Software Market Size 2026-2030

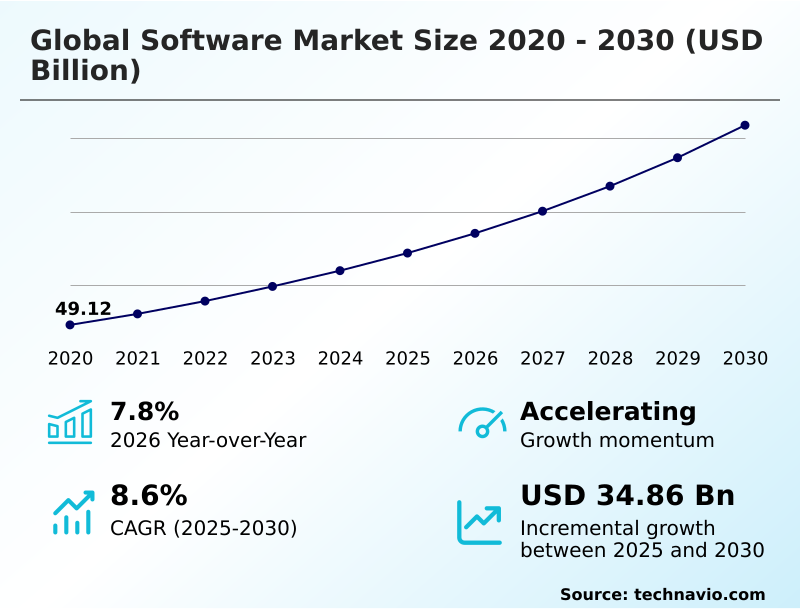

The software market size is valued to increase by USD 34.86 billion, at a CAGR of 8.6% from 2025 to 2030. Adoption of generative artificial intelligence models will drive the software market.

Major Market Trends & Insights

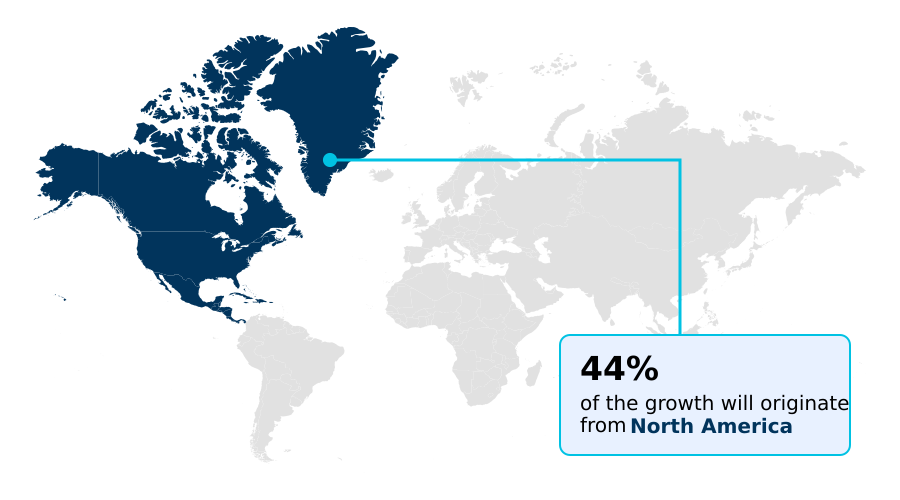

- North America dominated the market and accounted for a 44.5% growth during the forecast period.

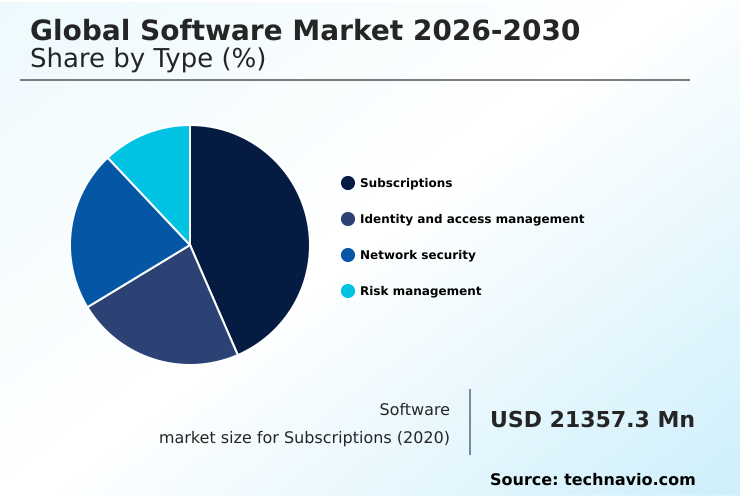

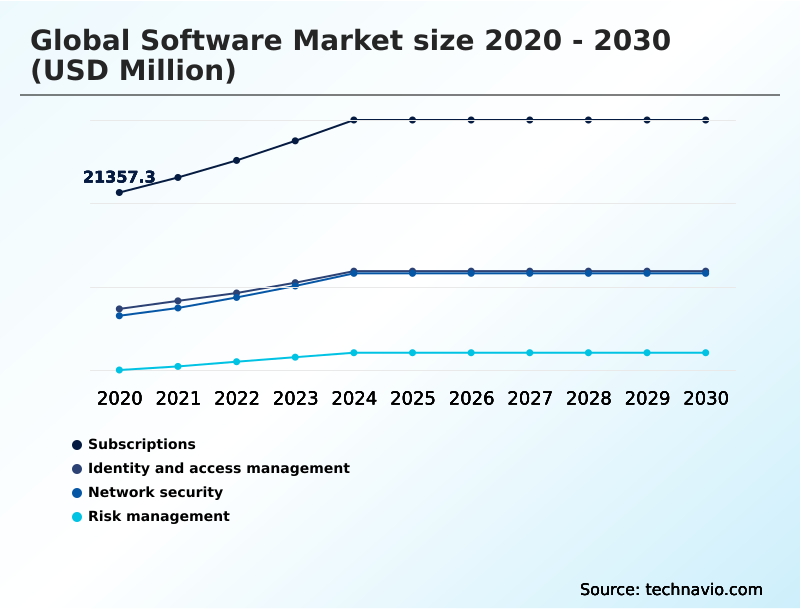

- By Type - Subscriptions segment was valued at USD 27.67 billion in 2024

- By Deployment - Cloud-based segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 54.46 billion

- Market Future Opportunities: USD 34.86 billion

- CAGR from 2025 to 2030 : 8.6%

Market Summary

- The software market is undergoing a foundational transition, moving beyond simple automation to embrace agentic artificial intelligence and autonomous workflow orchestration. This evolution is driven by the industrialization of generative artificial intelligence models, which are reshaping the development paradigm from static logic to adaptive, learning-centric distributed environments.

- As organizations prioritize operational efficiency, the demand for enterprise software with integrated machine learning models has intensified, supported by the rapid adoption of cloud-native architectures that enable hybrid work models. A key trend is the democratization of development through low-code development platforms, allowing for citizen developer integration.

- For instance, in supply chain management, task-specific agents now autonomously manage inventory logistics, optimizing routes and rerouting shipments in response to real-time disruptions, a task previously requiring significant manual oversight. However, this progress is tempered by the challenge of managing technical debt in legacy system modernization and navigating complex data sovereignty mandates.

- The industry’s focus on automated cybersecurity defense and zero-trust architectures is crucial for protecting the expanding digital frontier against threats like polymorphic malware.

What will be the Size of the Software Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Software Market Segmented?

The software industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Subscriptions

- Identity and access management

- Network security

- Risk management

- Deployment

- Cloud-based

- On-premises

- Sector

- Large enterprises

- Small and medium enterprises

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Type Insights

The subscriptions segment is estimated to witness significant growth during the forecast period.

The subscription model has replaced perpetual licensing as the dominant paradigm, emphasizing continuous value delivery over one-time ownership. This shift is enabled by software-as-a-service (SaaS) platforms, which are essential for modern hybrid work models.

The architecture of these offerings increasingly relies on scalable microservices and containerization technologies to allow for modular updates without system-wide disruption.

Organizations now demand that subscription services integrate natively with existing systems, driving innovation in API management to bridge cloud-native security with on-premise hardware.

This demand for behavioral analytics and seamless integration reflects a market where differentiation is based on deep, vertical-specific features. Adopting this model has been shown to reduce software shelfware, with some enterprises reporting a 15% improvement in license utilization efficiency.

The Subscriptions segment was valued at USD 27.67 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 44.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Software Market Demand is Rising in North America Get Free Sample

The geographic landscape is characterized by distinct regional dynamics. North America, contributing over 44% of incremental growth, leads in adopting endpoint detection and response and secure access service edge solutions due to a high concentration of enterprise software vendors.

Europe focuses on compliance, driving demand for platform as a service (PaaS) offerings that support strict data laws.

The APAC region is the fastest-growing market, with a surge in infrastructure as a service (IaaS) adoption to support its expanding digital economy. This regional diversification shapes demand for customer relationship management and enterprise resource planning systems.

The adoption of decentralized architectures and open-source frameworks is a common thread, with digital transformation initiatives occurring globally, though some sectors maintain on-premises deployment or private cloud architectures for security.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Enterprises are navigating a complex technological landscape, where understanding the impact of generative AI on software development life cycle is paramount for maintaining a competitive edge. This often begins with a critical assessment of managing technical debt in legacy system modernization, a necessary step before realizing the full benefits of cloud-native microservices architecture.

- The role of low-code platforms for citizen developers has become strategic, allowing businesses to rapidly build applications while IT focuses on core infrastructure. However, this agility introduces new risks, highlighting the challenges of data sovereignty in global software deployment and the need for robust governance. Consequently, automating cybersecurity with AI and machine learning is no longer optional.

- This involves implementing secure access service edge for remote work and building security frameworks based on strategies for building zero-trust network security. Internally, the transitioning from monolithic to microservices architecture continues, enabling organizations to better understand how agentic AI orchestrates business process workflows.

- Comparing on-premises vs cloud deployment security models reveals that adopting hybrid cloud for enterprise application portability offers a balanced approach. The evolution of identity and access management solutions is critical in this hybrid world, as is mitigating the risk of polymorphic malware in distributed networks.

- Finally, leveraging containerization technologies for application deployment and using serverless computing to reduce operational costs are key tactics for efficiency. The impact of open-source libraries on software supply chain remains a crucial consideration, alongside resolving enterprise resource planning system integration challenges and optimizing customer relationship management for small and medium enterprises.

- The advantages of autonomous workflow orchestration in finance are particularly notable, with automated systems reconciling accounts in minutes, a process that manually took hours, showcasing a dramatic efficiency improvement.

What are the key market drivers leading to the rise in the adoption of Software Industry?

- The rapid adoption of generative artificial intelligence models is a key driver propelling growth and innovation across the software market.

- Growth is propelled by the integration of generative artificial intelligence models, moving development toward intent-driven environments. A key driver is the expansion of sovereign cloud infrastructures, which cater to the increasing need for data residency and security in localized environments.

- This has led to the development of sophisticated hybrid cloud solutions and multi-cloud management tools. Simultaneously, the evolution of automated cybersecurity defense systems is critical.

- Organizations are demanding cybersecurity software with real-time automation to counter advanced threats, with automated systems detecting threats 60% faster than manual methods. This need for cloud-native security has made security a non-discretionary investment, reducing incident response times significantly.

- The use of machine learning models underpins these advancements.

What are the market trends shaping the Software Industry?

- The market is witnessing a significant trend toward the institutionalization of agentic AI. This evolution enables autonomous workflow orchestration, where systems independently manage complex business processes.

- The market's evolution is defined by the institutionalization of agentic artificial intelligence and autonomous workflow orchestration, shifting from assistive tools to fully autonomous systems. This trend involves microservices desegregation, where monolithic applications are broken into scalable microservices. Enterprises are rapidly adopting low-code development platforms, which foster citizen developer integration through intuitive visual interfaces.

- This democratization of development allows for rapid creation of application software that automates local workflows. The growth of cloud-native architectures and distributed environments supports this shift. This trend has accelerated application delivery cycles by up to 40%, with citizen-built apps showing a 25% faster time-to-market compared to traditional IT-led projects. These task-specific agents are becoming fundamental.

What challenges does the Software Industry face during its growth?

- The escalating complexity and sophistication of cybersecurity threats presents a key challenge affecting the industry's growth trajectory.

- The industry confronts significant challenges, including the threat of polymorphic malware and the complexity of credential stuffing attacks. This necessitates a move toward zero-trust architectures, but implementation can introduce latency. A primary restraint is managing technical debt during legacy system modernization, a process that can consume over 70% of IT budgets.

- The fragmentation of global regulatory frameworks and strict data sovereignty mandates create administrative burdens, with compliance overhead increasing by over 25% in some cases. The reliance on vast open-source libraries introduces systemic vulnerabilities into the software supply chain. Addressing these issues without stifling innovation requires a shift to security-by-design principles and developing automated tools for enterprise software migration.

Exclusive Technavio Analysis on Customer Landscape

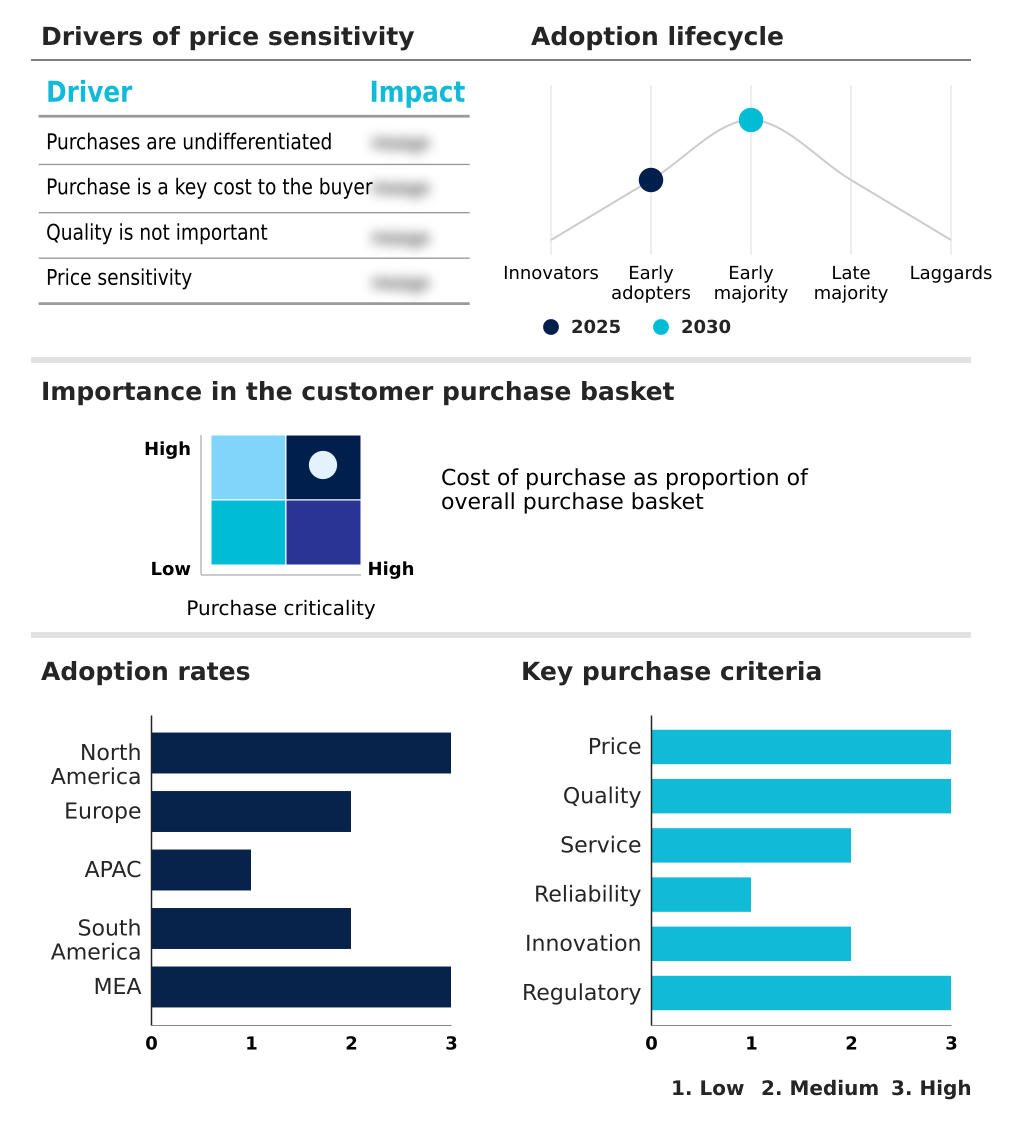

The software market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the software market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Software Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, software market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Adobe Inc. - Offers integrated software for digital media creation and document management, enabling streamlined content workflows for creative and business professionals.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adobe Inc.

- Amazon Web Services Inc.

- Atlassian Corp.

- Autodesk Inc.

- Broadcom Inc.

- CrowdStrike Inc.

- Dassault Systemes SE

- Google LLC

- IBM Corp.

- Intuit Inc.

- Microsoft Corp.

- Oracle Corp.

- Palo Alto Networks Inc.

- Salesforce Inc.

- SAP SE

- ServiceNow Inc.

- Shopify Inc.

- Snowflake Inc.

- Workday Inc.

- Zoom Communications Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Software market

- In September, 2024, Oracle Corp. announced the acquisition of a leading AI-powered code refactoring startup, aimed at enhancing its legacy system modernization tools within the Oracle Cloud Infrastructure suite.

- In November, 2024, ServiceNow Inc. launched its 'Sovereign Workflow' platform, a new suite of solutions designed to help European enterprises automate business processes while ensuring full compliance with local data residency mandates.

- In February, 2025, CrowdStrike Inc. and Snowflake Inc. formed a strategic partnership to deliver an integrated data security solution, enabling joint customers to apply real-time threat detection to massive data workloads within the Snowflake Data Cloud.

- In April, 2025, Microsoft Corp. unveiled a significant update to its Power Platform, introducing advanced generative AI templates that allow citizen developers to create complex applications using natural language prompts.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Software Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 299 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 8.6% |

| Market growth 2026-2030 | USD 34863.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 7.8% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Turkey and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The software market is defined by a structural shift toward intelligent, autonomous ecosystems. The rise of agentic artificial intelligence and the strategic necessity of sovereign cloud infrastructures are compelling executive boards to re-evaluate long-term technology investments, moving budgets from maintaining legacy systems toward adopting decentralized architectures.

- This transition is not merely technical but strategic, as autonomous workflow orchestration directly impacts operational resilience and competitive agility. For example, the integration of machine learning models into enterprise resource planning systems has enabled some manufacturers to achieve a 30% reduction in production downtime through predictive maintenance. This move toward real-time automation and cloud-native architectures is pivotal.

- The market is also heavily influenced by the need for advanced automated cybersecurity defense systems, with zero-trust architectures and endpoint detection and response becoming baseline requirements. The proliferation of low-code development platforms and software-as-a-service models further accelerates this transformation by enabling rapid, scalable deployment of business solutions.

What are the Key Data Covered in this Software Market Research and Growth Report?

-

What is the expected growth of the Software Market between 2026 and 2030?

-

USD 34.86 billion, at a CAGR of 8.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Subscriptions, Identity and access management, Network security, and Risk management), Deployment (Cloud-based, and On-premises), Sector (Large enterprises, and Small and medium enterprises) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Adoption of generative artificial intelligence models, Escalating complexity of complexity and sophisticated threat

-

-

Who are the major players in the Software Market?

-

Adobe Inc., Amazon Web Services Inc., Atlassian Corp., Autodesk Inc., Broadcom Inc., CrowdStrike Inc., Dassault Systemes SE, Google LLC, IBM Corp., Intuit Inc., Microsoft Corp., Oracle Corp., Palo Alto Networks Inc., Salesforce Inc., SAP SE, ServiceNow Inc., Shopify Inc., Snowflake Inc., Workday Inc. and Zoom Communications Inc.

-

Market Research Insights

- The market's dynamism is fueled by a strategic shift toward autonomous systems and digital agents that orchestrate complex business workflows. This digital transformation is underpinned by the proliferation of cloud-native security and open-source frameworks, enabling organizations to build resilient, distributed environments.

- The adoption of visual interfaces in software development has empowered non-technical users, with some firms reporting a 40% reduction in application backlogs. Furthermore, the move from perpetual licensing to subscription models provides continuous value delivery. Enhanced security through adaptive risk-based assessments and self-sovereign identity solutions has improved compliance reporting accuracy by over 25% for regulated industries.

- These advancements, combined with real-time analytics, are creating a more agile and data-driven enterprise landscape.

We can help! Our analysts can customize this software market research report to meet your requirements.

RIA -

RIA -