Enjoy complimentary customisation on priority with our Enterprise License!

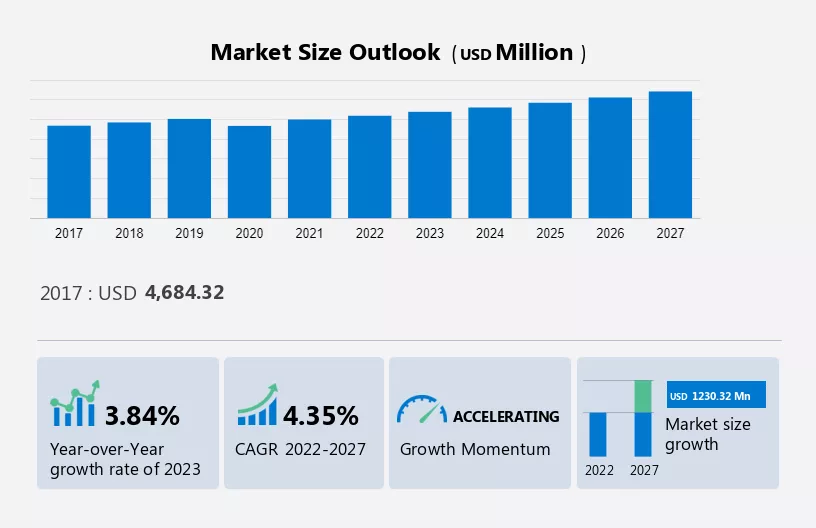

The Industrial Chillers Market size is estimated to grow by USD 1.23 billion at a CAGR of 4.35% between 2022 and 2027. The growth of the market depends on several factors such as the growing adoption of district heating and cooling infrastructure, stringent regulations on refrigerant use, and the growing use of industrial chillers across various industries.

The report also includes an in-depth analysis of drivers, trends, and challenges. Furthermore, the report includes historic market data from 2017 to 2021.

To learn more about this report, Download a FREE Report Sample

The report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies

Global Market Customer Landscape

Our researchers analyzed the data with 2022 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The growing adoption of district heating and cooling infrastructure is the key factor driving the market growth. A district cooling system is an economical option compared to running compressors for refrigeration, which require more energy. The system requires a central refrigeration plant, pumping stations, and a piping network. District cooling replaces traditional air cooling because it offers many advantages, such as energy savings, less environmental impact, and less maintenance requirements. They are often used in district cooling systems that can process and cool large volumes of water. Operating these large systems can result in significant power savings.

District cooling systems are highly adopted in many developed countries such as the United States, Canada, Japan, and European countries to reduce power consumption and environmental impact in large cities and high-density industries. Some Middle Eastern countries with hot climatic conditions, such as the UAE, Qatar, and Kuwait, use this technology because the energy consumption for cooling is very high. In developing countries, district cooling systems are relatively new as these systems are mostly used in industrial parks. The development of smart cities and the increasing urban population in these regions could lead to higher adoption of these systems. The global market is expected to grow during the forecast period owing to the increasing adoption of district heating and cooling infrastructure.

The advent of smart connected chillers will fuel the market growth. Growing need to improve reliability and performance, minimize equipment downtime, and reduce overall maintenance costs for chillers used in HVAC and R applications. This drives manufacturers to implement sensors and connectivity technologies into chillers. The advent of intelligently connected chillers is revolutionizing the way chillers are serviced and maintained. These chillers can be accessed and controlled remotely through a local network or internet cloud.

Intelligently connected chillers stream data directly from the device to the cloud for further use by technicians for advanced analytics and remote monitoring. With the advent of intelligently connected chillers, machine operators can predict when a chiller will fail or operate below peak capacity. This enables operators to perform early or predictive maintenance, promising fewer disruptions, less downtime, and longer equipment life. Some of the key features of smart connected chillers are critical alarm systems, cloud data storage, and remote monitoring and diagnostics functionality.

The high capital and maintenance costs can majorly impede the growth of the market. Various industries are focusing on improving the energy efficiency of their facilities, reducing energy costs, and reducing emissions, which is expected to create significant opportunities for the growth of the global market. However, high acquisition and maintenance costs are major challenges that may hinder market growth during the forecast period. Most energy-efficient HVAC and R technologies are significantly more expensive than their traditional counterparts. These offer significant energy savings but can significantly lengthen the break-even point of your return on investment.

The high cost of these can be a major challenge for budget-conscious customers, especially in emerging markets. Most industries and trading companies in developing countries such as India and China are very price-sensitive. Therefore, they are more concerned about initial acquisition costs. Annual maintenance costs are 20% to 35% higher than traditional chillers and can add up to a significant amount over the years. Therefore, the relatively high cost of industrial chillers is one of the main reasons expected to affect the market growth during the forecast period.

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Ait Deutschland GmbH: The company is involved in producing and developing energy-efficient chiller solutions for different industrial applications. It also offers that have optimal efficiency.

Carrier Global Corp: The company offers different value-added features such as rotary scroll compression and a quiet AeroAcoustic fan system.

We also have detailed analyses of the market’s competitive landscape and offer information on 20 market companies, including:

The report offers clients a deeper understanding of the market and its players through a combined qualitative and quantitative analysis of the companies. The analysis classifies companies into categories based on their business approach, including pure-play, category-focused, industry-focused, and diversified. companies are specially categorized into dominant, leading, strong, tentative, and weak to understand the dos and don’ts of business, which can help a client make the best decision.

The chemical and petrochemical industries segment will contribute a major share of the market, as these industries will be the major end users of the global market in 2022. The chemical and petrochemical industries segment showed a gradual increase in market share with USD 1,395.97 million in 2017 and will continue to grow by 2021. They are used in industry to maintain the temperature of process equipment or to cool chemicals and petrochemicals that need to be kept cold. Industries such as chemicals and petrochemicals are some of the major industrial consumers. These chillers can be directly integrated into the process and use the waste heat generated by the device. For example, heat from flue gas, wastewater, reflux condensers, intermediate compressor stages, and expander systems can be used to operate chillers. Such integration allows industrial customers to reduce fuel consumption and minimize the amount of heat released into the environment. Therefore, increasing investment in the above industries will directly affect the demand.

Get a Customised Report as per your requirements for FREE!

Industrial chillers are widely used in these industries to cool process chemicals and petrochemicals. Therefore, increasing investment in the oil and gas industry, such as petrochemical capacity expansion and new drilling activities, will be a key factor driving the growth of the global industrial chiller market. Such factors are anticipated to drive the growth of the chemical and petrochemical industry in the global market during the forecast period.

The economizer segment is leading when it comes to the type of industrial chillers used widely. Increasing investment in data centre construction will drive the market growth of this segment over the forecast period. The growth rate is expected to stabilize from 2022 onwards, as almost all data centres in countries with suitable climate conditions will be integrated into the use of free cooling technology. For example, on March 8, 2023, Vertiv Corp installed cold water thermal walls in Europe and its MEA slab floor data centres. Slab-floor data center design allows new empty space to be built faster and at a lower cost. As economizers are a cost-effective data centre cooling solution, increasing demand for data centers is expected to boost the demand for economizers during the forecast period. Such factors are anticipated to drive the growth of the global market during the forecast period.

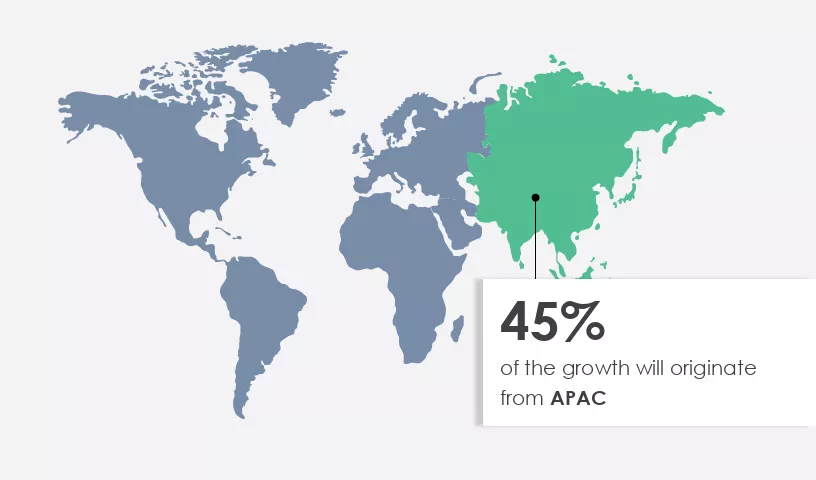

APAC is estimated to contribute 45% to the growth by 2027. Technavio’s analysts have elaborately explained the regional trends, drivers, and challenges that are expected to shape the market during the forecast period.

For more insights on the market share of various regions View PDF Sample now!

Asia Pacific is the largest market due to huge demand from China, Japan, India, and some countries in Southeast Asia. Factors such as rapid population growth, increasing industrialization, increasing urbanization, and increasing number of major trading companies are driving the growth of the market in the region. Growth in commercial and residential construction is a major driver of demand for medium to heavy-duty heating, ventilation, air conditioning, and refrigeration (HVAC & R) equipment in the region, and is also driving growth in the market. Adoption of green building initiatives in some countries such as China and India will be another factor boosting the demand in APAC during the forecast period.

The market report forecasts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and growth opportunities from 2017 to 2027.

The Market is influenced by factors such as valuation and per capita income, driving demand for cooling solutions like air conditioners and refrigerators across industries. In the healthcare and food sectors, chillers play a crucial role in maintaining temperature-sensitive products such as frozen food and pharmaceuticals.

Companies like Carrier and Daikin offer innovative solutions like the AquaForce Vision 30KAV air-cooled chillers and inverter-driven water-cooled and air-cooled screw chiller series to meet the diverse needs of industries. The market also caters to the data center and construction sectors, emphasizing the importance of temperature control in various applications. With growing concerns about global warming, industries are adopting more energy-efficient and environmentally friendly solutions. Manufacturers like Modine Manufacturing Company and M&M Carnot Refrigeration offer low-charge packaged ammonia/NH3 (R717) chiller series to address these needs, ensuring sustainable cooling solutions for the future. The Market also serves diverse sectors like the healthcare, food, pharmaceutical, and data center industries, providing crucial process cooling solutions. It also supports construction activities, offering industrial refrigeration systems for various applications. In the food and beverage segment, breweries and wineries rely on glycol chillers for efficient temperature control.

|

Industrial Chillers Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

163 |

|

Base year |

2022 |

|

Historic period |

2017-2021 |

|

Forecast period |

2023-2027 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.35% |

|

Market growth 2023-2027 |

USD 1230.32 million |

|

Market structure |

Fragmented |

|

YoY growth 2022-2023(%) |

3.84 |

|

Regional analysis |

APAC, North America, Europe, Middle East and Africa, and South America |

|

Performing market contribution |

APAC at 45% |

|

Key countries |

US, China, Japan, Germany, and UK |

|

Competitive landscape |

Leading companies, Market Positioning of companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

ait deutschland GmbH, Carrier Global Corp., Daikin Industries Ltd., Drake Refrigeration Inc., FRIGEL FIRENZE S.p.A., Friulair S.r.l., General Air Products, Johnson Controls International Plc., LG Corp., Mitsubishi Electric Corp., MTA S.p.A., Paul Mueller Co. Inc., PolyScience, Raytheon Technologies Corp., Reynold India Pvt. Ltd., Senho Machinery Shenzhen Co. Ltd., Sentry Equipment Corp., Smardt Chiller Group Inc., Trane Technologies Plc, and HYDAC Technology Corp. |

|

Market dynamics |

Parent market analysis, Market forecasting, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for the forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by End-user

7 Market Segmentation by Type

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights