External Ventricular Drain Market Size 2024-2028

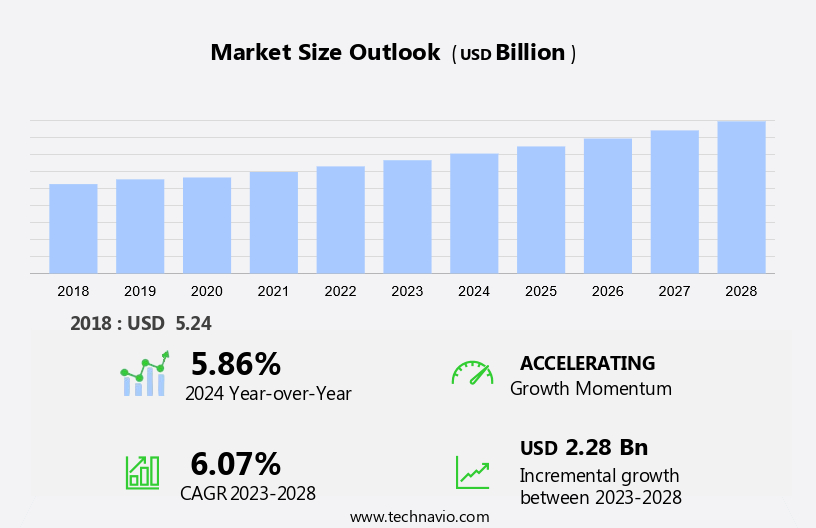

The external ventricular drain market size is forecast to increase by USD 2.28 billion, at a CAGR of 6.07% between 2023 and 2028.

- The market is witnessing significant growth due to the increasing number of neurosurgical procedures for medical conditions such as subarachnoid hemorrhages, strokes, and hematomas in the posterior fossa. The advancements in medical technology have led to the development of EVDs with enhanced monitoring capabilities for cerebrospinal fluid (CSF) drainage. This is crucial for the timely detection and management of complications, particularly in pediatric patients. However, the scarcity of trained experts to perform neurosurgical procedures remains a challenge. The aging population is also contributing to the growth of this market, as elderly individuals are more susceptible to neurological conditions requiring EVDs.

What will be the Size of the Market During the Forecast Period?

- The market has experienced significant growth in recent years, driven by the increasing demand for advanced neurological care. Neurological care providers have increasingly relied on EVDs as an essential tool for managing various neurological conditions, including hydrocephalus, brain injuries, and brain tumors. EVDs play a crucial role in maintaining brain health by managing cranial pressure. This device provides an avenue for the drainage of cerebrospinal fluid (CSF) from the brain's ventricular system. Neurological assessment and monitoring are integral components of neurological care, and EVDs enable healthcare professionals to assess intracranial pressure and evaluate neurological conditions effectively.

- Neurological research continues to advance, leading to new developments in neurosurgical procedures. Minimally invasive neurosurgeries, such as those using EVDs, have become increasingly popular due to their numerous benefits. These procedures offer reduced recovery time, minimal scarring, and lower risks compared to traditional neurosurgical techniques. Neurological specialists employ EVDs in various applications, including stroke rehabilitation, cognitive function improvement, and spinal cord injuries. The device's ability to monitor intracranial pressure and manage hydrocephalus makes it indispensable in the treatment of neurological conditions. Neurological care facilities and neurosurgery centers have adopted EVDs as a standard component of their neurosurgical technology

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- EVD system

- EVD catheter and accessories

- Application

- Traumatic brain injury

- Other non-traumatic hydrocephalus conditions

- Subarachnoid hemorrhage

- Intracerebral hemorrhage

- Geography

- North America

- Canada

- US

- Europe

- Germany

- UK

- Asia

- China

- Rest of World (ROW)

- North America

By Product Insights

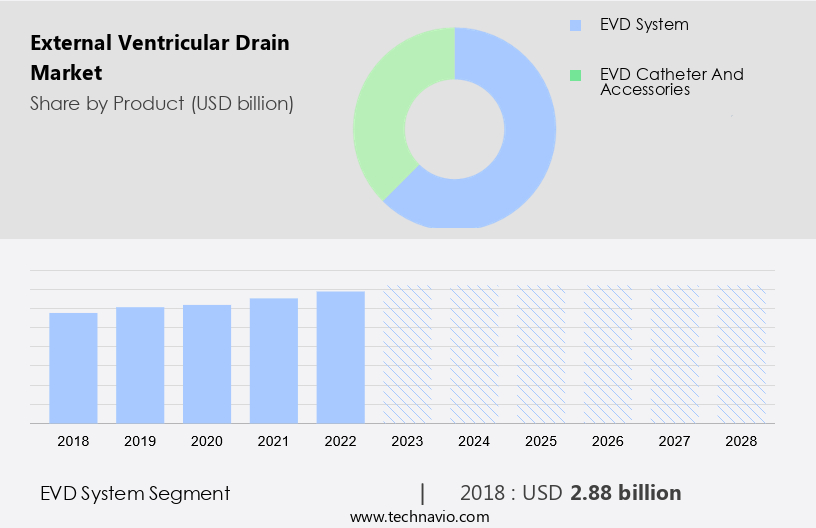

- The EVD system segment is estimated to witness significant growth during the forecast period.

External Ventricular Drainage (EVD) systems are essential medical devices used in neurology hospitals for managing intracranial pressure (ICP) and treating conditions such as subdural hematomas, IV ventricle obstruction, and various neurological disorders. These systems consist of a patient line with a stopcock, an anti-reflux valve and a sampling port, a graduated cylinder, a drainage tube, T-connectors or stopcock assembly, an extension line, a drainage bag, and a ruler. With the increasing number of neurological disorders and sports injuries, the demand for advanced EVD systems is on the rise. companies are responding to this trend by integrating Intracranial Pressure (ICP) monitoring devices into their EVD systems.

This innovation not only increases the adoption of these systems but also simplifies the process of draining cerebrospinal liquid for the treatment of neurological conditions in both adult and pediatric patients. One such example is Medtronic Plc's Duet external drainage and monitoring system. This system offers the benefits of both drainage and monitoring in a single device, making it a preferred choice for medical professionals. The global market for External Ventricular Drains is expected to grow significantly due to these advancements and the increasing incidence of neurological disorders.

Get a glance at the market report of share of various segments Request Free Sample

The EVD system segment was valued at USD 2.88 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

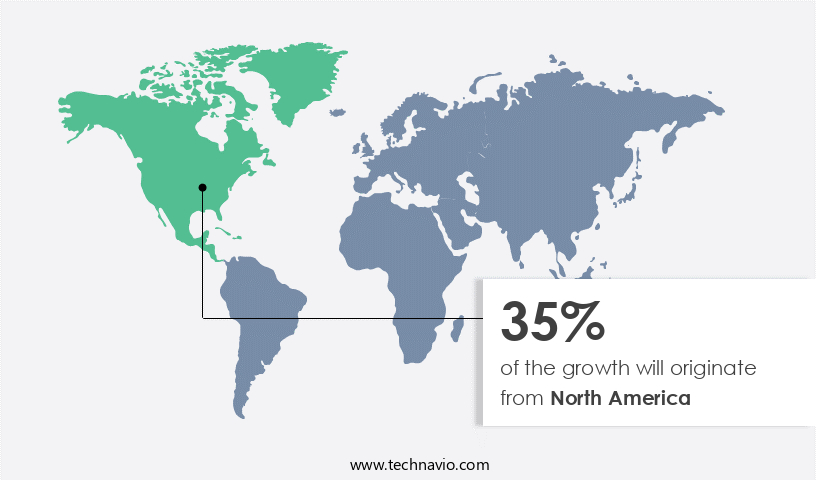

- North America is estimated to contribute 35% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The market in North America is projected to expand significantly due to the increasing prevalence of neurological conditions, such as traumatic brain injuries (TBI) and neurovascular strokes, as well as the growing elderly population. According to the Centers for Disease Control and Prevention (CDC), approximately 350,000 Americans sustain a TBI annually, and stroke is the fifth leading cause of death in the US. Ischemic strokes, in particular, are a major driver of the EVD market growth. The American Stroke Association reports that ischemic strokes accounted for about 87% of all strokes in the US in 2021.

Furthermore, advancements in neurovascular surgeries, such as intracranial vascular stenosis treatments and cerebrovascular disorders management, are expected to fuel market expansion. Hemorrhagic strokes and hemorrhages, including normal pressure hydrocephalus (NPH), also contribute to the demand for EVDs. In summary, the EVD market in North America is poised for substantial growth due to the rising incidence of neurological disorders and technological advancements in neurovascular care.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of the market?

The rise in elderly population is the key driver of the market.

- The market is witnessing significant growth due to the rising prevalence of cranial injuries, neurovascular strokes, intracranial vascular stenosis, cerebrovascular disorders, hemorrhagic stroke, hydrocephalus, ischemic stroke, head trauma, normal pressure hydrocephalus, and other neurological disorders. With the increasing stroke burden and the need for advanced procedures such as neurovascular surgeries, brain surgeries, and the latest equipment for monitoring intracranial pressure (ICP) and cerebrospinal fluid (CSF) in hospitals, the demand for EVD devices is increasing. The geriatric population, who are more susceptible to neurological illnesses due to aging, is a significant consumer of these devices.

- The market is also driven by new technology launches, joint ventures, and medical technology's technical progress. The EVD device is used for exterior drainage arrangement in cases of intracranial stress due to conditions such as intraventricular bleeding, intracranial pressure, and vascular malformations. It is also used for the treatment of infected cerebrospinal fluid, hematomas in the posterior fossa, subdural hematomas, and intraventricular obstruction. The market is expected to grow further with the increasing number of neurology hospitals and the need for advanced procedures for conditions such as subarachnoid hemorrhage, meningitis, and brain injuries. The market is also driven by increasing healthcare spending and the need for patient safety features in EVD devices.

What are the market trends shaping the market?

Technological advancements to improve ventricular drainage is the upcoming trend in the market.

- The market has experienced significant growth in recent years due to the increasing prevalence of cranial injuries, neurovascular strokes, intracranial vascular stenosis, cerebrovascular disorders, hemorrhagic stroke, and hydrocephalus. These conditions often result in raised intracranial pressure (ICP), which requires ventricular drainage to alleviate the pressure and prevent further damage to the brain. Neurosurgical procedures such as EVD installation are essential for treating various neurological illnesses, including traumatic brain injury (TBI), normal pressure hydrocephalus (NPH), and vascular malformations. EVD devices are commonly used to manage intracranial stress caused by intraventricular bleeding, hematomas, subarachnoid hemorrhage, and subdural hematomas.

- The latest equipment and advanced procedures enable neurosurgeons to monitor ICP and cerebrospinal fluid (CSF) flow in real-time, ensuring effective treatment and patient safety. Hospitals and neurology hospitals have increasingly adopted these technologies to improve patient outcomes and reduce the burden of strokes and brain injuries. Technological advancements have led to new EVD launches, joint ventures, and partnerships between medical technology companies, enhancing the capabilities of EVDs and improving patient care. These developments include cellphone-controlled EVDs, ultrasound guides, and neuronavigation systems, which facilitate precise and accurate placement of the drain. The geriatric population, who are more susceptible to neurovascular diseases and head trauma, particularly benefit from these advancements.

- Despite the promising developments, challenges remain, including the risk of infected cerebrospinal fluid and intracranial pressure fluctuations. Neurosurgeons must balance the benefits of EVDs with the risks and ensure proper patient monitoring and care during and after the surgical procedure. The future of EVDs lies in continued technological advancements and improved training programs for neurosurgeons to ensure optimal patient outcomes.

What challenges does the market face during the growth?

The scarcity of trained experts to conduct neurosurgery is a key challenge affecting the market growth.

- The market encompasses the production and distribution of ventricular drain sets used in managing various neurological conditions, including cranial injuries, traumatic brain injury (TBI), neurovascular strokes, intracranial vascular stenosis, cerebrovascular disorders, hemorrhagic stroke, intraventricular bleeding, hydrocephalus, ischemic stroke, head trauma, normal pressure hydrocephalus (NPH), and vascular malformations. These conditions can lead to raised intracranial pressure, hemorrhages, and intracranial stress, necessitating EVDs for monitoring and treatment. Neurological illnesses such as meningitis, intracranial pressure, and pressure scale require constant monitoring and intervention, making the EVD an essential tool in neurosurgical procedures. Hospitals, especially neurology hospitals, are major consumers of EVDs due to the high prevalence of neurological disorders in the geriatric population and sports injuries.

- New technology launches, joint ventures, and medical technology advancements continue to enhance the capabilities of EVDs, enabling advanced procedures for treating brain injuries and infections, such as infected cerebrospinal fluid. The EVD device, which includes a ventricular catheter and an access port, is a critical component of the latest equipment used in surgical procedures. Brain surgeons rely on these devices to manage various conditions, such as intracranial stress, intraventricular bleeding, and hydrocephalus, by providing exterior drainage arrangements. The market for EVDs is expected to grow significantly due to the increasing burden of strokes and the need for improved patient safety features in healthcare spending.

- The market also caters to children with conditions such as subdural hematomas and hematomas in the posterior fossa. In conclusion, the market plays a vital role in the diagnosis and treatment of various neurological disorders. The market's growth is driven by the increasing burden of neurological diseases, the need for advanced procedures, and the growing demand for improved patient safety features. The shortage of skilled neurologists in several countries highlights the importance of investing in training programs and technological advancements to meet the growing demand for EVDs.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Fuji Systems

- Integra Lifesciences Corp.

- Koc Holding AS

- Luciole Medical AG

- Medtronic Plc

- Moller Medical GmbH

- Natus Medical Inc.

- Neuromedex GmbH

- Sophysa

- Salvavidas

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

External ventricular drains (EVDs) are essential medical devices used to manage various neurovascular conditions, including traumatic brain injuries (TBIs), cerebrovascular disorders such as hemorrhagic and ischemic strokes, and intracranial vascular stenosis. These devices help alleviate raised intracranial pressure (ICP) caused by conditions like hydrocephalus, intraventricular bleeding, and hematomas. EVDs are particularly beneficial for patients with severe neurological illnesses, such as posterior fossa tumors and meningitis. Healthcare facilities invest significantly in the latest EVD technology to ensure patient safety features and advanced monitoring capabilities. Neurosurgical procedures using EVDs require general anesthesia and involve the insertion of a ventricular catheter into the brain ventricles.

These procedures are crucial for treating a range of conditions, from sports injuries to vascular malformations and brain damage in the geriatric population. Technical progress in medical technology has led to new agreements, joint ventures, and the launch of innovative EVD solutions. These advancements enable healthcare providers to offer more effective treatments and improved patient outcomes, ultimately contributing to a reduction in stroke burden and overall healthcare spending. In summary, external ventricular drains play a vital role in managing various neurovascular conditions and intracranial stress. With continuous technological advancements, these devices offer enhanced monitoring capabilities and improved patient safety features, making them an essential component of modern neurosurgical procedures.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

157 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.07% |

|

Market Growth 2024-2028 |

USD 2.28 billion |

|

Market structure |

Concentrated |

|

YoY growth 2023-2024(%) |

5.86 |

|

Key countries |

US, Canada, Germany, UK, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements.

RIA -

RIA -