Enjoy complimentary customisation on priority with our Enterprise License!

The Mini Data Center Market is estimated to grow by USD 5,843.99 million accelerating at a CAGR of 18.17% between 2022 and 2027.

Traditional data centers face high-energy consumption and rising operational expenses, while mini data centers offer a more energy-efficient solution with a PUE rating of around 1.1. Equipped with energy-efficient cooling units, these modules significantly reduce power consumption. With increasing adoption and N+1 redundancy, mini data centers are ideal for disaster recovery without business interruption.

This report extensively covers market segmentation by type (containerized data centers and micro data centers), Business segment (SMEs and large enterprises), and geography (North America, APAC, Europe, South America, and Middle East and Africa). It also includes an in-depth analysis of drivers, trends, and challenges. Furthermore, the report includes historic market data from 2017 to 2021.

To learn more about this report, Download Report Sample

The reports categorize the global mini data center market as a part of the global Internet services and infrastructure market within the global IT services market. The super parent global IT services market cover companies offering IT consulting and system integration services, application services, electronic data processing services, business process outsourcing services, infrastructure services, and Internet services. Our research report has extensively covered external factors influencing the parent market growth during the forecast period.

The increased deployment of VDI is notably driving the market growth, although factors such as operational limitations may impede the market growth. Our researchers analyzed the data with 2022 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Key Mini Data Center Market Driver

The increased deployment of VDI is notably driving the market growth. Virtual Desktop Infrastructure (VDI) is transforming the IT workspace. Many companies around the world are busy implementing VDI solutions to facilitate flexibility in the workplace. The largest users of VDI solutions are healthcare, BFSI, and education.

The emergence of converged infrastructure solutions and mini-data centers offers all SMEs the opportunity to implement mini-data centers with a unified IT infrastructure. This includes creating servers, storage, and networking to host multiple virtual machines in the same office building (rather than building data centers or co-locating existing data centers). Such an infrastructure can also be hosted in a small data center environment.

During the forecast period, VDIs may consider the advantages of small data centers for internal VDI deployments. This will help grow the market.

Significant Mini Data Center Market Trend

The growing need for edge computing is the key trend in the market. Edge computing is an architectural model in which data produced by IoT devices is processed at the edge of the network, which is primarily located near the data source. The number of Internet devices is estimated to grow to 11.7 billion in 2020, giving a significant boost to the global data center market. The use of RFID sensors to tag, track, connect, and read objects in logistics and warehouses in the late 1990s popularized the IoT concept. The ever-increasing number of connected devices leads to the generation of large volumes of data. At the same time, ideas like the grid car, connected home, connected health, and smart cities are gaining ground.

Many industries such as manufacturing, utilities, retail, automotive and social media are using IoT to augment data. By the end of 2021, IoT-enabled devices will increase data center traffic by about 40 times. The growing number of IoT-enabled devices is creating a need for edge computing services. Commercial deployment of 5G will also provide a significant boost to the market by the end of the forecast period.

Major Mini Data Center Market Challenge

Operational limitations are the major challenge impeding market growth. The focus of data center operators is on improving power density at the rack level by using high-performance computing infrastructure. Many mega data center racks have a thermal density of 20 kW to 25 kW. However, micro data center modules have limited support for such a high-performance infrastructure. This is because as the power density increases, power and cooling requirements increase. Using an efficient computing infrastructure with inadequate power and cooling systems leads to equipment failures that disrupt business continuity. Disaster recovery modules must be able to sustain operations during outages and failures without compromising performance.

Key Mini Data Center Market Customer Landscape

The report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Global Mini Data Center Market Customer Landscape

Vendors are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Vertiv Holdings - The company offers mini data centers and related solutions such as Smart Row as its key offerings. Its operation in the Americas includes products and services sold for applications within the data center, communication networks, and commercial/industrial markets in North America and Latin America.

The report also includes detailed analyses of the competitive landscape of the market and information about 15 market vendors, including:

Qualitative and quantitative analysis of vendors has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize vendors as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize vendors as dominant, leading, strong, tentative, and weak.

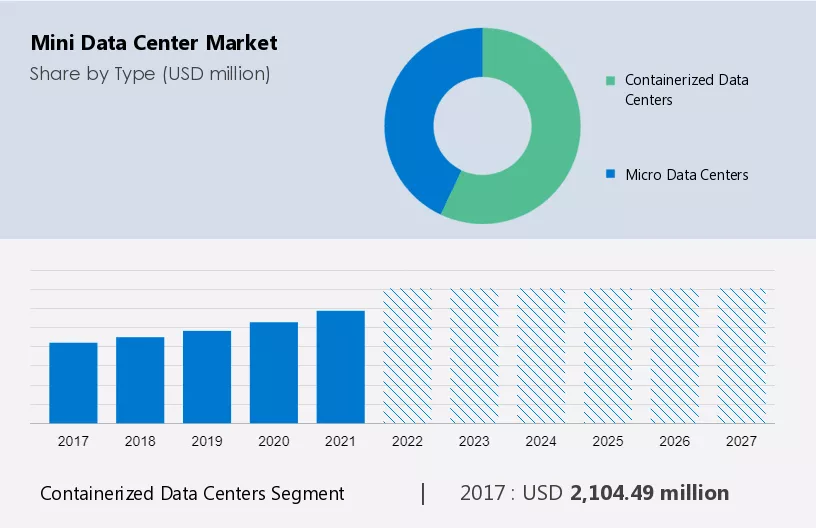

The market share growth of the containerized segment will be significant during the forecast period. Container data centers are the main support for future enterprises, providing the ability to use edge computing and disaster recovery. Businesses become competitive and want to expand to get more profit. The capacity of currently operating data centers will likely be depleted to make future business operations more efficient. Digital content produced by electronic devices is also exploding, increasing the need for reliable data center infrastructure with strong storage and processing power.

Get a glance at the market contribution of various segments Request a PDF Sample

The containerized segment was valued at USD 2,104.49 million in 2017 and continued to grow until 2021. These containerized data centers are more efficient and environmentally friendly in terms of energy consumption when compared to traditional facilities. Deploying these solutions also helps reduce capital expenditures and OPEX costs, which facilitates ease of installation and portability. Construction of these facilities with pre-installed infrastructure takes -6 months. Therefore, these benefits increase the adoption rate of these devices and help companies achieve business continuity.

For more insights on the market share of various regions Request PDF Sample now!

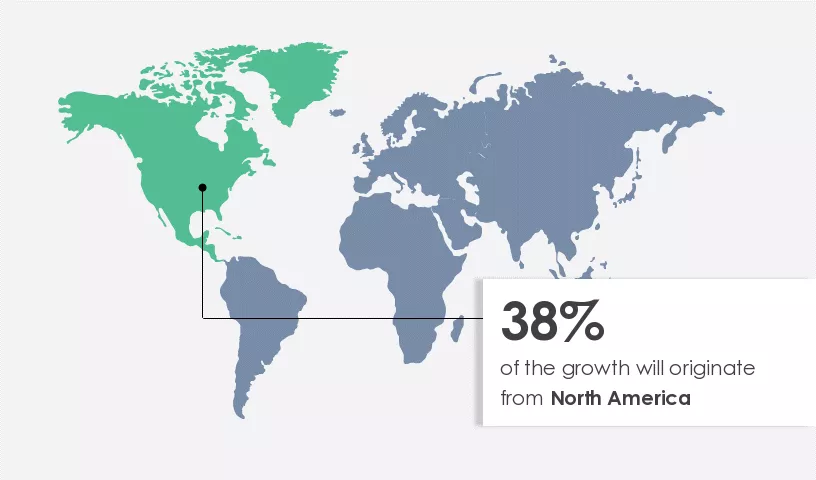

North America is estimated to contribute 38% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

Traditional data centers continue to grow in the United States, and mini data centers are being deployed in branch office environments. These mini data centers are primarily used by US government agencies and have recently spread to various industries such as healthcare. Infrastructure vendors such as HPE and Emerson Network Power may see market share during the forecast period. As the construction of modular data center facilities increases and awareness grows, these mini data centers will soon replace SMB server rooms. They are likely to see increased usage in sectors such as healthcare, education, and BFSI.

The outbreak of COVID-19 in 2020 propelled the market growth of cloud data centers in North America. Moreover, the companies realized the need for cloud-based solutions, as retail companies, enterprises, and consumers in this region are shifting toward using cloud-based software solutions. This is one of the major factors that have led to an increase in the need for mini-data centers. In addition, the rise in digitalization and innovations in the manufacturing sector are fueling the demand for mini-data centers in the region. Therefore, the mini data center market in the North American region is expected to witness a high growth rate during the forecast period.

The report forecasts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and growth opportunities from 2017 to 2027. The market has been segmented by Type (Containerized data centers and Micro data centers), Business Segment (SMEs and Large enterprises), and Geography (North America, APAC, Europe, South America, and the Middle East and Africa).

|

Mini Data Center Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

167 |

|

Base year |

2022 |

|

Historic period |

2017-2021 |

|

Forecast period |

2023-2027 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 18.17% |

|

Market growth 2023-2027 |

USD 5,843.99 million |

|

Market structure |

Fragmented |

|

YoY growth 2022-2023(%) |

16.11 |

|

Regional analysis |

North America, APAC, Europe, South America, and Middle East and Africa |

|

Performing market contribution |

North America at 38% |

|

Key countries |

US, China, Japan, UK, and Germany |

|

Competitive landscape |

Leading Vendors, Market Positioning of Vendors, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

CANCOM SE, Cannon Technologies Ltd., Canovate Group, Dataracks, Dell Technologies Inc., Eaton Corp. Plc, Gardner DC Solutions Ltd, Hanley Energy Ltd., Hewlett Packard Enterprise Co., Huawei Technologies Co. Ltd., International Business Machines Corp., Inspur Group, Legrand SA, Minkels B.V., Panduit Corp., Rahi, Rittal GmbH and Co. KG, ScaleMatrix Holdings Inc., Schneider Electric SE, and Vertiv Holdings Co. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, and Market condition analysis for the forecast period. |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this report to meet your requirements. Get in touch

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Type

7 Market Segmentation by Business Segment

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights