Enjoy complimentary customisation on priority with our Enterprise License!

The flight simulator market size is estimated to grow by USD 2.84 billion at a CAGR of 6.62% between 2022 and 2027. The demand for cost-effective virtual training in the aviation industry continues to rise due to its ability to provide realistic training scenarios without the high costs associated with traditional methods. Additionally, investments in simulations are increasing as companies recognize the benefits of using virtual environments to train employees and simulate complex scenarios. Collaboration among companies and OEMs (Original Equipment Manufacturers) is also important, as it can lead to the development of innovative solutions and improved programs.

Market Forecast 2023-2027

To learn more about this report, Request Free Sample

This report extensively covers market segmentation by product type (military flight simulator and commercial flight simulator), platform (rotary wing simulator, fixed wing simulator, and UAV simulator), and geography (North America, APAC, Europe, South America, and Middle East and Africa). It also includes an in-depth analysis of drivers, trends, and challenges.

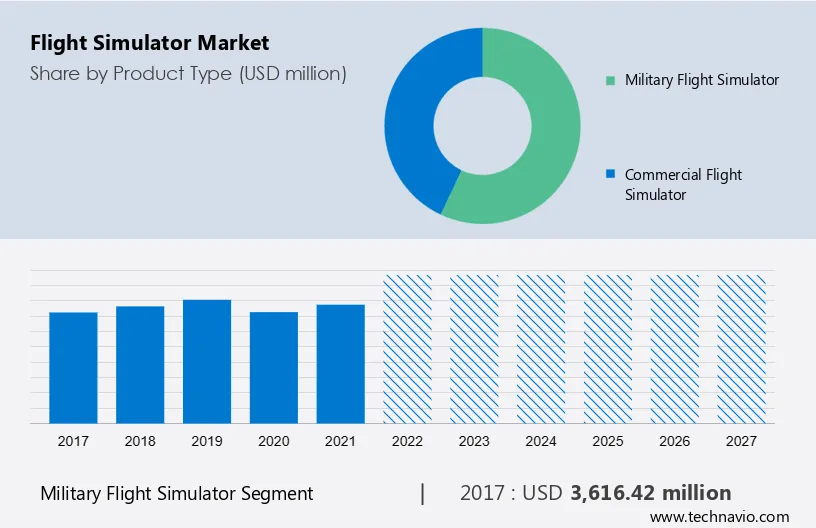

The military flight simulator segment will account for a major share of the market's growth during the forecast period. Significant factors that stimulate the growth of the market in the military segment are the increasing demand for synthetic training environments and an increased focus on virtual boot camps.

Get a Customised Report as per your requirements for FREE!

The military flight simulator segment was valued at USD 3.62 billion in 2017. This can be divided into two categories: full-flight simulators (FFS) and flight simulation training devices (FSTD). FFS allows pilots to train on a replica of a specific aircraft, while FSTD allows soldiers to train on a replica and other devices. Real-time simulations are time-consuming and have low reusability, resulting in increased costs for the military. They come in different models, depending on the aircraft being trained, to accommodate all three branches of the military (Air Force, Army, and Navy). However, all simulations have a similar setup that includes an electronic motion base or hydraulic lift system that responds to the user's inputs and provides haptic feedback. These factors are expected to drive the demand worldwide, thereby boosting the growth of the segment of the market during the forecast period.

For more insights on the market share of various regions View PDF Sample now!

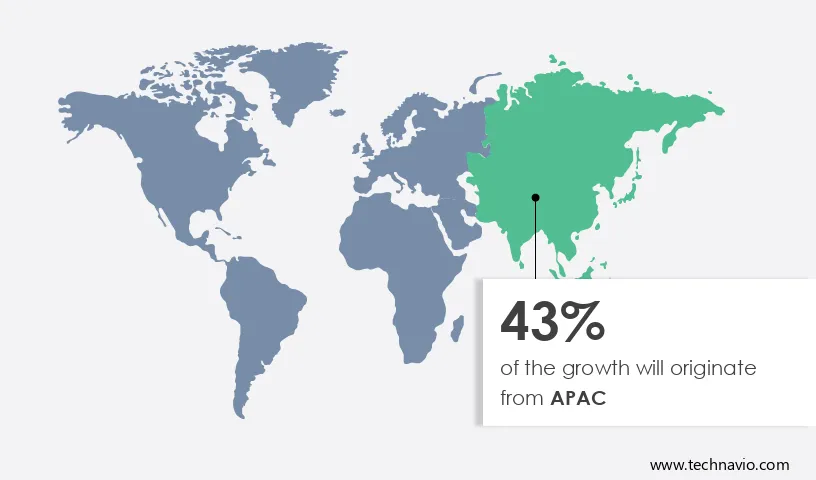

APAC is estimated to contribute 43% to the growth by 2027. Technavio’s analysts have elaborately explained the regional trends, drivers, and challenges that are expected to shape the market during the forecast period. Another region offering significant growth opportunities to companies is North America. The North American market is anticipated to experience a consistent growth rate due to increased investments by defense ministries in military training. The United States and Canada are the dominant players in this market. The US Department of Defense is collaborating with simulation companies to improve their services. The American market is showing steady growth due to the presence of major players such as L3Harris Technologies, CAE, and Boeing.

Moreover, companies in the region are offering virtual training modules that can be accessed through desktops, allowing trainers to access various scenarios. They are also integrating data analytics to improve the effectiveness of these systems. For example, CAE offers the CAE Rise flight simulator, which is a data-driven training system that uses analytics to improve military training. CAE Rise allows instructors to objectively assess pilot competencies using live data and provides standardized training to trainees. As a result, the product offerings of the company based on scenarios and models are expected to have a significant impact on the regional market in the future.

The market is experiencing significant growth, driven by advancements in aerospace technology and the increasing demand for pilot training. These simulators replicate the environment with sophisticated software and hardware, including realistic visual systems. They are utilized by various stakeholders, including pilots, aircraft manufacturers, and training institutions. Start-ups and investors are also entering the market, attracted by the potential in both the civil aviation and defense aviation sectors. With the rise in passenger air travel and the integration of unmanned aerial vehicles (UAVs), the demand for aircraft simulation technology (AST) is expected to soar. Key players like Textron are driving innovation in this sector, catering to the needs of airline firms, lessors, and others seeking to enhance their aircraft operation and training capabilities. The International Air Transport Association reports that the use of these simulators has become integral to maintaining safe and efficient air travel. Our researchers studied the data for years, with 2022 as the base year and 2023 as the estimated year, and presented the key drivers, trends, and challenges for the market.

Real-time training can be expensive due to its resource-intensive nature, whereas virtual training is more cost-effective, driving market growth. Real-time training involves additional expenses for fueling military platforms, acquiring training ammunition, and covering operational costs. This is particularly relevant for investors in the aerospace sector, as they consider factors like aircraft operation and pilot training when evaluating investments in aerospace technology. This mitigates risks associated with real-time training, such as personnel and equipment involvement. These agencies are increasingly adopting simulation and synthetic training methods for their benefit. Simulation and virtual training systems utilize commercial-off-the-shelf (COTS) components with plug-and-play capabilities.

Simulators rely heavily on COTS components to avoid the higher costs of customized equipment. These standardized components can be easily replaced with upgraded or different parts from other suppliers, maintaining functionality. This approach is beneficial for various stakeholders involved in the aviation industry, including those concerned with the aircraft flight environment, pilots, aircraft manufacturers, software developers, hardware suppliers, visual system providers, and other stakeholders. This practice is common in the aviation industry, reducing downtime for equipment compared to real-time training. Therefore, the adoption of these is expected to drive demand for these simulators, fueling market growth.

Training for 3D simulation focuses on fundamental aspects of UAV operation, including takeoff and landing, in-flight procedures, and resolving issues during various applications. These applications include commercial, scientific research, search and rescue, 3D mapping, and military operations. The simulation model utilizes actual UAV autopilot data to provide real-time situational awareness. The 3D simulation model enables a complete and operational 3D virtual world, including both voluntary and involuntary actions, as well as natural terrains such as realistic lighting conditions (time of day), photo-textures, urban areas, roads, railroad networks, airports, and real geological features and terrain database.

In addition, the 3D simulation model generates real-time videos to provide payload output both in infrared and visual modes. Also, it provides a tactical environment through a virtual environment to improve capabilities. For instance, H-SIM provides a real-time flight simulator, Simdrone. Likewise, Research Triangle Institute (RTI) International provides 3D simulation solutions such as RTI iShoppe Virtual Environment. Therefore, such developments will fuel the market growth during the forecast period.

The market may face challenges due to the high cost of flight simulators. This may prevent smaller companies and schools with limited budgets from investing in advanced training technologies. As a result, there may be reduced demand for simulators. Furthermore, the high cost of these may limit their accessibility to certain regions or organizations. However, in developing countries or smaller centers, purchasing the latest simulators or upgrading existing ones may not be financially feasible, which can hinder the growth and accessibility of virtual knowledge solutions. It's important to note that it requires ongoing maintenance, software updates, and occasional hardware upgrades to remain effective and up-to-date, making them a continuous investment.

Due to the high cost of these simulators, some organizations may opt for alternative methods, such as less-sophisticated simulators, virtual reality, or traditional aircraft-based knowledge, which can limit the demand. As a result, the high cost of simulators may hinder their adoption and adversely impact the market's growth during the forecast period.

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Aero Simulation Inc. - The company offers flight simulators such as Boeing 737-800 Flight Simulator, and the Airbus A320-200 Flight Simulator.

We also have detailed analyses of the market’s competitive landscape and offer information on 20 market companies, including:

Aero Simulation Inc., Airbus SE, Avenger Flight Group LLC, Berkshire Hathaway Inc., CAE Inc., FenixSim Ltd., Flight Sim Labs Ltd., Flight Simulation Technique Centre Pvt. Ltd., Gen24 Flybiz Pvt. Ltd., Groupe Gorge, HAVELSAN Inc., Indra Sistemas SA, L3Harris Technologies Inc., Lockheed Martin Corp., Raytheon Technologies Corp., Textron Inc., Thales Group, The 737 Experience, The Boeing Co., and VIER IM POTT.

Technavio report provides an in-depth analysis of the market and its players through combined qualitative and quantitative data. The analysis classifies companies into categories based on their business approaches, including pure-play, category-focused, industry-focused, and diversified. Companies are specially categorized into dominant, leading, strong, tentative, and weak, based on their quantitative data analysis.

The market report forecasts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and growth opportunities from 2017 to 2027.

The market is vital for aviation safety and pilot training, offering realistic simulation conditions and aircraft orientation. It plays a crucial role in accident investigation, providing an analytical depiction of flight data through devices like cockpit voice recorders and flight data recorders. With pilot shortages and cost concerns impacting the aviation industry, they offer cost-effective and safe training solutions. They also help in handling diverse flight conditions and scenarios, making them essential for civil aviation and military aircraft operations. As the global aviation sector grows, the flight simulator market is expected to expand, driven by advancements in simulation technology and training devices.

The market is a critical component of the aircraft industry and aviation safety, providing realistic environments for pilots and crew members. It plays a vital role in accident investigation and aviation research, offering insights into data and human factors. With the increasing demand for air travel and aerial connectivity, the market is poised for growth, driven by factors such as air traffic passenger demand and civil aviation industry expansion. Advanced simulation software and hardware enable realistic flight practice and training, ensuring pilot proficiency and safety. As the aviation industry evolves, the market continues to innovate, enhancing activities and safety standards.

The market is a critical aspect of aviation safety and pilot training, aiding in accident investigation and research. It encompasses various elements such as full flight simulators (FFS), flight training devices, and civil aviation simulators. These tools provide a realistic simulation of flight conditions and scenarios, helping pilots practice flight maneuvers and emergency procedures in a safe environment. The market is influenced by factors like air passenger revenues and fleet expansions, with the Federal Aviation Administration (FAA) playing a crucial role in setting safety standards. As the industry evolves, the demand for simulation-based training and advanced simulators is expected to grow, ensuring pilot proficiency and aviation safety.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

160 |

|

Base year |

2022 |

|

Historic period |

2017-2021 |

|

Forecast period |

2023-2027 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.62% |

|

Market growth 2023-2027 |

USD 2.84 billion |

|

Market structure |

Fragmented |

|

YoY growth 2022-2023(%) |

6.38 |

|

Regional analysis |

North America, APAC, Europe, South America, and Middle East and Africa |

|

Performing market contribution |

APAC at 43% |

|

Key countries |

US, China, India, UK, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Aero Simulation Inc., Airbus SE, Avenger Flight Group LLC, Berkshire Hathaway Inc., CAE Inc., FenixSim Ltd., Flight Sim Labs Ltd., Flight Simulation Technique Centre Pvt. Ltd., Gen24 Flybiz Pvt. Ltd., Groupe Gorge, HAVELSAN Inc., Indra Sistemas SA, L3Harris Technologies Inc., Lockheed Martin Corp., Raytheon Technologies Corp., Textron Inc., Thales Group, The 737 Experience, The Boeing Co., and VIER IM POTT |

|

Market dynamics |

Parent market analysis, Market Forecasting, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for the forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Product Type

7 Market Segmentation by Platform

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights