Commercial Aircraft Leasing Market Size 2026-2030

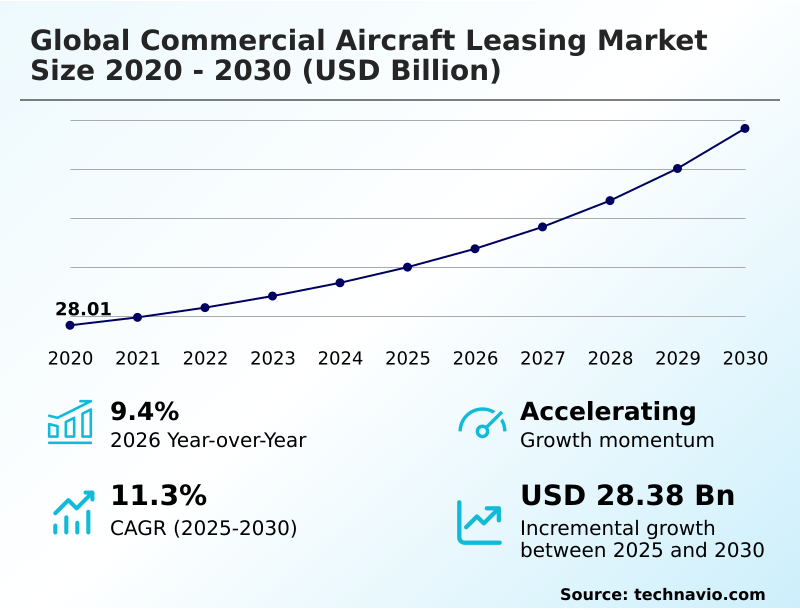

The commercial aircraft leasing market size is valued to increase by USD 28.38 billion, at a CAGR of 11.3% from 2025 to 2030. Growing strategic shift toward widebody leasing for long-haul recovery will drive the commercial aircraft leasing market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 41% growth during the forecast period.

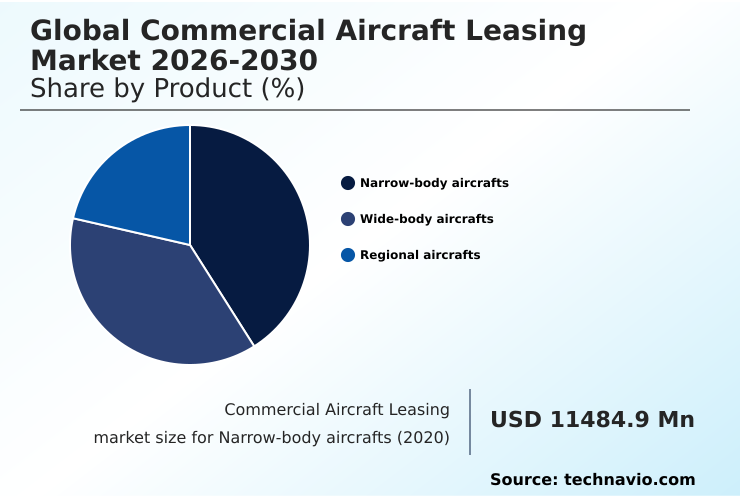

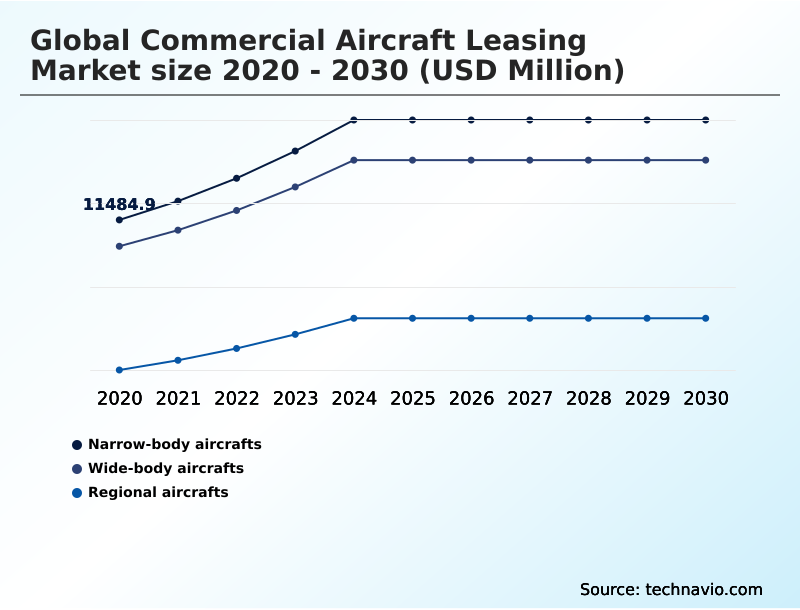

- By Product - Narrow-body aircrafts segment was valued at USD 15.14 billion in 2024

- By Type - Wet lease segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 40.28 billion

- Market Future Opportunities: USD 28.38 billion

- CAGR from 2025 to 2030 : 11.3%

Market Summary

- The commercial aircraft leasing market functions as a critical financial and operational backbone for the global aviation industry, enabling airlines to manage fleet flexibility and capital expenditure. Lessors provide access to aircraft through arrangements like the dry lease structure and wet lease agreement, allowing carriers to scale capacity in response to demand without the heavy upfront investment of direct purchases.

- A primary driver is the widespread adoption of the sale-and-leaseback transaction, where airlines sell new aircraft to lessors and lease them back, unlocking immediate capital for operational resilience. This dynamic is crucial for a fleet modernization strategy, as carriers seek next-generation assets to comply with fuel efficiency standards and environmental mandates.

- For instance, an airline might leverage leasing to upgrade its fleet, reducing fuel burn by over 15% and aligning with sustainability-linked financing goals. However, the sector faces significant headwinds from supply chain dislocation and OEM delivery delays, creating scarcity and elevating lease rates.

- Concurrently, managing residual value risk and navigating jurisdictional risk in emerging markets remain persistent challenges that shape lessor strategy and portfolio management solutions.

What will be the Size of the Commercial Aircraft Leasing Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Commercial Aircraft Leasing Market Segmented?

The commercial aircraft leasing industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Narrow-body aircrafts

- Wide-body aircrafts

- Regional aircrafts

- Type

- Wet lease

- Dry lease

- Application

- Passenger

- Freight

- Usage

- Short-term

- Long-term

- Geography

- APAC

- China

- India

- Japan

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- APAC

By Product Insights

The narrow-body aircrafts segment is estimated to witness significant growth during the forecast period.

The narrow-body aircraft segment is the cornerstone of the market, prized for its operational versatility and strong narrowbody aircraft liquidity. These single-aisle jets, essential for high-frequency domestic and regional routes, are central to airline fleet modernization strategy.

Lessors favor this segment for its broad operator base and stable asset values, which simplifies aircraft remarketing. Demand is fueled by the need to replace older fleets, with new-generation models reducing fuel consumption by up to 20%.

The high cost of funds makes direct purchasing difficult, reinforcing the reliance on lessors. The segment's resilience is supported by robust aircraft financing mechanisms like fixed-rate notes and green bonds.

However, persistent supply chain dislocation creates challenges, leading to potential asset valuation impairments on older jets as carriers await new deliveries.

The Narrow-body aircrafts segment was valued at USD 15.14 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 41% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Commercial Aircraft Leasing Market Demand is Rising in APAC Get Free Sample

The geographic landscape is shifting, with APAC poised to account for over 41% of incremental growth, driven by fleet expansion in China and India.

In North America, which shows a strong growth trajectory, carriers are leveraging leasing to mitigate supply chain dislocation and secure lift. European operators are aggressively pursuing portfolio management solutions to comply with carbon reduction mandates, prioritizing new technology aircraft.

Specialized financial instruments are gaining traction globally; for example, the japanese operating lease and sharia-compliant lease products are channeling new capital into the industry. Meanwhile, sovereign-backed leasing platforms in the Middle East are reshaping regional competition.

The effectiveness of a dry lease structure versus a wet lease agreement varies by region, depending on operational needs and regulatory environments, influencing how lessors deploy assets.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

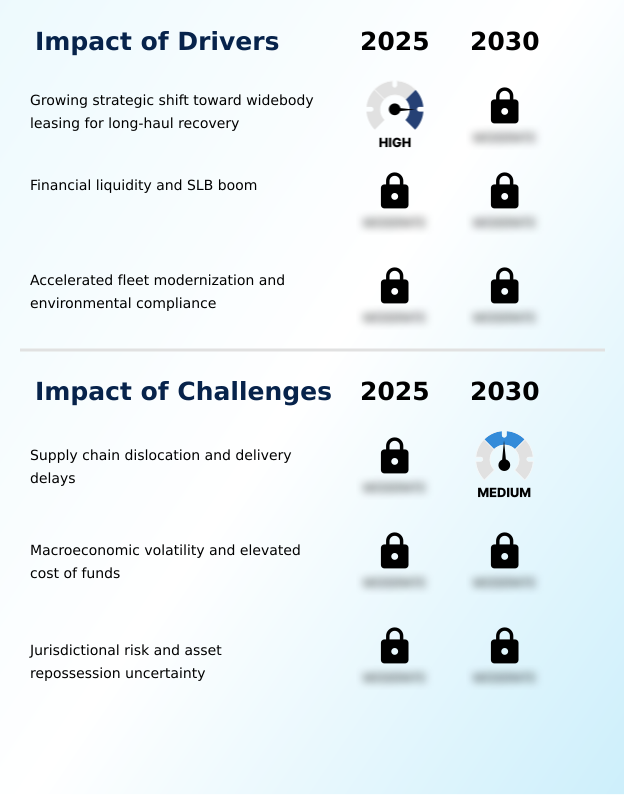

- Understanding the commercial aircraft leasing market dynamics requires analyzing several interconnected factors. The impact of OEM delivery delays on lessors is a central challenge, creating revenue uncertainty and complicating fleet management. In response, the sale-and-leaseback model for fleet expansion has become a primary tool for airlines to secure new assets while preserving capital.

- This aligns with the broader role of leasing in fleet modernization strategies, allowing carriers to adopt new technology without bearing full ownership risk. A key trend is the strategic pivot toward widebody asset acquisition, driven by the strong recovery in international travel.

- The demand drivers for widebody aircraft leasing are now outpacing those for narrowbodies in terms of value, leading to new opportunities in the secondary widebody market. Financially, the effect of interest rates on lessor profitability is forcing more disciplined capital allocation, while asset-backed securitization for aircraft portfolios remains a vital liquidity source.

- The economics of passenger-to-freighter p2f conversions are also gaining attention, offering a second life for mid-life assets. Operationally, a comparison of wet lease vs dry lease structures shows that long-term dry leases still dominate, but demand for short-term wet leases is growing faster.

- Throughout these activities, managing residual value risk for leased aircraft and navigating jurisdictional risk in aircraft finance are constant priorities. The Cape Town Convention helps, but challenges of aircraft repossession in emerging markets persist.

- Finally, the rise of sustainability-linked financing in aviation leasing is fundamentally reshaping how deals are structured, reflecting the industry's commitment to decarbonization and providing a new lens through which to view the trends in the global commercial aircraft leasing market 2026-2030.

What are the key market drivers leading to the rise in the adoption of Commercial Aircraft Leasing Industry?

- The market is primarily driven by a strategic shift toward widebody aircraft leasing, which is fueled by the strong recovery of long-haul international networks.

- A key driver is the urgent need for fleet renewal to meet environmental social governance (ESG) goals and achieve significant operational cost savings.

- Lessors act as the primary conduit for ESG capital, facilitating the adoption of aircraft that meet new fuel efficiency standards.

- This transition is made possible through sustainability-linked financing, which ties financial terms to performance targets like increased sustainable aviation fuel usage. Simultaneously, the strategic prioritization of liquidity has fueled a boom in sale-and-leaseback transactions, allowing carriers to optimize balance sheets.

- Short-term capacity gaps, often filled by an ACMI provider under a flight crew maintenance insurance model, highlight the market's need for flexibility.

- These drivers collectively strengthen the lessor's role in providing capital and asset management expertise, with some airlines reporting a 15% improvement in capital efficiency.

What are the market trends shaping the Commercial Aircraft Leasing Industry?

- A strategic resurgence in widebody asset acquisition is reshaping the market. Lessors are rebalancing portfolios to capitalize on the scarcity of production slots and a robust recovery in long-haul international travel.

- A dominant trend is the strategic pivot toward widebody asset acquisition, driven by recovering long-haul international networks. An aviation finance company is now balancing portfolios beyond the commercial jet transport aircraft to capitalize on higher margins. This shift is complemented by the industrial-scale acceleration of passenger-to-freighter conversion, creating new revenue streams for mid-life assets and strengthening the air cargo network.

- The financial architecture is also evolving, with asset-backed securitization becoming more common for managing large portfolios. These trends transform how lessors manage the aircraft operating lease, moving from simple financing to complex asset lifecycle management.

- This strategic repositioning is critical for navigating a market where growth in the regional aircraft market outpaces certain legacy segments and the risk of airline insolvency remains a constant consideration.

What challenges does the Commercial Aircraft Leasing Industry face during its growth?

- Systemic supply chain dislocations and persistent delivery delays from original equipment manufacturers present a key challenge affecting industry growth.

- The market faces significant challenges, primarily from production slot scarcity, which complicates fleet planning support and hinders growth for airlines seeking to expand. The inability of airframe manufacturers to meet demand for next-generation assets, including both single-aisle transactions and twin-aisle segment orders, creates a significant capital expenditure burden. This forces airlines toward balance sheet optimization through leasing.

- Managing aircraft lifecycle management becomes more complex as operators extend leases on older jets while awaiting new deliveries. This dynamic is exacerbated by OEM delivery delays, which have a cascading effect across the industry.

- The carbon intensity of the fleet remains a concern as the transition to more efficient models like the Airbus A330neo and Embraer e-jet e2 family is slowed by these supply-side constraints.

Exclusive Technavio Analysis on Customer Landscape

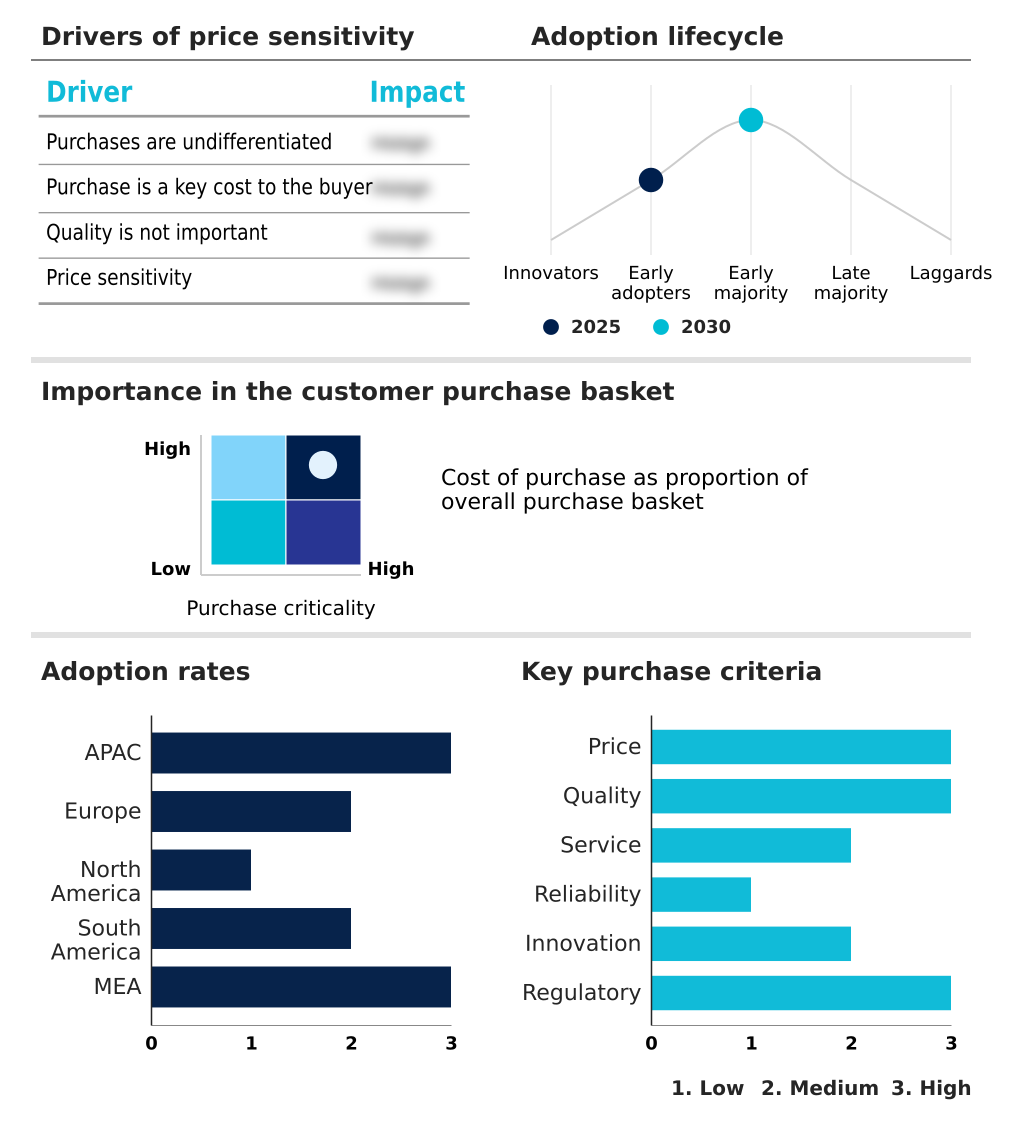

The commercial aircraft leasing market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the commercial aircraft leasing market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Commercial Aircraft Leasing Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, commercial aircraft leasing market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AerCap Holdings N.V. - Providers deliver comprehensive fleet solutions, including operating leases, sale-and-leaseback transactions, and aircraft portfolio management, facilitating airline fleet modernization and financial flexibility.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AerCap Holdings N.V.

- Air Lease Corp.

- Aircastle Ltd.

- Aviation Capital Group

- Avolon Aerospace Leasing Ltd.

- Azorra Aviation Holdings LLC

- BBAM US LP

- BOC Aviation Ltd.

- CDB Aviation

- DAE Ltd.

- Deucalion Aviation Ltd.

- ICBC Financial Leasing Co.

- Jackson Square Aviation LLC

- Macquarie Group Ltd.

- SMBC Aviation Capital Ltd.

- Stratos

- The Carlyle Group Inc.

- TrueNoord

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Commercial aircraft leasing market

- In January 2025, CDB Aviation announced the delivery of a new Boeing 737-8 to United Airlines as part of a broader series of sale-and-leaseback transactions supporting the carrier's fleet modernization and capital efficiency.

- In February 2025, Air Lease Corp. released its financial results, highlighting significant operational strain from persistent delivery slippages by major manufacturers that compromised its order book and necessitated constant renegotiations with airline customers.

- In March 2025, BOC Aviation Limited successfully priced a $500 million issuance of green notes, with proceeds specifically allocated to financing latest-technology aircraft that meet rigorous fuel efficiency standards.

- In April 2025, Avolon issued a trading update for its first quarter, revealing a significant uptick in the placement of new technology aircraft like the Airbus A320neo and Boeing 737 MAX, directly linked to customers' aggressive sustainability roadmaps.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Commercial Aircraft Leasing Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 296 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 11.3% |

| Market growth 2026-2030 | USD 28381.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 9.4% |

| Key countries | China, India, Japan, Singapore, Australia, Indonesia, Ireland, Germany, UK, France, The Netherlands, Spain, US, Canada, Mexico, Brazil, Argentina, Chile, UAE, Saudi Arabia, South Africa, Egypt and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The commercial aircraft leasing market is defined by its indispensable role in financing a fleet modernization strategy and managing asset valuation impairments for airlines globally. Lessors facilitate the transition to new technology aircraft, enabling carriers to meet stringent carbon reduction mandates and achieve fuel efficiency standards.

- This is critical as operational cost savings from a 15% to 20% reduction in fuel burn can offset lease payments. Key mechanisms include the aircraft operating lease and the sale-and-leaseback transaction, which provide liquidity and remove residual value risk from airline balance sheets.

- However, the landscape is fraught with challenges, including OEM delivery delays and supply chain dislocation, which disrupt revenue streams tied to pre-delivery payments. Jurisdictional risk premium and asset repossession uncertainty, despite protections from the Cape Town Convention, remain concerns. Lessors navigate this environment through sophisticated aircraft remarketing and portfolio management solutions, and by managing engine maintenance reserves.

- The market's financial architecture relies on aircraft financing tools like asset-backed securitization, green bonds, and fixed-rate notes to manage the cost of funds and net interest margins. Ultimately, success hinges on balancing widebody asset acquisition with narrowbody aircraft liquidity and aircraft lifecycle management.

What are the Key Data Covered in this Commercial Aircraft Leasing Market Research and Growth Report?

-

What is the expected growth of the Commercial Aircraft Leasing Market between 2026 and 2030?

-

USD 28.38 billion, at a CAGR of 11.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Narrow-body aircrafts, Wide-body aircrafts, and Regional aircrafts), Type (Wet lease, and Dry lease), Application (Passenger, and Frieght), Usage (Short-term, and Long-term) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Growing strategic shift toward widebody leasing for long-haul recovery, Supply chain dislocation and delivery delays

-

-

Who are the major players in the Commercial Aircraft Leasing Market?

-

AerCap Holdings N.V., Air Lease Corp., Aircastle Ltd., Aviation Capital Group, Avolon Aerospace Leasing Ltd., Azorra Aviation Holdings LLC, BBAM US LP, BOC Aviation Ltd., CDB Aviation, DAE Ltd., Deucalion Aviation Ltd., ICBC Financial Leasing Co., Jackson Square Aviation LLC, Macquarie Group Ltd., SMBC Aviation Capital Ltd., Stratos, The Carlyle Group Inc. and TrueNoord

-

Market Research Insights

- Market dynamics are increasingly shaped by the pursuit of balance sheet optimization and the need to manage capital expenditure burden. Airlines are leveraging lessors to access commercial jet transport aircraft for long-haul international networks without large upfront costs. This is particularly true in the regional aircraft market, where fleet flexibility is paramount.

- An aviation finance company now plays a critical role in facilitating access to models like the Boeing 787 Dreamliner and the Airbus A320neo family, with lease agreements often leading to operational cost savings of 15% or more. The scarcity of production slots has further elevated the lessor's importance.

- The ability to structure financing around environmental social governance (ESG) principles, addressing the carbon intensity of a fleet, is becoming a key competitive differentiator, with ESG-aligned portfolios showing a 10% higher placement rate.

We can help! Our analysts can customize this commercial aircraft leasing market research report to meet your requirements.

RIA -

RIA -