Enjoy complimentary customisation on priority with our Enterprise License!

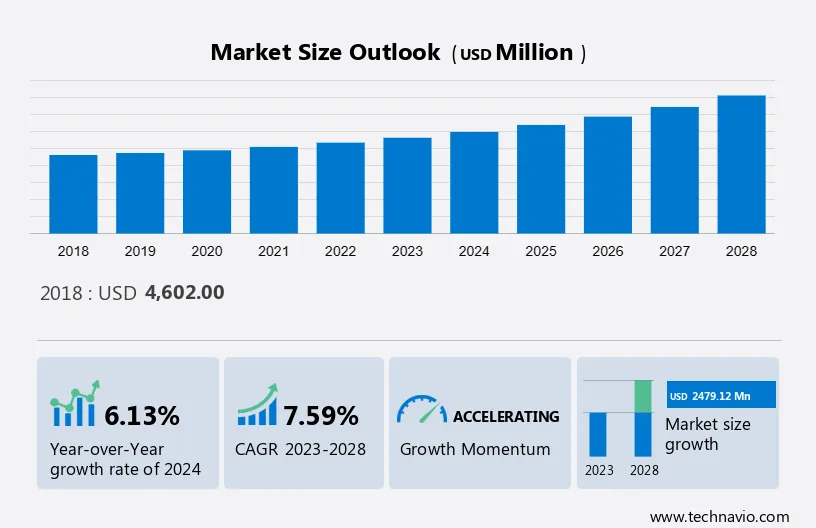

The industrial wireless automation market size is estimated to grow at a CAGR of 7.59% between 2023 and 2028. The market size is forecast to increase by USD 2,479.12 million. The growth of the market depends on several factors such as the integration of AI and ML with wireless automation, the growing adoption of high-speed communication network solutions for fast data transfer in the industrial sector and the increasing focus on predictive maintenance. Our report examines historic data from 2018 to 2022, besides analyzing the current market scenario.

This report extensively covers market segmentation by solution (field instrument and communication network), end-user (process industry and discrete industry), and geography (APAC, North America, Europe, Middle East and Africa, and South America). It also includes an in-depth analysis of drivers, trends, and challenges.

Industrial Wireless Automation Market Forecast 2024-2028

To learn more about this report, Request Free Sample

Our researchers studied the data for years, with 2022 as the base year and 2023 as the estimated year, and presented the key drivers, trends, and challenges for the market. Although there has been a disruption in the growth of the market during the COVID-19 pandemic, a holistic analysis of drivers, trends, and challenges will help companies refine marketing strategies to gain a competitive advantage.

The demand for IoT-enabled devices has increased significantly, primarily due to the need for data collection and analysis to solve complex maintenance tasks. IoT-enabled devices such as wireless acoustic transmitters and steam trap monitors are aiding in monitoring complete plant operations. With the available data regarding machines and systems, industrial operators can compare efficiency and performance. This helps operators plan maintenance accordingly and reduce the overall downtime caused by sudden machine failure. Hence, end-users have shifted their focus toward predictive maintenance, which helps in reducing overall production downtime and increases operational efficiency.

Consequently, monitoring of automation systems and instruments becomes a primary task for industrial operators. Wireless automation solution providers not only provide automation hardware and software but also focus on aftersales services software for plant and asset lifecycle management. This helps in predicting maintenance activities without affecting the manufacturing process and, in turn, will strengthen the global industrial automation market during the forecast period.

Wireless sensor networks (WSNs) are recognized as one of the most cost-effective and efficient mechanisms for collecting data in the industrial sector. WSNs consist of a number of inexpensive, small, and low-power-consuming devices called nodes, which work together by communicating with each other through a network. These sensors are gaining popularity in many diversified industries as they can be easily deployed and self-organized to achieve different purposes. WSNs are predominantly used in area monitoring, environmental monitoring, industrial monitoring, agriculture, home automation, and health care monitoring.

In addition, increasing flexibility in deploying industrial wireless sensor networks and their declining cost is encouraging end-users to install sensors in their factories and plants. Vendors are capitalizing on the availability of mobile, intelligent, and connected sensors to improve the capabilities of their offerings, which will boost the growth of the global industrial wireless automation market during the forecast period.

The cost of installing wireless communication devices is very high. Moreover, these devices should be proficient enough to withstand temperature and humidity extremes as well as exposure to vibrations, shocks, noise, electromagnetic interference, and others. The cost of an industrial wireless automation solution includes the cost of licensing, system design, implementation, and upgrades. Experts are required for the proper implementation and functioning of systems, and the integration of these applications with the existing operational processes can be quite challenging. Software licensing and hardware implementation, maintenance, customization, and training increase the total cost for the buyer. Industrial operators that purchase these wireless solutions also require trained IT professionals.

Moreover, after the implementation, the software and hardware need to be upgraded regularly to keep pace with the current market trends. The above-mentioned factors will lead to an increase in the implementation and maintenance costs of software and hardware, which will hinder the growth of the global industrial wireless automation market during the forecast period.

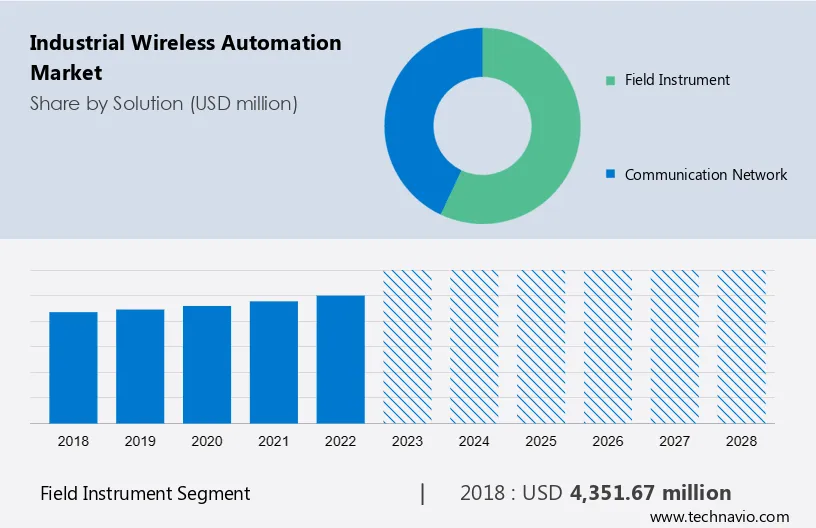

The market share growth of the field instrument segment will be significant during the forecast period. The demand for field instruments has increased significantly from both discrete and process industries. Field instruments mainly include sensors, transducers, and transmitters. These instruments aim to control and monitor various conditions such as temperature, pressure, and fluid levels in processing facilities, oil and gas pipelines, petrochemical plants, oil refineries, and other distribution operations.

Get a Customised Report as per your requirements for FREE!

The field instrument segment was valued at USD 4,351,67 million in 2017 and continue to grow by 2021. Industrial wireless sensors are extensively used in industrial process applications for measuring, monitoring, testing, scaling, and automation. The increasing use of IIoT has introduced new growth opportunities for vendors. Major end-users, such as industrial manufacturing, energy, and others, understand that improved data management drives down additional operational costs, which makes them more productive. These factors will contribute to the growth of the field instrument, which will enhance the global industrial wireless automation market during the forecast period.

For more insights on the market share of various regions View PDF Sample now!

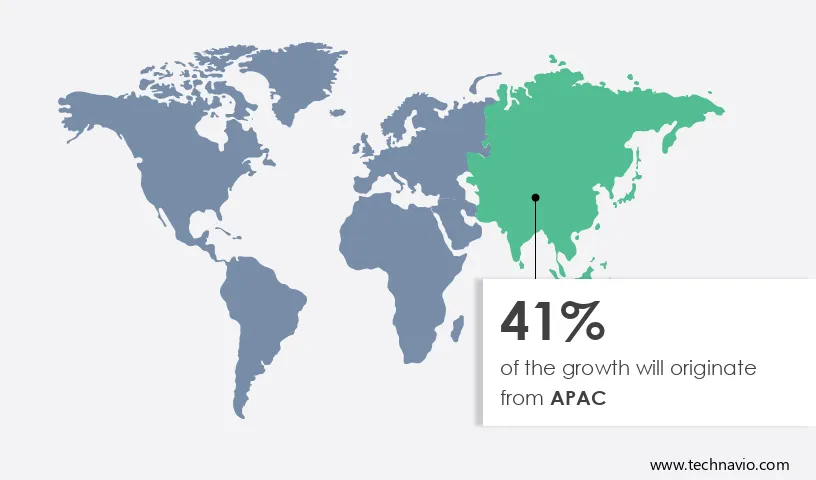

APAC is estimated to contribute 41% to the growth by 2027. Technavio’s analysts have elaborately explained the regional trends, drivers, and challenges that are expected to shape the market during the forecast period. There has been an increase in preference for wireless automation solutions to simplify complex production processes and improve operational efficiency among manufacturers in APAC. This is contributing to the growth of the market in APAC. With the increase in the scale of operations, the supply chain becomes complex. Therefore, established vendors are partnering with system integrators to provide automation services to increase their market reach. The high demand for energy is resulting in the commencement of several oil and gas projects in APAC.

Moreover, while downstream projects account for a significant share of oil and gas investments, several midstream projects are under development. The demand for industrial wireless automation will be led by liquefied natural gas (LNG) processing and pipeline transportation-related activities. Furthermore, in March 2021, the Indian Government announced an investment of USD 82 billion by 2035 in port projects and infrastructure. Hence, these factors are expected to create opportunities for the growth of the market in focus in the region during the forecast period.

The outbreak of COVID-19 in 2020 adversely affected the growth of the industrial sector in APAC. However, with the initiation of vaccination drives across APAC, the lockdown norms were relaxed in the second half of 2020. Moreover, the healthcare and pharmaceutical industries in APAC are expanding rapidly, driving the demand for automation in drug manufacturing, healthcare delivery, and medical device production. It will aid in many processes, including business management to plant operations. The healthcare and pharmaceutical industries in APAC are expanding rapidly, driving the demand for automation in drug manufacturing, healthcare delivery, and medical device production. These factors are expected to boost the growth of the industrial wireless automation market in APAC during the forecast period.

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

ABB Ltd. - The company offers industrial wireless automation such as ABB WirelessHART, enabling remote monitoring and control in industrial settings.

We also have detailed analyses of the market’s competitive landscape and offer information on 20 market companies, including:

ABB Ltd., Beijer Electronics Group AB, Belden Inc., Cisco Systems Inc., CommScope Holding Co. Inc., Eaton Corp. Plc, FANUC Corp., General Electric Co., Honeywell International Inc., Mitsubishi Electric Corp., Motorola Solutions Inc., Moxa Inc., OleumTech Corp., OMRON Corp., Phoenix Contact GmbH and Co. KG, Rockwell Automation Inc., Schneider Electric SE, Siemens AG, Yokogawa Electric Corp., and Emerson Electric Co.

Technavio report provides an in-depth analysis of the market and its players through combined qualitative and quantitative data. The analysis classifies companies into categories based on their business approaches, including pure-play, category-focused, industry-focused, and diversified. Companies are specially categorized into dominant, leading, strong, tentative, and weak, based on their quantitative data analysis.

The industrial wireless automation market report forecasts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and growth opportunities from 2018 to 2028.

|

Industrial Wireless Automation Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

173 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.59% |

|

Market Growth 2024-2028 |

USD 2,479.12 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.13 |

|

Regional analysis |

APAC, North America, Europe, Middle East and Africa, and South America |

|

Performing market contribution |

APAC at 41% |

|

Key countries |

US, China, Japan, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

ABB Ltd., Beijer Electronics Group AB, Belden Inc., Cisco Systems Inc., CommScope Holding Co. Inc., Eaton Corp. Plc, FANUC Corp., General Electric Co., Honeywell International Inc., Mitsubishi Electric Corp., Motorola Solutions Inc., Moxa Inc., OleumTech Corp., OMRON Corp., Phoenix Contact GmbH and Co. KG, Rockwell Automation Inc., Schneider Electric SE, Siemens AG, Yokogawa Electric Corp., and Emerson Electric Co. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for the forecast period. |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Solution

7 Market Segmentation by End-user

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights