Enjoy complimentary customisation on priority with our Enterprise License!

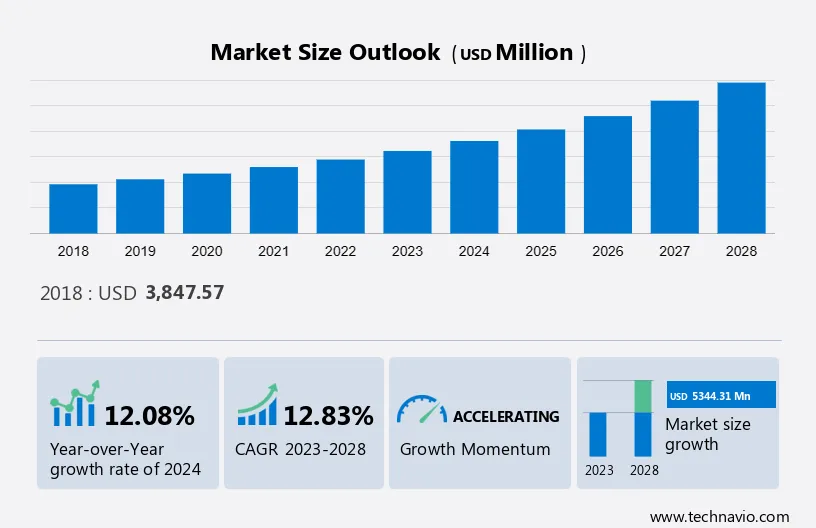

The vendor management software market size is estimated to grow at a CAGR of 12.83% between 2023 and 2028. The market size is forecast to increase by USD 5.34 billion. The growth of the market depends on several factors including increased adoption of cloud-based vendor management software, adoption of customer-centric pricing strategies and the need to comply with regulatory requirements. Vendor management software is a software application that helps organizations manage their supplier relationships and expedite the procurement process. It makes contract management, order processing, performance tracking, and vendor selection easier. Organizations may improve sourcing and procurement efficiency, reduce costs, assure compliance, and optimize their supply chains with the use of vendor management software. Organizations that are interested in efficiently handling their vendor ecosystem, increasing efficiency, reducing risks, and getting the most out of their supplier relationships must have this software.

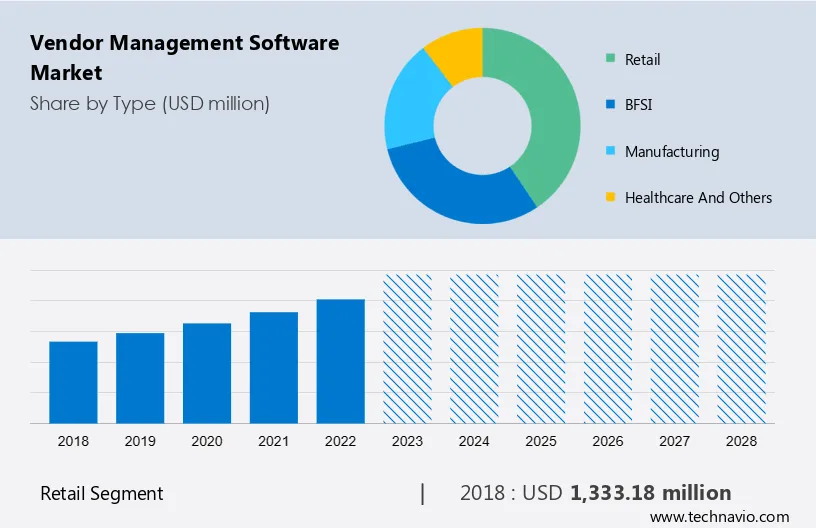

The research report on the vendor management software market offers industry forecasts and segmentation based on type including retail, BFSI, manufacturing, and healthcare and others. It also segments the market by deployment, which comprises on-premises and cloud-based. Geographically, the report covers North America, Europe, APAC, South America, and the Middle East and Africa. The market size, historical data (2018-2022), and future forecasts are presented in terms of value USD 1.33 billion for all these mentioned segments.

For More Highlights About this Report, Download Free Sample in a Minute

The adoption of customer-centric pricing strategies is notably driving market growth. To thrive in a competitive market environment, software vendors are adopting customer-centric pricing strategies enabled by advances in technology. A growing number of vendor management software providers are providing value-based pricing models focusing more on customer needs. The price of the software is based on the software vendor's ability to provide differentiating features of the software solution. The customers focus on certain economic and market factors before implementing the vendor management software. The market factors that the customers consider are constrained IT budgets, the ability to opt for free models, and ROI.

In addition, the high prices and limited IT budgets have driven the vendors to re-evaluate the software pricing and delivery models. Thus, vendors are providing SaaS, term licensing, and commercial open-source models to be in sync with the changing demands. Varying pricing structures of the vendor management software will increase its adoption among end-users, which, in turn, will propel the growth of the vendor management software market during the forecast period.

The rise in demand for integrated vendor management solutions is an emerging trend shaping the market growth. End-users prefer vendors that provide integrated and converged software suites, as opting for different software may lead to integration issues. Integrated products and software suites from the same vendor have better integration ability and support other functions. As the increased complexity of network infrastructure has made integration an important buying criterion, solutions with better integration are finding higher adoption. Witnessing this demand, all the major vendors are providing software suites with features such as accounting, ERP, CRM, procurement, financial systems, and supply chains.

Furthermore, there is likely to be a steep rise in the number of players focusing on offering SaaS-based vendor management software that is compatible with other applications, including marketing technologies. Therefore, such factors are expected to drive market growth during the forecast period.

High implementation and maintenance costs of on-premises vendor management software a significant challenges hindering the market growth. The high cost of deploying on-premises vendor management software is one of the major challenges in the market for SMEs. The price of the vendor management software includes the system design and customization cost, implementation cost, training, and maintenance cost. The implementation of the software in an organization requires IT staff with the relevant skills. The implementation of the vendor management software requires planning, adequate funding, self-assessment, cooperation, and a clear vision at all managerial levels. Enterprises also need to train their employees to use the software applications efficiently.

However, after being implemented, the software needs to be upgraded at regular intervals to keep up with the market trends. Thus, these factors lead to an increased cost of implementation of the vendor management software, which adversely affects its adoption among the end-users. This, in turn, will impede the growth of the vendor management software market during the forecast period.

The market share growth by the retail segment will be significant during the forecast period. The intense competition and shrinking profit margins demand retailers to streamline and enrich the exchange of information with vendors and suppliers. This is the only way to reduce the cost of goods sold and effectively manage just-in-time inventories. Vendor management software is gaining prominence in the retail sector as it helps retailers gain transparency across departments and establish a standard process to support cost-saving efforts, mitigate risks, and create service excellence across purchasing.

Get a glance at the market contribution of various segments Download the PDF Sample

The retail segment was the largest and was valued at USD 1.33 billion in 2018. vendor management software in the retail sector helps to focus on the tasks related to the processing of orders, enabling retailers to place sought-after merchandise on the shelves more quickly. In addition, it also allows retailers to reduce the tremendous effort spent in managing vendor relationships, eliminating paperwork, and the tedious routing of documents through approval and administrative cycles. Owing to such factors, the adoption of vendor management software is expected to increase from the retail end-user segment, which, in turn, will propel the growth of the global vendor management software market during the forecast period.

The on-premises vendor management software is installed and runs on the organization's premises. It is more expensive than cloud-based vendor management software because it requires in-house hardware and huge capital investment in the form of a software license. However, the on-premises vendor management software is secure as there is no third-party interference. IT specialists maintain it in the organization. The biggest advantage of the on-premises vendor management software is that businesses have complete control over their critical data. Some heavily regulated industries do not prefer to store their sensitive information in a public cloud environment. Since most cloud-based vendor management solutions operate in a public cloud environment, businesses with these constraints decide to opt for on-premises installations. Due to such factors, the on-premises deployment of vendor management software is expected to increase, which in turn will drive the growth of the global vendor management software market during the forecast period.

For more insights on the market share of various regions Download PDF Sample now!

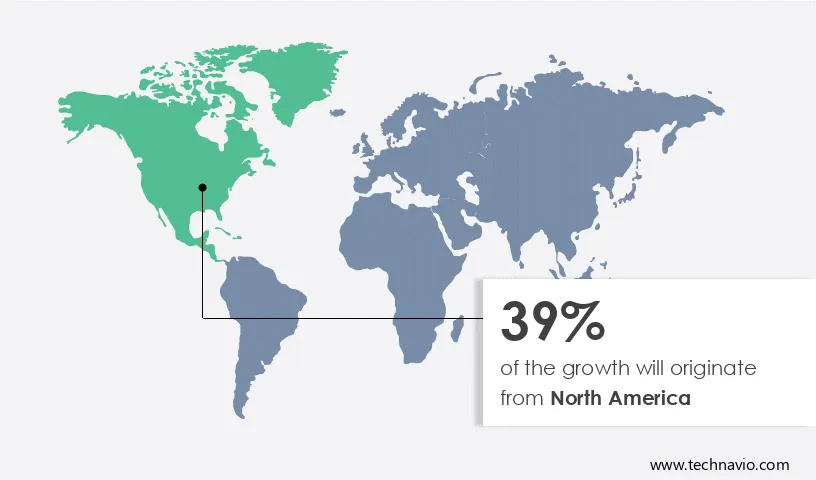

North America is estimated to contribute 39% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period. The dominance of North America is mainly due to the availability of adequate IT infrastructure and the wide geographical presence of employees due to increasing globalization. Organizations across several industry verticals in the Americas are improving their business processes to enhance customer satisfaction and gain a competitive advantage in the global market. However, the vendor management software market in North America has reached maturity. The competition among different vendor management software providers is increasing. Thus, the vendors are upgrading their offerings to hold onto their market share. The adoption of vendor management software is the highest in the US and Canada because of the growth of e-commerce and the shift toward omnichannel retail.

In addition, the markets in these countries are flourishing because the vendors are integrating specialized features in their products. In addition, due to the introduction of regulatory frameworks such as Basel III in the financial sector and HIPAA in the healthcare sector, enterprises operating in the region are seeking better solutions to achieve better compliance adherence. The increased implementation of cloud-based vendor management software in SMEs and large enterprises has further contributed to the market growth during the forecast period.

The COVID-19 pandemic-induced lockdowns had a devastating effect on the regional economy, as well as SMEs, in 2020. However, in 2021, with the lifting of lockdowns and the adoption of effective vaccination measures, the companies in the manufacturing industry tried to revive their businesses. Further, owing to the increasing need for data-driven supplier insights, supply chain resilience, procurement process automation, and regulatory compliance, the market for vendor management software in North America is projected to grow during the forecast period.

The Vendor Management Software Market report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Global Vendor Management Software Market Customer Landscape

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

360factors Inc. - The company offers vendor management software namely Predict360 that enables financial organizations to track, manage and report vendor risks associated with third parties under one platform.

Corcentric Inc. - The company offers vendor management software that retrieves, organizes, and manages supplier information while maximizing engagement and data quality across your global supplier base.

Coupa Software Inc. - The company offers vendor management software that mitigates third-party risk, accelerates supplier onboarding, and continuously monitors partner health with AI-powered insights.

The research report also includes detailed analyses of the competitive landscape of the market and information about 20 market companies, including:

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

The vendor management software market report forecasts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and growth opportunities from 2018 - 2022.

|

Vendor Management Software Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

171 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 12.83% |

|

Market Growth 2024-2028 |

USD 5.34 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

12.08 |

|

Regional analysis |

North America, APAC, Europe, South America, and Middle East and Africa |

|

Performing market contribution |

North America at 39% |

|

Key countries |

US, Canada, China, Germany, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

360factors Inc., Corcentric Inc., Coupa Software Inc., Deskera USA Inc., eSellerHub, Gatekeeper, HICX Solutions Ltd., Intelex Technologies ULC, International Business Machines Corp., Ivalua Inc., LogicGate Inc., LogicManager Inc., MasterControl Solutions Inc., MetricStream Inc., Proactis Holdings plc, Quantivate LLC, SalesWarp, SAP SE, Zoho Corp. Pvt. Ltd., and Zycus Inc. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for the forecast period. |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this market research report to meet your requirements.

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Type

7 Market Segmentation by Deployment

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights