Enjoy complimentary customisation on priority with our Enterprise License!

The Plastics Market for the Passenger Cars Industry size is forecast to increase by USD 22.02 billion at a CAGR of 10% between 2023 and 2027. The growth of the market depends on several factors, such as the adoption of new or improved emission standards, the increasing government support to promote the adoption of EVs, and the increasing incorporation of electronics in passenger cars. China, the US, Japan, India, and Germany are the top countries contributing to the growth of the market. China held the largest market share in 2021, projecting a revenue of USD 6.12 billion. Arkema is one of the key market players and the company offers automotive plastics in the form of Arkema Polymers used for fitting, connectors, and emission control systems. Besides analyzing the current market scenario, our market research and growth report examines historic data from 2017 to 2021.

To learn more about this report, Request Free Sample

The market is experiencing significant growth driven by the increasing demand for lightweight and durable materials in automotive manufacturing. With the rising focus on fuel efficiency and emission reduction, automotive manufacturers are turning to advanced materials such as Polyether Ether Ketone (PEEK), Polyethylene Terephthalate (PET), and Polysulfone (PSU) to replace traditional materials like metals and glass. Additionally, the incorporation of renewable sources and bioplastics, derived from materials like corn starch and vegetable oil, is gaining traction in the industry, aligning with sustainability goals. As the automotive sector continues to prioritize innovation and environmental sustainability, the global plastics market offers diverse opportunities for the development and adoption of advanced materials in passenger car manufacturing.

In the applications segment of the market, diverse plastic materials like Polyphenylsulfone (PPSU), Polystyrene (PS), Polyethylene (PE), Acrylonitrile butadiene styrene (ABS), and others are used for lightweight and durable components. These plastics replace traditional materials such as glass, metals, and wood in both interior and exterior parts. High-performance plastics like Polypropylene (PP), Polybutylene terephthalate (PBT), and Polyphenylene oxide (PPO) are utilized for structural components. Additionally, sustainable plastics sourced from petroleum, natural gas, renewable sources, and bioplastics derived from corn starch, vegetable oil, and food waste support eco-friendly initiatives. This segment also focuses on recyclable products and high-performance plastic packaging solutions.

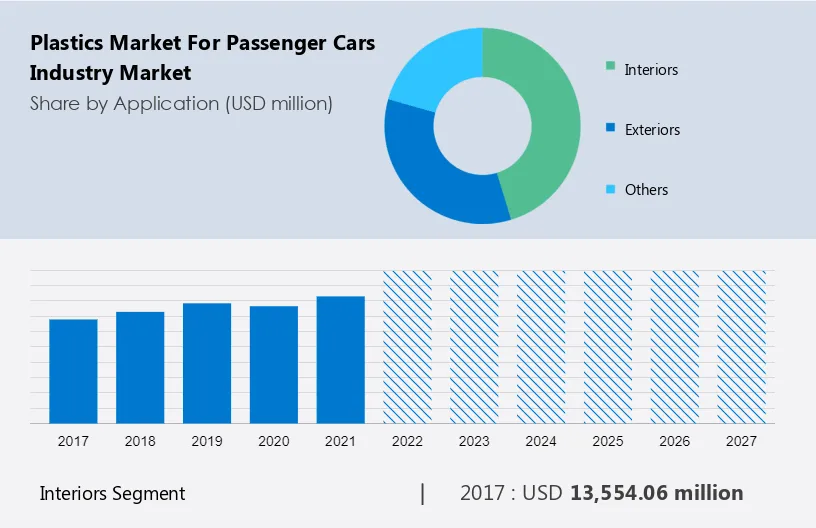

The interiors segment is estimated to witness significant growth during the forecast period. Plastics are widely used in the interior parts of passenger car segments, thus, OEMs are increasing their focus on the quality of the plastic used, such as high thermal stability, scratch resistance, high strength, and aesthetics. Additionally, UV stability, good sound absorption, good color retention, and low emissions of volatile or harmful constituents are some of the other features which are crucial when deciding on plastic material by manufacturers.

Get a glance at the market contribution of the segments, Request Free Sample

The interiors segment was the largest segment and was valued at USD 13.55 billion in 2017. Some of the key interior areas where plastics are widely used in passenger car segments include instrument panel clusters, glove boxes, door panels, overhead consoles, center and fascia consoles, lower and back seat trims, folding tables, inner safety seat parts, and speaker consoles.

As the automotive market is an extremely competitive one with several players, several manufacturers are differentiating their products by offering better value for the price that customers pay than their competitors by increasing the number of components which improves the convenience and comfort of passenger car occupants. Hence such an increase in the number of components in passenger cars will increase the demand for plastics which in turn is expected to drive the global market growth during the forecast period.

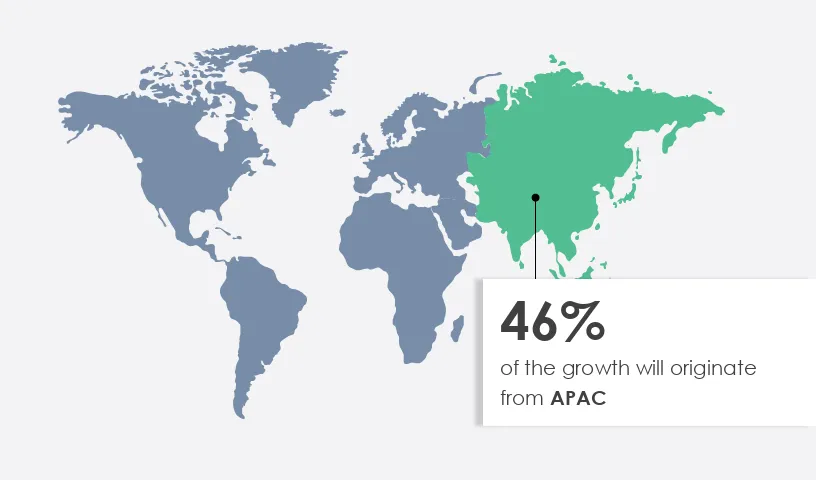

APAC is estimated to contribute 46% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

One of the main factors for the significant growth of the global market is due to the factors such as to the high demand for automobiles in countries such as China, Japan, South Korea, India, and Thailand. China is one of the prominent markets in terms of regional automotive production and sales, followed by Japan. Furthermore, there is an increasing demand for the luxury car segment in several APAC such as China, Japan, and South Korea which is expected to significantly contribute to the high demand for plastics in this region. Factors such as stringent regulatory norms on vehicular emissions and the increase in the adoption of EVs are expected to boost the demand for plastics which in turn will drive the global market growth during the forecast period.

The market is experiencing a transformative shift towards sustainable materials and innovative solutions. Wood, natural rubber, and bioplastics are gaining traction as eco-friendly alternatives to traditional plastics like Polyphenylene oxide (PPO) and Polyurethane (PU). Utilizing materials such as corn starch, vegetable oil, and food waste, manufacturers are producing recyclable products that reduce environmental impact. Additionally, sawdust is being repurposed to create high-performance plastic packaging solutions. This shift towards biodegradable and recyclable materials not only meets consumer demand for sustainability but also promotes a more environmentally-conscious approach within the automotive industry. Our researchers analyzed the data with 2022 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

One of the key factors driving the market growth is the adoption of new or improved emission standards. Due to the enforcement of stringent laws by various government institutions globally, there is an increase in the use of lightweight materials, such as plastics, for various applications in passenger cars. For instance, there is a growing implementation of Euro 6 emission standards or their equivalent in several countries such as the US, the UK, China, and India.

Hence, the implementation of such emission standards is forcing automotive component manufacturers to comply with the adoption of technologies that align with these standards. As a result, these new stringent emission standards facilitate the use of new or advanced materials that enhance fuel efficiency. Hence, such factors are expected to drive the global market growth during the forecast period.

A key factor shaping the global market growth is the lightweight and fuel efficiency of automobiles like passenger cars. Several vendors in the automotive industry are emphasizing lightweight vehicles to enhance fuel efficiency and minimize emissions. As a result, many manufacturers are adopting the use of advanced plastics and composites in passenger cars for the reduction of vehicle weight without compromising safety and performance.

Furthermore, there is a growing shift in consumer preferences towards vehicles that offer better fuel efficiency and emit fewer pollutants due to the rising awareness of climate change and the need to reduce carbon emissions. Thus, manufacturers are catering to consumer preferences by incorporating lightweight materials and technologies to improve the fuel efficiency of their vehicles. Therefore, such factors are expected to drive the global market growth during the forecast period.

Declining automotive production globally is one of the key challenges hindering global market growth. Factors that are hindering the market growth include semiconductor chip shortages, increasing input costs, rising commodity prices, and rising fuel costs, are negatively impacting the growth of automotive production globally.

Additionally, the rising popularity of ride-hailing and ride-sharing services across the world is also significantly contributing to the decline in passenger car sales, which in turn is declining automotive production. Furthermore, factors such as disruption in the supply chain and decline in demand from Russia and Ukraine with Ukraine being the leading supplier of neon gas further limited the manufacturing of automotive cars globally. Hence, such factors are expected to hinder the global market growth during the forecast period.

Companies are implementing various strategies by analyzing factors such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product or service launches, to enhance their presence in the market.

BASF SE- The company offers automotive plastic in the form of polymer for headlamps, handle doors, and interior car seats.

This market trends and analysis report also includes detailed analyses of the competitive landscape of the market and information about 15 market companies, including:

Arkema Group, BASF SE, Borealis AG, Celanese Corp., Covestro AG, Daicel Corp., Dow Chemical Co., DuPont de Nemours Inc., Evonik Industries AG, Hexion Inc., Koninklijke DSM NV, LG Chem Ltd., Nissan Motor Co. Ltd., Saudi Basic Industries Corp., SGL Carbon SE, Solvay SA, Sumitomo Corp., Teijin Ltd., Toray Industries Inc., and LyondellBasell Industries N.V.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

The market is a dynamic sector characterized by a wide range of materials and applications. Plastics such as polystyrene (PS), polyethylene (PE), and polypropylene (PP) play a vital role in manufacturing automotive parts, toys, and industrial components. These materials are also extensively used in the packaging sector due to their versatility and cost-effectiveness. Factors such as Good Manufacturing Practices (GMPs) and fluctuations in petrochemical and crude oil prices significantly impact the market. Injection molding, thermoforming, and blow molding are key manufacturing processes driving the industry forward. Additionally, plastics find applications in building & construction, contributing to their widespread use across various sectors, from automotive to aerospace, including the production of spacecraft and even everyday items like paper clips.

The market is shaped by diverse materials sourced from various origins. Key materials include plastic resins like Acrylonitrile butadiene styrene (ABS), Polybutylene terephthalate (PBT), and Polyvinyl chloride (PVC), among others. These plastics, derived from petrochemical sources such as petroleum and natural gas, are essential in manufacturing automotive components. Additionally, advancements in renewable sources are influencing the market landscape. Polycarbonate (PC), Polyamide (PA), and other plastics contribute to vehicle design, providing durability and versatility. As petrochemical prices fluctuate, the industry seeks sustainable alternatives. The interplay between traditional materials like glass and metals and innovative plastics reflects ongoing developments in the automotive sector, ensuring continual evolution and adaptation.

The market plays a pivotal role in various sectors, including healthcare, automotive, consumer goods, and more. In recent times, the demand for engineering plastics like Performance Polyethylene (PE) resins has surged due to their versatile applications, including the manufacturing of face masks, goggles, shields, gloves, and respirators. These plastics offer excellent thermal and mechanical properties, making them ideal for metal substitution in automotive components. Additionally, the industry is witnessing a shift towards circular polymers like CirculenRenew polymer, promoted by companies such as Iber Resinas, to address sustainability concerns. From the food & beverage industry to infrastructure & construction, plastics continue to drive innovation and efficiency across diverse sectors.

|

Plastics Market for Passenger Cars Industry Scope |

|

|

Report Coverage |

Details |

|

Page number |

186 |

|

Base year |

2022 |

|

Historic period |

2017-2021 |

|

Forecast period |

2023-2027 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 10% |

|

Market growth 2023-2027 |

USD 22.02 billion |

|

Market structure |

Fragmented |

|

YoY growth 2022-2023(%) |

9.3 |

|

Regional analysis |

APAC, North America, Europe, South America, and Middle East and Africa |

|

Performing market contribution |

APAC at 46% |

|

Key countries |

US, China, Japan, India, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Arkema Group, BASF SE, Borealis AG, Celanese Corp., Covestro AG, Daicel Corp., Dow Chemical Co., DuPont de Nemours Inc., Evonik Industries AG, Hexion Inc., Koninklijke DSM NV, LG Chem Ltd., Nissan Motor Co. Ltd., Saudi Basic Industries Corp., SGL Carbon SE, Solvay SA, Sumitomo Corp., Teijin Ltd., Toray Industries Inc., and LyondellBasell Industries N.V. |

|

Market dynamics |

Market growth and trends, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID 19 impact and recovery analysis and future consumer dynamics, Market condition analysis for forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this report to meet your requirements. Get in touch

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Application

7 Market Segmentation by Material

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights