Enjoy complimentary customisation on priority with our Enterprise License!

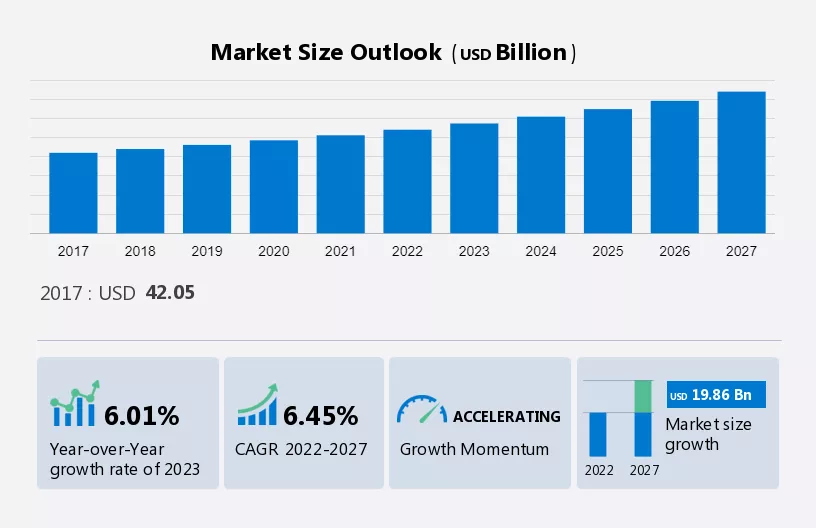

The global plastic additives market size is estimated to grow by USD 19.86 billion at a CAGR of 6.45% between 2022 and 2027. Market expansion hinges on a multitude of factors, notably the escalating demand for recycled plastics within the packaging sector, driven by a global push for sustainability. Additionally, the surge in demand for plastic additives, particularly in developing nations, contributes significantly to market growth spurred by rapid industrialization and infrastructure development. Moreover, the burgeoning e-commerce market fuels increased demand for plastics across various applications, ranging from packaging materials to product components. These dynamics underscore the pivotal role of recycled plastics and plastic additives in meeting the evolving needs of diverse industries while addressing environmental concerns. As sustainability practices gain prominence and consumer preferences evolve, the market for recycled plastics and plastic additives is poised for substantial growth, offering opportunities for innovation and collaboration across the value chain.

View the Bestselling Market Report sample Instantly

The market encompasses a wide range of products used to enhance the properties of polymers in various sectors. These additives include plasticizers like Phthalates and Bisphenol, which improve flexibility and elongation in plastics. Heavy metals, such as lead and cadmium, serve as stabilizers and pigments, ensuring long-term durability and aesthetic appeal. Governmental regulations play a significant role in the market, particularly concerning the use of chemicals like Phthalates and Bisphenol in consumer products.

This report extensively covers market segmentation by type (modifier, stabilizers, extenders, and processing aids), application (packaging, consumer goods, automotive, electrical and electronics, and others), and geography (APAC, North America, Europe, South America, and Middle East and Africa). It also includes an in-depth analysis of drivers, trends, and challenges. Furthermore, the report includes historic market data from 2017 to 2021.

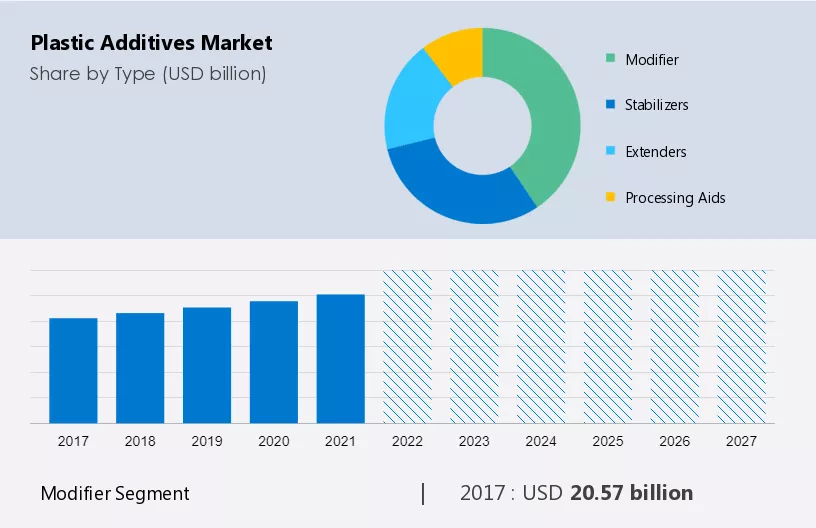

The market share growth of the modifier segment will be significant during the forecast period. Modifiers are added to plastics to change the physical properties of plastic molds or resins. They are added to improve the plasticity and viscosity of the material. For instance, impact modifiers are added to impart increased toughness and durability to plastic molds. These factors will facilitate segment growth during the forecast period.

Get a glance at the market contribution of the End User segment View Sample PDF

The modifier segment was valued at USD 20.57 billion in 2017. Modifiers through the polymerization process are incorporated as additives. Organic peroxides help in increasing polymerization activity at a faster pace, and nucleating agents are used to enhance the physical properties of the plastic, driving the market growth during the forecast period.

The consumer goods segment is expected to be the fastest-growing application segment of the market during the forecast period. The extensive use of plasticizers, flame retardants, impact modifiers, and impact modifiers and processing aids for toys, child care products, sports, and leisure products, and upholstered furniture, among other consumer goods-related applications, is a major driver of the consumer goods segment growth.

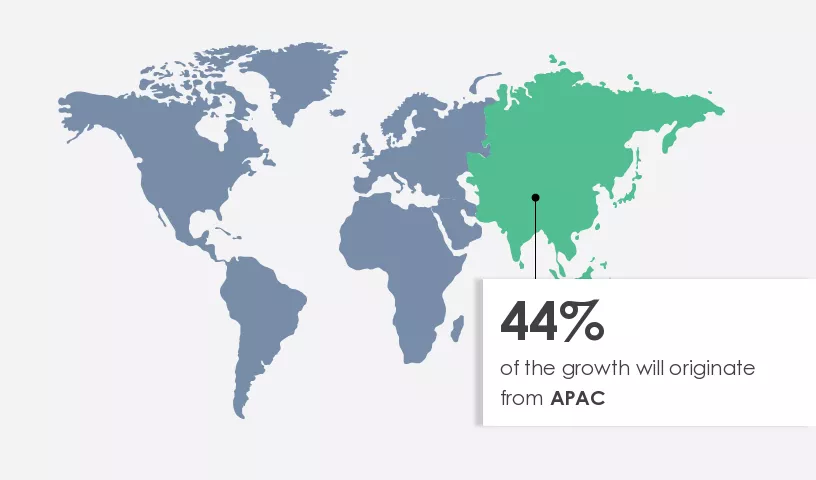

APAC is estimated to contribute 44% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions View Sample PDF now!

The market in APAC holds significant value and leads in demand, invention, and product development for plastic additives, particularly in applications like construction, automotive, and packaging. Packaging is a major application, utilizing plastic additives for antimicrobial features, mechanical properties, and barrier properties. Plastics, such as poly vinyl chloride, are used in various applications, including roofing materials, cables, and electrical components, due to their protective and thermal properties.

Further, advancements in additive types, like biodegradable additives and nano-additives, contribute to sustainable packaging solutions and reduce the environmental footprint. The automotive industry uses high-performance components with lightweight, fuel-efficient materials, enhancing safety and sales demand. Forecasts indicate continued growth, with China being a significant consumer due to its growing population and increasing consumption rate. Factual developments include the use of advanced thermoplastics in aircraft efficiency and the integration of nanoparticles and nanocomposites for improved mechanical properties in electronic devices.

In the aerospace sector, additives contribute to energy efficiency, impact strength, and thermal protection. The Construction and Automotive sectors rely on plastic additives for low-cost interiors, UV sensitivity, and resistance to discoloration and brittleness. In the Urbanization trend, plastic additives are essential for the production of PPE kits and medical-grade plastics, ensuring safety and protection. Overall, the market is a critical component in various industries, providing solutions for appearance, thermal protection, long-term durability, and regulatory compliance. Our researchers analyzed the data with 2022 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers, trends, and challenges will help companies refine their marketing strategies to gain a competitive advantage.

Increasing demand for recycled plastics is the key factor driving market growth. Due to the growing awareness of healthy living, many industries are embracing eco-friendly and sustainable solutions. This trend has resulted in a surge in demand for recycled plastics, leading to a boom in the plastic additives market worldwide. Recycled plastics are being extensively used by the packaging industry, which is gradually shifting towards their usage to meet the rising expectations of environmentally conscious consumers. In 2018, over 40% of the world's plastic production was consumed by the global packaging industry, making it the largest contributor to annual plastic waste generation.

Furthermore, Unilever Group pledged in January 2017 to make its plastic packaging 100% reusable, recyclable, and compostable by 2025. Recycled plastics are being used in various applications in the packaging industry, such as producing FDA-approved food packaging, plastic bottles, containers, jars, caps, engineered pumps, and sprayers. By utilizing recycled plastics, companies can reduce waste, energy consumption, carbon emissions, and water usage while maintaining quality and performance. Recycled plastics also enhance product protection and extend shelf life. Consequently, the increasing adoption of sustainable alternatives for various applications is expected to fuel the growth of the global recycled plastics market, leading to a significant surge in consumption during the forecast period.

The ban on phthalate plasticizers is a major restraint in the market. The specialty chemicals industry heavily relies on plastic additives as its primary source of revenue. Among the different types of plastic additives, plasticizers represent the largest segment of the market. However, due to the recent ban on the use of phthalates, which are commonly used in plasticizers, the growth of the plasticizers market has been hindered. The plastic industry has been instructed to discontinue the use of flexible PVC due to its potential negative impact on the human reproductive system. Consequently, the growing awareness of safety and environmental concerns surrounding phthalates has increased the demand for non-phthalates. Key market players are now focusing on developing non-phthalate plasticizers that meet the required standards for various applications such as food utensils, containers, packaging, and toys. These non-phthalate plasticizers include adipic acid polyester, trimellitic acid, epoxy ester, benzoic acid series, and adipic acid.

Further, during the forecast period, non-phthalate plasticizers are expected to witness the highest compound annual growth rate (CAGR). Phthalate ester plasticizers, which have traditionally dominated the flexible PVC market, are likely to face stiff competition from newer alternatives of non-phthalate plasticizers. As a result, the growth of the market in question is expected to be hampered during the forecast period.

Increasing demand for bio-based plasticizers is a major trend in the market. Plasticizers, such as phthalates, derived from petrochemicals, play a crucial role in the production of plastics, particularly PVC. Currently, phthalate-based plasticizers dominate the global plasticizer market. However, the increasing stringency of environmental regulations and growing health concerns associated with the use of plasticizers have spurred the demand for bio-plasticizers worldwide. This has resulted in a surge in demand for safe, non-phthalate, biodegradable, and bio-based plasticizers.

The growth of end-user industries in emerging economies, like India and China, is expected to fuel the growth of the bio-plasticizer market in the future. Additionally, the ban on phthalates in food packaging materials, consumer goods, medical devices, and soft toys is another factor propelling the growth of the plasticizers market. Moreover, bio-based plasticizers, such as sebacates and epoxides, are anticipated to experience the highest growth rate during the forecast period due to their notable properties, including high efficiency, non-toxicity, improved heat stability, and lower volatility. These materials are successfully utilized in a wide range of applications, such as adhesive and sealants, automotive, paints, and coatings, among others.

Companies are implementing various strategies by analyzing factors such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product or service launches to enhance their presence in the market.

BASF SE - The company offers plastic additives such as Valeras under its chemical segment.

The report also includes detailed analyses of the competitive landscape of the market and information about 16 market companies, including:

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

The report includes the adoption lifecycle of the market, from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on market penetration. Furthermore, the market forecasting report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Market Customer Landscape

The report forecasts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and growth opportunities from 2017 to 2027.

The market encompasses a significant segment of the global chemicals industry. Key players in this market include Chemic, Polymers, Government regulations, Metals, Wood, Urbanization, Consumers, Construction, and Producers. Plastics are essential in various industries due to their versatility, durability, and cost-effectiveness. They play a crucial role in enhancing the properties of plastic materials. These additives include fillers like Glass fibers, fibers, and minerals; regulators like stabilizers, lubricants, and plasticizers; and other additives like colorants, antioxidants, and fire retardants. The demand is driven by the increasing urbanization and the growing construction sector.

Moreover, the automotive industry's continuous quest for lightweight and fuel-efficient vehicles is also fueling the market's growth. The regulatory environment is a critical factor influencing the market. Governments worldwide are implementing stringent regulations to ensure the safety and environmental sustainability of plastic products. For instance, the European Union's REACH regulation sets strict guidelines for the production, use, and disposal of plastic additives. In conclusion, the market is a dynamic and evolving industry driven by various factors, including urbanization, construction, automotive, and regulatory requirements. Players in this market must stay abreast of these trends and adapt to the changing regulatory landscape to remain competitive.

Further, the market is driven by various factors, such as the demand for chemical compounds to enhance polymer properties. Additives play a crucial role in addressing challenges like aesthetic loss and ensuring the integrity of polymer properties. In industries like automotive and construction, there's a growing need for low-cost automobile interiors and UV sensitive construction materials, respectively. Additionally, the healthcare sector demands medical grade plastics for various applications. Coupled with advancements in coupling technologies, these additives contribute to the development of innovative plastic products, meeting the diverse needs of industries and consumers alike.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

177 |

|

Base year |

2022 |

|

Historic period |

2017-2021 |

|

Forecast period |

2023-2027 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.45% |

|

Market growth 2023-2027 |

USD 19.86 billion |

|

Market structure |

Fragmented |

|

YoY growth 2022-2023(%) |

6.01 |

|

Regional analysis |

APAC, North America, Europe, South America, and Middle East and Africa |

|

Performing market contribution |

APAC at 44% |

|

Key countries |

US, Saudi Arabia, China, Germany, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

ADEKA Corp., Albemarle Corp., Avient Corp., Baerlocher GmbH, Clariant AG, Covestro AG, Dow Inc., Evonik Industries AG, Exxon Mobil Corp., Grafe Advanced Polymers GmbH, Kaneka Corp., Lanxess AG, Milliken and Co., Mitsui Chemicals Inc., Nouryon Chemicals Holding BV, PMC Group Inc., Sabo Spa, Sakai Chemical Industry Co. Ltd., Songwon Industrial Co Ltd, and BASF SE |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID 19 impact and recovery analysis and future consumer dynamics, Market condition analysis for forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this report to meet your requirements. Get in touch

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Type

7 Market Segmentation by Application

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights