Enjoy complimentary customisation on priority with our Enterprise License!

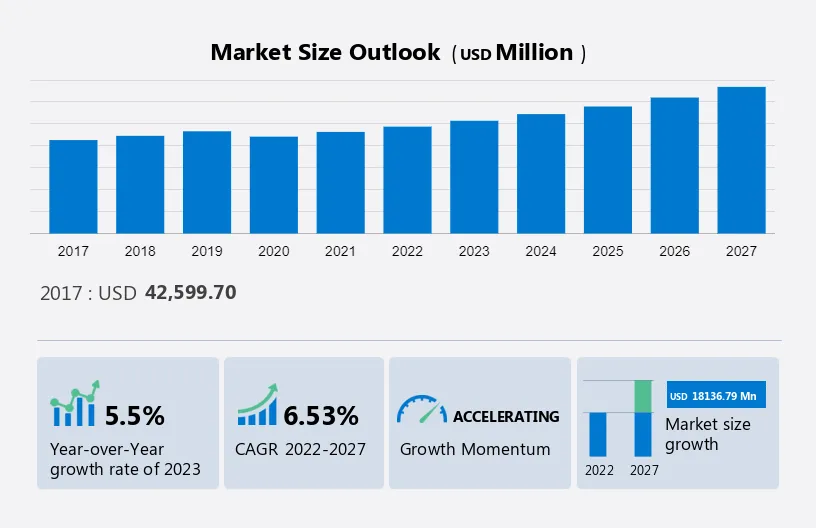

The Semiconductor Assembly and Testing Services (SATS) Market size is estimated to grow at a CAGR of 6.53% between 2022 and 2027 and the size of the market is forecast to increase by USD 18,136.79 million. The growth of the market depends on several factors, such as rising sales of IoT devices, increasing incorporation of electronic parts in vehicles, and rising adoption of cloud computing data centers.

This report extensively covers market segmentation by application (communication, computing and networking, industrial, consumer electronics, and automotive electronics), service type (assembly services and testing services), and geography (APAC, North America, Europe, South America, and Middle East and Africa). It also includes an in-depth analysis of drivers, trends, and challenges. Furthermore, the report includes historic market data from 2017 to 2021.

To learn more about this report, Download Report Sample

The report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Global Semiconductor Assembly and Testing Services Market Customer Landscape

Our researchers analyzed the data with 2022 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The increasing incorporation of electronic parts in vehicles is the key factor driving the global Semiconductor Assembly and Test Services Market. Semiconductors are widely used in the automotive industry due to new technologies such as autonomous driving and other electronic devices. Future self-driving cars will rely on powerful computing systems, arrays of sensors, networks, and satellite navigation, all of which require electronics. The adoption of safety-related electronic systems is therefore growing exponentially. Semiconductor component manufacturers are increasingly focusing on developing sophisticated systems. Automotive semiconductor suppliers are increasing demand for semiconductor devices such as miniature controllers, sensors, and memory for vehicles. Apart from that, electrical installations, automation, digital communications, and security systems are the main semiconductor devices incorporated into automotive electronics. Additionally, modern electric vehicles rely on power electronics to control the main propulsion motors and manage the battery system. Electrification of various mechanical systems has allowed automakers to increase efficiency, limit emissions and improve performance.

Additionally, customers prefer vehicles that support advanced connectivity systems that allow the synchronization of mobile devices with the vehicle's audio system. Electrification is a major driver of technological development in the automotive industry. Automotive systems such as fuel delivery systems, braking systems, steering systems, and safety systems are increasingly equipped with electronic components with integrated chips that fine-tune each action and improve overall system efficiency. The increasing use of automotive electronics in modern vehicles necessitates the introduction of automotive semiconductors to control body electronics. Hence, the above factors are anticipated to drive the growth of the Semiconductor Assembly and Test Services Market during the forecast period.

Advances in semiconductor assembly and testing services will fuel the global Semiconductor Assembly and Test Services (SATS) Market. In recent years, a new method of chip packaging known as 3D IC has emerged on the market. With the help of 3D packaging, foundries can reduce the size of electronic products with the help of miniaturized ICs. Additionally, 3D packaging allows information centers to be stacked, further addressing space constraint issues. Such packaging techniques enable electronic device manufacturers to develop advanced products that are much smaller, consume less power, and reduce overall product costs. In addition, interposer technology using organic substrates is becoming more popular due to its lower cost compared to silicon interposer technology. Several high-efficiency applications have been demonstrated with live connectors. However, efficacy in next-generation applications is still being observed.

Another widely used technology is Silicon-via-Interconnection (TSV). TSV's efficient interconnect technology is used as an alternative to wire bonding and flip chips to create 3D packages and its 3D integrated circuits. 2.5/3D IC technology uses TSV to improve circuit compression, power, and volume performance. The 3D ICs are directly stacked on top of each other and connections are made by matching the bonding areas with the TSVs. There are also applications in CMOS (Complementary Metal Oxide Semiconductor) image sensors (CIS). TSVs are embedded behind the image sensor to create interconnect lines and eliminate wire bonds, enabling high-density interconnects in a reduced form factor. Therefore, the above factors are expected to drive the growth of the Semiconductor Assembly and Test Services (SATS) Market during the forecast period.

High investment in packaging solutions can majorly impede the growth of the market. A large investment in packaging solutions can have a negative impact on the market. With a significant portion of the money going to packaging solutions, manufacturers can compromise on the quality of assembly and test services that are essential to ensuring the optimal operation of semiconductors. High costs associated with packaging solutions can also reduce a company's profit margins, which can adversely affect overall financial performance. It can divert away from the market, limiting innovation and preventing the introduction of new and better products to the market. Another problem associated with large investments in packaging solutions is the potential lack of scalability. Packaging solutions can be designed to fit a specific type of semiconductor or electronic device. However, with constant advancement in technology and increasing demand for versatile and customizable products, it can be difficult for businesses to keep up with changing customer needs and demands.

Additionally, the trend toward miniaturization poses significant challenges for packaging solutions. As electronics become smaller and more compact, traditional packaging solutions can become inadequate. Manufacturers may need to invest in more sophisticated and sophisticated packaging solutions, which can result in higher costs and increased complexity. In addition, large investments in packaging solutions can also have a negative impact on the environment. Most packaging materials are not biodegradable, contributing to the growing e-waste problem. Businesses must find new and innovative ways to reduce the environmental footprint of their products and services. This includes investing in eco-friendly packaging solutions. Therefore, such factors will hamper the growth of the Semiconductor Assembly and Test Services Market during the forecast period.

Vendors are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Amkor Technology Inc: The company offers different types of semiconductor assembly and testing services especially bumped wafer test packages.

Aptasic SA: Under its subsidiary, Bluetest Testservice, the company offers semiconductor assembly and testing services.

We also have detailed analyses of the market’s competitive landscape and offer information on 18 market vendors, including:

The report offers clients a deeper understanding of the market and its players through a combined qualitative and quantitative analysis of the vendors. The analysis classifies vendors into categories based on their business approach, including pure-play, category-focused, industry-focused, and diversified. Vendors are specially categorized into dominant, leading, strong, tentative, and weak to understand the dos and don’ts of business which in turn can help a client make the best decision.

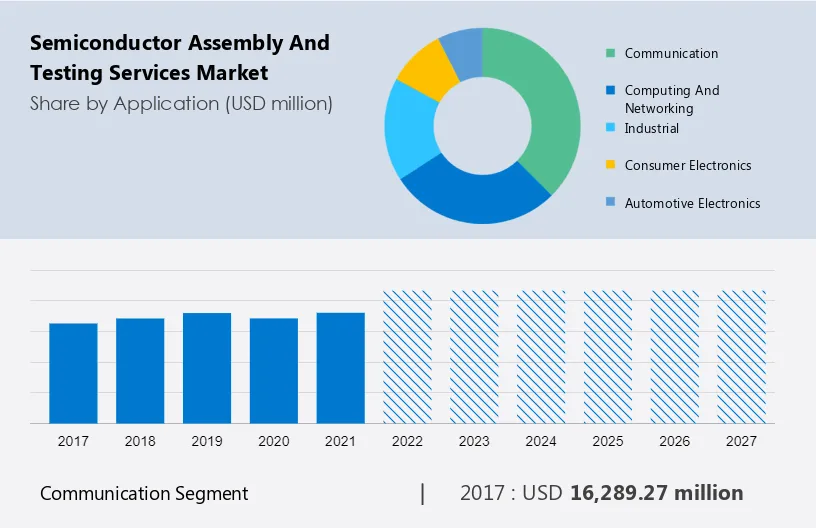

The communication segment will contribute a major share of the market, as it utilizes multiple applications of semiconductor assembly and testing services. The communication segment showed a gradual increase in market share with USD 16,289.27 million in 2017 and continued to grow until 2021. Semiconductor assembly and testing services play an important role in the telecom segment by providing quality components and services for telecom equipment manufacturing. Telecommunications segments require the use of solid-state components for signal amplification, filtering, and modulation. They are essential for the transmission of data and voice-over networks.

Get a Customised Report as per your requirements for FREE!

Some of the ways in which semiconductor assembly and testing services are used in communication segments are in the manufacturing of communication equipment, telecommunications equipment testing, and certification, customization of communication equipment, quality management, and IoT and wireless communication. Hence, the factors mentioned above are expected to drive the growth of the market through the communications segment during the forecast period.

In the semiconductor assembly and testing services industry, semiconductor assembly is also called IC packaging, along with encapsulation or sealing. The market for assembly services is a highly dynamic industry, requiring suppliers to invest heavily in research and development to remain competitive in the market. Rising smartphone sales and demand for IoT devices are pushing semiconductor assembly and testing services vendors to develop smaller and smaller case and packaging materials that can offer high efficiency. Electronic products are becoming smaller, lighter, and thinner, and are becoming faster and more multifunctional. However, providing access to these features requires a large number of connection points, a continuing challenge in package design. Today's industry designs and development packages reduce overall component size while maintaining or improving efficiency and performance. Increasing demand for these high-quality packaging solutions is expected to drive the growth of the market during the forecast period.

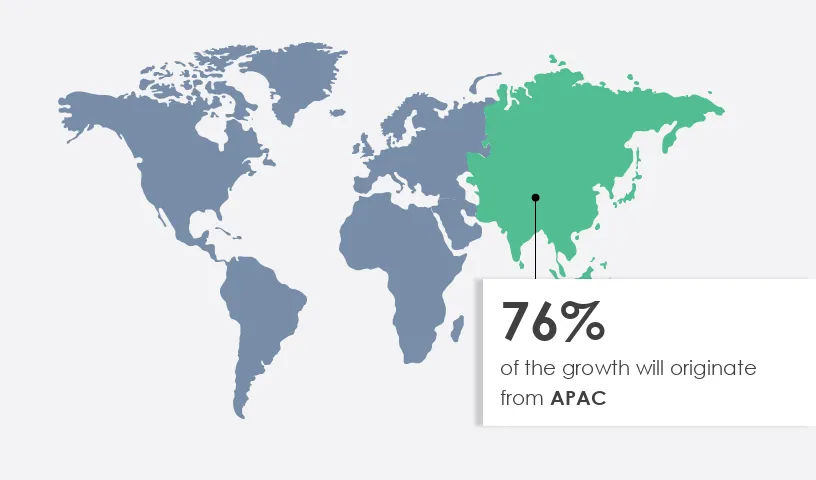

APAC is estimated to contribute 76% to the growth by 2027. Technavio’s analysts have elaborately explained the regional trends, drivers, and challenges that are expected to shape the market during the forecast period.

For more insights on the market share of various regions View PDF Sample now!

APAC has hosted a large semiconductor industry since the 20th century due to its low labor costs and proximity to various raw material sources. The semiconductor assembly and testing services industry in the region is dominated by Taiwan, followed by China, Japan, and Singapore. These countries, which are geographically very close, are major sources of raw materials and intermediate parts. All of these regions are investing heavily in building new fabs. China is also expected to set about building new manufacturing sectors, aided by favorable government policies. Globally, Taiwan is one of the early adopters of the discrete semiconductor manufacturing model. Different companies are involved in different processes such as designing, manufacturing, assembling, and testing the entire manufacturing setup. This model is now driving much of the semiconductor industry, resulting in the growth of the market in APAC.

The market faced major challenges in 2020 due to the COVID-19 outbreak. To contain the spread of the pandemic, governments of many countries imposed curfews, resulting in shutdowns/closures of semiconductor manufacturing plants. The pandemic also negatively impacted consumer purchasing behavior, reducing demand for consumer electronics such as smartphones and tablets. However, in the first half of 2021, several countries across the world stepped up vaccination programs and resumed semiconductor manufacturing in the fourth quarter of 2021. As a result, demand for semiconductor assembly and testing services across the world increased in 2021-2022.

The semiconductor assembly and testing services market report forecasts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and growth opportunities from 2017 to 2027.

|

Semiconductor Assembly And Testing Services Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

172 |

|

Base year |

2022 |

|

Historic period |

2017-2021 |

|

Forecast period |

2023-2027 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.53% |

|

Market growth 2023-2027 |

USD 18,136.79 million |

|

Market structure |

Fragmented |

|

YoY growth 2022-2023(%) |

5.5 |

|

Regional analysis |

APAC, North America, Europe, South America, and Middle East and Africa |

|

Performing market contribution |

APAC at 76% |

|

Key countries |

US, South Korea, Taiwan, China, and Japan |

|

Competitive landscape |

Leading Vendors, Market Positioning of Vendors, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Amkor Technology Inc., Aptasic SA, ASE Technology Holding Co. Ltd., ChipMOS TECHNOLOGIES Inc., DPA Components International, Flexitallic Group, Formosa Advanced Technologies Co. Ltd. , GlobalFoundaries Inc., Jiangsu Changdian Technology Co. Ltd., King Yuan Electronics Co. Ltd., Koninklijke Philips NV, Micross Inc., Ose Corp., Powertech Technology Inc., Rochester Electronics LLC, Teledyne Technologies Inc., Tianshui Huatian Technology Co. Ltd., Unisem M Berhad, UTAC Holdings Ltd., and Walton Advanced Engineering Inc. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID 19 impact and recovery analysis and future consumer dynamics, Market condition analysis for forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Application

7 Market Segmentation by Service Type

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights

Market - North America, Europe, EMEA, APAC : US, Canada, China, Germany, UK - Forecast 2023-2027")