Enjoy complimentary customisation on priority with our Enterprise License!

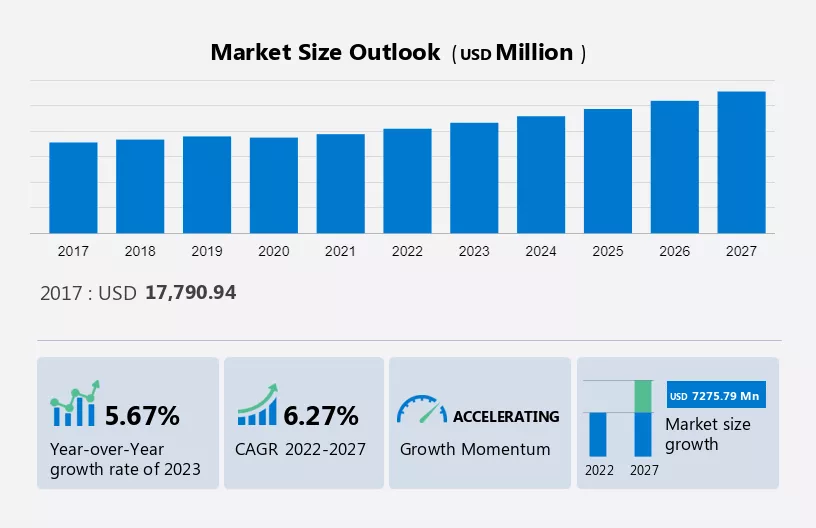

The retinal drugs market size is estimated to grow at a CAGR of 6.27% between 2022 and 2027. The retinal drugs market size is forecast to increase by USD 7,275.79 million. The growth of the market depends on several factors, including the rise in the prevalence of retinal diseases, the emergence of advanced diagnostic tools, and patient assistance programs.

This retinal drugs market report extensively covers market segmentation by distribution channel (hospital pharmacy, retail pharmacy, and online pharmacy), indication (macular degeneration, diabetic eye disease, and others), and geography (North America, Europe, Asia, and Rest of World (ROW). It also includes an in-depth analysis of drivers, trends, and challenges. Furthermore, the report includes historic market data from 2017 to 2021.

To learn more about this report, Download Report Sample

The rise in the prevalence of retinal diseases is notably driving the market growth, although factors such as limitations and risk factors associated with current retinal disease treatment drugs may impede the market growth. Our researchers analyzed the data with 2022 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The rise in the prevalence of retinal diseases is notably driving the market growth. The prevalence of retinal diseases such as wet AMD, diabetic retinopathy, DME, RVO, and mCNV is significantly increasing in developed and developing countries. AMD is the leading cause of visual disability in industrialized countries and the third leading cause of visual disability worldwide. It is expected that 202,200 million will suffer from AMD globally. Nearly nine out of every ten cases of AMD-related severe vision loss results from wet AMD. Every year, about 500,000 individuals are newly diagnosed with wet AMD globally.

The increasing prevalence of retinal diseases is associated with the rise in risk factors. RVO typically affects people over the age of 50 years, and the incidence increases with age. The risk of getting advanced AMD increases from 2% for people in the age group of 50-59 to nearly 30% for those over the age of 75. Globally, the older population is also growing rapidly owing to the rise in average life expectancy. By 2025, it is expected that approximately 810 million people will be aged 65 and above across the world. The increasing worldwide incidence of diabetes is also leading to an increase in the incidence of diabetic retinopathy, DME, and other complications. Therefore, these factors will increase the demand for retinal drugs, thereby, driving the market growth during the forecast period.

The rise in demand for sustained-release ocular formulations is an emerging trend in the market. Although anti-VEGF treatments are effective in many patients, the route of administration and duration of treatment remain limitations to therapy. Sustained-release ocular formulations can address the limitations of many of the current delivery modalities by reducing dosing frequency, eliminating the need for patient-administered drugs, and bypassing the physical barriers of the ocular tissues. The ozurdex implant is an approved biological intravitreal sustained DDS, which can release dexamethasone over the course of several months, leading to a marked improvement in visual acuity.

The demand for new sustained-release ocular DDS is steadily increasing due to the growing prevalence of major eye diseases, increasing R&D to find new approaches to deliver therapeutics, including small and large molecules, and the increasing need to reduce the frequency burden of repeat intravitreal injections. Several vendors are also increasingly focusing on the development of sustained-release formulations for the treatment of various retinal diseases. Thus, the rise in demand for sustained-release ocular formulations is expected to drive the growth of the global market during the forecast period.

The limitations and risk factors associated with current retinal disease treatment drugs are major challenges impeding market growth. Anti-VEGF drugs have been very successful in improving the visual outcomes of people with retinal disorders. However, they do not cure the underlying problem of these disorders. Despite being the most effective treatment for many retinal diseases, the visual improvement gained using anti-VEGF drugs is modest, averaging about two lines of vision and only a few regain their normal vision. The repeated and long-term use of anti-VEGF drugs is also associated with some systemic adverse events and devastating ocular complications, including serious infections, retinal detachment, cataracts, and glaucoma. There is also a potential risk of blood clots leading to a heart attack or a stroke. In addition, VEGF is an essential factor for cell survival, and the sustained blocking of VEGF can lead to undesirable adverse effects such as chorioretinal atrophy and cardiovascular complications.

Similarly, Avastin, which is widely prescribed to patients with retinal disorders, is also associated with several limitations and drawbacks. The lack of regulatory oversight has led to the widespread circulation of foreign counterfeit bevacizumab in several US medical practices. Also, systemic bevacizumab must be converted into ophthalmic form through a compounding process performed by local pharmacies. Any contamination introduced during the compounding of bevacizumab for ophthalmic use increases the risk of post-injection endophthalmitis. Bevacizumab from compounding pharmacies may contain drug concentrations lower than those used in clinical trials supporting bevacizumab efficacy. Such concerns may deter physicians from prescribing Avastin despite its clinical and financial advantages. Hence, such limitations will hinder the global market growth during the forecast period.

Key Retinal Drugs Market Customer Landscape

The report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Global Retinal Drugs Market Customer Landscape

Vendors are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

AbbVie Inc. - The company conducts research and development, manufacturing, commercialization, and sale of innovative medicines and therapies to allocate resources and assess business performance on a global basis in order to achieve established long-term strategic goals. The key offerings of the company include retinal drugs.

The retinal drugs market report also includes detailed analyses of the competitive landscape of the market and information about 15 market vendors, including:

Qualitative and quantitative analysis of vendors has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize vendors as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize vendors as dominant, leading, strong, tentative, and weak.

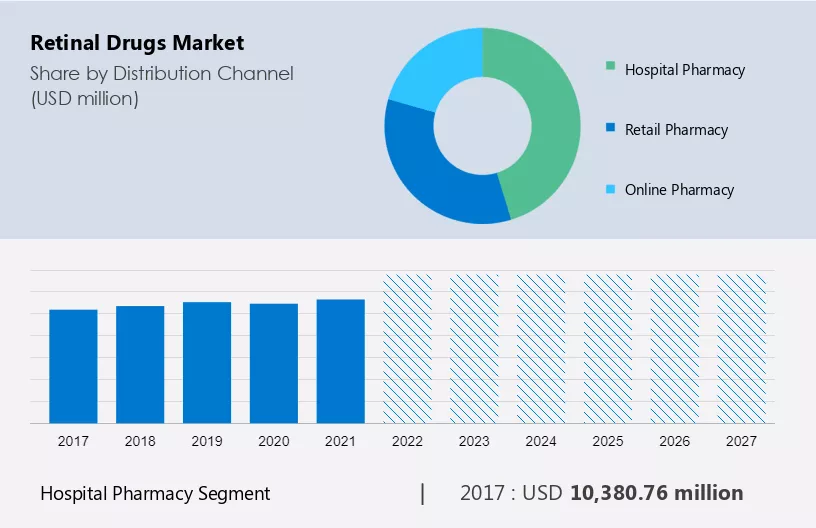

The market share growth by the hospital pharmacy segment will be significant during the forecast period. Hospital pharmacies comprise places selling drugs and other pharmaceutical-related products by hospitals from different pharmaceutical companies and are used for the treatment of either outpatients or inpatients.

Get a glance at the market contribution of various segments View a PDF Sample

The hospital pharmacy segment was valued at USD 10,380.76 million in 2017 and continued to grow until 2021. The drugs that are found in hospital pharmacies include therapeutic and critical care drugs. These drugs have applications in retinal diseases. The primary aim of hospital pharmacies is to procure, store, and sell medications to patients in hospitals. Hospital pharmaceuticals are administered to individuals during the hospital-enabled treatment period. They have rapidly emerged as the preferred distribution channel for compounded drugs. The reach and influence of hospitals will continue to increase as they purchase or take controlling stakes in physician practices. More hospitals are consolidating into larger healthcare systems, which can include payors, speciality services, outpatient clinics, long-term care facilities, and physician practices. Thus, owing to such factors the segment is expected to grow during the forecast period.

For more insights on the market share of various regions Request PDF Sample now!

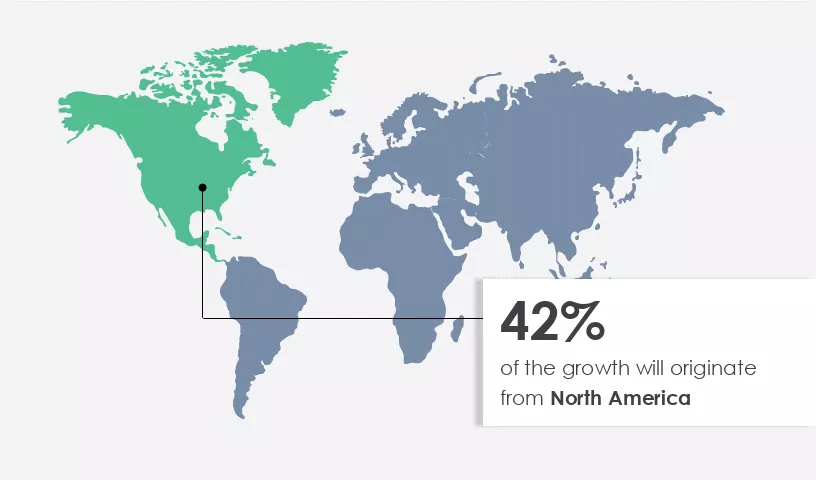

North America is estimated to contribute 42% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

North America accounts for the majority of the market share in the global market. The US is the major revenue generator in North America, followed by Canada. This is due to the high prevalence of retinal disorders and the high awareness among people about retinal disorders. Furthermore, Medicare provides coverage for all three anti-VEGF drugs, LUCENTIS, EYLEA, and Avastin, that are majorly prescribed for retinal disorders. The market in the US is expected to grow steadily due to the rising geriatric population and the related risk factors for retinal disorders. Furthermore, every year, approximately 1.5 million people in the region are diagnosed with diabetes. This is leading to an increase in the incidence of diabetic retinopathy, DME, and other complications. Thus, there is an increase in demand for retinal drugs, which, in turn, will drive market growth in the region during the forecast period.

The outbreak of COVID-19 negatively affected the market. However, following the widespread COVID-19 vaccination drives, lockdown restrictions in various countries were somewhat relaxed in 2021, which led to the resumption of business activities and manufacturing units of retinal drugs. Thus, such factors are expected to boost the growth of the market in North America during the forecast period.

The retinal drugs market report forecasts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and growth opportunities from 2017 to 2027.

|

Retinal Drugs Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

167 |

|

Base year |

2022 |

|

Historic period |

2017-2021 |

|

Forecast period |

2023-2027 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.27% |

|

Market growth 2023-2027 |

USD 7,275.79 million |

|

Market structure |

Fragmented |

|

YoY growth 2022-2023(%) |

5.67 |

|

Regional analysis |

North America, Europe, Asia, and Rest of World (ROW) |

|

Performing market contribution |

North America at 42% |

|

Key countries |

US, Canada, Germany, Spain, and China |

|

Competitive landscape |

Leading Vendors, Market Positioning of Vendors, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Bayer AG, AbbVie Inc., Alcon Inc., Alimera Sciences Inc., Bausch Health Co Inc., Bristol Myers Squibb Co., F. Hoffmann La Roche Ltd., Kubota Corp., MeiraGTx Holdings Plc, Novartis AG, Ocular Therapeutix Inc., Oxurion NV, Pfizer Inc., Regeneron Pharmaceuticals Inc., REGENXBIO Inc, Sanofi SA, Santen Pharmaceutical Co. Ltd., Teva Pharmaceutical Industries Ltd., Visufarma, and Johnson and Johnson Services Inc. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, and Market condition analysis for the forecast period. |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Distribution Channel

7 Market Segmentation by Indication

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights