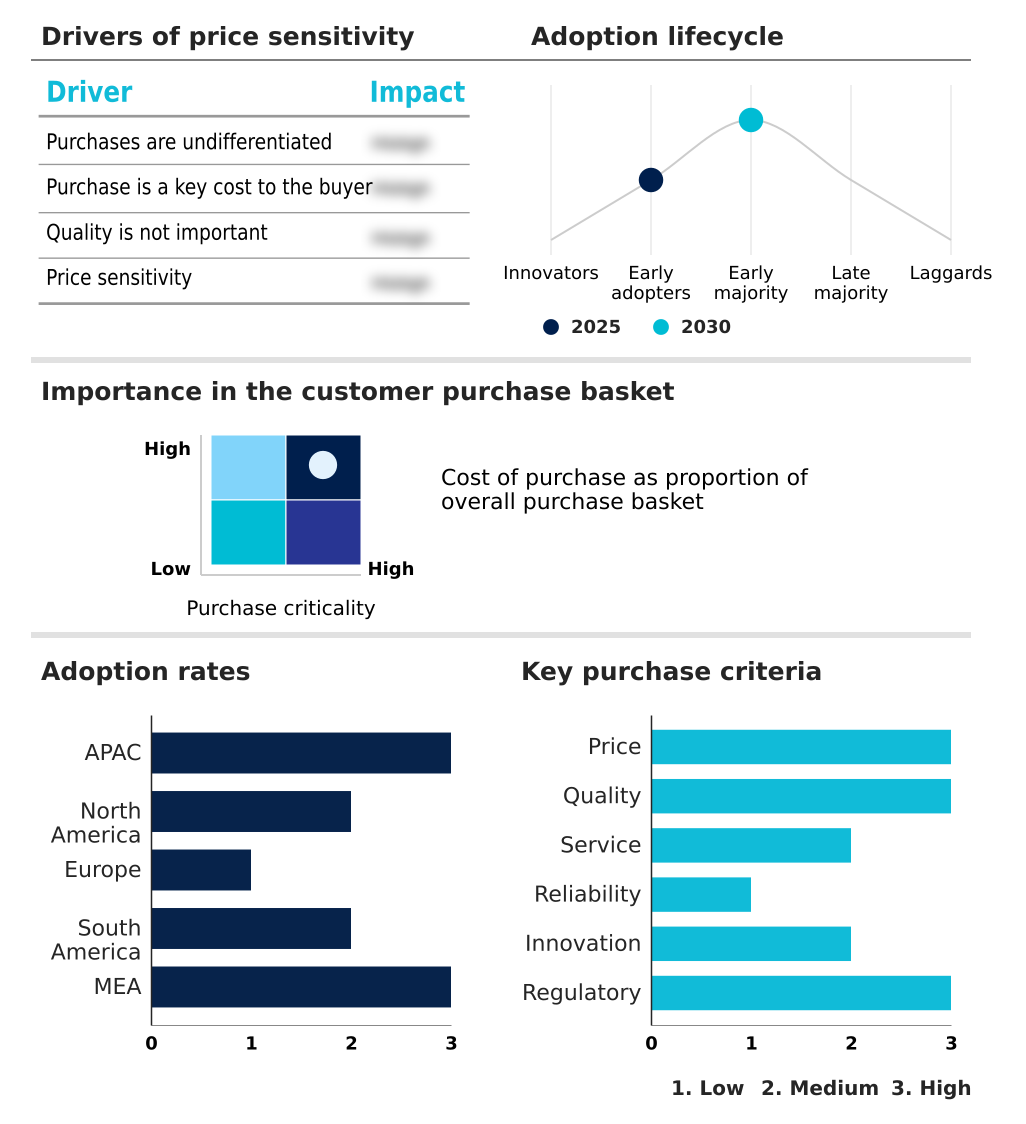

Exclusive Technavio Analysis on Customer Landscape

The biopolymer packaging market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the biopolymer packaging market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Biopolymer Packaging Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, biopolymer packaging market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alpagro Packaging NV - Delivers a portfolio of biopolymer packaging, including versatile flexible and rigid formats engineered for a variety of consumer and industrial applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alpagro Packaging NV

- Amcor Plc

- BASF SE

- BIOGREEN PACKAGING Pvt. Ltd.

- Biome Bioplastics Ltd.

- COMPOSTPACK SAS

- Earthpac Ltd.

- Eastman Chemical Co.

- Element Packaging Ltd.

- Fkur Kunststoff GmbH

- Green Gate Bio Packaging

- Minima Technology Co. Ltd.

- Mondi Plc

- Plastic Suppliers Inc.

- Tetra Pak International SA

- Tipa Ltd.

- Treemera GmbH

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Biopolymer packaging market

- In February 2025, Tetra Pak launched new carton packages in the Indian market that incorporate certified recycled polymers, aligning with local waste management regulations.

- In March 2025, PTT Global Chemical and Kaneka Corp. announced the successful commercial operation of their new PHA production facility in Thailand, utilizing third-generation feedstock from industrial wastewater.

- In March 2025, a European consortium led by the Fraunhofer Institute announced the commercialization of a new stereocomplexed PLA (sc-PLA) formulation suitable for high-temperature applications like coffee capsules.

- In May 2025, the Global Hospitality Alliance partnered with biotech firm FuturaPolymers to mandate the replacement of conventional plastics with PHA-based items across its member hotels by 2028.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Biopolymer Packaging Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 288 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 15.6% |

| Market growth 2026-2030 | USD 9780.0 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 12.4% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The biopolymer packaging market is driven by material science innovation, focusing on high-performance biopolymers that serve as viable single-use plastic alternatives. Boardroom decisions are increasingly influenced by the need to integrate circular economy principles into product strategy, mandating a shift toward bioplastic resins with defined end-of-life options like industrial composting or anaerobic digestion.

- The selection of biodegradable polymers, including polylactic acid (PLA) and polyhydroxyalkanoates (PHA), is no longer just a marketing choice but a core component of risk management and compliance. Innovations in biopolymer compounding and the development of stereocomplexed PLA (sc-PLA) address performance gaps, enabling use in rigid bioplastics and flexible film packaging.

- As companies re-evaluate their supply chains, feedstock sourcing from renewable resources becomes paramount for achieving carbon footprint reduction goals. Firms that successfully integrate these sustainable packaging solutions, from compostable food containers to heat-sealable films, have reported a 30% improvement in meeting their corporate ESG targets.

- This transition involves optimizing the bioplastic manufacturing and polymerization process to manage costs associated with thermoplastic starch and other bio-based feedstocks, ensuring effective packaging waste management and a sustainable product lifecycle. The push for certified recycled polymers and food grade biopolymers with enhanced barrier properties, capable of soil and marine degradation, defines the competitive landscape.

What are the Key Data Covered in this Biopolymer Packaging Market Research and Growth Report?

-

What is the expected growth of the Biopolymer Packaging Market between 2026 and 2030?

-

USD 9.78 billion, at a CAGR of 15.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Biodegradable, and Non-biodegradable), Material Type (Polylactic acid (PLA), Polyhydroxyalkanoates (PHA), and Others), End-user (Food and beverages, Consumer goods, Personal care, and Others) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasingly stringent government regulations and policies, High production costs and economic viability

-

-

Who are the major players in the Biopolymer Packaging Market?

-

Alpagro Packaging NV, Amcor Plc, BASF SE, BIOGREEN PACKAGING Pvt. Ltd., Biome Bioplastics Ltd., COMPOSTPACK SAS, Earthpac Ltd., Eastman Chemical Co., Element Packaging Ltd., Fkur Kunststoff GmbH, Green Gate Bio Packaging, Minima Technology Co. Ltd., Mondi Plc, Plastic Suppliers Inc., Tetra Pak International SA, Tipa Ltd. and Treemera GmbH

-

Market Research Insights

- The market is defined by a dynamic push toward advanced biopolymer materials and green packaging solutions. A shift in corporate strategy is evident, with companies prioritizing circular packaging design, resulting in a 25% increase in the use of materials certified for home and industrial composting.

- Innovations in sustainable material science are enabling the creation of compostable flexible films with enhanced functionality, improving product protection while meeting environmental packaging regulations. Businesses adopting these sustainable alternatives report an 18% improvement in brand perception among environmentally-conscious consumers.

- Furthermore, the integration of bio-based barrier materials into packaging formats has allowed for a 10% reduction in food waste in certain fresh produce applications, demonstrating a clear operational benefit beyond sustainability metrics.

We can help! Our analysts can customize this biopolymer packaging market research report to meet your requirements.

RIA -

RIA -