China Data Center Market Size 2026-2030

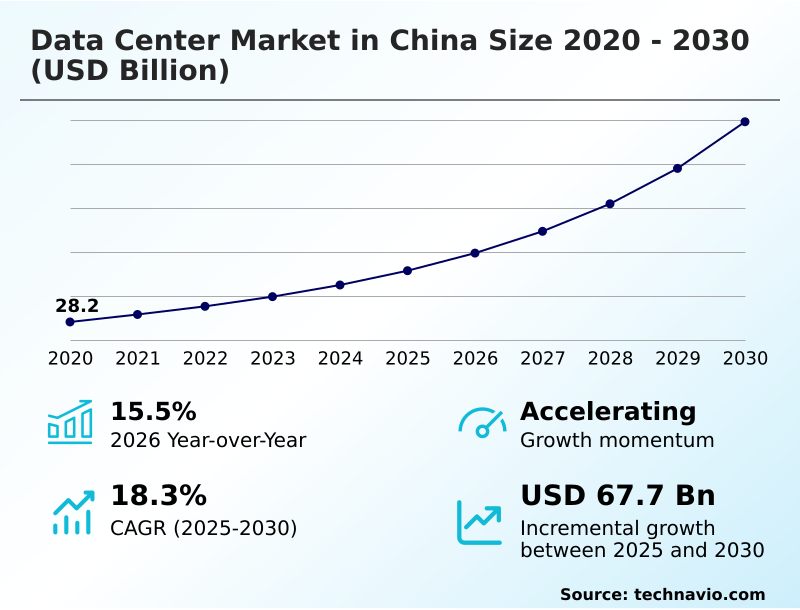

The china data center market size is valued to increase by USD 67.7 billion, at a CAGR of 18.3% from 2025 to 2030. Proliferation of generative AI and high performance computing will drive the china data center market.

Major Market Trends & Insights

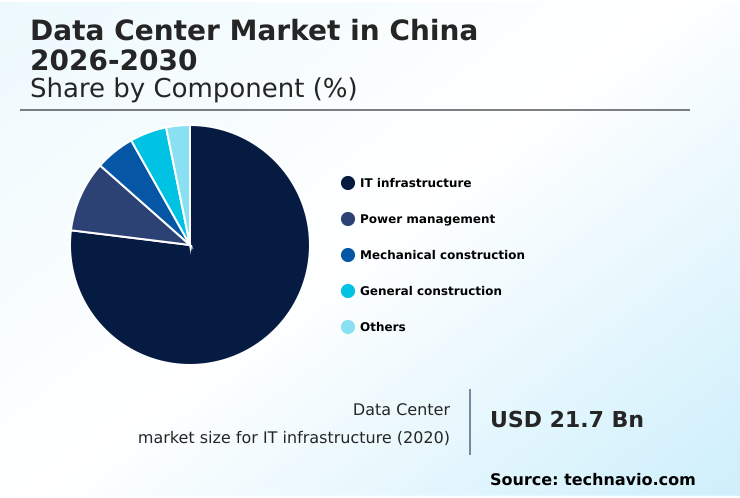

- By Component - IT infrastructure segment was valued at USD 34.4 billion in 2024

- By End-user - BFSI segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 91 billion

- Market Future Opportunities: USD 67.7 billion

- CAGR from 2025 to 2030 : 18.3%

Market Summary

- The data center market in China is undergoing a profound transformation, propelled by the convergence of digital economic strategies and technological sovereignty. This evolution is marked by a significant push towards high-performance computing capabilities to support burgeoning artificial intelligence and large language model workloads.

- Consequently, there is a heightened demand for facilities engineered for high-density configurations, leading to the widespread adoption of advanced thermal management solutions like direct-to-chip cooling. A key business scenario involves financial institutions migrating from legacy mainframes to cloud-native core banking systems hosted in distributed, highly secure data centers.

- This transition improves operational agility and enhances transaction processing speeds, but it also amplifies the need for robust data sovereignty compliance and quantum-resistant encryption. The market is also defined by the national Eastern Data, Western Computing initiative, which aims to rebalance digital resources by shifting compute-intensive tasks to energy-rich western provinces.

- This strategy fosters the development of green data centers that leverage renewable energy, addressing both power scarcity in eastern hubs and national carbon neutrality goals. The interplay between government-led initiatives, the demand for AI-driven analytics, and the necessity for secure, scalable infrastructure shapes a dynamic and highly competitive landscape.

What will be the Size of the China Data Center Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the China Data Center Market Segmented?

The china data center industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

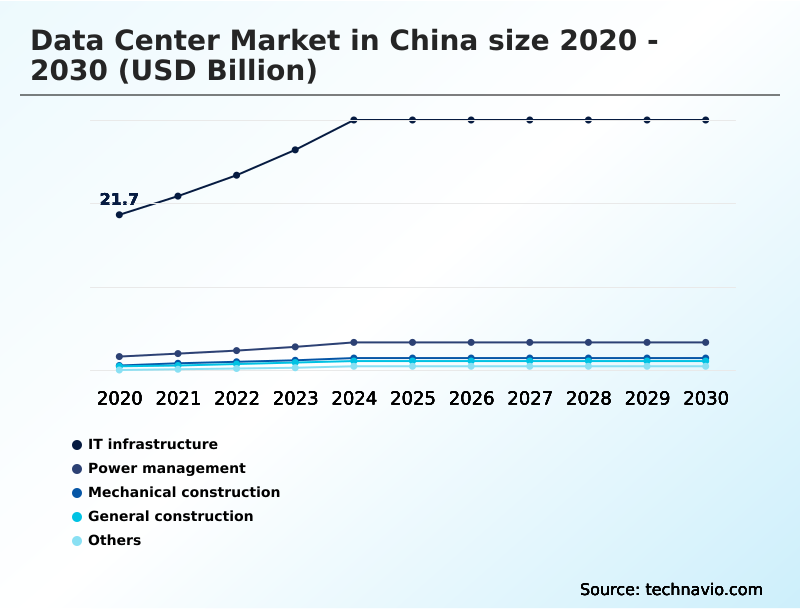

- Component

- IT infrastructure

- Power management

- Mechanical construction

- General construction

- Others

- End-user

- BFSI

- Telecom and IT

- Government

- Energy and utilities

- Others

- Type

- Colocation

- Hyperscale

- Edge

- Others

- Geography

- APAC

- China

- APAC

By Component Insights

The it infrastructure segment is estimated to witness significant growth during the forecast period.

The IT infrastructure segment is foundational, defined by the adoption of prefabricated modular data centers and hyper-converged infrastructure to accelerate deployment and simplify management.

The demand for higher bandwidth to support AI workloads is driving the upgrade to 800G networks and the implementation of all-flash arrays for faster data access. Thermal management within carrier-neutral facilities is evolving, with rear-door heat exchangers becoming common.

Operations are optimized using data center infrastructure management software. The critical environment design of modern facilities incorporates advanced security features like biometric access control.

Companies are also mitigating supply chain risks through strategic hardware stockpiling and using turnkey infrastructure solutions, including all-in-one container solutions and other containerized data solutions for rapid scaling.

The IT infrastructure segment was valued at USD 34.4 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the data center market in China 2026-2030 is increasingly complex, shaped by several intersecting priorities. The pursuit of data center market in china 2026-2030 sustainability goals is no longer optional, pushing operators to evaluate the cost-benefit of liquid cooling adoption versus traditional methods.

- Simultaneously, navigating data center market in china 2026-2030 regulatory compliance, particularly rules governing data sovereignty impact on architecture and compliance with cross-border data transfer, has become a primary operational focus.

- For performance, data center market in china 2026-2030 ai workload optimization is paramount, driving the impact of domestic chip integration and forcing a re-evaluation of the role of software-defined infrastructure in balancing workloads in distributed systems.

- The transition from air to liquid cooling is a direct response to managing high-density rack thermal output, a critical factor in optimizing power usage effectiveness. In parallel, data center market in china 2026-2030 edge computing latency reduction is being achieved through the strategic deployment of micro-facilities, leveraging the 5g network and edge node synergy.

- However, this distributed model introduces new challenges, including establishing robust security protocols for multi-cloud environments. Challenges in hyperscale energy procurement and data center market in china 2026-2030 supply chain resilience are forcing operators to adopt strategies for mitigating hardware shortages.

- The adoption of prefabricated construction time-to-market benefits has been a key response, reducing facility deployment times by up to 40% compared to traditional builds, a crucial advantage given the high investment drivers for carrier-neutral facilities.

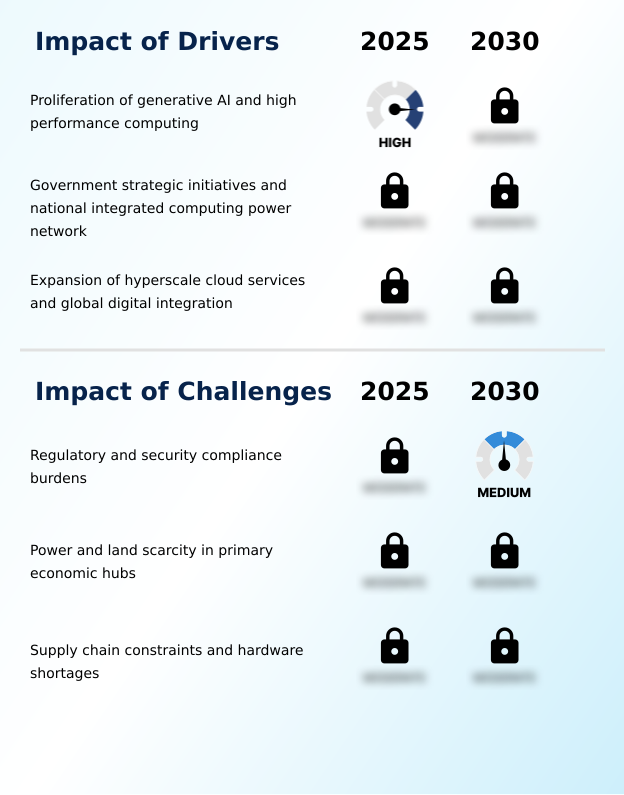

What are the key market drivers leading to the rise in the adoption of China Data Center Industry?

- The proliferation of generative AI and high-performance computing serves as a primary driver, fueling demand for advanced data center infrastructure.

- The primary driver for the market is the proliferation of high-performance computing to support ai model training and large language models. This has fueled demand for hyperscale build-to-suit projects that facilitate global digital integration.

- A strong government push for technological self-reliance is accelerating the use of domestic ai processors and fostering network-cloud convergence. Initiatives creating a unified computing resource platform with heterogeneous compute pools are enabling digital utility management at a national scale.

- The expansion of the industrial internet of things further drives the need for infrastructure capable of real-time data analytics, with some new AI clusters delivering a 25% increase in processing throughput for complex industrial simulations.

What are the market trends shaping the China Data Center Industry?

- The mainstream adoption of liquid cooling technologies is emerging as a significant trend. This shift addresses the increasing thermal management challenges posed by high-density computing environments.

- The market is defined by a significant trend toward advanced thermal management, with mainstream adoption of cold plate cooling and immersion cooling becoming critical for new ai-ready facilities. This shift allows operators to support higher rack densities while improving energy efficiency.

- Another key trend is the integration of sustainable energy through behind-the-meter generation and green power trading, enabling the use of zero-carbon electricity. Innovations in waste heat recovery are further reducing the environmental footprint. In parallel, the expansion of edge computing nodes supports localized high-performance compute, while hybrid cloud strategies leverage carrier-neutral interconnection and multi-cloud peering, giving enterprises flexibility.

- These trends have led to some facilities achieving a power usage effectiveness below 1.2, a 15% improvement over older designs.

What challenges does the China Data Center Industry face during its growth?

- Navigating complex regulatory frameworks and meeting stringent security compliance burdens presents a significant challenge to market growth and operations.

- Navigating a complex regulatory landscape presents a significant challenge, with stringent data sovereignty regulations and rules on cross-border data flow requiring careful architectural planning. This has created a bifurcated hardware industry and increased the need for third-party security audits.

- Resource scarcity in primary economic hubs is another constraint, forcing operators to adopt vertical data center design and invest in advanced power systems. Maintaining a low power usage effectiveness requires high-efficiency transformers and modern uninterruptible power supply systems with lithium-ion batteries.

- Supply chain disruptions for high-bandwidth memory and semiconductor component supply due to a lack of advanced chipmaking equipment also pose a risk, with hardware lead times increasing by up to 50% in some cases.

Exclusive Technavio Analysis on Customer Landscape

The china data center market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the china data center market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of China Data Center Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, china data center market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alibaba Cloud - Key offerings center on cloud data center infrastructure, providing compute, storage, and AI/ML services to support scalable enterprise and government agency solutions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alibaba Cloud

- Amazon.com Inc.

- CapitaLand Ltd.

- Chayora

- China Telecom Global Ltd.

- Chindata Group

- Digital Realty Trust Inc.

- Equinix Inc.

- Huawei Technologies Co. Ltd.

- IBM Corp.

- Inflection AI

- Microsoft Corp.

- NetApp Inc.

- Newtech

- Nippon Telegraph and Corp.

- Princeton Digital Group

- SpaceDC

- VNET Group Inc.

- Wangsu Science and Technology

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in China data center market

- In September 2024, China Unicom inaugurated a specialized artificial intelligence data center in Qinghai, representing a $390 million investment utilizing nearly 23,000 domestic chips.

- In November 2024, VNET Group reported a significant expansion in its wholesale data center capacity, reaching 783 megawatts to meet soaring demand for hyperscale and AI applications.

- In January 2025, GDS Holdings announced a private placement of $300 million from a Chinese institutional investor to facilitate the development of high-performance data centers.

- In February 2025, Tencent Cloud detailed plans to establish new data center facilities in the Middle East to support the international expansion of Chinese companies.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled China Data Center Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 211 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 18.3% |

| Market growth 2026-2030 | USD 67.7 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 15.5% |

| Key countries | China |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The data center market in China is experiencing a strategic pivot towards high-density and specialized infrastructure, driven by the intense demands of ai model training. This shift is compelling a move away from traditional cooling to advanced solutions like direct-to-chip cooling, cold plate cooling, and immersion cooling to manage the thermal output of high-density server racks.

- The adoption of hyper-converged infrastructure and the upgrade to 800g networks are becoming standard for new carrier-neutral facilities. A national focus on technological self-reliance is promoting the integration of domestic ai processors. Power systems are also being modernized with uninterruptible power supply systems that use lithium-ion batteries and smart power distribution units.

- Operators are using data center infrastructure management and software-defined management platforms to optimize operations. This focus on efficiency has enabled some new facilities to achieve a power usage effectiveness (PUE) that is 20% lower than the industry average from five years ago, influencing boardroom budgeting for sustainable infrastructure investment.

- This entire ecosystem supports high-performance computing for everything from large language models to the industrial internet of things.

What are the Key Data Covered in this China Data Center Market Research and Growth Report?

-

What is the expected growth of the China Data Center Market between 2026 and 2030?

-

USD 67.7 billion, at a CAGR of 18.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (IT infrastructure, Power management, Mechanical construction, General construction, and Others), End-user (BFSI, Telecom and IT, Government, Energy and utilities, and Others), Type (Colocation, Hyperscale, Edge, and Others) and Geography (APAC)

-

-

Which regions are analyzed in the report?

-

APAC

-

-

What are the key growth drivers and market challenges?

-

Proliferation of generative AI and high performance computing, Regulatory and security compliance burdens

-

-

Who are the major players in the China Data Center Market?

-

Alibaba Cloud, Amazon.com Inc., CapitaLand Ltd., Chayora, China Telecom Global Ltd., Chindata Group, Digital Realty Trust Inc., Equinix Inc., Huawei Technologies Co. Ltd., IBM Corp., Inflection AI, Microsoft Corp., NetApp Inc., Newtech, Nippon Telegraph and Corp., Princeton Digital Group, SpaceDC, VNET Group Inc. and Wangsu Science and Technology

-

Market Research Insights

- The market's dynamic is increasingly shaped by a move toward a distributed architecture, supporting localized high-performance compute for latency-sensitive applications. This shift complements the expansion of centralized hubs, where multi-cloud peering is becoming standard, enabling seamless workload portability and reducing vendor lock-in by over 20%.

- A strong focus on sustainability is driving the adoption of zero-carbon electricity and grid balancing services, with some new facilities achieving a 15% greater energy efficiency through integrated digital utility management. These advancements reflect a dual focus on performance and environmental responsibility, reshaping infrastructure investment priorities across the sector.

We can help! Our analysts can customize this china data center market research report to meet your requirements.

RIA -

RIA -