Enjoy complimentary customisation on priority with our Enterprise License!

The dry eye syndrome drugs market size is forecast to increase by USD 2.15 billion, at a CAGR of 6.53% between 2022 and 2027. The market's expansion hinges on numerous factors, prominently the burgeoning geriatric population with a rising incidence of health concerns. The escalating healthcare expenditure and shifting lifestyles also play pivotal roles. Furthermore, the increasing prevalence of diseases like dry eye syndrome due to modern lifestyle choices underscores the market's growth trajectory. As individuals experience prolonged screen time and environmental factors impact ocular health, the demand for dry eye syndrome treatments intensifies. These interconnected dynamics drive innovation and investment in the ophthalmic industry, propelling advancements in eye care technologies and therapies to meet the evolving needs of consumers and healthcare providers alike.

To learn more about this report, View Report Sample

This market report extensively covers market segmentation by distribution channel (retail pharmacies, hospital pharmacies, and online pharmacies), product (OTC drugs and prescription drugs), and geography (North America, Europe, Asia, and Rest of World (ROW)). It also includes an in-depth analysis of drivers, trends, and challenges. Furthermore, the report includes historic market data from 2017 to 2021.

The market is driven by several factors, including the increasing prevalence of Dry Eye Disease among the Geriatric population and individuals with Autoimmune Disorders. Emerging trends in Alternative Therapies like Nutritional Supplements and Acupuncture are gaining traction. Innovations such as the CEQUA therapy drug and Preservative-free lubricant eye drops incorporating Nanodroplet technology represent significant advancements. However, challenges like navigating Regulatory procedures for Drug approval and conducting extensive Clinical trials to ensure safety and efficacy remain critical in this dynamic market landscape. The growing geriatric population is notably driving the market growth, although factors such as the presence of strong substitutes for treating dry eye syndrome may impede market growth. Our researchers analyzed the data with 2022 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The growing geriatric population is notably driving the market growth. Dry eye syndrome occurs when the eyes do not produce enough tears or when the tears evaporate too quickly. It is more prevalent among the geriatric population, and the risk of developing the condition increases with age. Asia is one of the most lucrative regions in the market owing to its rapidly growing geriatric population. However, North America and Europe hold the major shares owing to high investment in the healthcare sector.

Moreover, dry eye syndrome has a direct relation with age, as tear production declines with increasing age. According to the National Institutes of Health (NIH), the disease is more prevalent in people aged 50 years and above. Decreased tear production as a result of altered reflex secretion, lacrimal gland dysfunction, inflammatory destruction of lacrimal glands, or diminished corneal sensation may lead to tear deficiency, causing dry eye syndrome. Other factors, such as the use of topical medications, also increase the risk of dry eyes. These factors will drive market growth during the forecast period.

Advancements in drug delivery technologies are a key trend in the market. In recent years, there have been significant advancements in drug delivery systems aimed at improving the efficacy and convenience of dry eye syndrome treatments. These advancements have addressed various challenges associated with traditional eye drop formulations, such as low bioavailability, poor patient compliance, and inconsistent dosing.

Moreover, lipid-based formulations mimic the composition of natural tears and help stabilize the tear film, reducing tear evaporation. Sustained release drug delivery systems, such as hydrogels, inserts, and punctual plugs, have been developed to provide controlled and extended drug release over an extended period. Nanoparticles and nano micelles can encapsulate therapeutic agents, protect them from degradation, and enhance their penetration into ocular tissues. Hence, advancements in drug delivery technologies will propel the growth of the market during the forecast period.

The presence of strong substitutes for treating dry eye syndrome is challenging market growth. There are many options available for the treatment of dry eyes apart from medications, such as surgical procedures and nutritional supplements. Many patients with dry eyes undergo severe corneal injuries, leading to the loss of vision.

Moreover, advanced surgical procedures such as using salivary glands as an alternative for tears have been developed in the market. Minor gland salivary auto transplant is another new surgical technique that has demonstrated effectiveness in studies. Punctual occlusion is another non-therapeutic treatment for dry eye syndrome. These are small bags that seal the tear ducts, keeping the eyes moist. Therefore, the increasing adoption of alternative treatment options will hamper the revenue growth of the market during the forecast period.

The market report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Global Market Customer Landscape

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Bausch Health Co. Inc. - The company offers dry eye syndrome drugs such as NOV03. The Bausch Lomb International segment focuses on pharmaceutical products, OTC products, medical devices, for vision care, eye surgery, and other ophthalmic products.

The research report also includes detailed analyses of the competitive landscape of the market and information about 15 market companies, including:

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

The market encompasses various segments, from Eye Care Centers and Eye Clinics to Ophthalmologists and Optometrists practicing in Private Practices. With a focus on Clinical Care for DED (Dry Eye Disease), the market also explores Alternative Therapies such as Nutritional Supplements and Acupuncture. Key players like Alcon contribute with innovative products like the CEQUA therapy drug and Preservative-free lubricant eye drops, leveraging advancements like Nanodroplet technology. Factors like Hormonal changes, Geriatric population, and High screen time are significant influencers in the market, affecting Blood composition and exacerbating conditions in patients with Autoimmune Disorders or Rheumatic conditions. Navigating Regulatory procedures, Drug approval, and conducting Clinical trials are crucial steps for drug manufacturers targeting Dry Eye Syndrome, especially in populations affected by conditions like Diabetes. Understanding the role of Contact lenses and addressing High screen time challenges further segments the market, ensuring tailored solutions for diverse patient needs.

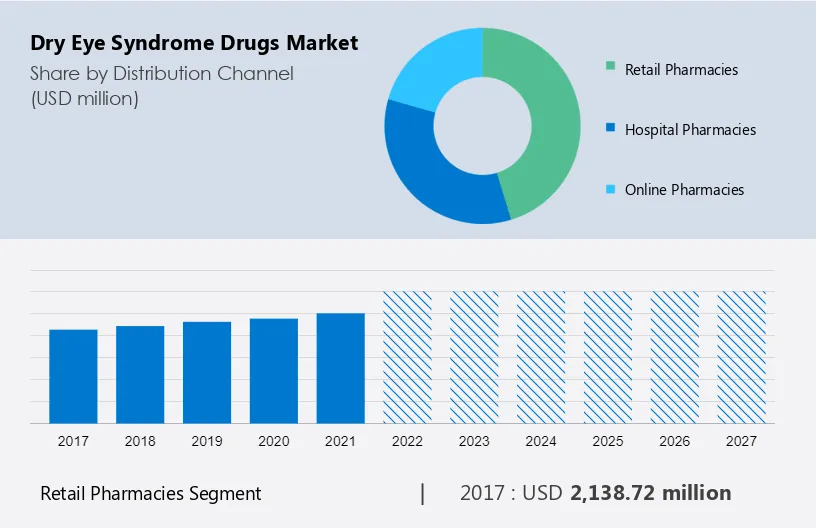

The market share growth by the retail pharmacies segment will be significant during the forecast period. Retail pharmacies play a critical role in the distribution and availability of drugs to consumers. They serve as convenient points of access for patients seeking OTC or prescription medications for managing dry eye symptoms. They generally include independent pharmacies, chain pharmacies, and drugstore retailers and stock a wide variety of drugs, including artificial tears, ointments, gels, and prescription medications. Patients can consult with pharmacists to receive guidance on the selection and proper use of dry eye medications.

Get a glance at the market contribution of various segments View the PDF Sample

The retail pharmacies segment was valued at USD 2.14 billion in 2017 and continued to grow until 2021. Retail pharmacies cater to the needs of patients who prefer in-person assistance, immediate availability, and personalized recommendations. Patients can discuss their symptoms and concerns with a pharmacist and purchase suitable drugs based on their requirements. These factors will drive the growth of the segment during the forecast period.

For more insights on the market share of various regions Download PDF Sample now!

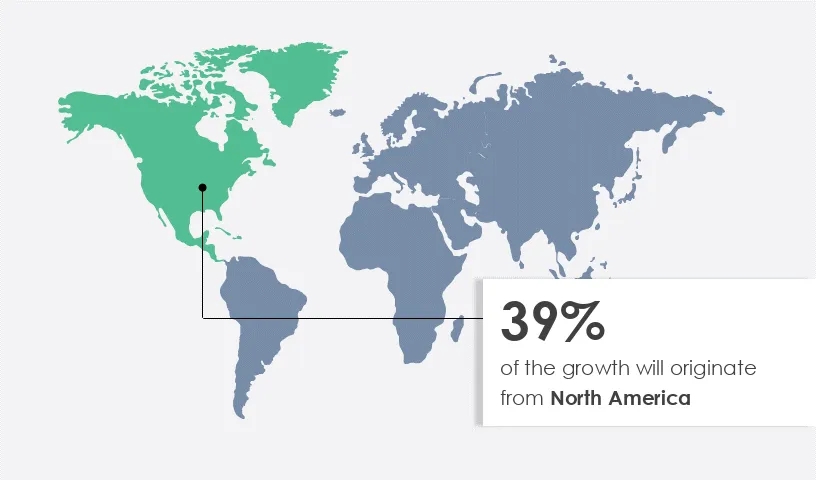

North America is estimated to contribute 39% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The US and Canada are the leading revenue-generating countries. The growth of the market in the region is attributed to factors such as the entry of new prescription-based products, the presence of pharmaceutical giants, and the high prevalence rate of dry eye diseases. The growing awareness and diagnosis of dry eye syndrome also have contributed to market expansion. Various types of drugs are available in the market, including artificial tears, anti-inflammatory drugs, immunosuppressants, and secretagogues. Several pharmaceutical companies are engaged in the development and commercialization of drugs in North America. These factors will fuel the regional market's growth during the forecast period.

The market report forecasts market growth by revenue at global, regional, & country levels and provides a market growth analysis of the latest trends and growth opportunities from 2017 to 2027.

The market is witnessing significant growth driven by various factors. Dry Eye Disease (DED), often linked to autoimmune disorders and hormonal changes, has become a prevalent concern, prompting increased attention from eye care centers and ophthalmologists. Alternative therapies such as acupuncture and innovative drug formulations like CEQUA therapy from Alcon are gaining traction. Emerging nanobiotechnology and microencapsulation techniques are revolutionizing drug delivery, offering preservative-free lubricant eye drops and nanodroplet technology for improved efficacy.

Furthermore, the market is dynamic, with optometrists and private practices playing key roles in clinical care for patients suffering from DED (Dry Eye Disease). As emerging markets witness a surge in DED cases, innovative treatments like the CEQUA therapy drug and preservative-free lubricant eye drops are gaining prominence. Factors such as high screen time, vitamin A deficiency, Lupus, and thyroid disease contribute to DED occurrence, impacting blood composition and tear glands. Diagnosis and treatment rely on understanding the functioning of the eye and addressing inflammation effectively, often utilizing drugs like cyclosporine with reversible pharmacokinetic characteristics to minimize systemic absorption.

Moreover, rising cases of diabetes and rheumatic conditions contribute to DED, necessitating advanced diagnosis and treatment methods. However, the market faces challenges such as regulatory procedures for drug approval and the high investment cost associated with developing novel drugs. Additionally, patient burden due to chronic health conditions and the need for collaboration between drug manufacturers, eye clinics, and healthcare infrastructure entities further shape the market landscape. Despite challenges, the market is propelled by ongoing clinical trials, promising Phase 3 data, and the introduction of advanced emerging drugs targeting Meibomian gland dysfunction and other underlying causes. As ocular conditions continue to affect a wide patient pool, the focus on healing treatments and patient-centric approaches remains crucial for sustainable growth in the market.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

161 |

|

Base year |

2022 |

|

Historic period |

2017-2021 |

|

Forecast period |

2023-2027 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.53% |

|

Market growth 2023-2027 |

USD 2.15 billion |

|

Market structure |

Fragmented |

|

YoY growth 2022-2023(%) |

5.51 |

|

Regional analysis |

North America, Europe, Asia, and the Rest of the World (ROW) |

|

Performing market contribution |

North America at 39% |

|

Key countries |

US, UK, Germany, Japan, and China |

|

Competitive landscape |

Leading companies, Market Positioning of companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Abbott Laboratories, AbbVie Inc., AFT Pharmaceuticals Ltd., Akorn Operating Co. LLC, Bausch Health Co. Inc., F. Hoffmann La Roche Ltd., GlaxoSmithKline Plc, I MED Pharma Inc., Johnson and Johnson Services Inc., Laboratoires THEA SAS, Mitotech SA, Novaliq GmbH, Novartis AG, Oasis Medical Inc., Otsuka Holdings Co. Ltd., Santen Pharmaceutical Co. Ltd., Sentiss Pharma Pvt. Ltd., Sun Pharmaceutical Industries Ltd., Viatris Inc., and Visufarma |

|

Market dynamics |

Parent market analysis, Market forecasting, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for the forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this market research report to meet your requirements.

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Distribution Channel

7 Market Segmentation by Product

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights

- US,UK,Germany,Japan,China - Size and Forecast 2023-2027")