Europe Seed Market Size 2024-2028

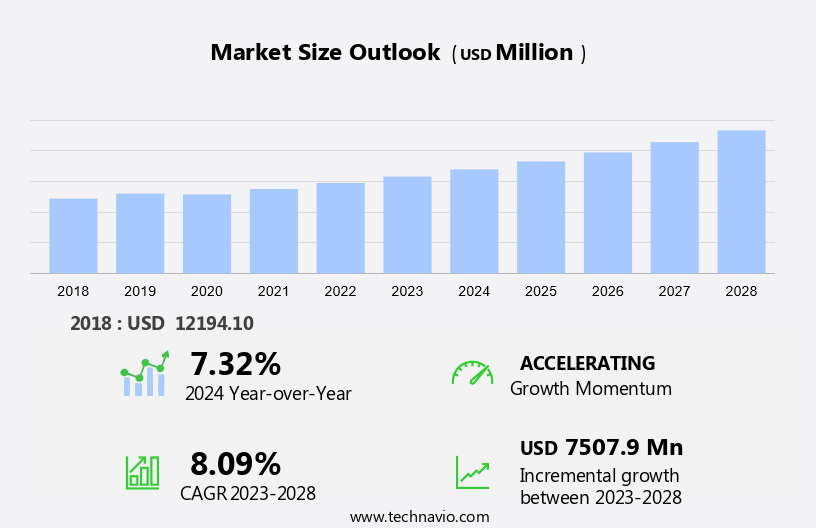

The Europe seed market size is forecast to increase by USD 7.51 billion billion at a CAGR of 8.09% between 2023 and 2028.

- The European seed market is experiencing significant growth due to several key drivers. The increasing demand for biofuels is one such factor, as seeds used for biofuel production are in high demand. Additionally, the adoption of seeds with advanced generation traits is on the rise, as farmers seek to improve crop yields and reduce reliance on chemical inputs. However, the market also faces challenges, including the availability of counterfeit seeds, which can negatively impact farmers and the overall industry. Plant-based protein companies and the animal feed industry are significant consumers of seed meals (soybean meal, cottonseed meal, etc.). These trends and challenges are shaping the European seed market, providing opportunities for growth and innovation. The use of advanced technologies, such as genomic selection and precision farming, is also gaining traction, offering potential solutions to address the challenges and drive market growth. Overall, the European seed market is poised for continued expansion, driven by these key factors and trends.

What will be the size of the Europe Seed Market during the forecast period?

- The European seed market encompasses a diverse range of players, including multinational corporations, small-scale seed producers, and public research institutions. This market caters to various crop types, with a significant focus on row crops such as soybean, sunflower, cotton, and oilseed crops like rapeseed and their derived meals, including soybean meal, sunflower meal, and cottonseed meal. Breeding technology advances continue to shape the European seed industry, with an emphasis on producing hybrids, open pollinated varieties, and hybrid derivatives. The cultivation mechanism varies, with both open field and protected cultivation methods employed. The European seed market is driven by the demand for high-yielding, uniform, and disease-resistant seeds that can thrive in diverse agro-climatic conditions.

- The market's size is substantial, reflecting the importance of seed in modern agriculture, food production, and biofuels. The global seed industry is undergoing modernization, with a focus on improving crop productivity, yield, color, and other essential qualities. The animal feed industry also plays a crucial role In the demand for seed meals. Overall, the European seed market is dynamic and evolving, driven by advancements in technology and the ongoing quest for improved agricultural practices.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

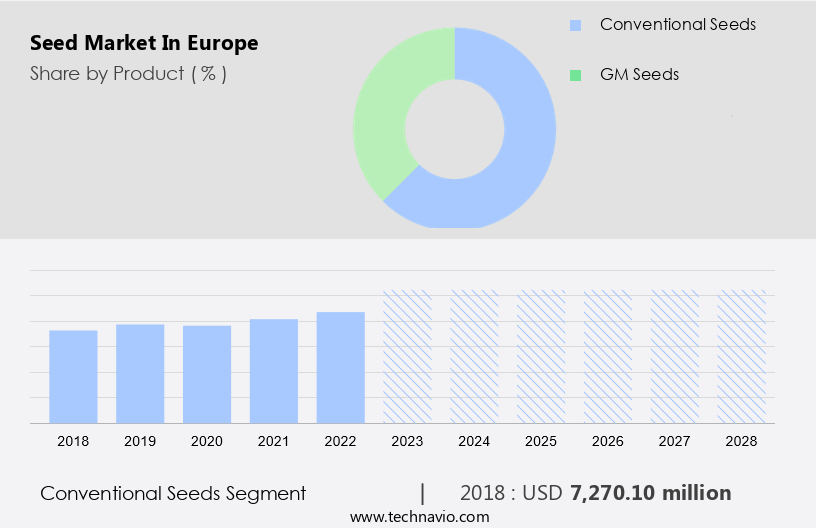

- Conventional seeds

- GM seeds

- Type

- Grain seeds and oil seeds

- Fruits and vegetable seeds

- Others

- Geography

- Europe

- Germany

- UK

- France

- Italy

- Europe

By Product Insights

- The conventional seeds segment is estimated to witness significant growth during the forecast period.

The European seed market encompasses various stakeholders, including multinational corporations, small-scale seed producers, public research institutions, and the animal feed industry. In the EU, conventional seeds, which are not hybridized or genetically modified (GM), are gaining traction due to safety concerns and environmental issues associated with GM crops. The EU's partial ban on GM grains has created opportunities for the conventional seeds market, particularly In the context of the growing organic farming trend. This sector is expected to thrive, as organic farming prohibits the use of GM seeds. Key crop types include cereals & grains (wheat, rice, corn, rapeseed, etc.),

oilseeds (soybean, sunflower, cottonseed, etc.), and forage crops (alfalfa, forage corn). Modernization of agriculture, food production, and biofuels are driving the demand for seed technologies, such as seed coating and pelleting. The availability of financial and technical assistance from organizations like the Rockefeller Foundation, World Bank, and Ford Foundation is also contributing to the market's growth. The cultivation mechanism can be open field or protected, depending on the crop type and agro-climatic conditions. The regulatory stance on seed varieties and traits, including herbicide-tolerant and insecticide-resistant, varies across regions. The seed replacement rate and emerging economies also impact the market dynamics.

Get a glance at the market share of various segments Request Free Sample

The Conventional seeds segment was valued at USD 7.27 billion in 2018 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of Europe Seed Market?

Rising demand for biofuels is the key driver of the market.

- In Europe, the seed market encompasses various crop types, including cereals and grains such as wheat, rice, corn, and barley, as well as oilseeds like soybean, sunflower, cottonseed, rapeseed, mustard, safflower, and groundnut. Multinational corporations, small-scale seed producers, and public research institutions collaborate to develop new seed varieties using advanced plant breeding techniques, such as molecular breeding, genetic engineering, and hybridization. The animal feed industry is a significant consumer of seed by-products, including oilseed meals like soybean meal, sunflower meal, cottonseed meal, and others. Plant-based protein companies are also emerging as key players In the market, utilizing seeds to produce various plant-based protein sources.

- The EU Commission's REFORMA Project focuses on enhancing the competitiveness of the European seed sector through modernization and innovation. Seed technologies, such as seed coating and pelleting, are increasingly being adopted to improve seed quality and uniformity. The availability of seed varieties is crucial for agriculture and food production, with farmers relying on seeds for nourishment, dispersal, and dormancy. The regulatory stance on seed treatment and traits, such as herbicide-tolerant and insecticide-resistant, varies across countries. The global seed industry is undergoing modernization, with emerging economies showing significant growth potential. The seed replacement rate is a critical factor In the market, as farmers continually seek new and improved seed varieties to optimize their farming systems and improve crop productivity, yield, and disease resistance.

- The FAO and various organizations, including the Rockefeller Foundation, World Bank, and Ford Foundation, provide financial and technical assistance to promote the availability and accessibility of quality seeds for farmers worldwide. The cultivation mechanism, whether in open fields or protected cultivation, influences the choice of seed types and varieties. The market dynamics of the seed industry are influenced by various factors, including agro-climatic conditions, crop type, crop productivity, and yield. The use of gene-tagged markers and advanced plant breeding techniques, such as hybridization and molecular breeding, contribute to the development of transgenic and non-transgenic hybrid seeds. Thus, the market is a dynamic and evolving industry, driven by the demand for high-quality seeds, the need for sustainable agriculture, and the pursuit of innovation and technological advancements. The market's growth is influenced by various factors, including regulatory stance, population growth, and the agricultural sector's import and export trends.

What are the market trends shaping the Europe Seed Market?

Growing usage of seeds with advanced generation traits is the upcoming trend In the market.

- The European seed market is experiencing significant growth due to the increasing demand for high-quality seeds with advanced traits. The adoption of herbicide-tolerant and disease-resistant seeds, such as hybrid soybean and corn, is on the rise. These seeds offer enhanced productivity and resistance to pests and herbicides, making them a popular choice among farmers. companies are investing in research and development to produce seeds with specific traits, including abiotic stress tolerance, modified quality pollination control systems, and insecticide resistance. The cultivation of row crops, such as cereals & grains like wheat, rice, corn, and oilseeds like soybean, sunflower, cottonseed, rapeseed, mustard, safflower, and forage crops like alfalfa and forage corn, is driving market growth.

- The EU Commission's REFORMA project and various public research institutions are collaborating to improve breeding technology and develop transgenic and non-transgenic hybrid seeds. The market dynamics are influenced by various factors, including agro-climatic conditions, crop productivity, yield, uniformity, color, and disease resistance. The availability of financial and technical assistance from organizations like the Rockefeller Foundation, World Bank, and Ford Foundation is also contributing to the market's growth. The seed industry is undergoing modernization, with emerging economies increasingly adopting new seed technologies, such as seed coating and pelleting, to improve crop productivity and food production. The market's growth is further fueled by the demand for seed varieties with high starch content for use in animal feed and biofuels. The regulatory stance towards seed treatment and traits varies across Europe, making it essential for companies to stay informed about the latest regulations to ensure the quality and availability of their seeds.

What challenges does Europe Seed Market face during the growth?

Availability of counterfeit seeds is a key challenge affecting the market growth.

- The European seed market faces a significant challenge with the prevalence of counterfeit and substandard seeds. Deceptive packaging and seed adulteration are major concerns, leading to crop failure and decreased productivity. This results in substantial financial losses for farmers and the agricultural sector. The increasing cost of authentic seeds is contributing to the growth of the counterfeit seed market. Some countries export low-quality seeds to cost-conscious buyers at subsidized prices, eroding trust In the local seed industry. The use of inferior seeds can negatively impact agro-climatic conditions, crop type, cultivation mechanism, and seed trait, ultimately affecting crop productivity, yield, uniformity, color, disease resistance, and starch content.

- The European Union Commission, through initiatives like the REFORMA Project, is addressing this issue by promoting the modernization of agriculture, food production, and biofuels through seed technologies such as molecular breeding, gene-tagged markers, hybrid seeds, and non-transgenic and transgenic hybrid seeds. The global seed industry is undergoing significant changes, with a focus on new technologies, seed replacement rates, and financial and technical assistance from organizations like the Rockefeller Foundation, World Bank, and Ford Foundation. The availability of seed varieties and the regulatory stance on seed treatment and seed trait are also crucial factors influencing the seed market dynamics.

Exclusive Europe Seed Market Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, market growth and forecasting, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- BASF SE

- Bayer AG

- Bejo Zaden BV

- Corteva Inc.

- DLF Seeds AS

- Enza Zaden Beheer B.V.

- FMC Corp.

- Gans Dunhaung Seed

- Groupe Limagrain

- KWS SAAT SE and Co. KGaA

- Land O Lakes Inc.

- Mahyco Pvt. Ltd.

- Rijk Zwaan Zaadteelt en Zaadhandel BV

- Royal Barenbrug Group

- Sakata Seed Corp.

- Syngenta Crop Protection AG

- Takii and Co. Ltd.

- UPL Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The European seed market is a dynamic and intricate industry that plays a vital role In the agricultural sector. This market encompasses various stakeholders, including multinational corporations, small-scale seed producers, and public research institutions. The industry's primary focus is on supplying seeds for row crops, such as cereals and grains, including corn, wheat, rice, rapeseed, and others, as well as vegetables and forage crops. The European seed market is driven by several factors. The demand for seeds is influenced by farming systems, agro-climatic conditions, and crop productivity. The need for high-quality seeds that ensure uniformity, color, disease resistance, and yield is essential for farmers to maintain optimal crop productivity.

Seeds are also crucial for the production of food, biofuels, and animal feed. The animal feed industry is a significant consumer of seeds and their by-products, such as oilseed meals, including soybean meal, sunflower meal, cottonseed meal, and groundnut meal. These meals are rich in protein and contribute to the nourishment of livestock, making them an essential component of the agricultural sector. The European seed market is undergoing modernization, with advancements in breeding technology and seed coating and pelleting techniques. Molecular breeding, gene-tagged markers, and genetic engineering are some of the modern techniques used to develop transgenic and non-transgenic hybrid seeds.

These new technologies aim to enhance seed traits, such as herbicide tolerance, insect resistance, and improved dormancy. The regulatory stance towards seed production and distribution varies across Europe. The European Union Commission has several initiatives, such as the REFORMA project, which aims to promote the availability of quality seeds and provide financial and technical assistance to farmers. The FAO also plays a role in supporting the global seed industry's modernization and ensuring food production's sustainability. The European seed market is diverse, with multinational corporations, small-scale seed producers, and public research institutions contributing to the industry's growth. The market's dynamics are influenced by factors such as population growth, agricultural sector development, and import and export trends.

Emerging economies are also increasing their demand for seeds, leading to a growing market for seed varieties and new technologies. The cultivation mechanism for seeds can vary from open field to protected cultivation, depending on the crop type. Row crops, such as cereals and grains, are typically grown in open fields, while vegetables and forage crops may be grown in protected cultivation to ensure optimal growing conditions. The European seed market is a complex ecosystem that requires a deep meaning is of the various stakeholders, market trends, and regulatory frameworks. The industry's continued growth and success depend on the ability to adapt to changing market dynamics and invest in new technologies to meet the evolving needs of farmers and consumers.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

146 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.09% |

|

Market growth 2024-2028 |

USD 7.51 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

7.32 |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across Europe

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -