Enjoy complimentary customisation on priority with our Enterprise License!

The global health and wellness food market is estimated to increase by USD 452.93 million, growing at a CAGR of 8.5% between 2022 and 2027.

This market has seen significant growth in recent years as more people prioritize their health and well-being.|It includes various sectors, such as organic foods, foods and dietary supplements, plant-based alternatives, and natural remedies. Additionally, increasing adoption of healthy eating habits and preference for organic and natural food products, healthy grocery, and plant-based dairy alternatives, along with rising awareness of food sensitivities, has propelled the health food market growth. Globally, healthy eating market shows a trend toward healthier lifestyles, favoring unprocessed, wholegrain foods and balanced nutrition and health. Recognizing the impact on emotional, physical, and cognitive well-being, people prioritize a balanced diet and regular exercise. This awareness extends to preventing chronic diseases like coronary heart disease and obesity. As a result, the market anticipates growth, with consumers actively seeking products supporting their overall wellness.

In today's fast-paced world, prioritizing health and wellness has become increasingly vital. The healthy food in market plays a pivotal role in promoting overall well-being by offering a wide array of nutritious options. From clean label food products to protein-based snacks, consumers are presented with choices that align with their desire for a balanced diet and healthy lifestyle. One of the key considerations in the industry is the nutritional value of packaged food products. Consumers are increasingly focused on calorie content and fat content, seeking options that support weight management and digestive health. These products often boast functional benefits, providing immune support and addressing nutritional deficiencies. Cleanliness and traceability are paramount, driving the popularity of functional snacks, frozen dinners, and portable beverage options. From farmers markets to grocery stores, the market for healthy foods is expanding rapidly, catering to individuals seeking to maintain a healthy diet and prevent illness through nature-inspired and nutrient-rich offerings.

In today's fast-paced world, more and more people are turning to a healthy lifestyle rooted in nutrition, exercise, and wellness. This shift towards wellness encompasses a variety of practices, including maintaining a balanced diet rich in organic and natural foods, as well as incorporating supplements to ensure adequate intake of essential vitamins and minerals. Many individuals are also embracing plant-based diets with plant-based substitutes, such as vegan and vegetarian lifestyles, which not only promote better digestion and immune function but also support weight management and overall health. The focus on holistic health extends beyond just food choices, with an emphasis on exercise and fitness to boost energy levels and enhance physical well-being. Additionally, the consumption of superfoods, packed with antioxidants and probiotics, has become increasingly popular due to their potential to support immune function and promote digestive health.

Our researchers analyzed the data with 2022 as the base year, along with the key trends, and challenges. A holistic analysis of drivers, trends, and challenges will help stakeholders in the value chain refine their marketing strategies to gain a competitive advantage.

The global market is set to thrive due to the increasing adoption of prebiotic and probiotic foods. Prebiotics are indigestible substances found in food that ferment in the large colon, nourishing the probiotic bacteria in the gut microbiome and promoting a healthy digestive system. Regular consumption of prebiotics offers numerous benefits, including reduced risk of cardiovascular diseases, increased levels of healthy cholesterol, improved gut health, digestion, and immune function, lower stress response, decreased risk of obesity and weight gain, reduced inflammation and autoimmune reactions, and hormonal balance.

Leading companies like Nestle provide prebiotic food options such as Quakers oats, which reduce gastric activity and promote the growth of intestinal bacteria. On the other hand, probiotics are live beneficial bacteria naturally present in fermented foods like yogurt. As consumers gradually embrace prebiotic and probiotic foods, companies like Danone and Nestle are likely to expand their offerings in the probiotic product market, driving further healthy food market growth in the industry.

The global market faces a significant obstacle in the form of high costs. Organic food products, in particular, are approximately 60% more expensive than conventionally produced alternatives due to the increased labor required for organic crop cultivation. Organic food grains, for example, tend to be pricier compared to items like soft drinks and biscuits that utilize less expensive ingredients such as margarine, sugar, and edible oil. Organic farmers prioritize crop rotation and avoid chemical weed control to maintain soil health and prevent weed growth.

In the United States, organic food producers must obtain USDA organic certification to ensure compliance with specified organic standards for farming operations and production methods. The certification fees vary based on the scale of operations, further adding to producers' costs. To maintain profitability, producers pass on these production expenses to consumers, resulting in higher prices for products. The elevated price point poses a challenge by limiting consumer demand and impeding market growth.

The market research report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Global Market Customer Landscape

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The global market report also includes detailed analyses of the competitive landscape of the market and information about 15 market companies, including:

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

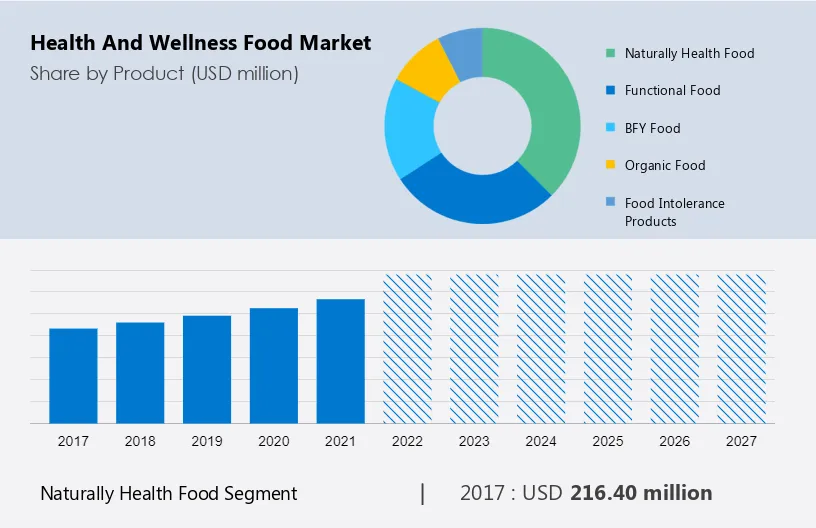

This market report extensively covers market segmentation by Product (naturally health food, functional food, bfy food, organic food, and food intolerance products), Distribution Channel (offline and online), and Geography (North America, APAC, Europe, Middle East and Africa, and South America). It also includes an in-depth analysis of drivers, trends, and challenges. The industry emphasizes the importance of exercise and physical activity in maintaining wellness. Regular exercise not only contributes to physical health but also enhances mental performance, reducing stress and tension. By incorporating protein-based foods and nutritious formulations into their diets, individuals can support their overall health and well-being, paving the way for preventive healthcare practices and disease prevention. In essence, the health and wellness food industry plays a crucial role in promoting wellness and vitality, offering consumers the tools they need to prioritize nutrition, exercise, and holistic well-being in their daily lives.

This is readily available in various retail outlets, including department health food stores, specialty stores, supermarkets, convenience stores, and drug stores. These retail stores offer a superior shopping experience, allowing customers to interact directly with store staff for product recommendations and feedback on product usage. Unlike online purchases, retail stores provide immediate product possession and the opportunity to examine products before buying. These advantages drive the growth of the retail segment in the market.

Retail outlets cater to the increasing demand for health and wellness products by stocking and selling a wide range of options. For example, The Organic Supermarket in Ireland has multiple branches that offer organic food products, including fresh fruits, vegetables, and packaged items like cheese and tofu. The presence of such retail outlets, along with their investments, supports market growth. Major food retailers like Whole Foods Market and Safeway are actively procuring healthy foods market to meet the rising consumer demand. Whole Foods Market, for instance, replaces sugary drinks and snacks with healthier beverage alternatives. This trend of retailers prioritizing health-conscious products and minimally processed food foods further contributes to the expansion of the market.

Naturally healthy food refers to food products that undergo minimal processing and do not contain artificial ingredients. These foods are free from hormones, antibiotics, and artificial flavors. Examples of naturally healthy options include zero trans-fat oils, whole wheat and multigrain bread, baked potato chips and wedges, and cereal grain flour. To provide complete product information and avoid misbranding, food companies that manufacture natural health foods often include a "natural" label on their products. This label may indicate that the food has no added coloring, no artificial ingredients, or is minimally processed.

The natural health food segment showed a gradual increase in market share of USD 216.40 million in 2017 and continued to grow by 2021. Naturally healthy food is consumed globally due to its numerous health benefits. These include improved digestion, better nutrient absorption, regulation of blood sugar levels, and enhanced immunity due to the antioxidant properties of such food products. While natural food products do not carry certifications from authorities like the USDA, FDA, or ESFA for their "natural" labeling, the absence of formal regulations and certifications has led to an increase in market growth. The rising adoption of natural health products for their inherent health benefits has attracted new players to enter the market and meet the growing demand.

For a detailed summary of the market segments Request for Sample Report

Functional food is produced using specific ingredient transparency known as plant stanols and sterols, which offer health-enhancing properties and help prevent certain diseases. These components, derived from plant membranes, have been shown to lower blood cholesterol levels. An example of functional food is low-fat spreads that contain stanols to aid in cholesterol reduction. Additionally, functional foods can be fortified with nutrients not typically found in the product. For instance, omega-3 fatty acids extracted from fish oils can be added to bread or baked beans to provide additional health benefits. Consequently, the consumption of functional food has increased as individuals seek to improve their health and compensate for poor dietary habits. The growing prevalence of diseases like diabetes, cancer, allergies, and dental issues has further motivated people to choose functional food options. It's worth noting that oral health is closely linked to one's diet, with dietary acids found in soft drinks posing risks of dental erosion.

Get a glance at the market share of various regions View PDF Sample

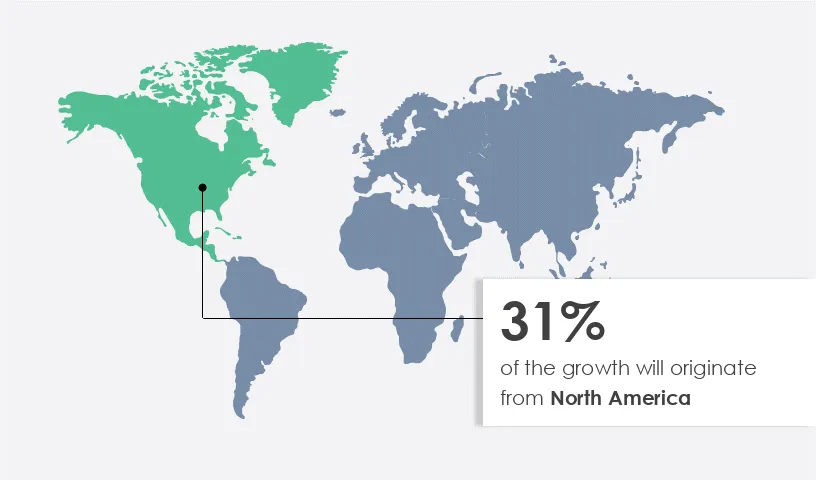

North America is projected to contribute 31% by 2027. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

North America has a large number of food halls and retail stores and chains such as Walmart, Costco, Kroger, SuperTarget, Safeway, and Whole Foods Market that offer health and nutritional food such as organic food. The increasing number of food service establishments and eateries, the presence of several small and large players, M&A (such as the acquisition of Cold Brew Coffee by Nestle and RXBAR by Kellogg), and the emergence of startups are driving the growth of the regional market. Processed food is the leading cause of chronic health problems such as obesity, hypertension, diabetes, and cardiovascular diseases (CVDs) due to high levels of refined grains, added sugar, salt, unhealthy fats, and animal-source ingredients in such food products.

In today's health and wellness market, consumers are increasingly prioritizing their well-being, driving demand for a wide range of nutritious food products. From snacks to supplements, individuals are seeking options that support their dietary needs and fitness goals. Retailers and brands are responding to this demand by offering a variety of innovative products, with a focus on natural, organic, and gluten-free options. The emphasis on holistic wellness extends beyond just physical health, with consumers also seeking products that support immune function, digestion, and energy levels.

With growing awareness of the health benefits of vitamins, minerals, antioxidants, and probiotics, the market for wellness foods is booming. From grocery stores to health food shops, consumers have access to a plethora of options to support their healthy lifestyles. As the wellness industry continues to evolve, innovation and knowledge-sharing are driving the development of new strategies and products to meet the diverse needs of consumers in different regions. Whether it's in-store or online, the health and wellness market offers an array of options for individuals looking to prioritize their well-being through dietary choices and lifestyle changes.

The packaged food industry is experiencing a significant shift as consumers increasingly prioritize a nutritional diet and active lifestyle. With a growing focus on low calories options, the market value is expected to soar, driven by a rising demand for protein-based nutritional and healthy food. The surge in popularity of clean label food among millennials underscores a broader trend towards fortified food and beverages. However, trade regulations and import-export analysis may impact market dynamics, as well as challenges such as raw material shortage and shipping delays.

The market report forecasts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and growth opportunities from 2017 to 2027.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

176 |

|

Base year |

2022 |

|

Historic period |

2017-2021 |

|

Forecast period |

2023-2027 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.5% |

|

Market growth 2023-2027 |

USD 452.93 million |

|

Market structure |

USD Fragmented |

|

YoY growth 2022-2023(%) |

7.87 |

|

Regional analysis |

North America, APAC, Europe, Middle East and Africa, and South America |

|

Performing market contribution |

North America at 31% |

|

Key countries |

US, China, Japan, UK, and France |

|

Competitive landscape |

Leading companies, Market Positioning of companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Amys Kitchen Inc., Archer Daniels Midland Co., Bobs Red Mill Natural Foods Inc., Chobani Global Holdings LLC, Clif Bar and Co., Dairy Farmers of America Inc., Danone SA, Dr. Schar AG, Fifty50 Foods, General Mills Inc., Glanbia Plc, GlaxoSmithKline Plc, Kellogg Co., London Foods Ltd., Mars Inc., Nestle SA, PepsiCo Inc., Yakult Honsha Co. Ltd., Mondelez International Inc., and United Natural Foods Inc. |

|

Market dynamics |

Parent market analysis, market growth and trends, market forecasting, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for forecast period. |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

BUY NOW Full Report and Discover more

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Product

7 Market Segmentation by Distribution Channel

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights