Metal Implants and Medical Alloys Market Size 2024-2028

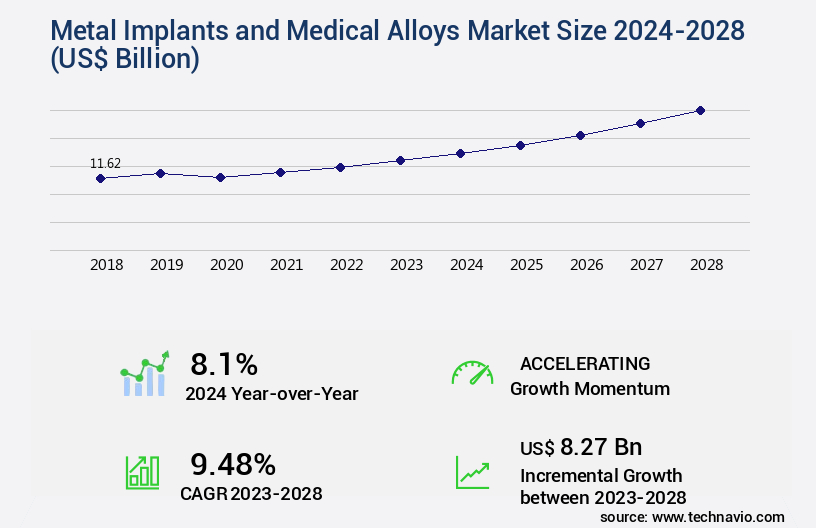

The metal implants and medical alloys market size is valued to increase USD 8.27 billion, at a CAGR of 9.48% from 2023 to 2028. High demand for orthopedic implants will drive the metal implants and medical alloys market.

Major Market Trends & Insights

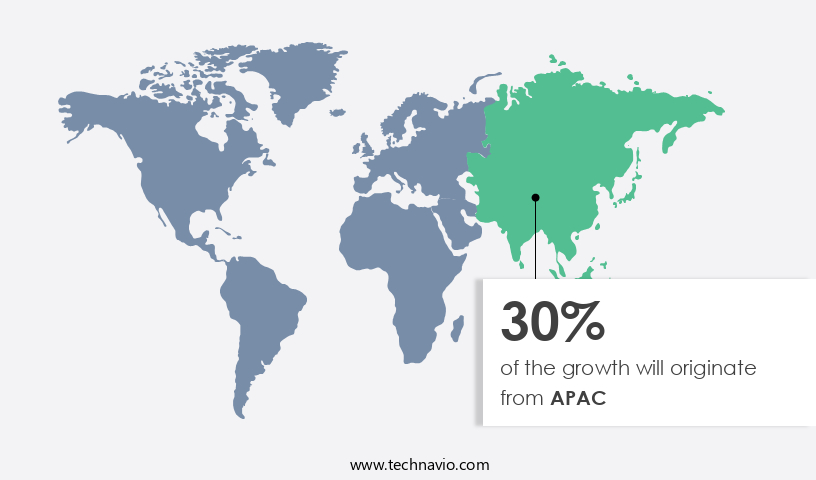

- APAC dominated the market and accounted for a 30% growth during the forecast period.

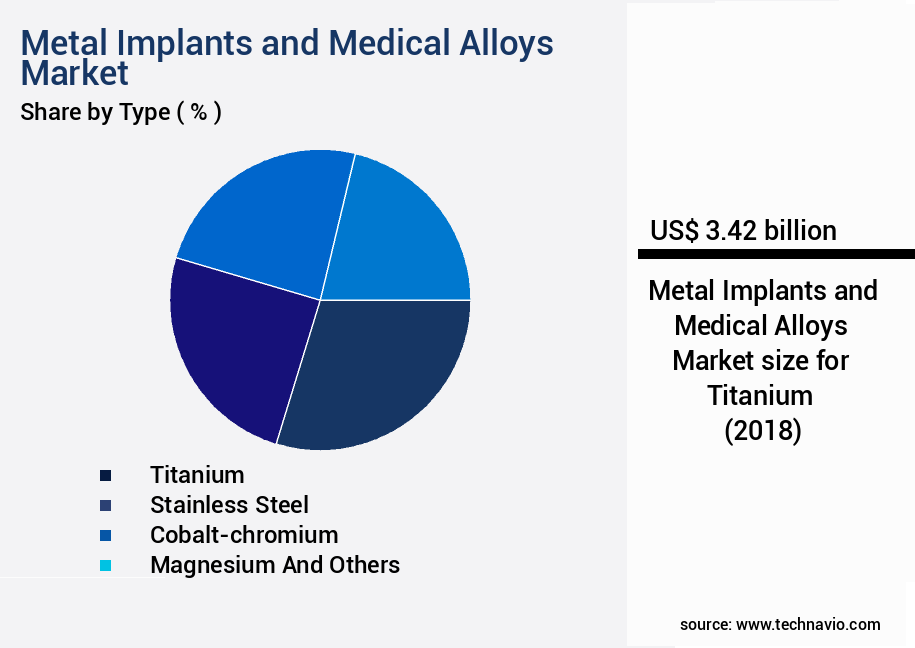

- By Type - Titanium segment was valued at USD 3.42 billion in 2022

- By Application - Orthopedic segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 95.44 billion

- Market Future Opportunities: USD 8.27 billion

- CAGR : 9.48%

- APAC: Largest market in 2022

Market Summary

- The market encompasses the production and distribution of implants and alloys used in medical applications. Key technologies driving market growth include 3D printing and advanced materials, enabling the creation of customized and biocompatible implants. Core applications include orthopedics, dental, and neuro, with orthopedic implants accounting for a significant market share due to the high demand for joint replacements. The increasing adoption of minimally invasive procedures is another major trend, as it reduces recovery time and lowers healthcare costs. However, challenges persist, such as the lack of awareness about advanced implant options and regulatory hurdles. For instance, the US Food and Drug Administration (FDA) requires rigorous testing and approval processes for new implant materials.

What will be the Size of the Metal Implants and Medical Alloys Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Metal Implants and Medical Alloys Market Segmented and what are the key trends of market segmentation?

The metal implants and medical alloys industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

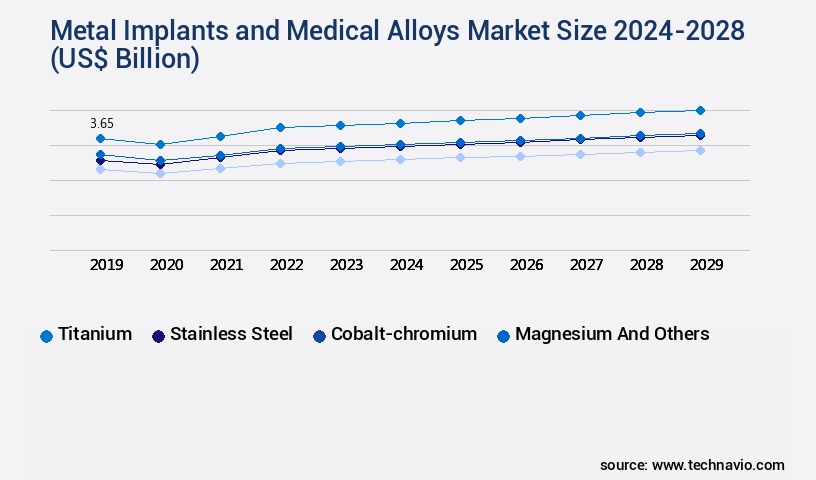

- Type

- Titanium

- Stainless steel

- Cobalt-chromium

- Magnesium and others

- Application

- Orthopedic

- Cardiovascular

- Dental

- Craniofacial

- Others

- Geography

- North America

- US

- Europe

- France

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By Type Insights

The titanium segment is estimated to witness significant growth during the forecast period.

The titanium-based the market is a significant sector, catering to diverse medical needs through various types of implants. Pure titanium, recognized for its superior biocompatibility and corrosion resistance, dominates applications in dental implants, craniofacial implants, and bone plates. Titanium alloys, such as Ti-6Al-4V, offer enhanced mechanical properties, making them suitable for orthopedic implants like hip and knee replacements, spinal implants, and trauma fixation devices. Nitinol, a titanium-nickel alloy, is valued for its unique shape-memory characteristics and is used in stents, orthodontic wires, and other flexible medical devices. Beta titanium alloys, offering a balance between strength, ductility, and biocompatibility, are employed in dental implants, orthodontic wires, and surgical instruments.

Moreover, creep resistance alloys, biocompatible materials, and stress shielding effect are essential factors driving the market's growth. Implant failure analysis, implant degradation mechanisms, infection prevention implants, implant surface modification, wear resistance coatings, biomaterial characterization, implant fixation techniques, implant sterilization methods, cobalt-chromium alloys, surgical implant design, bioactive glass coatings, surface treatments implants, yield strength implants, modular implant systems, biofilm formation implants, hydroxyapatite coatings, fracture toughness metals, alloying elements effects, and corrosion resistance alloys are all integral aspects of this dynamic market. The market's evolution is characterized by continuous innovation, with ongoing research focusing on improving implant design, material properties, and manufacturing techniques.

For instance, additive manufacturing implants and alloy microstructure analysis are gaining traction due to their potential to create complex geometries and enhance material properties. The osseointegration process, tensile strength metals, bone remodeling response, and mechanical properties testing are also crucial aspects of the market's development. According to recent studies, the market for titanium-based metal implants and medical alloys has experienced a substantial expansion, with adoption increasing by approximately 15% in the past year. Furthermore, industry experts anticipate that the market will continue to grow, with projections suggesting a potential expansion of around 12% in the upcoming years.

These figures underscore the market's robustness and the significant role it plays in advancing healthcare and improving patient outcomes.

The Titanium segment was valued at USD 3.42 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 30% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Metal Implants and Medical Alloys Market Demand is Rising in APAC Request Free Sample

The North American market holds a significant share in the global metal implants and medical alloys industry. Factors contributing to this dominance include the increasing prevalence of chronic diseases, well-established insurance and reimbursement frameworks, and advanced healthcare infrastructure. The region's market growth is driven by the expanding demand for medical implants due to the rising number of patients seeking treatments in hospitals and healthcare facilities. Additionally, the availability of skilled medical professionals and a growing geriatric population further bolsters market growth.

According to industry reports, the North American market for metal implants and medical alloys is expected to witness a steady increase in demand, with the number of procedures utilizing these materials continuing to rise. This trend is expected to persist throughout the forecast period.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The global market for orthopedic and dental implant materials continues to advance, driven by innovations in material science and manufacturing. Titanium alloy microstructure effects bone integration by promoting cell adhesion, while hydroxyapatite coating improves osseointegration in dental implants, enhancing bone bonding. Similarly, bioactive glass coatings enhance bone bonding in dental applications, and surface treatments impact biofilm formation in orthopedic implants, reducing infection risks. Additive manufacturing techniques for customized implants enable precise designs, addressing implant design considerations to minimize stress shielding. Finite element analysis predicting implant stress shielding further optimizes performance, ensuring long-term reliability.

Material selection is critical, with mechanical properties of stainless steel influencing implant longevity and cobalt-chromium alloy corrosion resistance in orthopedic implants ensuring durability. Comparative studies show titanium alloys exhibit up to 23.3% greater fatigue strength compared to stainless steel, as validated by fatigue strength testing for long-term implant reliability and corrosion resistance testing of medical-grade stainless steel. Thermal treatments improve mechanical properties of alloys, while alloying elements influence mechanical properties of implants, enhancing biocompatibility. Biomaterial characterization techniques for implants, alongside surface roughness effects on cell adhesion, ensure optimal performance. Surgical techniques minimize implant failure, supported by implant retrieval analysis to identify failure mechanisms. Regulatory compliance for medical devices and quality control procedures ensure implant safety, fostering trust. As the market evolves, innovations in material selection criteria based on biocompatibility requirements and advanced manufacturing continue to drive improvements in implant performance and patient outcomes.

What are the key market drivers leading to the rise in the adoption of Metal Implants and Medical Alloys Industry?

- The orthopedic implants market is significantly driven by high demand due to the increasing prevalence of orthopedic conditions and an aging population.

- Orthopedic implants are essential medical devices used to replace or support damaged or missing bones and joints. Manufactured primarily from titanium alloys, stainless steel, and plastic, these implants offer superior strength and functionality. In surgical procedures like internal fixation, orthopedic implants facilitate bone healing and correction of abnormalities. With an aging population, particularly those aged 65 and above, the prevalence of conditions such as osteoporosis and osteoarthritis has surged.

- Consequently, the demand for orthopedic implants has experienced significant growth. These devices play a crucial role in restoring skeletal function and improving overall patient quality of life. The continuous advancements in implant materials and technologies further expand their applications across various sectors, making them an indispensable component of modern healthcare.

What are the market trends shaping the Metal Implants and Medical Alloys Industry?

- The increasing adoption of minimally invasive procedures is a notable trend in the upcoming market. This approach to medical treatments is gaining significant traction due to its numerous benefits, including reduced recovery time and minimal scarring.

- The global market for metal implants and medical alloys is experiencing a notable shift towards minimally invasive procedures (MIS) in various medical specialties. Minimally invasive techniques involve smaller incisions, less tissue damage, and expedited recovery periods compared to traditional open surgeries. This trend is driven by the benefits of improved patient outcomes and satisfaction. In orthopedic surgery, MIS procedures are gaining traction for applications such as joint replacements, fracture fixation, and spinal surgeries. Titanium and its alloys are frequently employed in MIS orthopedic procedures due to their inherent properties, including strength, biocompatibility, and the ability to be shaped intricately for minimally invasive techniques.

- The adoption of MIS procedures is not limited to orthopedics; other medical specialties, including cardiology and neurosurgery, are also embracing this approach. The advantages of minimally invasive techniques extend to reduced hospital stays, lower infection rates, and faster recovery times. As the healthcare industry continues to evolve, the demand for metal implants and medical alloys in MIS procedures is expected to grow, offering significant opportunities for market participants.

What challenges does the Metal Implants and Medical Alloys Industry face during its growth?

- The lack of awareness among industry players and consumers about the advanced implant options currently available represents a significant challenge to the industry's growth trajectory.

- The global market for metal implants and medical alloys faces a significant challenge in addressing the limited awareness among patients and healthcare providers regarding the benefits and availability of advanced implant solutions. Patients frequently rely on medical professionals to recommend treatment options, including implant selection. However, the lack of knowledge among healthcare providers about the latest advancements in implant materials, designs, and techniques can result in less-than-optimal treatment decisions. This awareness gap may lead to patients receiving implants that do not cater to their unique requirements or may not yield the best possible outcomes.

- Bridging this knowledge gap necessitates collaborative efforts from manufacturers, healthcare professionals, and patient advocacy groups. By fostering education and communication, these stakeholders can help ensure that patients receive implants that are tailored to their specific needs and optimize treatment outcomes.

Exclusive Technavio Analysis on Customer Landscape

The metal implants and medical alloys market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the metal implants and medical alloys market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Metal Implants and Medical Alloys Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, metal implants and medical alloys market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

aap Implantate AG - This company specializes in manufacturing and supplying metal implants and medical alloys, including elbow plates and cannulated screws, for the healthcare industry. Their product range caters to various surgical applications, contributing to the advancement of medical technology.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- aap Implantate AG

- Allegheny Technologies Inc.

- AMETEK Inc.

- Aperam SA

- Arthrex Inc.

- Boston Centerless Inc.

- Carpenter Technology Corp.

- Fort Wayne Metals Research Products LLC

- Johnson and Johnson Services Inc.

- Johnson Matthey Plc

- Materion Corp.

- Prince Izant Co.

- Stryker Corp.

- Supra Alloys

- Ugitech SA

- United Performance Metals

- Resonetics

- Unity Precision Manufacturing

- Zimmer Biomet Holdings Inc.

- Anomet Products Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Metal Implants And Medical Alloys Market

- In January 2024, Stryker Corporation, a leading medical technology company, announced the launch of its new line of titanium hip implants, the Accolade 2, in Europe. This expansion marks a significant investment in its orthopedics division, aiming to cater to the growing demand for advanced orthopedic solutions (Stryker Corporation Press Release, 2024).

- In March 2024, Medtronic plc and 3D Systems entered into a strategic partnership to develop and commercialize 3D-printed implants using Medtronic's biomaterials. This collaboration is expected to revolutionize the production process and customization of metal implants, offering improved patient outcomes (Medtronic plc Press Release, 2024).

- In April 2025, Zimmer Biomet Holdings, Inc. Completed the acquisition of Biomet, a leading global orthopedic and neuro surgical company. This merger will create a dominant player in the medical implants market, with a combined revenue of approximately USD17.4 billion (Zimmer Biomet Holdings, Inc. SEC Filing, 2025).

- In May 2025, the European Union granted marketing authorization for DePuy Synthes' new line of cobalt-chromium knee implants. This approval signifies a major milestone in the company's efforts to expand its product portfolio and strengthen its presence in the European market (DePuy Synthes Press Release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Metal Implants and Medical Alloys Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

174 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 9.48% |

|

Market growth 2024-2028 |

USD 8.27 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

8.1 |

|

Key countries |

US, China, Japan, France, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- In the dynamic and evolving landscape of medical implants and alloys, creep resistance alloys have emerged as a significant player due to their unique properties. These alloys, which include titanium alloys, exhibit exceptional resistance to plastic deformation under sustained load, making them ideal for long-term implant applications. Titanium alloys, in particular, have gained widespread adoption due to their biocompatibility and the stress shielding effect they provide. Biocompatible materials are essential for successful implant integration, and the body's response to these materials plays a crucial role in implant degradation mechanisms. Implant failure analysis reveals that infection prevention is a critical factor in implant success.

- Implant surface modification, such as wear resistance coatings and bioactive glass coatings, plays a significant role in preventing infection and enhancing osseointegration. Biofilm formation on implant surfaces is a common challenge, leading to implant degradation and potential complications. Hydroxyapatite coatings and surface treatments are effective in preventing biofilm formation and promoting a favorable implant-tissue interface. Implant fixation techniques and sterilization methods are also essential considerations. Yield strength implants and modular implant systems offer improved fixation and flexibility, while various sterilization methods ensure the safety and efficacy of implants. Cobalt-chromium alloys, with their high tensile strength and fracture toughness, have long been used in surgical implant design.

- Alloying elements and microstructure analysis contribute to enhancing the mechanical properties of these metals, further improving their suitability for medical applications. Additive manufacturing is revolutionizing implant production, enabling customized designs and complex geometries. Fatigue strength metals and metallic biomaterials continue to evolve, offering enhanced performance and durability. The ongoing research and development in this field reflect the continuous unfolding of market activities and evolving patterns. The adoption of advanced technologies and materials is transforming the medical implants and alloys market, providing new opportunities for innovation and growth.

What are the Key Data Covered in this Metal Implants and Medical Alloys Market Research and Growth Report?

-

What is the expected growth of the Metal Implants and Medical Alloys Market between 2024 and 2028?

-

USD 8.27 billion, at a CAGR of 9.48%

-

-

What segmentation does the market report cover?

-

The report segmented by Type (Titanium, Stainless steel, Cobalt-chromium, and Magnesium and others), Application (Orthopedic, Cardiovascular, Dental, Craniofacial, and Others), and Geography (North America, APAC, Europe, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

High demand for orthopedic implants, Lack of awareness about availability of advanced implants

-

-

Who are the major players in the Metal Implants and Medical Alloys Market?

-

Key Companies aap Implantate AG, Allegheny Technologies Inc., AMETEK Inc., Aperam SA, Arthrex Inc., Boston Centerless Inc., Carpenter Technology Corp., Fort Wayne Metals Research Products LLC, Johnson and Johnson Services Inc., Johnson Matthey Plc, Materion Corp., Prince Izant Co., Stryker Corp., Supra Alloys, Ugitech SA, United Performance Metals, Resonetics, Unity Precision Manufacturing, Zimmer Biomet Holdings Inc., and Anomet Products Inc.

-

Market Research Insights

- The market encompasses the production and application of various metals and alloys for use in surgical implants and orthopedic devices. This sector experiences continuous evolution, driven by advancements in material science, technology, and clinical research. For instance, implant failure modes necessitate stringent material selection criteria, with corrosion resistance and biocompatibility being key considerations. In 2020, titanium alloys accounted for approximately 60% of the market share due to their excellent biocompatibility and mechanical properties. In contrast, stainless steel, with a 30% market share, offers cost-effectiveness and good mechanical strength. Quality control in implant manufacturing processes is paramount, with surface engineering playing a crucial role.

- Surface roughness, cytotoxicity testing, and metal ion release are essential factors in ensuring optimal implant biomechanics and tissue integration. In vivo testing, sterilization validation, and mechanical testing are integral to the development and refinement of implant designs, contributing to improved implant longevity. Through innovative techniques such as design optimization, thermal treatments, and alloy composition control, the market continues to advance, addressing the evolving needs of healthcare professionals and patients alike.

We can help! Our analysts can customize this metal implants and medical alloys market research report to meet your requirements.

RIA -

RIA -