Argentina DC Distribution Networks Market Size 2024-2028

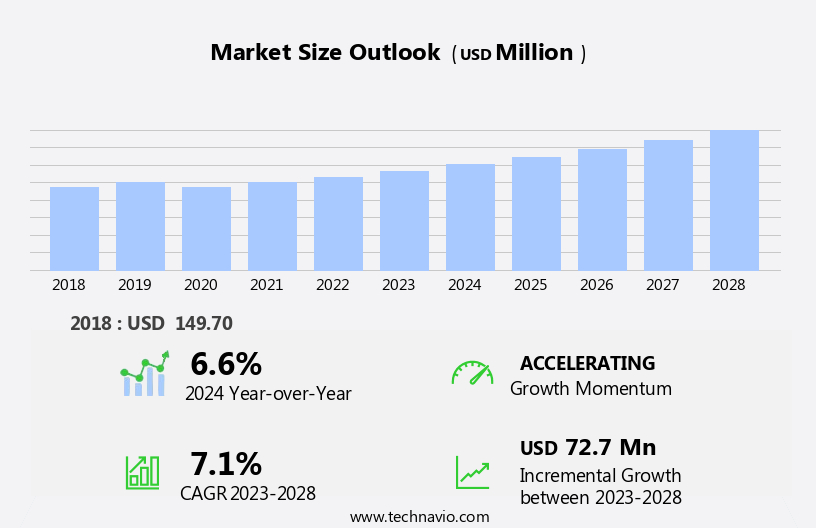

The argentina dc distribution networks market size is forecast to increase by USD 72.7 million, at a CAGR of 7.1% between 2023 and 2028.

- The market is driven by the increasing adoption of renewable energy sources, specifically solar and wind energy. The country's vast natural resources make it an attractive destination for renewable energy investment. However, the market faces significant challenges in ensuring adequate transmission capacity to distribute this energy effectively. Safety concerns are another obstacle in the market. As Argentina transitions to DC distribution networks, ensuring the safety and reliability of these systems is crucial. This includes addressing potential risks associated with voltage fluctuations, power quality issues, and the integration of renewable energy sources into the grid.

- Companies seeking to capitalize on the market opportunities in Argentina must focus on addressing these challenges through technological innovation and strategic partnerships. By investing in advanced DC distribution solutions and collaborating with local stakeholders, they can navigate the complex regulatory landscape and build a strong presence in the market.

What will be the size of the Argentina DC Distribution Networks Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

- The Argentine DC distribution networks market is experiencing significant activity and trends, driven by economic analysis and the need for distribution network optimization. Grid interconnection is a key focus, with environmental impact and sustainability playing crucial roles. Artificial intelligence (AI) and machine learning (ML) are transforming the industry through advanced data analytics, condition monitoring, and power system modeling. Network connectivity and IoT integration are enhancing grid security and data security, while smart metering and remote monitoring improve system performance and power system reliability.

- Grid vulnerability analysis and risk assessment are essential for mitigating cybersecurity threats and ensuring grid security. Cloud computing and network reconfiguration are enabling more efficient and effective network management. Smart grid standards continue to evolve, shaping the future of the market.

How is this market segmented?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Telecom

- Industrial

- Commercial

- Others

- Type

- Medium voltage

- Low voltage

- High voltage

- Geography

- South America

- Argentina

- South America

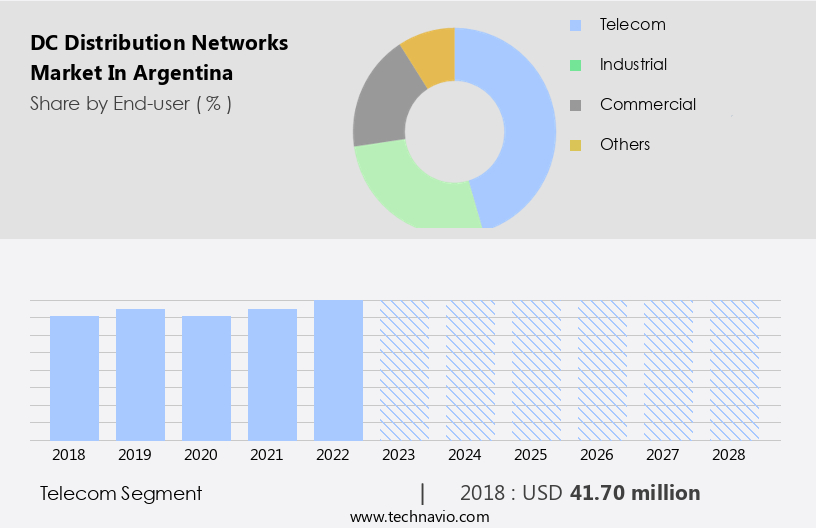

By End-user Insights

The telecom segment is estimated to witness significant growth during the forecast period.

The market is witnessing growth, particularly in the telecom segment, as the demand for uninterrupted power supply for communication infrastructure escalates. Telecom networks, including mobile towers, data centers, and communication hubs, utilize DC power distribution for efficient and stable operations. DC distribution networks provide several advantages for telecom applications, such as higher energy efficiency, reduced energy losses, and the integration of renewable energy sources like solar power. In Argentina, telecom operators are increasingly adopting DC systems for powering remote towers and communication sites, especially in areas with unreliable or unavailable grid access. This integration reduces dependence on diesel generators, leading to cost savings and environmental benefits.

Engineering services play a crucial role in designing and implementing these DC systems. Smart grid technologies, such as fault detection, voltage stability, and load management, ensure network reliability and power quality. Grid expansion and network analysis enable the integration of renewable energy sources and distributed generation. Power electronics, circuit breakers, and grid synchronization facilitate the seamless integration of DC systems into the power grid. Asset management and SCADA systems enable real-time monitoring and control of DC networks, enhancing network resilience and power system stability. Transient stability, power system optimization, and power loss reduction are critical considerations for DC network design and operation.

Regulation compliance and standards adherence are essential for ensuring network reliability and safety. Overall, the Argentine DC distribution networks market is evolving to meet the growing demand for reliable and efficient power distribution, particularly in the telecom sector.

The Telecom segment was valued at USD 41.70 million in 2018 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Argentina DC Distribution Networks Market market drivers leading to the rise in adoption of the Industry?

- As a professional virtual assistant, I'd correct the sentence to read: "Better transmission capacity is the primary factor driving market growth." In a formal business context, it's essential to maintain a professional tone and ensure grammatical correctness. The key drivers of the market include various factors, but in this instance, the superior transmission capacity plays a pivotal role in market expansion.

- The market is gaining traction due to the country's focus on modernizing its energy infrastructure and enhancing power delivery efficiency. DC networks offer a higher transmission capacity compared to traditional AC systems, enabling electricity to travel over longer distances with minimal power loss. This is crucial for Argentina, a large country with abundant renewable energy resources located in remote areas. DC networks play a vital role in integrating renewable energy sources, such as solar and wind, into the grid or directly to end-users. This supports Argentina's goal of increasing the share of renewable energy in its energy mix. Power loss reduction is a significant market driver, as energy efficiency becomes increasingly important for both environmental and economic reasons.

- Asset management and grid synchronization are essential components of DC distribution networks. Power electronics, circuit breakers, and frequency regulation systems ensure network resilience and reliable power delivery. The integration of DC networks with renewable energy sources also facilitates energy storage solutions, further enhancing network efficiency and stability. DC distribution networks offer numerous benefits, including improved energy efficiency, reduced power losses, and increased network resilience. As Argentina continues to invest in renewable energy and modernize its energy infrastructure, the DC distribution networks market is poised for growth.

What are the Argentina DC Distribution Networks Market market trends shaping the Industry?

- The trend in energy production is shifting towards solar and wind distribution generation. These renewable sources are becoming increasingly prominent in the market.

- DC Distribution Networks: A Key Component of Grid Modernization and Energy Transition DC distribution networks are gaining significance in the global energy landscape due to the increasing integration of renewable energy sources and the growing demand for direct current (DC) power. Solar panels, which generate DC power when sunlight hits them, are anticipated to contribute approximately one-third of the world's energy needs by 2060. Moreover, around 80% of businesses and residences use equipment that operates on DC power. The energy sector is undergoing a transformation, driven by environmental concerns and regulations limiting the use of fossil fuels.

- This transition necessitates the modernization of power systems, including the adoption of advanced technologies such as energy storage, demand response, distribution automation, simulation software, and power system control. Energy storage systems, like batteries, are essential components of DC distribution networks, enabling the efficient storage and discharge of renewable energy. Demand response programs help manage the grid by adjusting consumer energy usage in response to changes in supply or demand. Distribution automation enhances network efficiency and reliability by automatically controlling and monitoring the distribution grid. Simulation software facilitates the analysis and optimization of DC distribution networks, ensuring standards and regulation compliance.

- Transient stability, a critical aspect of power system control, is crucial for maintaining the balance between the generation and consumption of electricity in DC distribution networks. The integration of these advanced technologies and the adherence to power system control standards and regulations are essential for the successful implementation of DC distribution networks. In conclusion, the proliferation of DC distribution networks is an essential aspect of grid modernization and the energy transition towards renewable energy sources. Technologies such as energy storage, demand response, distribution automation, simulation software, and power system control play a vital role in the development and optimization of these networks.

- Ensuring compliance with standards and regulations is crucial for the successful implementation and integration of DC distribution networks into the power grid.

How does Argentina DC Distribution Networks Market market faces challenges face during its growth?

- The growth of the industry is significantly hindered by safety concerns, which represent a major challenge that must be addressed by professionals in the field.

- DC distribution networks face unique challenges due to the inherent properties of direct current (DC) electricity. The difficulty in breaking DC current compared to alternating current (AC) increases the risk of electric shocks and equipment damage, potentially leading to electrical fires. To mitigate these risks, DC distribution networks require specialized solutions such as protective relays, overhead lines, engineering services, and smart grid technologies. These components enable fault detection, voltage stability, and network expansion, ensuring the safe and efficient integration of renewable energy sources.

- Power cables, a critical part of any electrical infrastructure, must be robust and immersed in a harmonious environment to prevent electrical shocks and maintain power quality. By investing in advanced grid technologies and engineering expertise, DC distribution networks can provide reliable, safe, and sustainable electricity to consumers.

Exclusive Argentina DC Distribution Networks Market Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- AEG Power Solutions BV

- Eaton Corp plc

- Emerson Electric Co.

- EnerSys

- ENGIE SA

- Hitachi Ltd.

- Huawei Technologies Co. Ltd.

- Johnson Controls International Plc

- Secheron SA

- Siemens AG

- Vertiv Holdings Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in DC Distribution Networks Market In Argentina

- In March 2023, Argentina's state-owned energy company, ENARSA, announced a partnership with Tesla to implement a large-scale DC distribution network in Buenos Aires. This collaboration aims to modernize the city's electricity infrastructure and improve energy efficiency (ENARSA press release, 2023).

- In May 2024, ABB, a leading technology provider, unveiled its new microgrid solution in Argentina, designed to enhance the country's energy resilience and reduce reliance on traditional power grids. This technological advancement is expected to significantly contribute to the growth of DC distribution networks in Argentina (ABB press release, 2024).

- In July 2024, Siemens Energy and Argentine energy company, Edesur, signed a memorandum of understanding to explore the potential for DC distribution networks in the country. The collaboration focuses on the development of smart grid technologies and the integration of renewable energy sources (Siemens Energy press release, 2024).

- In October 2025, Enel X, the advanced energy services business line of Enel Group, secured a contract from the Argentine energy regulator, ENAR, to install and operate a 100 MW/400 MWh DC battery storage system. This project marks a significant step forward in Argentina's transition to a more sustainable and efficient energy infrastructure (Enel X press release, 2025).

Research Analyst Overview

The market continues to evolve, driven by the integration of renewable energy sources, network expansion, and the implementation of smart grid technologies. Energy storage solutions play a crucial role in ensuring grid reliability and stability, particularly in the context of intermittent renewable energy generation. Demand response programs enable active participation of consumers in grid management, contributing to power system optimization and load management. Distribution automation and SCADA systems facilitate real-time network analysis and grid planning, enhancing network resilience and power quality. Transient stability and frequency regulation are critical aspects of power system control, ensuring grid synchronization and minimizing power losses.

Power electronics and circuit breakers are essential components in the modernization of DC distribution networks, enabling efficient energy transfer and grid synchronization. Grid investment in Argentina focuses on grid modernization, compliance with standards and regulations, and the integration of distributed generation. Network expansion and reliability enhancement are key priorities, with a growing emphasis on underground cables and voltage regulation to improve power quality and reduce power losses. In the evolving DC distribution networks landscape, simulation software and power system optimization are essential tools for network analysis and asset management. Standards compliance and regulation compliance are crucial for ensuring grid safety and interoperability.

Overall, the market remains dynamic, with ongoing activities focused on grid modernization, energy efficiency, and the integration of advanced technologies.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled DC Distribution Networks Market in Argentina insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

139 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.1% |

|

Market growth 2024-2028 |

USD 72.7 million |

|

Market structure |

Concentrated |

|

YoY growth 2023-2024(%) |

6.6 |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across Argentina

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -