Enjoy complimentary customisation on priority with our Enterprise License!

The Marine Propulsion Engine Market size of the market is forecast to increase by USD 1.54 billion, at a CAGR of 3.99% between 2022 and 2027. Market expansion in the marine industry is contingent upon several factors, prominently the surge in maritime trade and the concurrent expansion of fleet sizes worldwide. Additionally, there is a burgeoning demand for naval vessels, predominantly driven by defense requirements across various nations. Furthermore, the growing adoption of liquefied natural gas (LNG) as a marine fuel is reshaping the industry landscape, fueled by its lower emissions and cost-effectiveness compared to traditional fuels. As environmental regulations become more stringent, the marine sector is increasingly turning to LNG to comply with emissions standards while maintaining operational efficiency. These converging trends underscore a promising outlook for the market, with sustained growth anticipated as maritime activities continue to expand and the adoption of LNG gains traction within the industry.

To learn more about this market report, Download Report Sample

This report extensively covers market segmentation by application (passenger, commercial, and defense), type (diesel and gas), and geography (APAC, Europe, North America, Middle East and Africa, and South America). It also includes an in-depth analysis of drivers, trends, and challenges. Furthermore, the report includes historic market data from 2017 to 2021.

In the market, innovations in impellers, cylinder blocks, and valves are optimizing performance and efficiency. Liners and towers enhance durability, while advancements in materials and design cater to the demanding conditions of cargo ships. Ship owners are increasingly seeking alternatives to Heavy Fuel Oil, exploring eco-friendly options like biofuels and minerals. These developments underscore a growing emphasis on sustainability and efficiency in maritime operations, driving the demand for modern propulsion solutions and reducing reliance on traditional fossil fuels.

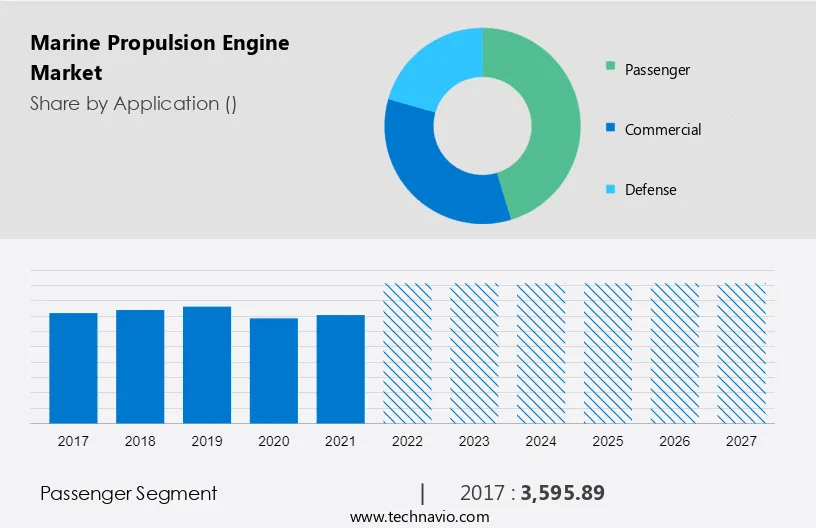

The passenger segment will contribute a major share of the market. The passenger segment is an important segment in the market. This segment includes passenger ships, ferries, cruise ships, and other types of vessels designed to carry people across various waterways. Engines used in the passenger segment are designed to provide high levels of reliability, efficiency, and passenger comfort while ensuring compliance with stringent environmental regulations.

Get a Customised Report as per your requirements for FREE!

The passenger segment showed a gradual increase in the market share with USD 3.60 billion in 2017. Marine propulsion engines are typically classified by horsepower, fuel type, and technology. For example, diesel engines, known for their fuel efficiency and reliability, are commonly used on passenger ships. Similarly, electric drive systems are gaining importance in the passenger segment due to their low noise and emission levels. The passenger segment also includes different types of vessels with different performance requirements, from small ferries to large cruise ships. These engines used in the passenger segment are therefore available in a wide power range from hundreds of kilowatts to several megawatts. The demand is expected to continue to grow, driven by the growing demand for environmentally friendly and efficient propulsion solutions. Such factors drive the growth of the passenger segment in the market during the forecast period.

The diesel segment held the largest share of the market, with a market share of around 50%. Diesel is the most common type of fuel in the marine sector for onboard propulsion engines. It is widely popular and favored because it costs less than any other form of fuel. However, this segment faces major challenges in the form of environmental regulations and is threatened by the LPG fuel segment, which is seen as a greener alternative. Diesel engines currently dominate the market. However, its share is expected to decrease during the forecast period as more engines will be replaced by those using natural gas as fuel. Shipbuilding industry momentum is likely to come from APAC countries during the forecast period. Shipping companies and ocean freight forwarders are increasingly looking for super-large vessels that offer fuel efficiency and economies of scale. Due to the presence of huge shipyards and deep ports in APAC, shipyards in the region are well-positioned to deliver such vessels. Orders for new ships are sluggish in almost every region of the world, especially in the shipbuilding powerhouses of China, South Korea, and Japan. This poses a challenge as diesel propulsion engine manufacturers face declining demand from the sector. Such factors will hinder the growth of the diesel segment of the market during the forecast period.

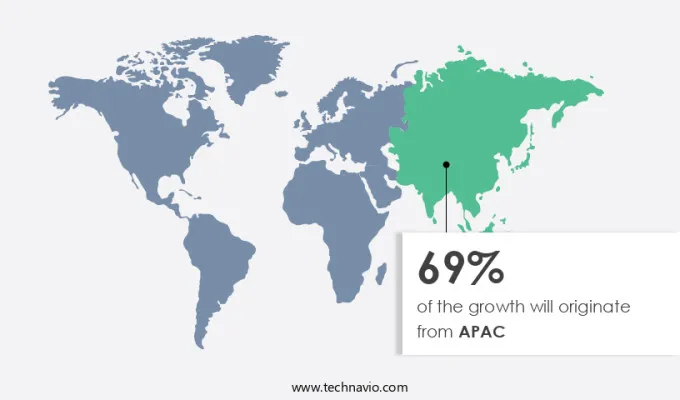

APAC is estimated to contribute 69% to the growth by 2027. Technavio’s analysts have elaborately explained the regional trends, drivers, and challenges that are expected to shape the market during the forecast period.

For more insights on the market share of various regions View PDF Sample now!

The shift in mass production of commodities to APAC due to the comparative cost advantages offered by the region was facilitated by the increasing size of container ships. As global trade expands, so does the demand for new vessels, especially containerships and tankers capable of transporting oil, natural gas, and more. The APAC countries such as China, Japan, and South Korea hold the highest share of the market. However, Japan has implemented strategies and plans to account for about one-third of the global shipbuilding industry in terms of ships completed by the end of the forecast period. These countries will continue to adopt heavy investments and technologies to increase their market share during the forecast period.

The report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Market Customer Landscape

The market is witnessing a transformation driven by concerns over fossil fuel consumption and environmental sustainability. Ship owners are increasingly exploring alternatives such as biofuels and synthetic fuels to replace traditional Heavy Fuel Oil. Moreover, advancements in exhaust gas aftertreatment systems and sensors enable better emission control and efficiency. Advanced controls and remote monitoring technologies optimize engine performance and maintenance. Electric propulsion, utilizing electrical motors, propellers, and pump jets, is gaining traction, reducing reliance on internal combustion engines. As the industry moves towards greener solutions, the focus remains on efficient utilization of natural resources and minimizing environmental impact in both consumer supplies and container ship sectors. Our researchers analyzed the data with 2022 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

An increase in maritime trade and fleet size is the key factor driving the market. International maritime trade shows healthy growth every year. Rapid industrialization and economic liberalization are the two key drivers of maritime trade volume, facilitating trade between nations. The development of multi-fuel engines and increased fuel efficiency have made ships a viable means of transportation. Demand for shipping trade is the largest among developing countries in Asia. Population growth in emerging markets has increased the demand for commodities and raw materials from these regions. For this reason, there is an increasing demand for building bulk cars, containers, or cargo ships.

Additionally, large ships are essential for efficient trade. The size of a ship has a direct effect on increasing the number of goods carried on a voyage. The expansion of maritime trade and an increase in the number of ocean-going ships will lead to an increase in CO2 emissions. The growing interest in reducing marine emissions and tightening emissions regulations have led to increased adoption of low-carbon ships. Such factors are anticipated to drive the market during the forecast period.

Technology focus shifting toward the development of dual-fuel engines will fuel the market. As the name suggests, a dual-fuel engine is one that uses both diesel and gas as fuel sources to power a vessel's engine. These engines draw natural gas into the compression chamber along with air. Diesel is used to ignite the mixture, and gas serves as the primary fuel source. Diesel is commonly a standby fuel and is used when the gas supply to the engine is restricted. A major advantage of fuel switching to natural gas is the effective reduction of emissions compared to diesel engines and other engine technologies that only reduce specific emissions.

For example, Wartsila's low-pressure dual-fuel engine helps reduce NOx emissions by 85%, SOx emissions by 99%, particulate matter by up to 99%, and carbon dioxide emissions by 20% to 30%. These engines also offer the high energy efficiency, long-term reliability, torque, and power characteristics of diesel engines and reduce operating costs by replacing diesel with gas. The advantages of dual-fuel engines allow merchant shipping lines to reduce fuel costs while reducing emissions. Such technological and commercial advancements are likely to be adopted across different industries and regions, leading to the growth of the market during the forecast period.

Volatility in crude oil and natural gas prices can majorly impede the growth of the market. Crude oil involves a complex value chain from production to distribution and supply and demand in the oil and gas industry, making accurate price forecasting extremely difficult. Oil prices have fluctuated many times over the past decade, making them a highly volatile commodity. Past and present oil price volatility has vaguely followed what is now called the 'oil price cycle'. However, it is difficult to predict oil prices.

Furthermore, increasing demand for natural gas will expose consumers to higher natural gas prices over time. Fluctuations in the prices of crude oil and natural gas affect the profits of oil and gas companies, creating a domino effect. Therefore, if the selling price falls, production will also fall. Some vessels, such as tankers, rely heavily on transporting crude oil and natural gas to refineries, end-users, and other stakeholders in the value chain, so the decline in production will affect the shipping industry. This will adversely affect the growth of the market during the forecast period.

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

We also have detailed analyses of the market’s competitive landscape and offer information on 18 market companies, including:

The report offers clients a deeper understanding of the market and its players through a combined qualitative and quantitative analysis of the companies. The analysis classifies companies into categories based on their business approach, including pure-play, category-focused, industry-focused, and diversified. Companies are specially categorized into dominant, leading, strong, tentative, and weak to understand the dos and don’ts of business, which can help a client make the best decision.

The market forecasting report forecasts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and growth opportunities from 2017 to 2027.

The market is undergoing significant transformation due to factors such as Heavy Fuel Oil (HFO) regulations, stringent emission standards, and the shift towards carbon-neutral fuels. Shipbuilders, fuel suppliers, and regulators are pivotal in shaping this transition. Technologies like electric propulsion engines and gas turbines are gaining traction, driven by concerns over greenhouse gas emissions and fuel efficiency. Initiatives like the International Maritime Organization (IMO) emission regulations and tax incentives for eco-friendly solutions are driving investment in intelligent ships and alternative fuels such as bio-methane and algal oils. Key players, including engine manufacturers like HSD Engine, are focusing on developing low-sulfur engines and waste heat reduction systems to meet Sulfur Emission Control Areas standards and reduce environmental impact. The market encompasses a wide range of vessels, from containerships to LNG carriers, each demanding efficient propulsion solutions to navigate the evolving regulatory landscape and meet 20,000 HP power requirements.

Additionally, the marine propulsion engine market is undergoing a paradigm shift driven by various factors, including regulatory pressures such as Sulfur Emission Control Areas, which necessitate the adoption of cleaner fuels and technologies to reduce sulfur oxides and nitrogen oxides (NOx) emissions. Engine manufacturers are innovating with advanced designs like gas turbines, dual-fuel diesel, and natural engines to meet stringent environmental standards while maintaining fossil fuel usage efficiency. Technological advancements such as artificial intelligence (AI) are enhancing propulsion systems' efficiency and reliability. These developments are crucial for the maritime industry, encompassing various sectors like international trade, shipping businesses, and defense applications, which rely on marine propulsion engines for efficient transportation of manufactured products, agricultural goods, automobiles, and other commodities while mitigating environmental impact and ensuring load capacity optimization.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

172 |

|

Base year |

2022 |

|

Historic period |

2017 - 2021 |

|

Forecast period |

2023-2027 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.99% |

|

Market growth 2023-2027 |

USD 1.54 billion |

|

Market structure |

USD Fragmented |

|

YoY growth 2022-2023(%) |

3.47 |

|

Regional analysis |

APAC, Europe, North America, Middle East and Africa, and South America |

|

Performing market contribution |

APAC at 69% |

|

Key countries |

US, China, South Korea, Japan, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

AB Volvo, ABB Ltd., BAE Systems Plc, Beta Marine Ltd., Caterpillar Inc., Cummins Inc., Daihatsu Diesel Mfg. Co. Ltd., General Electric Co., Hyundai Heavy Industries Co. Ltd., IHI Corp., Kawasaki Heavy Industries Ltd., Kongsberg Gruppen ASA, Leonardo DRS Inc., Mitsubishi Heavy Industries Ltd., Porsche Automobil Holding SE, Rolls Royce Holdings Plc, Shandong Heavy Industry Group Co. Ltd., Steyr Motors Betriebs GmbH, Wartsila Corp., and Yanmar Holdings Co. Ltd. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, Market growth and Forecasting, COVID 19 impact and recovery analysis and future consumer dynamics, Market condition analysis for forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Application

7 Market Segmentation by Type

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights