Industrial Sugar Market Size 2025-2029

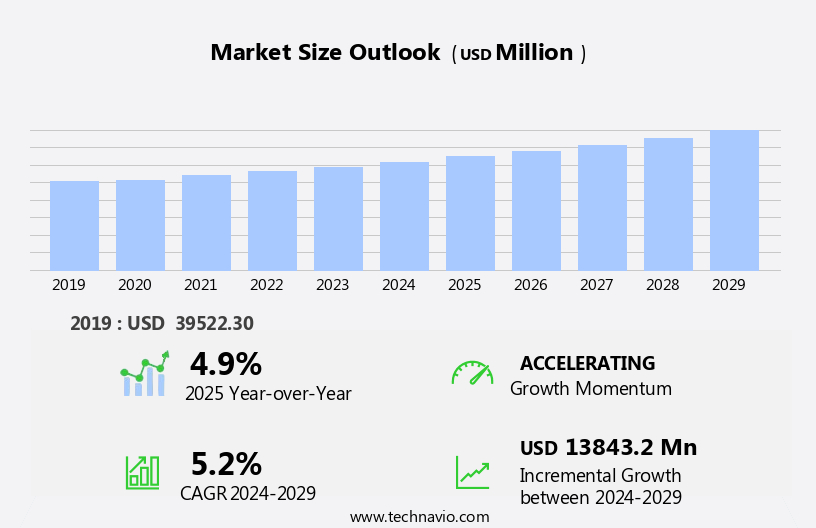

The industrial sugar market size is forecast to increase by USD 13.84 billion at a CAGR of 5.2% between 2024 and 2029.

- The market is experiencing significant growth, driven primarily by the increasing demand for raw sugar in food and beverage applications. This trend is fueled by consumers' shifting preferences towards natural and organic food products, which often utilize raw sugar as a sweetener. However, market expansion is not without challenges. Government regulations on the production, processing, and sales of raw sugar pose hurdles for market participants. These regulations aim to ensure food safety and ethical production practices, but they can increase production costs and complicate supply chains. Consumers are increasingly seeking healthier food options and condiments, leading to a demand for vinegar as a natural flavoring agent and health supplement. Additionally, inconsistencies in the sugar supply chain, including fluctuations in sugar prices and availability, can temper growth potential.

- Companies seeking to capitalize on market opportunities must navigate these challenges effectively by staying informed of regulatory changes and implementing robust supply chain management strategies. By doing so, they can position themselves to meet the rising demand for raw sugar in various industries while maintaining operational efficiency and profitability. Furthermore, the increasing benefits and the rising demand for products with health and wellness attributes, coupled with the increasing popularity of regional cuisines outside of their originated region, are likely to propel the growth of the household segment during the forecast period.

What will be the Size of the Industrial Sugar Market during the forecast period?

- The market is characterized by continuous advancements in technology and sustainability initiatives. Sugar milling technology and refining processes have undergone significant improvements, enhancing efficiency and product quality. Sugar logistics and transport systems have also evolved, ensuring timely delivery and reducing costs. Sugar certification programs play a crucial role in maintaining market transparency and promoting sustainability. Sugar sustainability initiatives, such as beet cultivation practices and traceability systems, are gaining traction among consumers and stakeholders. Sugar analytics and data analysis tools help market participants make informed decisions amidst sugar market fluctuations. Sugar reduction and sugar-free product development are key trends, driven by health concerns and consumer preferences. In the culinary world, distilled white vinegar is commonly used for pickling vegetables and adds a strong acidic kick to salad dressings, marinades, and sauces.

- Sugar innovation trends include automation and robotics in sugar production, as well as the exploration of sugar alternatives and substitutes. Sugar health benefits and economic impact are subjects of ongoing research and debate. Sugar beet harvesting and cane cultivation practices continue to evolve, with a focus on minimizing environmental impact and maximizing yields. Sugar awareness campaigns aim to educate consumers about sugar consumption reduction and the importance of quality control in the sugar industry. Price volatility remains a challenge for sugar market participants, necessitating effective demand forecasting strategies. Social impact and sugar's role in local communities are increasingly important considerations for stakeholders. Additionally, distilled white vinegar is used in pharmaceuticals for various health benefits, in cosmetics for its astringent properties, and in biofuels due to its high acetic acid content. Overall, the sugar market is dynamic and complex, requiring constant adaptation and innovation to meet evolving consumer demands and market trends.

How is this Industrial Sugar Industry segmented?

The industrial sugar industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

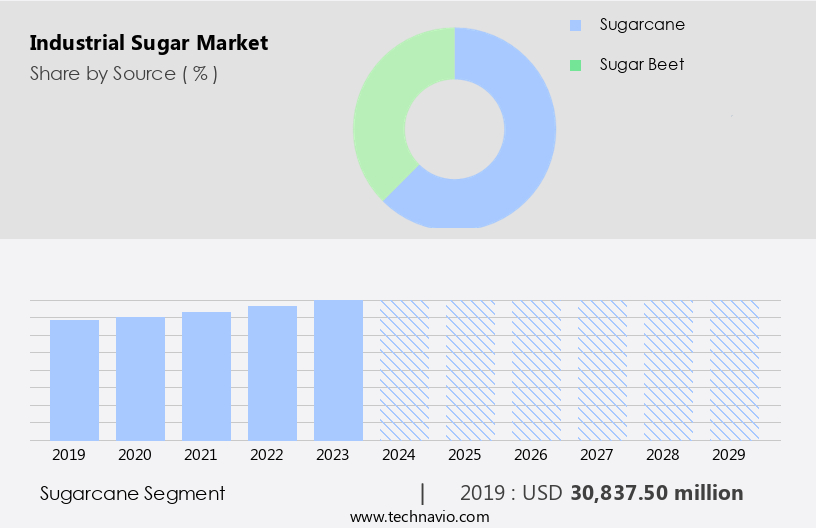

- Source

- Sugarcane

- Sugar beet

- Type

- White sugar

- Brown sugar

- Liquid sugar

- Application

- Food and beverage

- Pharmaceutical

- Biofuel

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Source Insights

The sugarcane segment is estimated to witness significant growth during the forecast period. Sugarcane, a key component of the market, is primarily grown in regions with favorable climates, including South America, the Caribbean, APAC, and parts of Africa. This tropical grass is cultivated for its high sucrose content. The sugar production process begins with the growth of sugarcane in extensive plantations. Once mature, the cane is harvested by cutting it close to the ground. The harvested cane is then transported to sugar mills for processing. Here, the cane undergoes crushing to extract the juice, which is further purified through various stages of filtration and crystallization to produce refined sugar. Sugarcane juice is also used as a raw material in the production of sugar syrup, a sweetener widely used in various industries, including the confectionery, beverage, and bakery sectors.

Sugar technology plays a crucial role in enhancing sugar efficiency and reducing production costs. Innovations in sugar processing, such as sugar crystallization and drying techniques, have led to improvements in sugar quality and purity. The pet food industry utilizes sugar beet pulp as a primary source of dietary fiber. Sugar beets are extracted using sugar extraction techniques, which yield both sugar and beet molasses as byproducts. Sugar molasses is used as animal feed or processed further to produce sugar derivatives, such as ethanol and various other industrial applications. Sugar regulations and certifications, such as those related to sugar traceability and sustainability, have become increasingly important in the sugar industry.

From sugar extraction and refining to the production of sugar syrup, sugar derivatives, and beet pulp, various industries depend on sugar to meet their specific needs. Innovations in sugar technology and sustainability, as well as regulatory compliance, will continue to shape the future of the sugar industry.

The Sugarcane segment was valued at USD 30.84 billion in 2019 and showed a gradual increase during the forecast period. These regulations ensure the ethical sourcing and production of sugar while maintaining consumer trust. The biotech industry has also contributed to sugar innovation through genetically modified sugarcane varieties that exhibit higher sugar yield and resistance to pests and diseases. The sugar industry's future lies in its ability to adapt to changing market trends and consumer preferences. Sugar consumption trends have shifted towards healthier alternatives, leading to an increased focus on low-calorie sweeteners and sugar substitutes. The dairy industry has also shown a growing demand for lactose-free milk, which is produced using sugar beet lactose. The market is a dynamic and evolving industry that relies on the efficient production and processing of sugarcane.

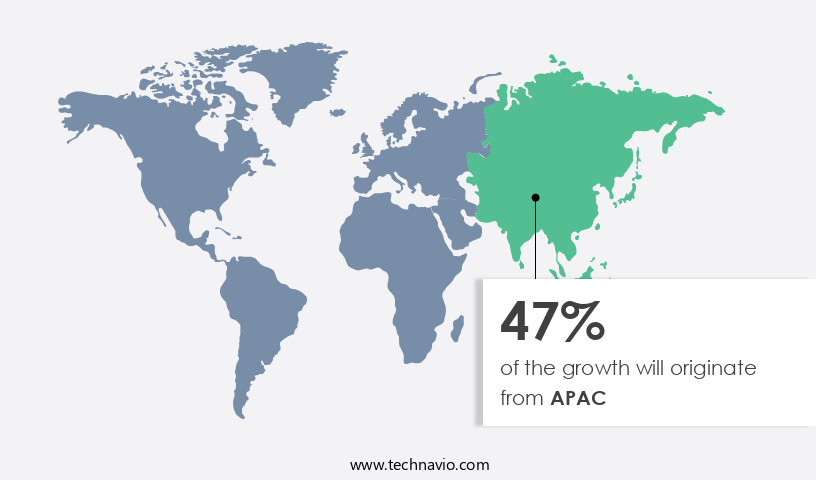

Regional Analysis

APAC is estimated to contribute 47% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market is a significant global sector, with the Asia Pacific region holding a prominent position due to its large and growing population and increasing demand for sweeteners and confectioneries. Key countries, including India, China, Thailand, Indonesia, and Australia, contribute significantly to the sugar industry. The food and beverage industry is the primary consumer of industrial sugar, utilizing it in the production of various processed foods, confectionery, and beverages. Additionally, the pharmaceutical and cosmetic sectors also demand industrial sugar in substantial quantities. Sugar factories and refineries employ advanced technology and sugar extraction methods to maximize sugar efficiency.

Sugar production processes include sugar crystallization, refining, and drying. Refined sugar, cane sugar, and beet sugar are the primary forms of sugar used in various industries. The confectionery industry, beverage industry, bakery industry, and dairy industry are significant consumers of sugar. Sugar derivatives and byproducts, such as sugar molasses, sugar beet pulp, and sugarcane bagasse, are utilized in various applications, including biofuel production and animal feed. Sugar regulations and certifications play a crucial role in ensuring sugar quality and sustainability. Sugar legislation and policy also impact the sugar market significantly. The pet food industry uses sugar syrup as an ingredient in various pet food products.

Sugar traceability is essential to maintain transparency and ensure food safety. Sugar prices fluctuate based on supply and demand dynamics. Sugar innovation continues to drive the market, with advancements in sugar technology and sugar processing methods. The biotech industry also contributes to sugar production through genetic modifications and bioprocessing techniques. The sugar industry's sustainability is a growing concern, with a focus on reducing sugar's environmental impact and improving sugar yield. Sugar ethanol is a promising area of research for the production of renewable energy. Overall, the market is dynamic and evolving, with various sectors and regions driving its growth and trends.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Industrial Sugar market drivers leading to the rise in the adoption of Industry?

- The primary factor fueling market growth is the increasing demand for raw sugar in various food and beverage applications. The global sugar market experiences steady growth due to the increasing consumption of sweetened foods and beverages. Sugarcane, the primary source of raw sugar, undergoes processing to produce this essential ingredient. The sugar industry's production and consumption are interconnected, with the demand for sugar significantly influencing its production. Raw sugar, derived from sugarcane, plays a pivotal role in the manufacturing of various sweetened products and beverages. Sugar processing involves several stages, including sugar drying, crystallization, refining, and storage. These processes ensure the production of high-quality sugar, which is crucial for maintaining the desired taste and texture in food and beverage applications.

- Moreover, sugar derivatives and byproducts, such as sugar alcohols and ethanol, are gaining popularity in the beverage industry and the biotech sector, further expanding the market's scope. The sugar traceability and quality standards have become increasingly important, emphasizing the need for efficient sugar processing and storage methods. The beverage industry's growth, driven by consumer preferences for sweetened drinks, fuels the demand for sugar. The sugar market's growth is underpinned by the increasing consumption of sweetened products and beverages, the expanding applications of sugar derivatives, and the need for efficient sugar processing and storage methods.

What are the Industrial Sugar market trends shaping the Industry?

- The increasing preference for raw sugar in beauty products represents a notable market trend. This trend reflects consumers' growing awareness and demand for natural and minimally processed ingredients in their personal care products. The market is driven by various factors, including sugar regulations and sugar certification. Strict sugar policies implemented by governments worldwide ensure that the production and trade of sugar adhere to specific standards, thereby increasing the demand for sugar certification. In the sugar industry, sugar production techniques such as sugar filtration and sugar fermentation are essential for maintaining sugar purity. Sugar is a crucial ingredient in various industries, including the bakery industry, where sugar sweetness is a key factor in the production of baked goods. Sugar ethanol, derived from sugarcane and sugar beet pulp, is another significant application of sugar, used as a biofuel in the energy sector.

- The sugar market is subject to fluctuations due to changes in sugar supply and demand. Cane sugar and beet sugar are the primary sources of sugar production, with sugarcane being the dominant source. The sugar trade is an essential component of the global economy, with various countries exporting and importing sugar based on their production capabilities and consumption needs. The market is a dynamic and essential industry, driven by various factors such as sugar regulations, sugar certification, sugar production techniques, and sugar applications in various industries. Understanding these market dynamics is crucial for businesses looking to invest or expand in the sugar industry. Recent research suggests that the market is expected to continue growing due to increasing demand for sugar in various industries and the ongoing development of new sugar production technologies.

How does Industrial Sugar market faces challenges face during its growth?

- The growth of the raw sugar industry is significantly influenced by government regulations governing production, processing, and sales. These regulations pose a significant challenge to industry expansion. Industrial sugar, derived from raw sugar, is subjected to stringent regulations to maintain consumer health and safety. In major sugar-producing countries, governments impose regulations covering sugar production, processing, and sales. These regulations aim to ensure raw sugar is free from harmful contaminants and adheres to safety standards. One significant policy is the Hazard Analysis and Critical Control Point (HACCP) system, a food safety management system that identifies and manages potential hazards in sugar production processes. The dairy industry is a significant consumer of sugar, with sugar applications including taste enhancement and preservation. Sugar demand is influenced by various factors, including sugar taste preferences, sugar packaging, and sustainability.

- Sugarcane juice and sugar beet juice are the primary sources of raw sugar, while sugar molasses feed is used as animal feed. Sugar sustainability is a growing concern, with an increasing focus on reducing sugarcane bagasse waste and improving refined sugar color. Sugar legislation continues to evolve, with a focus on transparency and traceability.

Exclusive Customer Landscape

The industrial sugar market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the industrial sugar market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, industrial sugar market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AGRANA Beteiligungs AG - The company specializes in providing high-quality industrial sugar solutions for the beverage and chemical industries.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AGRANA Beteiligungs AG

- American Crystal Sugar Co.

- Archer Daniels Midland Co.

- Associated British Foods Plc

- Balrampur Chini Mills Ltd.

- Cargill Inc.

- COSAN S.A.

- Dalmia Bharat Sugar and Industries Ltd.

- EID Parry India Ltd.

- Louis Dreyfus Co. BV

- Michigan Sugar Co.

- Mitr Phol Group

- Nordzucker AG

- Rogers Sugar Inc.

- Shree Renuka Sugars Ltd.

- Sudzucker AG

- Tate and Lyle PLC

- Tereos Participations

- Triveni Engineering and Industries Ltd.

- Wilmar International Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Industrial Sugar Market

- In February 2023, Archer-Daniels-Midland Company (ADM) announced the expansion of its sugar production capacity in Brazil by investing USD400 million. This strategic move aimed to strengthen ADM's position as a leading global supplier of industrial sugars (ADM Investor News, 2023).

- In May 2024, Tate & Lyle PLC, a leading provider of specialty food ingredients, entered into a strategic partnership with Bio-Techne Corporation. This collaboration focused on the development and commercialization of novel sweeteners derived from plant-based sources. The partnership was expected to expand Tate & Lyle's product portfolio and cater to the growing demand for natural and low-calorie sweeteners (Tate & Lyle Press Release, 2024).

- In October 2024, Sucden, a global commodities merchant and processor, acquired a 50% stake in the Brazilian sugar and ethanol producer, Usina São Martinho. This acquisition aimed to expand Sucden's presence in the Brazilian sugar market and provide access to the company's extensive sugarcane production and processing capabilities (Sucden Press Release, 2024).

- In January 2025, the European Union (EU) approved the renewal of sugar quotas for its member states. This decision aimed to maintain the stability of the EU sugar market and protect European sugar producers from global market volatility. The quota system would remain in place until 2030 (European Commission Press Release, 2025).

Research Analyst Overview

The market continues to evolve, driven by dynamic market dynamics and diverse applications across various sectors. Sugar cane juice and raw sugar undergo extensive processing to produce refined sugar, which is utilized in a multitude of industries. The dairy industry relies on sugar for flavor enhancement, while the confectionery sector uses it for texture and sweetness. Sugar demand is further fueled by the beverage industry, where it serves as a primary ingredient for sweetened beverages. Sugar packaging and standards play a crucial role in ensuring product quality and consumer safety. In the food and beverage industry, grape juice, cooking wines are used for gourmet cooking and in traditional food cultures. Innovations in sugar technology have led to advancements in sugar extraction and crystallization processes, increasing efficiency and reducing waste.

The Industrial Sugar Market is shaped by advancements in sugarcane cultivation and sugar beet cultivation, with efficient sugarcane harvesting and sugarcane transport optimizing supply chains. Similarly, sugar beet transport ensures a steady raw material flow. Cutting-edge sugar refining technology, alongside sugar automation and sugar robotics, boosts production efficiency. Enhanced sugar data analysis and sugar traceability systems improve monitoring, ensuring sugar quality control and precise sugar testing methods. Market trends reflect sugar price volatility and the need for accurate sugar demand forecasting. The industry's sugar environmental impact, sugar social impact, and sugar economic impact drive sustainability discussions. Rising interest in sugar-free products fuels innovation, meeting health-conscious consumer preferences while reshaping market dynamics.

Sugarcane bagasse and beet pulp are byproducts of sugar production, finding applications in the biofuel and animal feed industries. Sugar legislation and regulations continue to shape the market, with a focus on sustainability and traceability. Sugar molasses feed and sugar derivatives are gaining popularity due to their potential as sustainable alternatives to traditional fossil fuels. The biotech industry is exploring new possibilities for sugar applications, from sugar ethanol to sugar biofuel. Sugar prices and distribution patterns are subject to constant fluctuations, influenced by various factors such as weather conditions, production yields, and geopolitical events. The sugar industry's ongoing evolution reflects its adaptability to changing market demands and its commitment to innovation and sustainability.

Dive into Technavio's strong research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Industrial Sugar Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

208 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.2% |

|

Market growth 2025-2029 |

USD 13.84 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

4.9 |

|

Key countries |

India, US, China, Japan, Canada, France, UK, Germany, South Korea, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Industrial Sugar Market Research and Growth Report?

- CAGR of the Industrial Sugar industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the industrial sugar market growth of industry companies

We can help! Our analysts can customize this industrial sugar market research report to meet your requirements.

RIA -

RIA -