DDOS Protection Mitigation Market Size 2024-2028

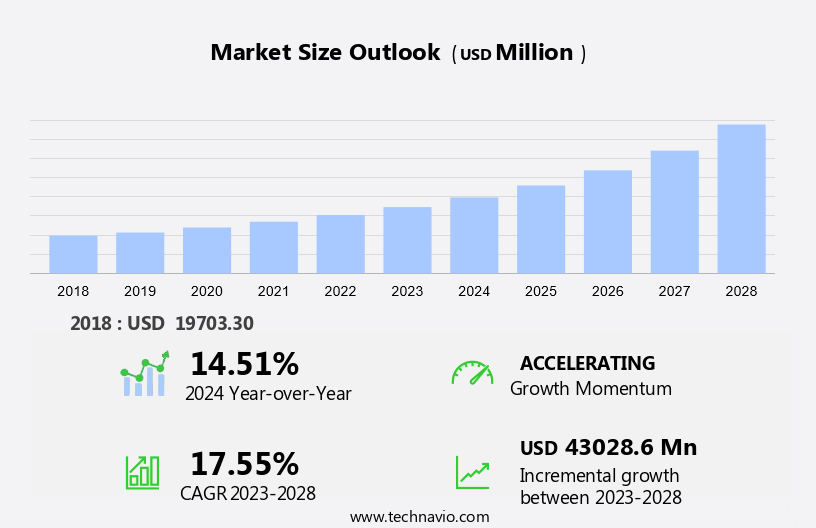

The DDOS protection mitigation market size is forecast to increase by USD 43.03 billion at a CAGR of 17.55% between 2023 and 2028. Market growth hinges on several factors such as the uptick in Distributed Denial-of-Service attacks, escalating reliance on digital services as a primary driver, and the strategic utilization of cyber insurance. As the digital landscape expands, so does vulnerability to cyber threats, elevating the need for strong protection measures. Organizations increasingly prioritize cybersecurity investments, with cyber insurance emerging as a critical component in risk mitigation strategies. The rise of OpenRAN-based 5G networks has introduced new challenges, necessitating strong protection for HTTP servers and other network components. The rise in Distributed Denial-of-Service attacks underscores the urgency for enhanced cybersecurity solutions and proactive defense mechanisms. Leveraging cyber insurance not only safeguards against financial losses but also fosters a culture of resilience in the face of evolving cyber threats, driving market growth and fortifying digital ecosystems.

The market is rapidly growing, driven by the increasing frequency of DDoS attacks, including ransom DDoS attacks, targeting enterprises and critical infrastructures. These attacks often lead to significant financial and personal losses, especially in emerging economies, where IT and telecom companies are under pressure to deploy effective defense mechanisms. Regulatory and compliance requirements are also pushing businesses to adopt more sophisticated DDoS mitigation strategies. Gaming, educational platforms, and various online services are particularly vulnerable, making proactive DDoS protection essential. As DDoS attacks evolve, enterprises must prioritize comprehensive solutions to safeguard their digital assets and operations.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Network security

- Application security

- Database security

- Endpoint security

- Component

- Hardware solution

- Software solution

- Services

- Geography

- North America

- Canada

- US

- Europe

- Germany

- APAC

- China

- Japan

- South America

- Middle East and Africa

- North America

By Application Insights

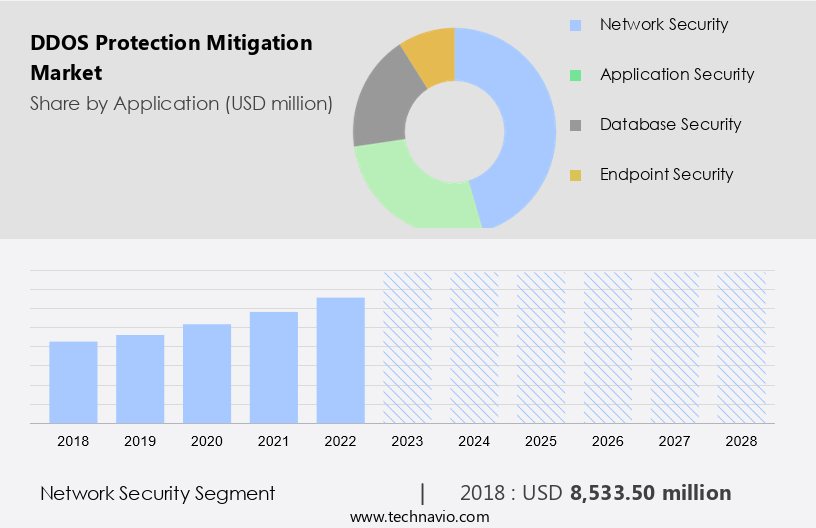

The network security segment is estimated to witness significant growth during the forecast period. Distributed Denial of Service (DDoS) attacks pose a significant threat to network security by flooding servers or networks with excessive traffic, rendering them unreachable for legitimate users. Businesses and organizations rely on DDoS protection and mitigation solutions to safeguard their websites and online services from such attacks. For e-commerce platforms, financial institutions, and other businesses with a strong online presence, ensuring uninterrupted access to their services is essential to prevent substantial financial losses due to customer disruption.

Additionally, securing critical infrastructure, including power grids, water treatment facilities, and hospitals, is another crucial application of DDoS protection and mitigation. Protocol-specific attacks, such as Memcached Amplification and Jenkins DoS, pose a growing concern in the telecom industry. These attacks can reach gigabit-per-second levels, making it imperative for organizations to invest in advanced DDoS protection and mitigation solutions.

Get a glance at the market share of various segments Request Free Sample

The network security segment was valued at USD 8.53 billion in 2018 and showed a gradual increase during the forecast period.

Regional Insights

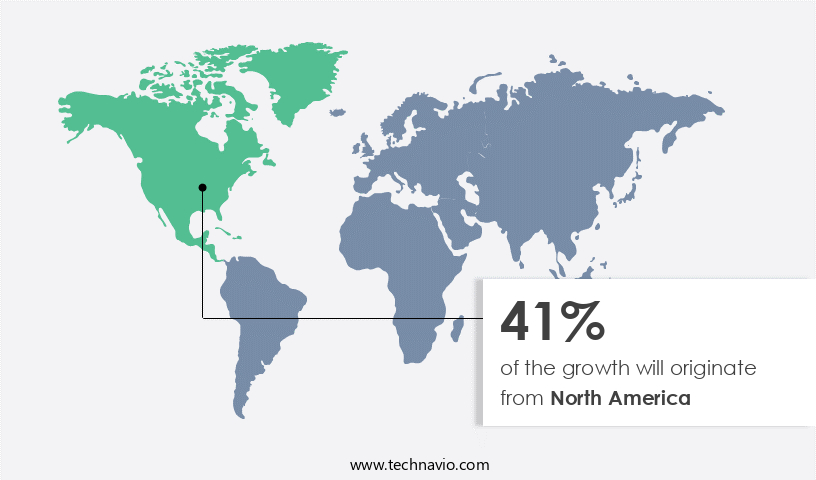

North America is estimated to contribute 41% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

In North America, the DDoS protection and mitigation market is experiencing significant growth due to the region's technological advancements and increasing cybersecurity threats. Major tech companies, including Apple, Microsoft, Intel, Google, Oracle, IBM, and NVIDIA, are based in North America and are constantly innovating to stay competitive. The region's heavy reliance on the internet and digital services has led to a ripple in demand for DDoS protection solutions. This demand is driven by the rise in Botnet DDoS attacks, the expansion of IoT and cloud computing, and the growing popularity of cyber insurance. Cloud-native DDoS protection tools are particularly in demand, as they offer scalability and flexibility.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

The growing number of DDoS attack is the key driver of the market. The number of DDoS attacks has been on the rise, posing a significant threat to various industries, including medical organizations and delivery services. These network attacks occur when an overwhelming amount of traffic is directed to a target system from multiple compromised devices. The wave in internet-connected devices, increasing dependence on digital services, and the growing pool of cybercriminals seeking to exploit these services are some factors fueling the increase in DDoS attacks.

Consequently, businesses are compelled to invest in DDoS protection solutions to safeguard against potential financial losses, damage to reputation, and operational disruption. These attacks can cause substantial harm, making it essential for organizations to implement strong security measures to mitigate the risk.

Market Trends

Strategic initiatives by companies is the upcoming trend in the market. Recent advancements in the market indicate several noteworthy trends among key players. In October 2022, Akamai unveiled an upgraded DDoS protection platform, Prolexic, featuring new software-defined scrubbing centers with a 20 Tbps dedicated defense capacity. In April 2021, Radware launched Cloud DDoS Protection Service, designed to secure cloud-based services and applications.

Further, this tool offers precise network traffic control to minimize false positives and utilizes advanced machine learning algorithms and real-time threat intelligence for detecting and mitigating DDoS attacks. Frequency and sophistication of attack vectors, including SYN, RST, and UDP floods, continue to challenge organizations. These solutions aim to provide effective defense against diverse and evolving threats.

Market Challenge

DDoS protection solutions deployment and management complexity is a key challenge affecting the market growth. DDoS protection mitigation is a critical aspect for safeguarding business systems and individual users from extortionate attacks. These malicious acts can lead to significant financial burdens and potential loss of user loyalty. Cloudflare, a leading DDoS protection provider, highlights the importance of effective DDoS protection solutions. However, implementing and managing these solutions can be intricate. They require a deep understanding of networking protocols, security best practices, and the latest DDoS attack techniques and tools.

Moreover, real-time response to DDoS attacks can be challenging due to the intricacy of deployment and management, which may hinder organizations from promptly recognizing and halting the attacks. In summary, DDoS protection mitigation is a vital investment for businesses and individuals to secure their systems and maintain user loyalty, but its implementation and management necessitate specialized expertise and resources.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Corero Network Security Plc - The company offers Cloudflare distributed denial of service protection solutions.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- A10 Networks Inc.

- Akamai Technologies Inc.

- Amazon.com Inc.

- BT Group Plc

- Cloudflare Inc.

- DDoS-Guard

- F5 Inc.

- Fastly Inc.

- Fortinet Inc.

- Haltdos Inc. Ltd.

- Huawei Technologies Co. Ltd.

- Imperva Inc.

- Link11 GmbH

- NetScout Systems Inc.

- Nexusguard Inc.

- Radware Ltd.

- Ribbon Communications Inc.

- Sitelock LLC

- TransUnion

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

DDOS attacks, a type of cyber threat, pose significant risks to various industries, including medical organizations and delivery services. These network attacks, orchestrated by criminals with a growing understanding of extortion and user loyalty, can cause business systems to crash or become unavailable, leading to financial burdens and damage to user trust. DDOS protection solutions are essential in mitigating these threats, which can come in various forms, such as SYN and RST floods, UDP floods, protocol-specific attacks like MDNS and Memcached, Jenkins DOS attacks, and botnet attacks. The sophistication and frequency of these attacks continue to evolve, with some reaching gigabit-per-second levels.

Further, the telecom industry, data centers, and financial institutions are prime targets, as are HTTP servers and 5G networks. The emergence of IoT devices, mobiles, remote working, and cloud-native applications adds to the complexity of DDOS protection.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

171 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 17.55% |

|

Market Growth 2024-2028 |

USD 43.03 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

14.51 |

|

Regional analysis |

North America, Europe, APAC, South America, and Middle East and Africa |

|

Performing market contribution |

North America at 41% |

|

Key countries |

US, Germany, Canada, China, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

A10 Networks Inc., Akamai Technologies Inc., Amazon.com Inc., BT Group Plc, Cloudflare Inc., Corero Network Security Plc, DDoS-Guard, F5 Inc., Fastly Inc., Fortinet Inc., Haltdos Inc. Ltd., Huawei Technologies Co. Ltd., Imperva Inc., Link11 GmbH, NetScout Systems Inc., Nexusguard Inc., Radware Ltd., Ribbon Communications Inc., Sitelock LLC, and TransUnion |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -