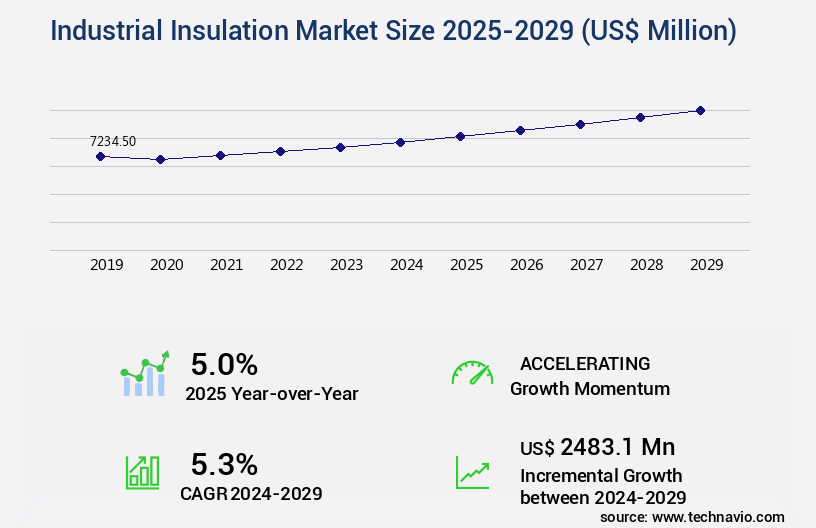

Industrial Insulation Market Size 2025-2029

The industrial insulation market size is valued to increase USD 2.48 billion, at a CAGR of 5.3% from 2024 to 2029. Growing need for energy efficiency in buildings will drive the industrial insulation market.

Major Market Trends & Insights

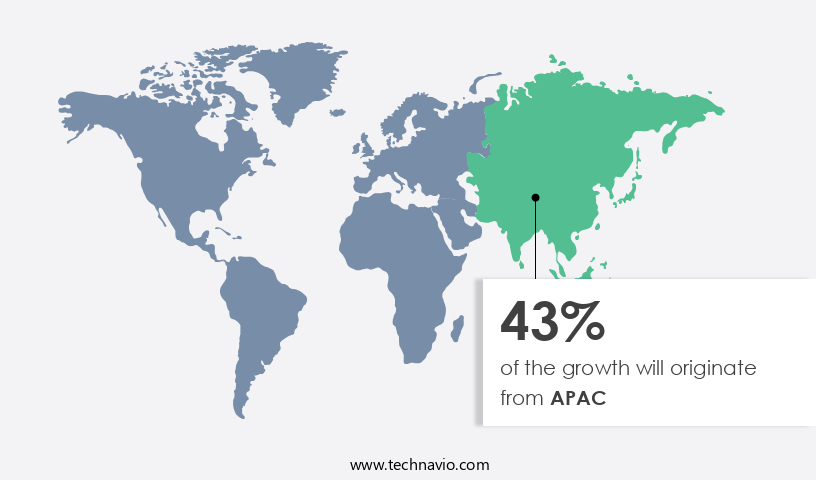

- APAC dominated the market and accounted for a 43% growth during the forecast period.

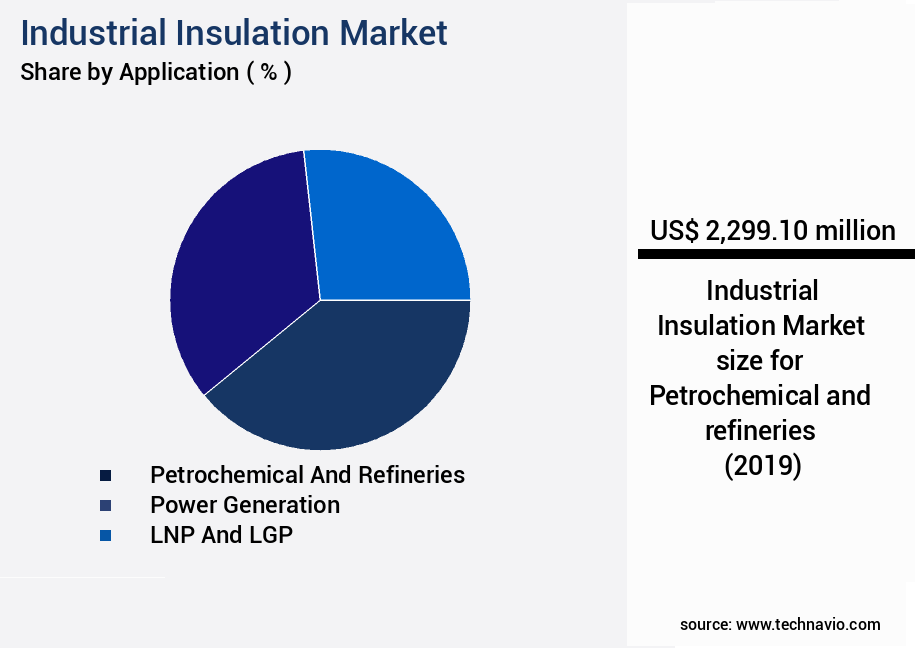

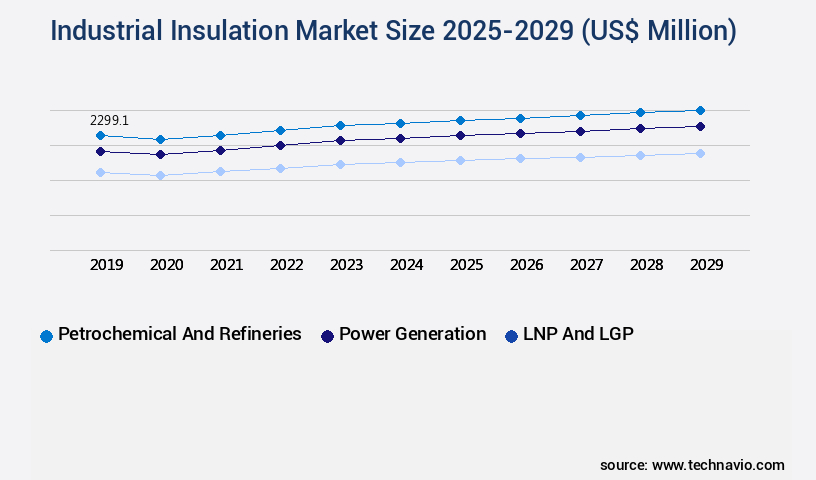

- By Application - Petrochemical and refineries segment was valued at USD 2.3 billion in 2023

- By Material - Mineral wool segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 49.62 million

- Market Future Opportunities: USD 2483.10 million

- CAGR : 5.3%

- APAC: Largest market in 2023

Market Summary

- The market encompasses the production and application of various insulation materials and techniques to protect industrial processes from heat loss or gain, chemical reactions, and external environmental factors. This dynamic market is driven by the growing need for energy efficiency in industries and buildings, with core technologies and applications evolving to integrate smart technologies and digitalization in insulation systems. Service types, such as insulation installation and maintenance, are crucial components of the market. Product categories, including thermal insulation, acoustic insulation, and fireproof insulation, cater to diverse industry requirements. Regulations, such as energy efficiency standards and safety regulations, shape the market landscape.

- The market is expected to witness significant growth in the coming years, with the increase in popularity of acoustic insulation solutions in the construction sector being a major driver. According to recent market research, the global acoustic insulation market is projected to reach a 30% market share by 2025. This growth is fueled by the demand for noise reduction in residential and commercial buildings, as well as in industrial applications. Related markets such as the Building Insulation and Refrigeration Insulation markets are also experiencing similar trends. The challenges faced by the market include the high cost of insulation materials and the need for skilled labor for installation and maintenance.

- However, opportunities exist in the form of technological advancements, such as the development of eco-friendly insulation materials and the increasing adoption of automation in insulation processes. In conclusion, the market is a continuously evolving entity, shaped by technological advancements, regulatory requirements, and market trends. The market's future growth is expected to be robust, driven by the increasing demand for energy efficiency and noise reduction solutions.

What will be the Size of the Industrial Insulation Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Industrial Insulation Market Segmented and what are the key trends of market segmentation?

The industrial insulation industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Petrochemical and refineries

- Power generation

- LNP and LGP

- Others

- Material

- Mineral wool

- Plastic foam

- Calcium silicate

- Others

- Product

- Blanket

- Board

- Pipe

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Application Insights

The petrochemical and refineries segment is estimated to witness significant growth during the forecast period.

Industrial insulation plays a pivotal role in various industries by ensuring thermal efficiency, energy savings, and safety. In 2024, the petrochemical and refineries segment accounted for a substantial share in The market. This segment focuses on insulating equipment, piping, and processing units in petrochemical plants and refineries to maintain operational efficiency, safety, and environmental compliance. Effective insulation is essential in preventing heat loss, conserving energy, and facilitating controlled temperatures for high-temperature petrochemical processes. Insulation materials, such as refractory materials and pipe insulation, are used to maintain optimal temperatures in reactors, distillation columns, and furnaces.

Insulation testing is crucial to ensure thermal performance, vibration damping, condensation control, and moisture resistance. Heat transfer and thermal conductivity are critical factors in insulation applications. Insulation materials with low thermal conductivity, such as polyurethane and mineral wool, are preferred for their excellent insulating properties. Protective coatings are also used to enhance insulation materials' resistance to corrosion and degradation, extending their lifespan. Industrial insulation systems are continually evolving to meet the demands of various sectors. For instance, refrigeration insulation is used to maintain low temperatures in cold storage facilities and refrigeration systems. Energy efficiency and environmental impact are increasingly important considerations in the market.

Building codes and regulations also influence the adoption of insulation materials and systems. Insulation installation procedures and maintenance are crucial for maximizing the benefits of insulation systems. Retrofit insulation is an essential aspect of upgrading existing insulation systems to improve energy efficiency and reduce heat loss. Proper insulation thickness and the use of appropriate materials are essential for achieving optimal performance. In the future, the market is expected to grow significantly, driven by increasing demand for energy efficiency, safety, and environmental compliance. For instance, The market is projected to grow by 15.3% in terms of revenue by 2027.

Additionally, the market for acoustic insulation is expected to grow by 7.5% during the same period due to the increasing demand for noise reduction in industrial applications. In conclusion, the market is a dynamic and evolving sector that plays a crucial role in various industries. Effective insulation is essential for maintaining optimal temperatures, reducing energy consumption, and ensuring safety and environmental compliance. The market is expected to grow significantly in the coming years, driven by increasing demand for energy efficiency, safety, and environmental sustainability.

The Petrochemical and refineries segment was valued at USD 2.3 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 43% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Industrial Insulation Market Demand is Rising in APAC Request Free Sample

The market in APAC is experiencing significant growth, making it the largest market globally. China, as a major producer and consumer, plays a pivotal role in this expansion. The region's responsive customer base has led manufacturing bases to relocate from Western Europe and North America, fueling market growth. Infrastructure development and China's emergence as a global manufacturing hub are primary drivers, with the increasing number of construction projects in China being a significant factor. According to recent data, APAC accounted for approximately 45% of the global industrial insulation demand in 2020.

Furthermore, the region's insulation market is projected to grow at a steady pace, with China's market share expected to reach 60% by 2025. This growth can be attributed to the increasing adoption of insulation materials in various industries, such as power generation, oil and gas, and chemical processing, to improve energy efficiency and reduce emissions.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market encompasses a wide range of high temperature insulation materials and industrial pipe insulation systems designed to enhance thermal performance in various applications. With increasing focus on reducing heat loss and improving energy efficiency, thermal performance building codes continue to evolve, driving the demand for efficient insulation installation methods and optimal insulation thickness calculations. Insulation material selection criteria vary depending on the specific application. For instance, refractory insulation is crucial for industrial furnaces, while moisture management is a key consideration for insulation systems in humid environments. In addition, protective coatings and fire-resistant insulation specifications are essential for ensuring safety and compliance with regulations.

Acoustic insulation and vibration damping applications are also gaining traction in the industrial sector, particularly for machinery and equipment that generate noise and vibrations. Insulation material life cycle assessment is increasingly important for organizations seeking to minimize environmental impact and optimize costs. When it comes to industrial pipe insulation, reducing thermal conductivity is a critical factor for ensuring energy efficiency and cost savings. For instance, a study comparing two commonly used insulation materials, polyurethane and mineral wool, revealed that polyurethane offers a thermal conductivity value 0.032 W/mK lower than mineral wool (Source: ASHRAE Handbook). This translates to potential energy savings and reduced greenhouse gas emissions.

Insulation system corrosion protection is another essential aspect, with thermal bridging in industrial buildings being a significant concern. Proper insulation installation and regular testing against industry standards, such as ASTM C111 and ASTM C518, can help mitigate these issues and ensure the longevity of insulation systems. In summary, the market is driven by various trends, including energy efficiency, safety, and environmental sustainability. By selecting the right insulation materials, installation methods, and testing standards, organizations can optimize their operations, reduce costs, and minimize environmental impact.

What are the key market drivers leading to the rise in the adoption of Industrial Insulation Industry?

- The increasing demand for energy efficiency in buildings serves as the primary market catalyst.

- The market experiences continuous growth due to the increasing emphasis on energy efficiency in commercial and residential buildings. Energy consumption in structures equipped with refrigerators and air-conditioning units contributes significantly to the overall energy demand. Insulation materials play a crucial role in reducing energy leakage and enhancing a building's efficiency. The rising energy costs and the push for energy conservation by governments worldwide fuel the market's expansion. By implementing insulation, buildings can minimize their reliance on fossil fuels for power generation, thereby contributing to environmental sustainability.

- The adoption of advanced insulation technologies and the increasing awareness of energy conservation further boost the market's growth. Companies specializing in industrial insulation solutions continue to innovate, offering products with improved thermal performance and durability. This ongoing development ensures the market remains dynamic and responsive to the evolving needs of various sectors.

What are the market trends shaping the Industrial Insulation Industry?

- The integration of smart technologies and digitalization is becoming a mandated trend in the insulation systems market. Smart technologies and digitalization are increasingly being integrated into insulation systems.

- The integration of smart technologies and digitalization in insulation systems within The market signifies a substantial evolution in the industry. This transformation focuses on augmenting energy efficiency, cost-effectiveness, and optimizing performance in industrial settings. One illustrative application of this integration is the implementation of smart sensors in insulation systems. These sensors are engineered to observe and compile data on temperature, humidity, and other significant variables.

- By harnessing this data, industrial facilities can obtain real-time insights into their insulation systems' performance. This forward-thinking approach facilitates the early identification of potential issues, enabling timely maintenance and minimizing energy loss. The implementation of these advanced technologies fosters a more data-driven and proactive approach to industrial insulation management.

What challenges does the Industrial Insulation Industry face during its growth?

- The rising demand for acoustic insulation solutions poses a significant challenge to the industry's growth trajectory.

- The market faces ongoing challenges due to the lack of technical expertise and installation issues. These hurdles significantly impact the industry's efficiency, effectiveness, and safety. Subpar insulation installations, resulting from insufficient knowledge and skills, lead to increased energy consumption in industrial facilities. Moreover, inadequate insulation installations pose safety concerns, as they can create fire hazards and fail to meet regulatory requirements. This puts the safety of workers and the integrity of industrial operations at risk.

- The ongoing need for technical proficiency in insulation installation is crucial for the industry's continuous growth and improvement.

Exclusive Customer Landscape

The industrial insulation market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the industrial insulation market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Industrial Insulation Industry

Competitive Landscape & Market Insights

Companies are implementing various strategies, such as strategic alliances, industrial insulation market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

API Group Corp. - Anco Products, Inc., a subsidiary of the company, specializes in the production of industrial insulation, including cryogenic LNG tank insulation. Their offerings ensure optimal temperature maintenance and energy efficiency for various industries.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- API Group Corp.

- Armacell International SA

- Aspen Aerogels Inc.

- BASF SE

- BNZ Materials.

- Cabot Corp.

- Compagnie de Saint Gobain SA

- Dongsung Finetec

- DUNA-Corradini Spa

- Ibiden Co. Ltd.

- Imerys S.A.

- Kingspan Group Plc

- Knauf Digital GmbH

- L ISOLANTE K FLEX S.p.A.

- Morgan Advanced Materials Plc

- NICHIAS Corp.

- NMC International SA

- Owens Corning

- Pacor Inc.

- Rath Aktiengesellschaft

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Industrial Insulation Market

- In January 2024, DuPont de Nemours, a leading materials science company, announced the launch of Tyvek Insulation ENERSHIELD Plus, an advanced insulation solution that combines thermal insulation and water resistance (DuPont Press Release, 2024). This product expansion aims to cater to the growing demand for energy-efficient and water-resistant insulation in industrial applications.

- In March 2024, BASF SE and Huntsman Corporation announced a strategic collaboration to develop and commercialize new insulation materials based on BASF's Neopor open-cell structural foam technology (BASF Press Release, 2024). This partnership is expected to strengthen their market position in the industrial insulation sector by offering innovative and sustainable insulation solutions.

- In May 2024, Johns Manville, a Berkshire Hathaway company, completed the acquisition of Axiall Corporation's Engineered Products business for approximately USD3.3 billion (Johns Manville Press Release, 2024). This acquisition significantly expanded Johns Manville's product portfolio and market reach in the market.

- In April 2025, the European Union passed the revised Energy Performance of Buildings Directive (EPBD), which includes stricter energy efficiency requirements for new and existing buildings (European Parliament Press Release, 2025). This regulatory initiative is expected to boost the demand for advanced insulation materials and technologies in the European the market.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Industrial Insulation Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

213 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.3% |

|

Market growth 2025-2029 |

USD 2483.1 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

5.0 |

|

Key countries |

China, US, Japan, India, Canada, Germany, UK, South Korea, France, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market encompasses a diverse range of insulation types and applications, each designed to mitigate heat transfer and enhance thermal performance in various industries. Insulation materials, such as pipe insulation and refractory materials, exhibit distinct thermal conductivities and material densities, influencing their effectiveness in different contexts. Heat transfer between surfaces plays a significant role in insulation's importance, with insulation materials reducing heat loss and surface temperature differences. Insulation testing is crucial to assessing the thermal performance of insulation systems, ensuring optimal energy savings and environmental impact reduction. Industrial insulation systems serve numerous applications, including protective coatings, refrigeration insulation, and insulation for equipment and buildings.

- These systems contribute to corrosion prevention, vibration damping, condensation control, and moisture resistance. Insulation materials' lifespan and fire resistance are essential factors in their adoption. Thinner insulation thicknesses and advanced insulation installation techniques have emerged to address building codes and thermal bridging concerns. The market for insulation materials is dynamic, with ongoing research and development focusing on enhancing insulation materials' thermal performance, energy efficiency, and environmental sustainability. Material innovations, such as acoustic insulation and insulation degradation mitigation, continue to expand the market's scope. Maintenance procedures and retrofit insulation are critical aspects of insulation systems' longevity and performance.

- As industries strive for energy efficiency and regulatory compliance, the demand for advanced insulation technologies and systems continues to grow.

What are the Key Data Covered in this Industrial Insulation Market Research and Growth Report?

-

What is the expected growth of the Industrial Insulation Market between 2025 and 2029?

-

USD 2.48 billion, at a CAGR of 5.3%

-

-

What segmentation does the market report cover?

-

The report segmented by Application (Petrochemical and refineries, Power generation, LNP and LGP, and Others), Material (Mineral wool, Plastic foam, Calcium silicate, and Others), Product (Blanket, Board, Pipe, and Others), and Geography (APAC, North America, Europe, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Growing need for energy efficiency in buildings, Increase in popularity of acoustic insulation solutions

-

-

Who are the major players in the Industrial Insulation Market?

-

Key Companies API Group Corp., Armacell International SA, Aspen Aerogels Inc., BASF SE, BNZ Materials., Cabot Corp., Compagnie de Saint Gobain SA, Dongsung Finetec, DUNA-Corradini Spa, Ibiden Co. Ltd., Imerys S.A., Kingspan Group Plc, Knauf Digital GmbH, L ISOLANTE K FLEX S.p.A., Morgan Advanced Materials Plc, NICHIAS Corp., NMC International SA, Owens Corning, Pacor Inc., and Rath Aktiengesellschaft

-

Market Research Insights

- The market encompasses a diverse range of insulation solutions, including reflective, HVAC, tank, pipe lagging, and spray foam insulation, among others. Two key areas of focus in this market are ensuring quality control and adherence to health and safety regulations. For instance, high-temperature insulation, such as mineral wool and cellular glass, are commonly used in industrial processes to maintain optimal operating temperatures and enhance energy efficiency. In contrast, low-temperature insulation, like vacuum insulation and aerogel, are essential for cryogenic applications. Cost analysis plays a crucial role in material selection for industrial insulation projects. For instance, fiber glass insulation offers a competitive cost advantage in many applications due to its affordability and ease of installation.

- However, high-performance insulation materials like aerogel and vacuum insulation may have higher upfront costs but can yield significant long-term energy savings and improved regulatory compliance. Installation techniques, such as spray foam application and pipe lagging, are continually evolving to optimize insulation performance and reduce labor costs. Thermal modeling and energy audits are integral to the design specifications process, ensuring that insulation solutions meet the unique demands of various industrial applications. Regulatory compliance remains a critical consideration, with insulation standards continually being updated to reflect evolving environmental and safety requirements.

We can help! Our analysts can customize this industrial insulation market research report to meet your requirements.

RIA -

RIA -