Enjoy complimentary customisation on priority with our Enterprise License!

The orthopedic surgical robots market size is forecast to increase by USD 808.5 million, at a CAGR of 20.11% between 2022 and 2027. Market growth hinges on several factors: the rise of robotic surgical platforms due to limitations in traditional surgeries, evolving regulatory landscapes, and ongoing technological advancements. These elements collectively drive innovation and adoption within the medical field. The shift towards robotic solutions stems from the need for enhanced precision, reduced invasiveness, and improved patient outcomes, addressing shortcomings in conventional surgical methods. Furthermore, regulatory changes play a pivotal role in shaping market dynamics, influencing the development and deployment of advanced medical technologies. With continuous technological progress, including AI integration and surgical automation, the market is poised for further expansion and transformative changes in healthcare practices.

To learn more about this report, View Report Sample

This market report extensively covers market segmentation by application (knee surgery and hip surgery), end-user (hospitals and ambulatory service centers), and geography (North America, Europe, Asia, and Rest of World (ROW)). It also includes an in-depth analysis of drivers, trends, and challenges. Furthermore, the report includes historic market data from 2017 to 2021.

The market is driven by the rising demand for precise and minimally invasive procedures in treating musculoskeletal disorders like osteoarthritis and spinal deformities. Technological advances in surgical robots, including the integration of Robotic Arm technology, are revolutionizing orthopedic surgery. However, challenges such as high initial investment costs, regulatory complexities surrounding manufacturing and new developments, and the need for specialized training for surgical robots pose significant hurdles. Despite these challenges, the market is expected to witness continuous growth fueled by musculoskeletal research and the increasing adoption of Molecular diagnostics in orthopedics. Our researchers analyzed the data with 2022 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Technological developments are the key factor driving the growth of the global market. A major factor that is expected to impact the growth of the market in focus is the miniaturization of sensors, which has happened over the years and is expected in the forecast period as well. This miniaturization has reduced the cost of sensors and, in turn, that of robots. There have been innovations in mechatronic components as well, which is in tandem with the increased prevalence of information and communications technology (ICT). The software that enhances the capabilities of robotic systems has also become more affordable for companies.

Moreover, as the price of sensors continues to fall, it is expected to lead to the development of more robots that can be used for orthopedic surgeries. Orthopedic surgical robots use highly advanced and complex sensors. The development and growth of these products are closely dependent on technological advancements and growth in sensor and imaging technologies, among other components. Therefore, the growth in the sensor market and the availability of highly advanced application-specific sensors may fuel more R&D activities in the market. This is expected to improve the growth of the market in focus during the forecast period.

An increase in minimally invasive surgical (MIS) procedures in orthopedics is the primary trend in the global orthopedic surgical robot market growth. Minimal-invasive surgeries are becoming a preferred procedure in the field of orthopedics. This technique is proving to be advantageous for the reconstruction of fractured bones, joint replacement, and realignment of bone extremities. As they result in less postoperative swelling than open techniques and reduce the risk of complications, pain, and recovery times, there is an increase in preference for such surgeries. Arthroscopy is among the most common MIS procedures.

Moreover, as the market gains traction, minimally invasive spinal surgeries for stabilizing spinal joints and vertebral discs are expected to gain traction during the forecast period. Companies in the market are expected to capitalize on the preference for MIS procedures by investing in R&D and offering products such as orthopedic surgical robots, which are expected to contribute to the growth of the burgeoning market.

The presence of alternative treatment methods poses a challenge to the global market. Some of the alternative therapies include high-intensity focused ultrasound (HIFU), laparoscopy, cryotherapy, and open surgeries. The complexities involved in the use of robotic surgical systems, coupled with the lack of skilled surgeons, are forcing the existing healthcare fraternity to shift toward other popular alternative therapies to treat a wide variety of disorders and diseases. There are also economic benefits linked to laparoscopic surgeries that act as an alternative, such as shorter hospital stay lowers overall medical costs.

Moreover, this therapy is less invasive than open surgery and, therefore, results in minimal blood loss, shorter recovery periods, shorter hospital stays, and less pain. Further, in developing regions such as Africa, open surgeries are preferred over robotic surgeries due to the lack of adequate healthcare infrastructure, budget constraints, and expertise in performing robotic surgeries. Such advantages fuel the demand for alternative therapies and are expected to hamper the growth of the market in focus during the forecast period.

The market report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Market Customer Landscape

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Asensus Surgical US Inc.: The company offers orthopedic surgical robots, namely the Senhance Surgical System. Also, they focus on augmented intelligence, connectivity, and robotics solutions in laparoscopy, addressing the current clinical, cognitive, and economic shortcomings.

The research report also includes detailed analyses of the competitive landscape of the market and information about 15 market companies, including:

Qualitative and quantitative market research and growth analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. In market growth analysis, data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

The market has seen a substantial surge in demand due to various factors related to the musculoskeletal system. One significant driver is the increasing prevalence of conditions such as bone infections, joint fractures, and spinal deformities, necessitating advanced treatments like knee and hip replacement surgeries and anterior cruciate ligament reconstruction. Surgical robots equipped with Robotic Arm technology are at the forefront of orthopedic surgery, offering precision in procedures like acetabulum positioning and extremity orthopedics. These technological advances have revolutionized the field, enabling molecular diagnostics and new developments in addressing musculoskeletal disorders like osteoarthritis. Companies like Monogram Orthopedics and Engage Surgical are leading innovators, contributing to the market growth of orthopedic surgical robots such as the Triathlon Hinge system. The adoption of robotic-assisted arthroscopy and the manufacturing of advanced surgical robots signifies the industry's continuous evolution to provide efficient and effective solutions for musculoskeletal traumas and bone deformities.

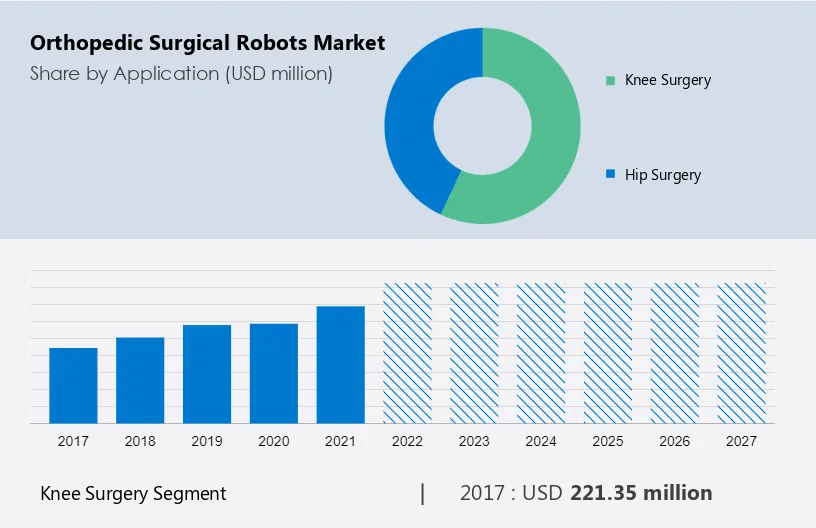

The market share growth by the knee surgery segment will be significant during the forecast period. Partial knee replacement is a treatment option for adults suffering from mid-stage osteoarthritis in the inner, top, or outer compartments of the knee. Robotic surgery ensures that precision is consistently reproduced while performing partial knee resurfacing.

Get a glance at the market contribution of various segments View the PDF Sample

The knee surgery segment was valued at USD 221.35 million in 2017 and continued to grow until 2021. The knee orthopedic surgical robots offer the advantage of more precise surgeries as they restrict any unnecessary motion of the knee by tracking motion through fiducial markers and infrared camera systems, which immediately stop the robot in case of any unnecessary motion. Such advances are expected to drive the future growth of this segment during the forecast period. The growth of the knee segment is expected to contribute to the growth of the global market during the forecast period.

For more insights on the market share of various regions Download PDF Sample now!

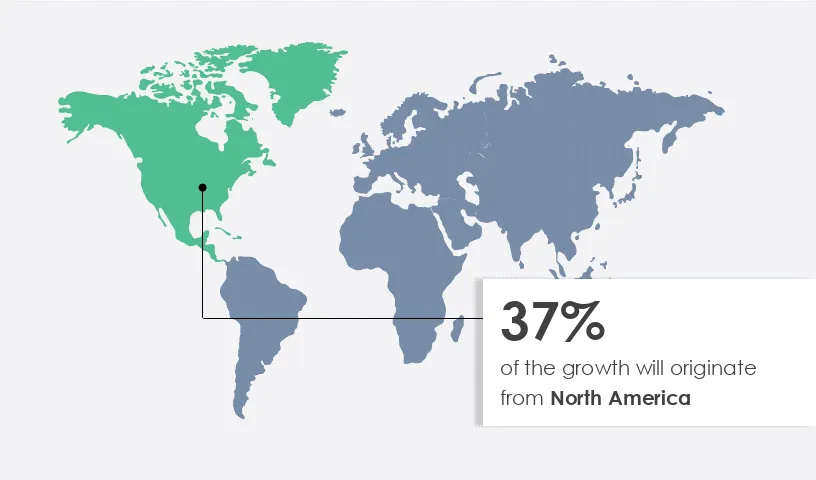

North America is estimated to contribute 37% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period. The orthopedic market in North America is growing at a significant rate owing to the high adoption of orthopedic surgical robots and an increase in the number of surgical procedures. Also, the growing volume of spinal non-fusion procedures, fast and easier acceptance of technologically updated spinal implants, and growing investments by companies in clinical trials are driving market growth in this region. Further, the rise in sports-related injuries has contributed largely toward the growth of the joint reconstruction product segment, which acquired more than one-fourth of the global market share. For instance, it is estimated that 1.35 million youths suffer from sports injuries each year in North America, of which about 451,000 injuries are sprains or strains. Nearly 400,000 injuries are concussions and fractures.

In certain cases, knee replacement or knee arthroplasty is recommended by physicians to resurface a knee damaged by arthritis. The rising prevalence is driving the demand for knee replacement, which is increasing the demand for robots for increased precision and accuracy. This, in turn, is expected to increase the demand for the market in North America.

The market research report provides comprehensive data (region wise segment analysis), with forecasts and estimates in "USD Million" for the period 2023 to 2027, as well as historical data from 2017 to 2021 for the following segments

The market is driven by a multitude of factors, notably the aging population leading to an increased demand for joint replacements like knee and hip surgeries. Technological advances, including robot-assisted orthopedic surgery with systems like Mako Orthopedic Robot and Engage Surgical, enhance precision and safety in procedures such as femoral osteotomies and acetabulum positioning. These robots cater to complex cases like ligament ruptures and musculoskeletal traumas, benefiting from molecular diagnostics and digitization. Regulatory standards and approval processes ensure quality and safety in manufacturing medtech devices, further influencing strategic decisions and healthcare expenditure. Orthopedic surgeons and providers increasingly rely on robotic equipment for efficient and effective treatments, inpatient facilities addressing bone fractures, joint fractures, and orthopedic disorders with skillful expertise and supportive care.

Moreover, the market is witnessing significant growth due to various factors, particularly the aging population worldwide. As people age, they are more prone to bone deformities, knee disorders like osteoarthritis, and injuries requiring knee replacements or anterior cruciate ligament reconstruction surgeries. The rise in awareness about musculoskeletal disorders and advancements in diagnostic technology has further fueled the demand for orthopedic surgical robots. These robots, such as the CORI knee replacement system and robotic arms, are designed to enhance precision and efficiency in femur preparation, addressing hip fractures and other musculoskeletal issues in the geriatric population.

Furthermore, healthcare facilities, including inpatient and outpatient centers, are increasingly adopting robot-assisted orthopedic surgery for procedures like meniscus tear repairs and spinal deformities corrections. Orthopedic surgeons and medical professionals benefit from residency training programs and skilled expertise to effectively utilize these robotic systems, minimizing skill gaps and ensuring, self efficacy, supportive care needs, and patient safety. Regulatory standards play a crucial role in the approval and regulation of medical devices, including orthopedic surgical robots like the Triathlon Hinge system. As the field continues to witness new developments and innovative solutions from companies like Monogram Orthopedics, the market is poised for further expansion to meet the growing needs of patients with musculoskeletal disorders and complex orthopedic conditions.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

158 |

|

Base year |

2022 |

|

Historic period |

2017-2021 |

|

Forecast period |

2023-2027 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 20.11% |

|

Market growth 2023-2027 |

USD 808.5 million |

|

Market structure |

Fragmented |

|

YoY growth 2022-2023(%) |

19.0 |

|

Regional analysis |

North America, Europe, Asia, and Rest of World (ROW) |

|

Performing market contribution |

North America at 37% |

|

Key countries |

US, UK, Germany, China, and Japan |

|

Competitive landscape |

Leading companies, Market Positioning of companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Asensus Surgical US Inc., Brainlab AG, Corin Group PLC, Curexo Inc., Galen Robotics Inc., GANYMED ROBOTICS SAS, Intuitive Surgical Inc., Johnson and Johnson Services Inc., KUKA AG, Medtronic Plc, Nuvasive Inc., OrthAlign Corp., Renishaw Plc, Shanghai MicroPort MedBot Group Co. Ltd., Siemens AG, Smith and Nephew plc, Stryker Corp., THINK Surgical Inc., Zimmer Biomet Holdings Inc., and Globus Medical Inc. |

|

Market dynamics |

Parent market analysis, Market forecasting, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for forecast period. |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this market research report to meet your requirements.

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Application

7 Market Segmentation by End-user

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights

- US,UK,Germany,China,Japan - Size and Forecast 2023-2027")