Cyber Insurance Market Size 2026-2030

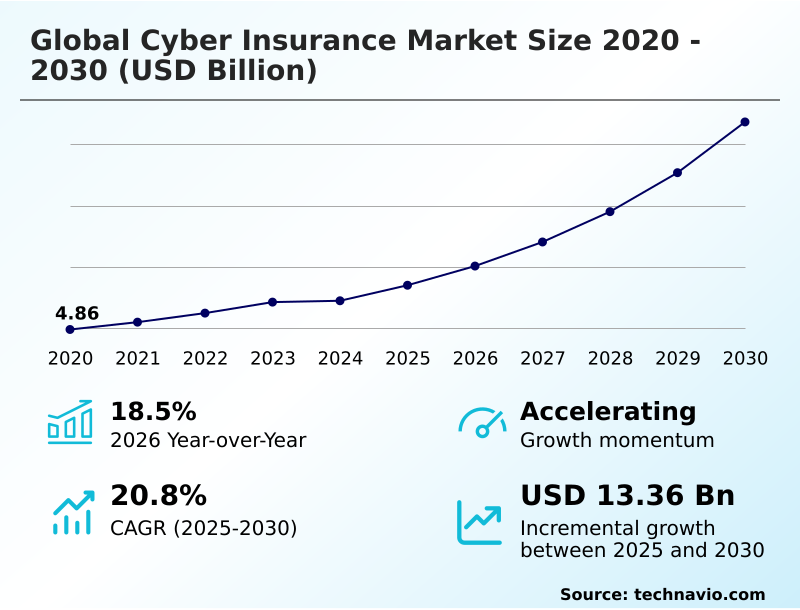

The cyber insurance market size is valued to increase by USD 13.36 billion, at a CAGR of 20.8% from 2025 to 2030. Increasing financial and operational imperative from advanced cyber threats will drive the cyber insurance market.

Major Market Trends & Insights

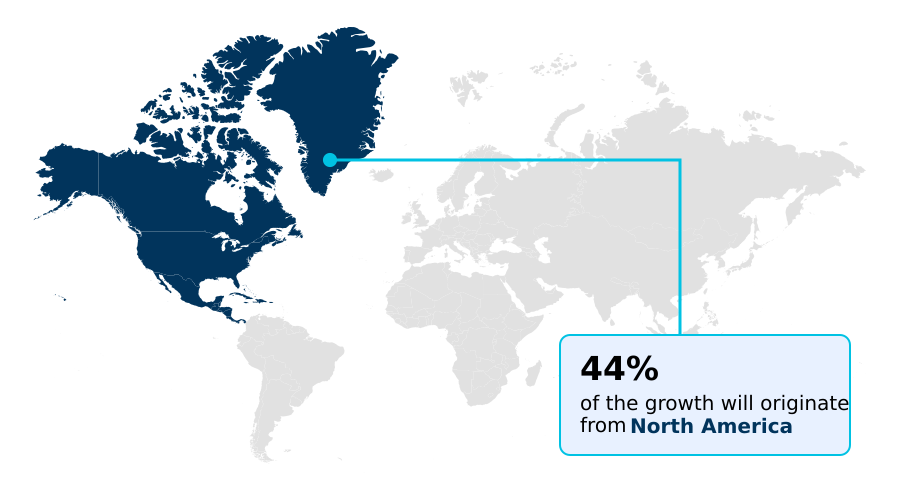

- North America dominated the market and accounted for a 44.3% growth during the forecast period.

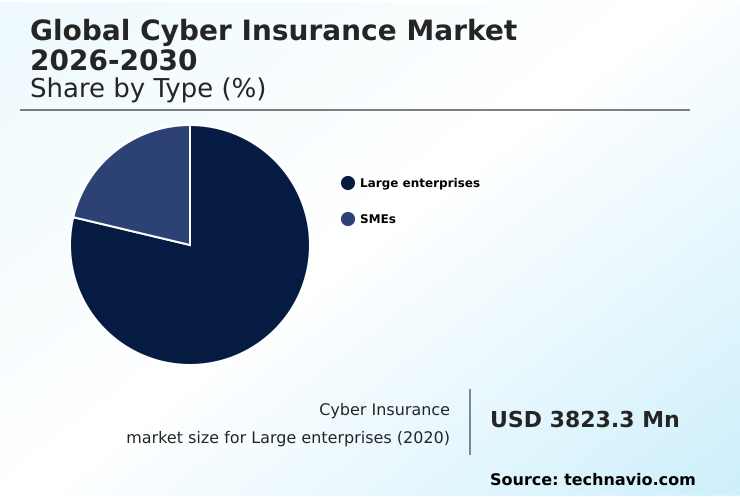

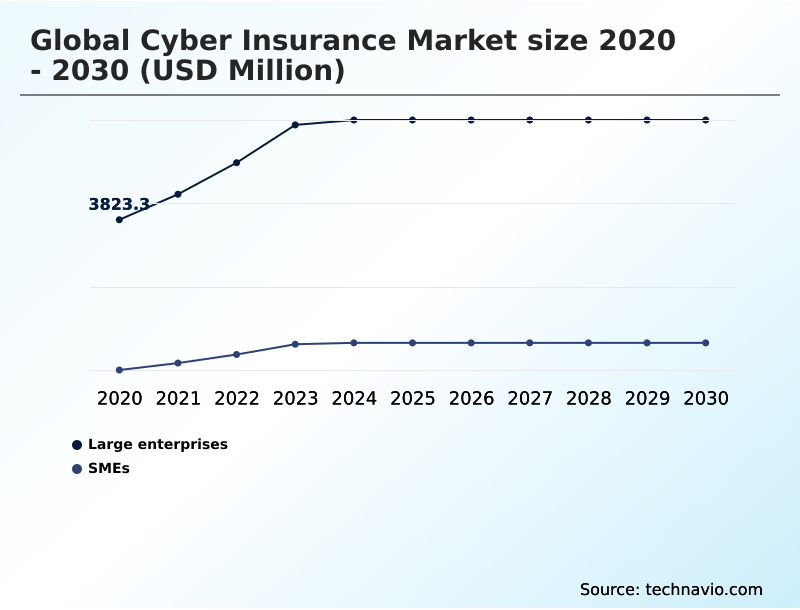

- By Type - Large enterprises segment was valued at USD 5.68 billion in 2024

- By Solution - Standalone segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 16.98 billion

- Market Future Opportunities: USD 13.36 billion

- CAGR from 2025 to 2030 : 20.8%

Market Summary

- The cyber insurance market is undergoing a critical transformation, driven by an increasingly severe threat landscape where financial indemnity alone is insufficient. Organizations now seek comprehensive risk transfer strategies that address not only data breaches but also catastrophic business interruption and reputational damage from double-extortion scenarios.

- A key trend is the shift toward proactive risk mitigation, where insurers partner with clients, leveraging security ratings platforms and continuous risk evaluation to improve cyber resilience. This symbiotic relationship is reflected in evolving underwriting standards, which demand robust cybersecurity controls as a prerequisite for coverage.

- For instance, a global logistics firm facing a supply-chain cyber incident could suffer operational paralysis far exceeding the cost of data recovery; its ability to secure coverage would depend on demonstrating advanced digital risk protection and incident response capabilities.

- Challenges such as systemic cyber risk and the potential for correlated losses from a single-point-of-failure modelling are compelling the industry to innovate with solutions like parametric triggers and alternative capital solutions, ensuring market stability and relevance.

What will be the Size of the Cyber Insurance Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Cyber Insurance Market Segmented?

The cyber insurance industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Large enterprises

- SMEs

- Solution

- Standalone

- Packaged

- Product type

- Analytics platform

- Risk assessment

- Disaster recovery and business continuity

- Resilience

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- North America

By Type Insights

The large enterprises segment is estimated to witness significant growth during the forecast period.

The large enterprises segment constitutes the most mature portion of the market, where organizations face persistent and sophisticated business continuity threats.

For these entities, procurement is driven by intense board-level pressure and regulatory mandates, necessitating highly customized policies with significant policy coverage limits. The underwriting process is rigorous, demanding detailed proof of proactive risk mitigation and cyber resilience.

A key development shaping this segment is the heightened awareness of systemic cyber risk, stemming from attacks on shared technology platforms.

This has spurred a significant uptick in demand for alternative capital solutions, including cyber catastrophe bonds and policies with parametric triggers, as firms seek more dependable protection against widespread operational disruptions, improving incident containment by over 15% through proactive cybersecurity services.

The Large enterprises segment was valued at USD 5.68 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 44.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Cyber Insurance Market Demand is Rising in North America Get Free Sample

The geographic dynamics of the market are characterized by varying levels of maturity and growth.

North America remains the largest segment, contributing over 44% of the incremental growth, driven by a stringent regulatory environment and a high concentration of enterprises demanding extensive policy coverage limits.

In contrast, APAC is emerging as the fastest-growing region, with adoption rates increasing by nearly 30% as organizations address expanding attack surface management challenges. Europe is also experiencing robust growth, fueled by strict data privacy laws.

Across all regions, the demand for specialized underwriting and hyper-niche coverage is growing.

Insurers are leveraging advanced cyber risk modeling and actuarial data to develop tailored solutions, addressing specific regional threats like coordinated ransomware deployment and ensuring compliance with local mandates.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Navigating the complexities of the global cyber insurance market 2026-2030 requires a nuanced understanding of how coverage is adapting to new threats. The debate over standalone vs packaged cyber policies continues, with larger organizations favoring bespoke, standalone options that offer higher limits and specific protections. Understanding the cost of cyber incident response is critical, as it often dictates policy selection.

- For smaller businesses, the primary cyber insurance for smes challenges revolve around affordability and meeting stringent underwriting standards for cyber policies. A key aspect is the role of analytics in cyber insurance, where data-driven risk assessment in cyber underwriting is becoming standard practice.

- This analytical approach is crucial for managing systemic risk in cyber insurance and addressing the challenges of cyber risk aggregation. Insurers are also exploring parametric insurance for cyber events as an alternative to traditional indemnity models. The market is heavily shaped by cyber insurance regulatory compliance impact, which mandates certain coverage levels in critical sectors.

- Consequently, understanding data breach liability coverage details and policies for business interruption insurance for cyberattacks, including specific cyber extortion and ransomware policies, is essential. The impact of silent cyber exclusion has further clarified the need for explicit third-party cyber risk insurance.

- Ultimately, the benefits of security ratings platforms and proactive cyber risk mitigation services are clear, as firms using them report recovery times up to 50% faster, and a transparent cyber insurance claims process explained to clients builds necessary trust.

What are the key market drivers leading to the rise in the adoption of Cyber Insurance Industry?

- The primary market driver is the escalating financial and operational imperative for organizations to mitigate the impact of sophisticated, advanced cyber threats.

- The market's primary driver is the severe financial impact of sophisticated cyber threats, which now extend far beyond simple data theft to include catastrophic business interruption.

- The rise of double-extortion scenarios and attacks on critical cloud infrastructure breaches has made robust risk transfer strategies an executive-level priority.

- Organizations recognize that even strong defenses can be penetrated, making coverage for business interruption, incident response remediation, and regulatory fines protection essential for operational continuity.

- The financial protection afforded by first-party cyber coverage is critical, with analysis showing that insured firms recover financially from major incidents up to 60% faster.

- As threat actors target interconnected supply-chain cyber incidents, the need for comprehensive protection against these cascading events continues to accelerate market growth and drive innovation in policy offerings.

What are the market trends shaping the Cyber Insurance Industry?

- A dominant market trend marks the evolution from traditional risk transfer models toward active risk mitigation partnerships. Insurers are increasingly functioning as proactive allies in managing cyber resilience.

- A dominant trend reshaping the market is the shift from providing passive financial indemnity to fostering active risk management partnerships. Insurers are leveraging API-driven risk intelligence and data-driven insights to embed themselves within their clients' cybersecurity ecosystems. This collaborative approach, which includes offering vulnerability monitoring and incident response support, enables continuous risk evaluation.

- By utilizing advanced portfolio risk analytics, carriers can better model potential exposures and incentivize policyholders to enhance their cyber resilience. The adoption of such proactive cybersecurity services has been shown to reduce critical security alerts by up to 30%.

- Furthermore, this model strengthens loss prevention efforts and allows for more specialized underwriting, ensuring that coverage accurately reflects an organization's security posture and preparedness for events like a zero-day vulnerability exploit.

What challenges does the Cyber Insurance Industry face during its growth?

- A primary challenge affecting industry growth is the rising tide of systemic cyber threats and the consequent aggregation risk for the insurance ecosystem.

- A primary challenge confronting the market is the escalating threat of systemic events that can trigger catastrophic and correlated losses across entire portfolios. A single managed IT services compromise can cascade through digital supply chains, leading to an overwhelming volume of claims that threaten insurer solvency.

- This risk aggregation is difficult to quantify, leading to uncertainty in pricing and the introduction of more restrictive terms, such as broader exclusions for non-affirmative coverage. To combat this, some insurers are imposing co-insurance clauses for up to 50% of losses stemming from such systemic breaches.

- The industry is also responding with alternative capital solutions and more sophisticated catastrophe modelling to better prepare for a large-scale, coordinated ransomware deployment, but the potential for widespread, simultaneous disruption remains a significant constraint on market capacity and stability.

Exclusive Technavio Analysis on Customer Landscape

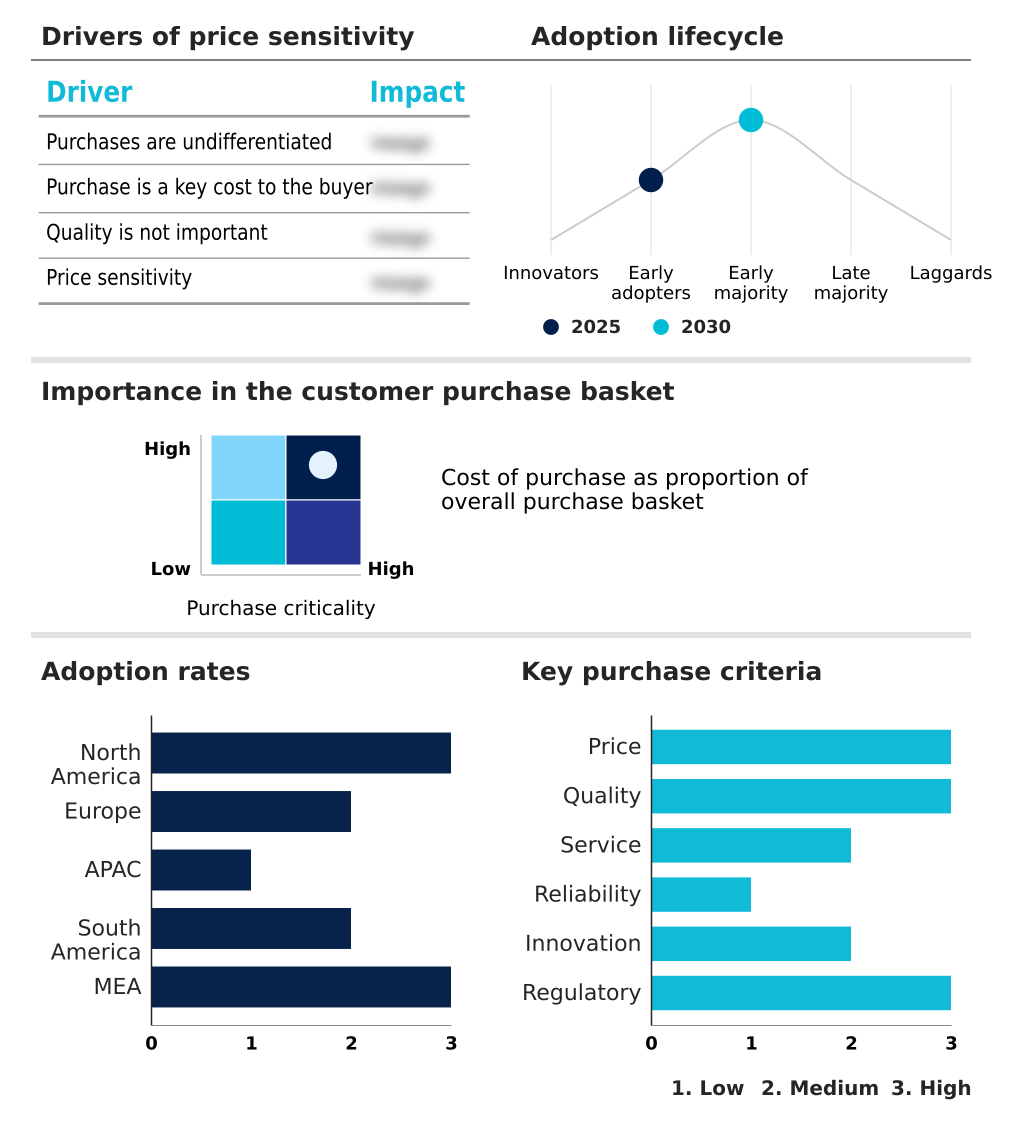

The cyber insurance market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the cyber insurance market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Cyber Insurance Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, cyber insurance market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

American International Group - Delivers comprehensive cyber insurance covering data breaches, business interruption, and liability, complete with expert incident response and forensic support.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- American International Group

- Aon plc

- At Bay Inc.

- AXA XL

- BCS Financial Corp.

- Beazley Plc

- BitSight Technologies Inc.

- CFC Underwriting Ltd

- Chubb Ltd.

- CNA Financial Corp.

- Coalition Inc.

- Guy Carpenter and Co LLC

- Hanover Insurance Group Inc

- Lloyds Banking Group Plc

- Lockton Co.

- SecurityScorecard Inc.

- Tata Consultancy Services

- The Travelers Co. Inc.

- Zurich Insurance Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Cyber insurance market

- In February 2025, Chubb and Aon collaborated to introduce a standardized assessment protocol designed to pinpoint and address vulnerabilities within the digital infrastructures of multinational corporations, with a specific focus on mitigating risks associated with third-party software dependencies.

- In May 2025, Coalition and SecurityScorecard initiated a partnership to furnish policyholders with automated security alerts, facilitating the immediate remediation of critical cyber threats and enhancing proactive defense postures.

- In April 2025, CFC launched a cyber proactive response product, which features broader coverage and fewer exclusions, thereby strengthening the value proposition for enterprise clients seeking more comprehensive protection.

- In April 2025, K2 Cyber formed a partnership with TransUnion, granting its policyholders access to a suite of advanced services, including incident response remediation, forensic consultation, and robust identity theft prevention tools.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Cyber Insurance Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 292 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 20.8% |

| Market growth 2026-2030 | USD 13355.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 18.5% |

| Key countries | US, Canada, Mexico, UK, Germany, France, Italy, Spain, The Netherlands, China, Japan, India, Australia, South Korea, Singapore, Brazil, Argentina, Chile, UAE, Saudi Arabia, South Africa, Israel and Qatar |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The cyber insurance market is defined by a fundamental shift toward rigorous, evidence-based underwriting. The integration of advanced cyber risk modeling, vulnerability intelligence, and security ratings platforms allows for precise cyber risk quantification, which has improved loss prediction accuracy by over 25% for leading carriers.

- This evolution is compelling a strategic realignment at the boardroom level; securing adequate coverage is no longer a simple procurement task but a reflection of an organization's commitment to proactive risk mitigation. Stringent underwriting standards now mandate robust digital risk protection and attack surface management as prerequisites for obtaining favorable policy coverage limits.

- Insurers are enhancing their claims support with forensic investigation support and cybersecurity advisory services, moving beyond mere financial reimbursement. The market is also innovating with solutions like cyber catastrophe bonds and parametric triggers to manage systemic cyber risk and risk aggregation modeling challenges.

- This dynamic landscape necessitates that organizations view their claims management infrastructure and reinsurance arrangements as integral components of their overall resilience strategy.

What are the Key Data Covered in this Cyber Insurance Market Research and Growth Report?

-

What is the expected growth of the Cyber Insurance Market between 2026 and 2030?

-

USD 13.36 billion, at a CAGR of 20.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Large enterprises, and SMEs), Solution (Standalone, and Packaged), Product Type (Analytics platform, Risk assessment, Disaster recovery and business continuity, and Resilience) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing financial and operational imperative from advanced cyber threats, Rising tide of systemic cyber threats and aggregation risk

-

-

Who are the major players in the Cyber Insurance Market?

-

American International Group, Aon plc, At Bay Inc., AXA XL, BCS Financial Corp., Beazley Plc, BitSight Technologies Inc., CFC Underwriting Ltd, Chubb Ltd., CNA Financial Corp., Coalition Inc., Guy Carpenter and Co LLC, Hanover Insurance Group Inc, Lloyds Banking Group Plc, Lockton Co., SecurityScorecard Inc., Tata Consultancy Services, The Travelers Co. Inc. and Zurich Insurance Co. Ltd.

-

Market Research Insights

- The market's momentum is defined by a strategic pivot toward proactive, data-driven risk management. Insurers are embedding proactive cybersecurity services into offerings, a move that has helped policyholders reduce claim frequency by up to 25%.

- The use of continuous risk evaluation, supported by advanced risk modeling tools, allows for more precise cyber risk quantification and has improved underwriting accuracy by over 30%. This emphasis on active risk management is critical as organizations grapple with complex digital supply chain risk and contingent business interruption threats.

- As a result, comprehensive cyber resilience programs that integrate insurance with preemptive security measures are becoming the standard for mitigating an organization's overall cyber risk exposure and ensuring operational continuity in the face of persistent threats.

We can help! Our analysts can customize this cyber insurance market research report to meet your requirements.

RIA -

RIA -