Enjoy complimentary customisation on priority with our Enterprise License!

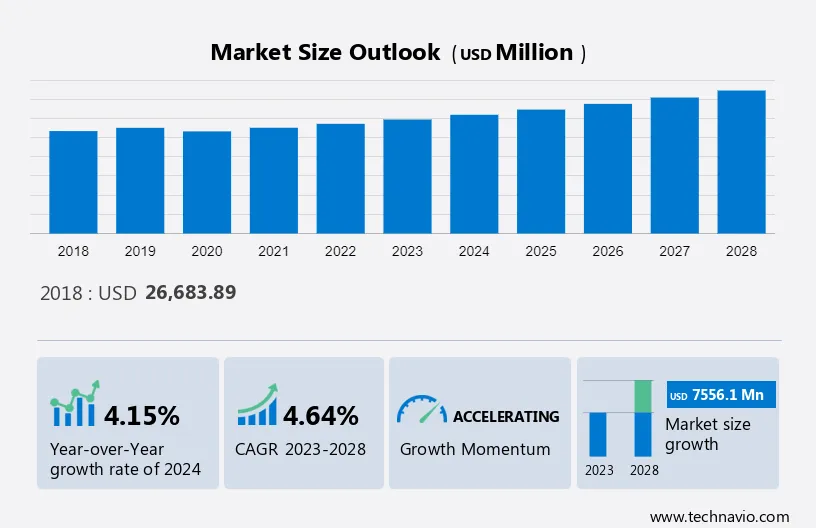

The front end of the line semiconductor equipment market size is estimated to grow at a CAGR of 4.64% between 2024 and 2028. The market size is forecast to increase by USD 7.56 billion. The market's growth depends on several factors, including the growth of the advanced consumer electronics industry, the miniaturization of electronic devices, and the advent of 3D ICs. The production of semiconductors involves different steps that are achieved using semiconductor production equipment. The production process involves two categories, namely the front end of the line and the back end of the line (BEOL). FEOL refers to gate formation, while BEOL refers to interconnect formation or wiring development. FEOL semiconductor equipment includes different types of machinery that perform lithography, deposition, etching, inspection, surface preparation, ion implant, chemical planarization, and thermal processing.

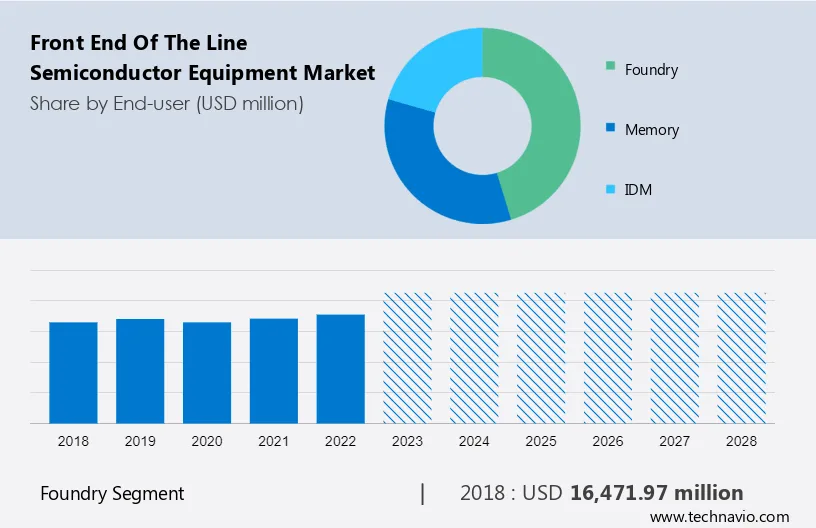

This front end of the line semiconductor equipment market report extensively covers market segmentation by end-user (foundry, memory, and IDM), product (stepper, CVD equipment, silicon etching equipment, coater developer, and others), and geography (APAC, North America, Europe, South America, and Middle East and Africa). It also includes an in-depth analysis of drivers, trends, and challenges. Furthermore, the report includes historic market data from 2018-2022.

For More Highlights About this Report, Download Free Sample in a Minute

The advent of 3D ICs is the key factor driving market growth. Numerous chips are piled onto a single stack using this technique, which leads to less space usage, reduction in power consumption, and improvement in the transmission speed. 3D ICs are being manufactured by chip manufacturers in order to meet the high demand from electronic product manufacturers that are looking for improved performance and minimum space utilization by ICs.

For example, Applied Materials introduced a new dielectric etch system called the Centura Avatar that is designed to meet the new requirements in creating 3D memory architecture, which delivers the high-density, terabit storage capability required for data-intensive mobile devices. Thus. such developments will boost the growth of the global front end of the line semiconductor equipment market during the forecast period.

The proliferation of automotive electronics is the primary trend shaping market growth. The automotive market is going through a lot of transformations, with electronics such as advanced driver assistance systems (ADAS), connected vehicles, and electric energy having high growth potential. In the future, most automobile buying decisions will be made based on the electronic content in vehicles and associated systems.

In addition, automotive manufacturers are using different types of semiconductor ICs in functions such as airbag control, global positioning system (GPS), power doors and windows, anti-lock braking system (ABS), car navigation and display, infotainment, and automated driving. Thus, such factors will boost the market growth during the forecast period.

Stringent fluctuations in the semiconductor industry is a challenge that affects market growth. The global front-end-of-the-line semiconductor equipment market is highly reliant on the growth in sales of semiconductor ICs, which depends on the sales of electronic devices. The fluctuations in demand for electronic products such as consumer electronic devices and mobile devices, make the future of the semiconductor market unpredictable and can lead to an oversupply or undersupply of semiconductor ICs.

Moreover, in the case of an oversupply, fabs can fulfill the demand for semiconductor ICs without expanding their manufacturing capacity, which reduces their capital spending. This indirectly reduces the growth in the sales of front end of the line semiconductor equipment, which, in turn, impedes the growth of the market during the forecast period.

The market share growth by the foundry segment will be significant during the forecast period. The foundry segment will gain momentum due to the increasing fab construction activities. The increasing capital expenditure by foundries is primarily driven by the demand for advanced mobile phone chips. The increasing technological functionalities in mobile devices remain the primary driver for foundry spending on semiconductor production equipment, such as front-end-of-the-line semiconductor equipment.

Get a glance at the market contribution of various segments Download the PDF Sample

The foundry segment showed a gradual increase in the market share of USD 16.47 billion in 2018. Moreover, maintaining the demand in the supply chain is important in the semiconductor industry. Hence, many foundries upgrade their semiconductor equipment to meet the production of and demand for high-quality end products. Hence, such factors create a demand for front end of the line semiconductor equipment during the forecast period.

Steppers were created to address the problems that limit the yield of working devices in semiconductor wafer manufacturing. Technological advancements in semiconductor wafer specifications due to the growing miniaturization of electronic devices such as smartphones and tablets and the increase in demand for semiconductor devices, especially ICs used in storage and memory devices and computers, have been driving the growth of the stepper equipment market. Furthermore, market players such as Nikon have already started expanding the product line for MEMS steppers for various photolithography applications. Thus, such factors will have a positive impact on the growth of the stepper segment of the semiconductor front-end equipment market during the forecast timeframe.

For more insights on the market share of various regions Download PDF Sample now!

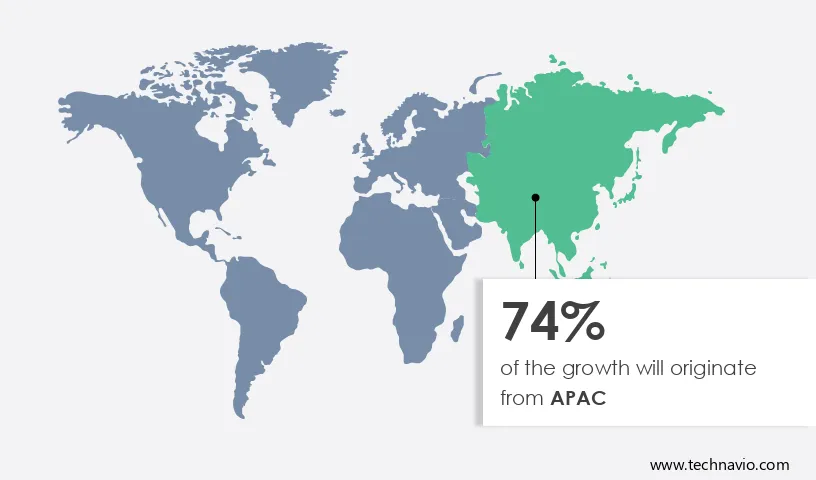

APAC is estimated to contribute 74% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period. APAC has some prominent semiconductor foundries, which produce the demand for FEOL semiconductor equipment. Furthermore, APAC is the largest consumer of semiconductor devices and contributes to more than 50% of the total revenue in the semiconductor industry due to the presence of dominant semiconductor front-end equipment market players.

In addition, the increasing industrialization and the significant production of automobiles and industrial machinery are demanding foundry equipment, which is driving the growth of the semiconductor front-end equipment market. In APAC, competitive manufacturing costs and high economic growth rates are the main factors that support the growth of the market in the rapidly growing end-user industries such as automotive, aerospace, and construction. These factors are also encouraging the global market players to expand their business in APAC. Hence, such factors are expected to drive market growth in this region during the forecast period.

The outbreak of COVID-19 negatively affected the growth of the front end of the line semiconductor equipment market in the APAC region. However, in 2021, the initiation of large-scale vaccination drives?lifted the lockdown and travel restrictions, which led to the resumption of supply chain activities. Furthermore, increasing demand for consumer electronics, the growing adoption of 5G technology, the expansion of automotive and transportation sectors, and the rising investments in smart manufacturing and industrial automation will fuel the growth of the regional market during the forecast period.

The Front End of the Line Semiconductor Equipment Market report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Global Front End of the Line Semiconductor Equipment Market Customer Landscape

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The research report also includes detailed analyses of the competitive landscape of the market and information about 20 market companies, including:

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

The front end of the line semiconductor equipment market report forecasts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and growth opportunities from 2018-2022.

|

Front End Of The Line Semiconductor Equipment Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

180 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.64% |

|

Market Growth 2024-2028 |

USD 7.56 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.15 |

|

Regional analysis |

APAC, North America, Europe, South America, and Middle East and Africa |

|

Performing market contribution |

APAC at 74% |

|

Key countries |

US, Taiwan, South Korea, Japan, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Allwin21 Corp., Applied Materials Inc., ASML, C and D Semiconductor Services Inc., CVD Equipment Corp., ECM USA Inc., Hitachi Ltd., Kingstone Semiconductor Joint Stock Co. Ltd., KLA Corp., Lam Research Corp., Mattson Technology Inc., Nikon Corp., Nissin Electric Co. Ltd., Screen Holdings Co. Ltd., Sumitomo Corp., SUSS MICROTEC SE, TBS Holdings Inc., Toyota Motor Corp., ULVAC Inc., and Veeco Instruments Inc. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, and market condition analysis for the forecast period. |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this market research report to meet your requirements.

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by End-user

7 Market Segmentation by Product

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights