Potato Starch Market Size 2024-2028

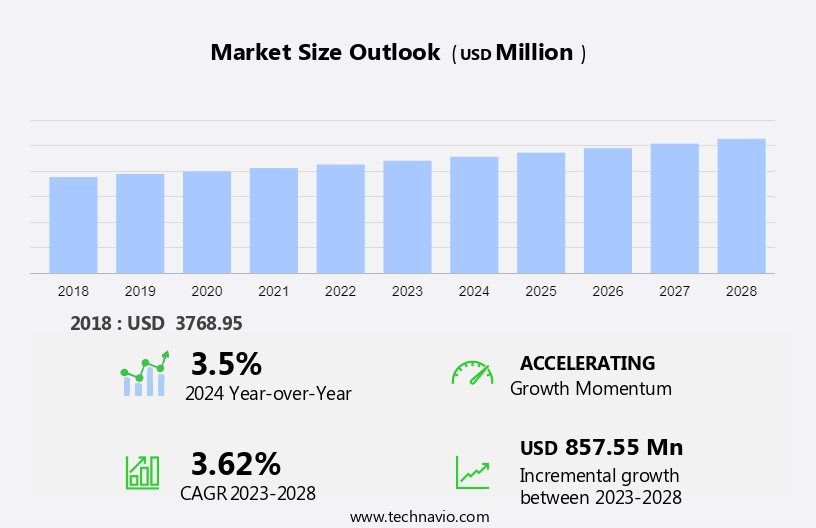

The potato starch market size is forecast to increase by USD 857.55 million at a CAGR of 3.62% between 2023 and 2028. The market is witnessing significant growth due to the increasing use of potato starch as a natural additive in various food applications, particularly in sauces, soups, and gluten-free products. The rising trend of environmental sustainability and consumer preference for veganism and vegetarian diets are driving the demand for clean-label products, making potato starch an attractive alternative to synthetic additives.

Additionally, potato starch's ability to act as a binding agent and thickener in various food applications, coupled with its cost-effectiveness, makes it a preferred choice in the global food industry. Furthermore, the increasing awareness of health and nutrition has led to the popularity of nutritious and organic starch, providing opportunities for market growth. Despite these opportunities, the availability of substitutes for potato starch and the challenge of maintaining consistent quality may hinder market growth.

Potato starch, derived from the processing of potato tubers, is a versatile functional ingredient with applications in various industries. It is a popular alternative to tapioca starch, coconut flour, rice flour, and cassava roots, due to its superior binding and thickening properties. In the food industry, potato starch is extensively used in the production of bioplastics, cereals, noodles, soups, sauces, canned vegetables, meat, snacks, confectioneries, dry mixes, extruded food products, pet foods, and animal nutrition. Additionally, it serves as a crucial ingredient in microbial enzymes and industrial enzymes. Beyond food applications, potato starch finds significant use in the detergent industry, feed industry, and wastewater treatment industry. It is also employed in the production of biodegradable plastics, contributing to the growth of the European Bioplastics market. Moreover, potato starch is a natural, gluten-free alternative, making it suitable for use in textiles industry and various other applications. The increasing demand for natural and biodegradable products is expected to boost the market growth for potato starch in the coming years.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD Million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Conventional

- Organic

- End-user

- Food and beverages

- Paper industry

- Pharmaceuticals

- Animal feed

- Others

- Geography

- Europe

- Germany

- France

- North America

- US

- APAC

- China

- South America

- Middle East and Africa

- Europe

By Type Insights

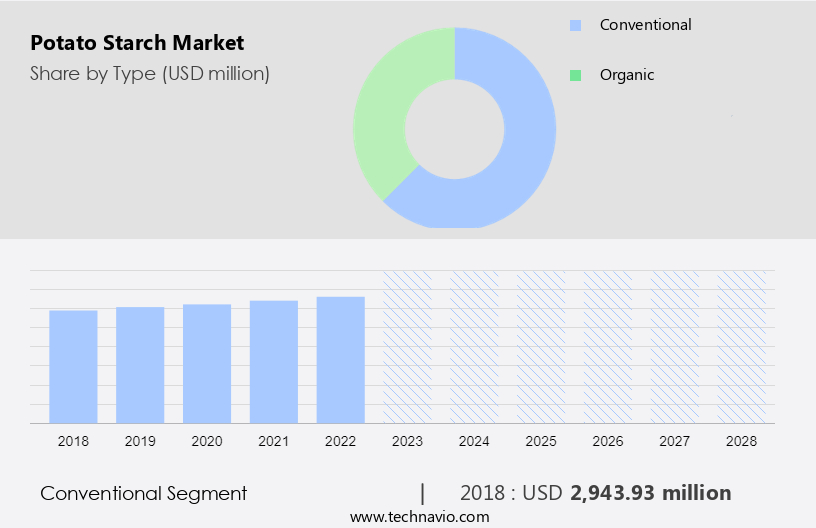

The conventional segment is estimated to witness significant growth during the forecast period. The market encompasses various applications, including confectioneries, dry mixes, and extruded food products. In the confectionery industry, potato starch serves as a vital thickening agent, while in dry mixes, it acts as a binding agent. In the production of pet foods and animal nutrition, potato starch functions as a source of dietary fiber and energy. Furthermore, potato starch finds application in the manufacturing of microbial and industrial enzymes, detergents, and feed industries. Additionally, it is used in the production of biodegradable plastics, aerobic composting, and as a soil improver. The conventional potato starch segment caters to the demand for affordable starch derived from potatoes grown using conventional agricultural practices, which may include the use of synthetic pesticides, chemical fertilizers, and genetically modified foods. Despite concerns regarding the potential health and environmental implications of such practices, consumers prioritize affordability over higher-priced organic or non-GMO certified potato starch. The natural product sector also utilizes potato starch as a gluten-free alternative in various applications.

Get a glance at the market share of various segments Request Free Sample

The conventional segment accounted for USD 2.94 billion in 2018 and showed a gradual increase during the forecast period.

Regional Insights

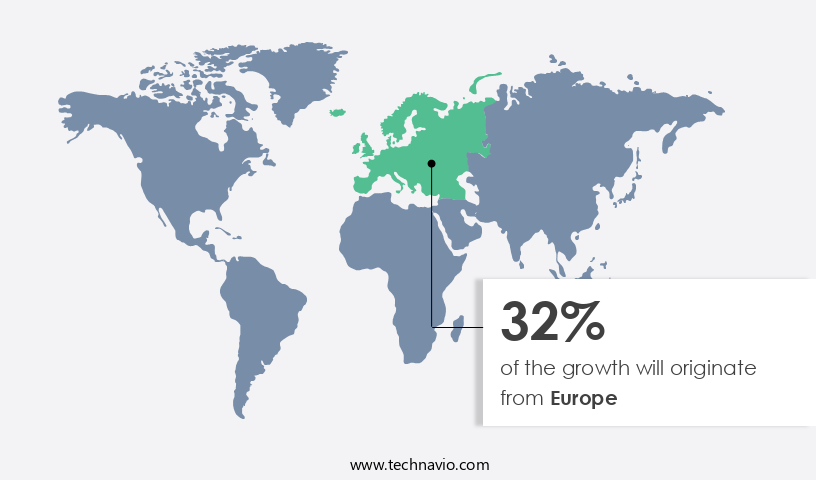

Europe is estimated to contribute 32% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The European region holds a substantial position in the market, driven by its significant production and consumption. The food industry, particularly confectioneries, dry mixes, and extruded food products, is a major consumer of potato starch in Europe. The increasing demand for natural and organic food products, as well as the preference for clean-label food items, is fueling the growth of the market in this region. Key European players include Germany, the UK, France, and Russia, each contributing uniquely to the expanding market. In addition to food applications, potato starch finds use in various industries such as pet foods, animal nutrition, microbial and industrial enzymes, detergent industry, feed industry, biodegradable plastics, aerobic composting, soil improver, and natural products. The market in Europe is expected to witness steady growth during the forecast period due to these diverse applications.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

Increased use of potato starch as a thickener is the key driver of the market. Potato starch is widely used in food processing due to its neutral flavor and moderate gelatinization temperature. Its ability to thicken sauces, soups, and gravies without altering their taste makes it a preferred choice. The thickening property of potato starch is attributed to its behavior in the presence of hot water. When heated in a liquid, potato starch granules absorb water, expand, and release long starch molecules, resulting in thickening. In the context of food production, potato starch serves as a substitute for high-calorie sugar or high-cholesterol food ingredients.

Additionally, potato starch finds applications in the production of bioplastics, particularly in Europe, as per European Bioplastics. Other alternative starches, such as tapioca starch, rice flour, cassava roots, coconut flour, and cereals, also hold significance in various industries. However, potato starch's versatility and effectiveness make it a noteworthy contender in the market. It is used extensively in the production of noodles, canned vegetables, meat products, snacks, and various other food items. Furthermore, potato starch plays a crucial role in the preparation of soups and sauces, adding to its market value.

Market Trends

Increasing awareness about gluten-free products is the upcoming trend in the market. The demand for gluten-free food products has experienced a notable wave due to the growing awareness about celiac disease and other gluten intolerances. Potato starch, being naturally gluten-free, has gained significant attention in the food industry. Unlike grains such as wheat, barley, rye, and spelt, which contain gluten proteins that form a sticky network when water is added, potato starch does not contain gluten. This makes it an ideal substitute for grains in various food applications, including noodles, soups, sauces, canned vegetables, meat, and snacks. Moreover, potato starch is also used in the production of bioplastics, which are eco-friendly alternatives to traditional plastics.

However, other alternatives to wheat-based starches include tapioca starch, rice flour, and cassava roots. European Bioplastics, an association representing the bioplastics industry, highlights the importance of these alternatives in reducing the carbon footprint and promoting sustainable food production. Cereals, a major food category, also utilize these alternatives to cater to the growing demand for gluten-free food products.

Market Challenge

The availability of substitutes for potato starch is a key challenge that is affecting market growth. Potato starch is a type of starch derived from the tubers of potatoes. It is widely used in various industries, including food and beverages, pharmaceuticals, and industrial applications. However, there are several alternatives to potato starch, such as tapioca starch, coconut flour, rice flour, and cassava roots. Tapioca starch, derived from cassava roots, is a popular alternative to potato starch in the food industry. It is often used in the production of bioplastics due to its biodegradable properties. European Bioplastics, an organization representing the bioplastics industry, reports that tapioca starch is the most commonly used plant-based starch in bioplastics production. Cereals, such as corn and wheat, are also sources of starch. Cornstarch is a widely used alternative to potato starch in various applications. It is effective in thickening and baking applications, and can be used in an equivalent quantity to potato starch. Cornstarch is also used in the production of paper and adhesives. Rice flour and coconut flour are other alternatives to potato starch.

Further, rice flour is commonly used in the production of noodles, soups, sauces, and canned vegetables. Coconut flour is a popular alternative for those with gluten intolerance and is often used in baking. In conclusion, while potato starch has its unique properties, there are several alternatives, including tapioca starch, cornstarch, rice flour, and coconut flour, that can effectively replace it in various applications. These alternatives offer similar functional properties and are widely used in industries such as food and beverages, pharmaceuticals, and industrial applications.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

AKV AMBA - The company offers potato starch which is used in many meat, sauces and dry mixes, soup, noodle and extruded products.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Cargill Inc.

- Cooperatie Koninklijke Cosun UA

- Emsland Starke GmbH

- Ingredion Inc.

- KMC

- Lyckeby Starch AB

- PEPEES SA

- RadchenUSA

- Roquette Freres SA

- Royal Avebe

- SIA Aloja Starkelsen

- Stagot Potatoes Product LLP

- Sudstarke GmbH

- Sudzucker AG

- Tate and Lyle PLC

- Tereos Participations

- VIMAL PPCE

- Royal Ingredients Group BV

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Potato starch is a type of starch derived from the tubers of the potato plant. It is a versatile ingredient used in various industries, including food and beverage, bioplastics, and industrial applications. Potato starch finds extensive usage in the food industry for producing a wide range of products such as noodles, soups, sauces, canned vegetables, meat, snacks, confectionaries, dry mixes, extruded food products, pet foods, and animal nutrition. In the bioplastics industry, potato starch is used as a raw material for manufacturing biodegradable plastics. The European Bioplastics and other organizations promote the use of bioplastics due to their eco-friendly nature and sustainability. Potato starch is also used as a natural additive in the textiles, pharmaceuticals, and paper manufacturing industries. The market is driven by factors such as consumer preferences for natural food ingredients, clean-label products, and plant-based products.

Additionally, the market includes native type, modified potato starch, and organic potato starch. Modified potato starch is used as a thickening agent, binding agent, and stabilizing agent in various applications. Native type and organic potato starch are used in the production of naturally-derived ingredients, organic processed foods, and gluten-free products. The market is influenced by factors such as food safety, animal welfare concerns, environmental sustainability, veganism, and vegetarian diets. However, the market faces restraining factors such as obesity, cardiovascular diseases, diabetes, and the use of chemicals and pesticides in the production of conventional potato starch. The global food industry's shift towards nutritious and cost-effective additives is expected to boost the market's growth.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

173 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.62% |

|

Market growth 2024-2028 |

USD 857.55 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.5 |

|

Regional analysis |

Europe, North America, APAC, South America, and Middle East and Africa |

|

Performing market contribution |

Europe at 32% |

|

Key countries |

US, China, France, Germany, and The Netherlands |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

AKV AMBA, Cargill Inc., Cooperatie Koninklijke Cosun UA, Emsland Starke GmbH, Ingredion Inc., KMC, Lyckeby Starch AB, PEPEES SA, RadchenUSA, Roquette Freres SA, Royal Avebe, SIA Aloja Starkelsen, Stagot Potatoes Product LLP, Sudstarke GmbH, Sudzucker AG, Tate and Lyle PLC, Tereos Participations, VIMAL PPCE, and Royal Ingredients Group BV |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across Europe, North America, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -