India Electric Vehicle Market Size 2026-2030

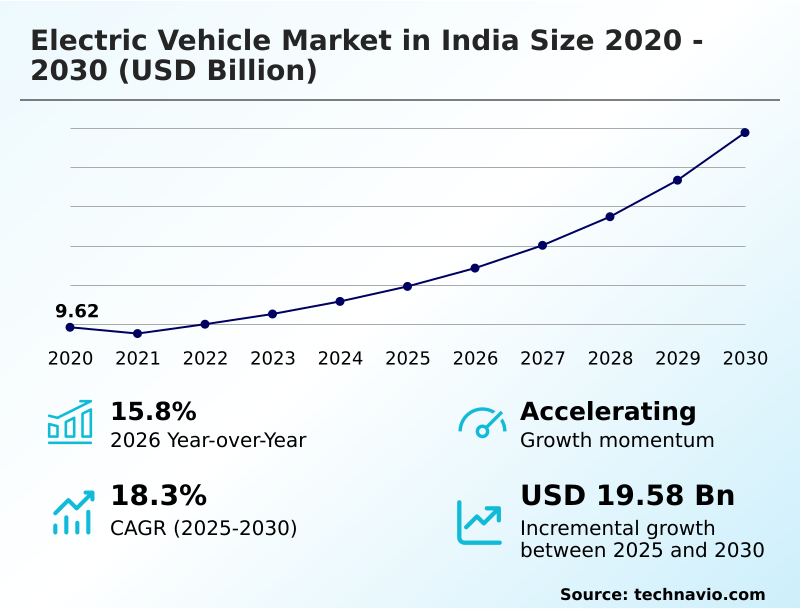

The india electric vehicle market size is valued to increase by USD 19.58 billion, at a CAGR of 18.3% from 2025 to 2030. Comprehensive government policy frameworks and fiscal incentives will drive the india electric vehicle market.

Major Market Trends & Insights

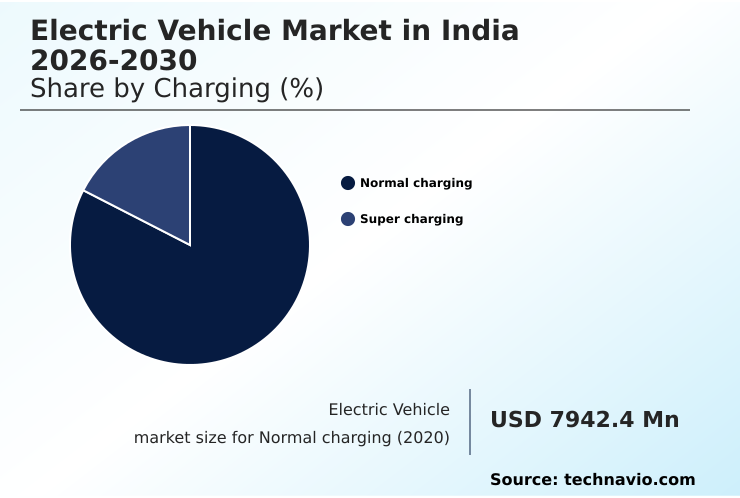

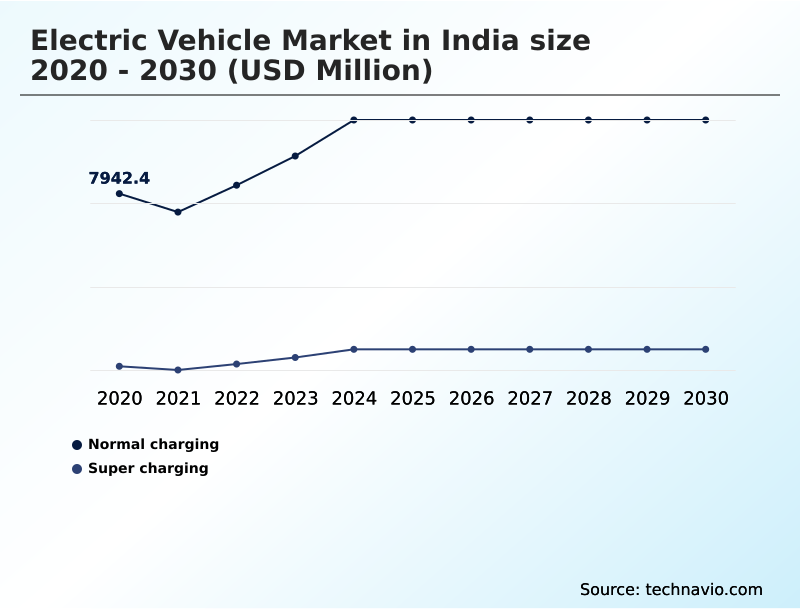

- By Charging - Normal charging segment was valued at USD 10.61 billion in 2024

- By Vehicle Type - Passenger cars segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 24.77 billion

- Market Future Opportunities: USD 19.58 billion

- CAGR from 2025 to 2030 : 18.3%

Market Summary

- The electric vehicle market in India is undergoing a significant transformation, driven by robust government policies and a growing consumer preference for sustainable mobility. This industrial shift is characterized by a strong focus on localizing the supply chain through production-linked incentives, which are crucial for reducing dependency on imported components and lowering the total cost of ownership for end-users.

- While the passenger car segment is maturing with new model introductions, the market's momentum is primarily fueled by the two- and three-wheeler segments, which dominate last-mile connectivity and urban transport.

- For instance, a fleet operator evaluating a transition to electric vehicles for its last-mile delivery operations must analyze not just the initial acquisition cost but also the long-term savings from lower fuel and maintenance expenses, factoring in available subsidies and the density of charging infrastructure.

- However, the industry grapples with challenges like fiscal policy instability and an inverted duty structure that can impede the progress of domestic manufacturing. The expansion of high-speed charging networks and innovations in battery technology are critical for addressing range anxiety and ensuring the long-term viability of this transition to a low-carbon transport economy.

What will be the Size of the India Electric Vehicle Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the India Electric Vehicle Market Segmented?

The india electric vehicle industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Charging

- Normal charging

- Super charging

- Vehicle type

- Passenger cars

- Commercial vehicles

- Type

- BEV

- PHEV

- Geography

- APAC

- India

- APAC

By Charging Insights

The normal charging segment is estimated to witness significant growth during the forecast period.

The normal charging segment, primarily composed of AC chargers, forms the bedrock of the electric vehicle market in India, supporting the mass adoption of electric two-wheelers and the electric three-wheeler cargo sector.

This infrastructure is concentrated in residential and workplace settings, where lower power draw aligns with longer parking durations, enhancing grid stability integration and promoting a seamless urban mobility transition.

As of August 2025, the deployment of approximately 29,300 public charging stations reflects a strategic push to mitigate range anxiety.

The emphasis is on optimizing onboard charger specifications and smart charging solutions to lower the total cost of ownership, making the existing electric vehicle architecture more accessible for semi-urban mobility and accelerating the localization of lithium-ion cell manufacturing.

The Normal charging segment was valued at USD 10.61 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

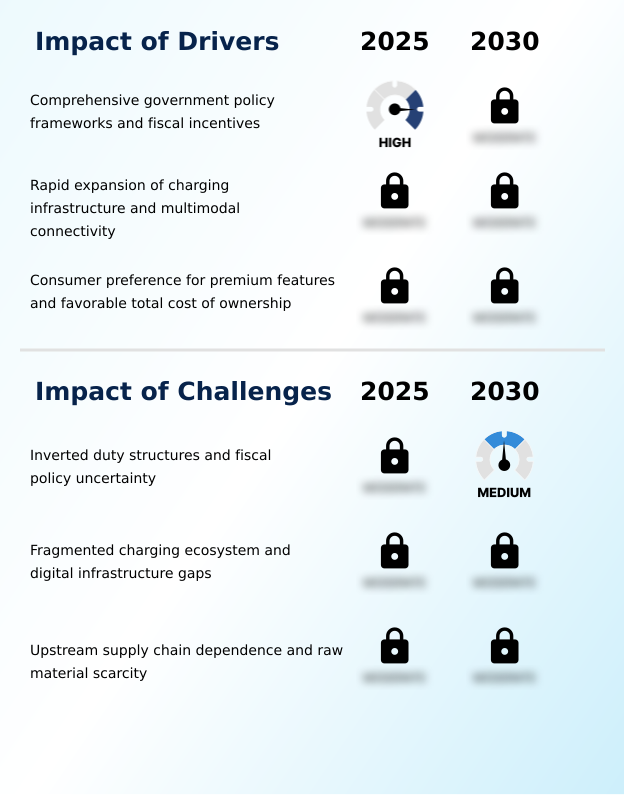

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The trajectory of the electric vehicle market in India 2026-2030 is intricately linked to overcoming specific economic and operational hurdles. A primary concern is the impact of GST on EV component pricing, where an inverted duty structure imposes higher tax rates on raw materials and parts compared to finished vehicles.

- This discrepancy complicates the challenges in localizing EV components and negatively affects the profitability of domestic manufacturing. In response, innovative business strategies are emerging, highlighting the role of battery-as-a-service models in reducing the high upfront cost for consumers. For commercial operators, the debate over battery swapping vs fast charging for fleets is crucial for optimizing uptime and operational efficiency.

- Simultaneously, government subsidies for electric passenger cars continue to stimulate demand in the personal mobility segment. For public transport, the focus remains on the total cost of ownership for electric buses, where lower operational expenses present a compelling case for municipal fleet conversion.

- The future of electric three-wheeler logistics, in particular, hinges on creating a cost-effective and resilient ecosystem that can support the nation's burgeoning e-commerce and last-mile delivery sectors, which have seen operational costs reduced by over 25% in some fleets after electrification.

What are the key market drivers leading to the rise in the adoption of India Electric Vehicle Industry?

- Comprehensive government policy frameworks and fiscal incentives are the primary drivers accelerating market adoption and investment.

- Robust government policies are the primary driver, with the production linked incentive scheme being pivotal for fostering supply chain localization and indigenous technology development.

- These incentives are designed to scale up the manufacturing of advanced chemistry cell batteries and critical power electronics, directly improving the total cost of ownership for consumers.

- This strategic support has fortified the domestic manufacturing ecosystem, with the automotive sector now contributing approximately 15% to national GST collections.

- While fiscal policy uncertainty remains a concern, the push for local traction motor design and battery-as-a-service models is creating a more resilient market.

- The focus on local lithium-ion cell manufacturing is expected to reduce supply chain costs by over 25% in the coming years.

What are the market trends shaping the India Electric Vehicle Industry?

- The structural dominance of electric two-wheelers and the rapid commercialization of last-mile logistics are defining the market's current growth trajectory.

- A defining trend is the structural dominance of two-wheelers in the urban mobility transition, alongside the rapid last-mile commercialization driven by the gig economy fleet. This bottom-up adoption is fueled by a superior total cost of ownership and the expansion of battery swapping infrastructure, which directly addresses range anxiety for commercial users.

- Consequently, the zero-emission fleet mandate from e-commerce giants has accelerated the uptake of light commercial electric vehicles. The market has seen a 60% increase in electric two-wheeler registrations in metropolitan hubs. While the electric drivetrain complexity is lower, firms are competing on regenerative braking efficiency and high-voltage battery pack performance.

- This trend has also spurred interest in high-performance electric SUV models, broadening the market's appeal beyond utilitarian use cases.

What challenges does the India Electric Vehicle Industry face during its growth?

- Inverted duty structures and uncertainty in fiscal policy create significant challenges for the industry's sustainable growth and localization efforts.

- A significant challenge remains the inverted duty structure, where critical components face an 18% tax while finished vehicles are taxed at 5%, straining manufacturers' working capital. This fiscal friction discourages deeper localization efforts for parts like the electric motor controller and battery management systems.

- Furthermore, the lack of long-term policy stability creates uncertainty, affecting investments in charging infrastructure expansion and commercial vehicle electrification. Addressing these gaps is crucial for the successful integration of renewable energy into the grid.

- The development of unified fast-charging standards and the exploration of vehicle-to-grid technology are essential to support the green mobility mandate, but progress is hampered by these underlying economic disincentives, delaying the widespread adoption of technologies like solid-state battery technology.

Exclusive Technavio Analysis on Customer Landscape

The india electric vehicle market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the india electric vehicle market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of India Electric Vehicle Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, india electric vehicle market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ashok Leyland Ltd. - Analysis indicates a focus on electrifying commercial vehicle segments, offering medium and heavy-duty bus and truck platforms designed for fleet and logistics applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ashok Leyland Ltd.

- BMW AG

- BYD Co. Ltd.

- Stellantis NV

- EKA Mobility

- Etrio Automobiles Pvt Ltd

- Euler Motors Pvt Ltd

- Hyundai Motor Co.

- JBM Group

- Mahindra and Mahindra Ltd.

- Mercedes Benz Group AG

- MG Motor

- TI Clean Mobility Pvt Ltd

- OMEGA SEIKI MOBILITY

- Tata Motors Ltd.

- Tesla Inc.

- VinFast Auto Ltd.

- Volvo Car Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in India electric vehicle market

- In February, 2025, VinFast Auto Ltd. announced plans to launch three new electric models and double its retail footprint to seventy-five showrooms across India to accelerate its market penetration strategy.

- In December, 2024, Mahindra and Mahindra Ltd. reported securing over 93,000 bookings for its new electric SUV models, signaling strong consumer demand for its INGLO-based platforms.

- In October, 2024, Ashok Leyland Ltd. inaugurated a new electric bus manufacturing facility in Lucknow with an investment of one thousand crore rupees to scale up its public transit electrification capacity.

- In September, 2024, leaders from JSW MG Motor India and Oben Electric publicly advocated for the rationalization of the inverted duty structure in the upcoming Union Budget to support the domestic manufacturing ecosystem.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled India Electric Vehicle Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 170 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 18.3% |

| Market growth 2026-2030 | USD 19580.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 15.8% |

| Key countries | India |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The electric vehicle market in India is defined by rapid technological evolution and a strategic push toward a self-reliant manufacturing ecosystem. At the core of this transition is the decreasing electric drivetrain complexity and the increasing sophistication of battery management systems, which are critical for optimizing performance and longevity.

- The industry's focus is on scaling up advanced chemistry cell batteries and advancing lithium-ion cell manufacturing to reduce import reliance, a move that can lower component costs by over 20%. The development of a localized electric vehicle architecture, including proprietary traction motor design and powertrain electrification, is enabling the creation of vehicles tailored for local conditions.

- Innovations such as over-the-air updates are transforming vehicles into software-defined platforms, presenting new revenue opportunities for automakers. Boardroom decisions are now centered on integrating these technologies, from vehicle-to-grid technology to solid-state battery technology, to build a competitive advantage in a market increasingly shaped by fast-charging standards and the expansion of battery swapping infrastructure.

What are the Key Data Covered in this India Electric Vehicle Market Research and Growth Report?

-

What is the expected growth of the India Electric Vehicle Market between 2026 and 2030?

-

USD 19.58 billion, at a CAGR of 18.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Charging (Normal charging, and Super charging), Vehicle Type (Passenger cars, and Commercial vehicles), Type (BEV, and PHEV) and Geography (APAC)

-

-

Which regions are analyzed in the report?

-

APAC

-

-

What are the key growth drivers and market challenges?

-

Comprehensive government policy frameworks and fiscal incentives, Inverted duty structures and fiscal policy uncertainty

-

-

Who are the major players in the India Electric Vehicle Market?

-

Ashok Leyland Ltd., BMW AG, BYD Co. Ltd., Stellantis NV, EKA Mobility, Etrio Automobiles Pvt Ltd, Euler Motors Pvt Ltd, Hyundai Motor Co., JBM Group, Mahindra and Mahindra Ltd., Mercedes Benz Group AG, MG Motor, TI Clean Mobility Pvt Ltd, OMEGA SEIKI MOBILITY, Tata Motors Ltd., Tesla Inc., VinFast Auto Ltd. and Volvo Car Corp.

-

Market Research Insights

- The dynamics of the electric vehicle market in India are shaped by a confluence of supportive policies and persistent structural challenges. The push for a domestic manufacturing ecosystem is evident, yet fiscal policy uncertainty complicates long-term investment decisions.

- For example, an inverted duty structure where components are taxed at 18% while finished vehicles are taxed at 5% directly impacts the profitability of local assembly, a critical factor for companies planning market entry. Despite this, consumer adoption is accelerating, with electric passenger vehicle registrations showing a 77% year-on-year increase.

- This growth is a testament to a favorable total cost of ownership and a growing charging infrastructure expansion, which together help in range anxiety mitigation and support the broader urban mobility transition for both private and gig economy fleet applications.

We can help! Our analysts can customize this india electric vehicle market research report to meet your requirements.

RIA -

RIA -