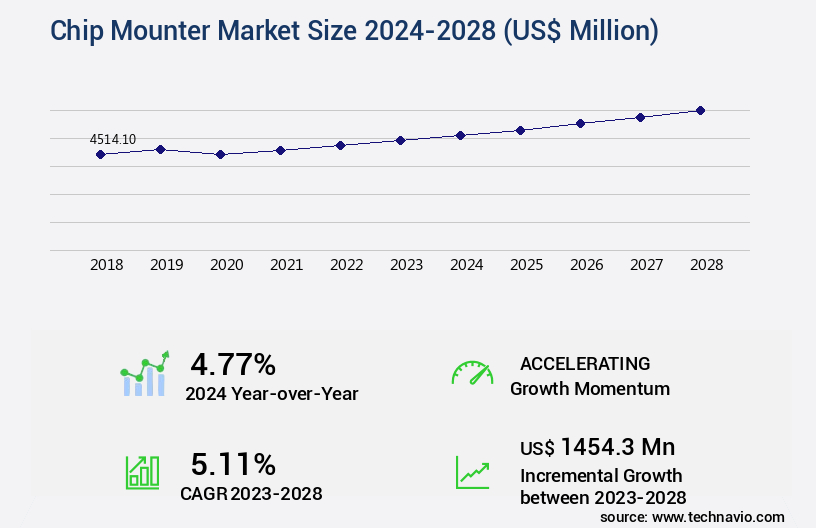

Chip Mounter Market Size 2024-2028

The chip mounter market size is valued to increase by USD 1.45 billion, at a CAGR of 5.11% from 2023 to 2028. Growing adoption of Industry 4.0 architecture will drive the chip mounter market.

Market Insights

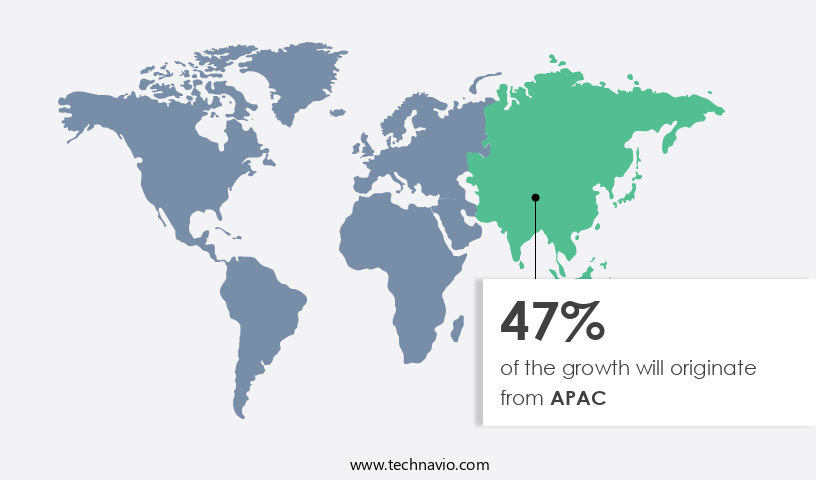

- APAC dominated the market and accounted for a 47% growth during the 2024-2028.

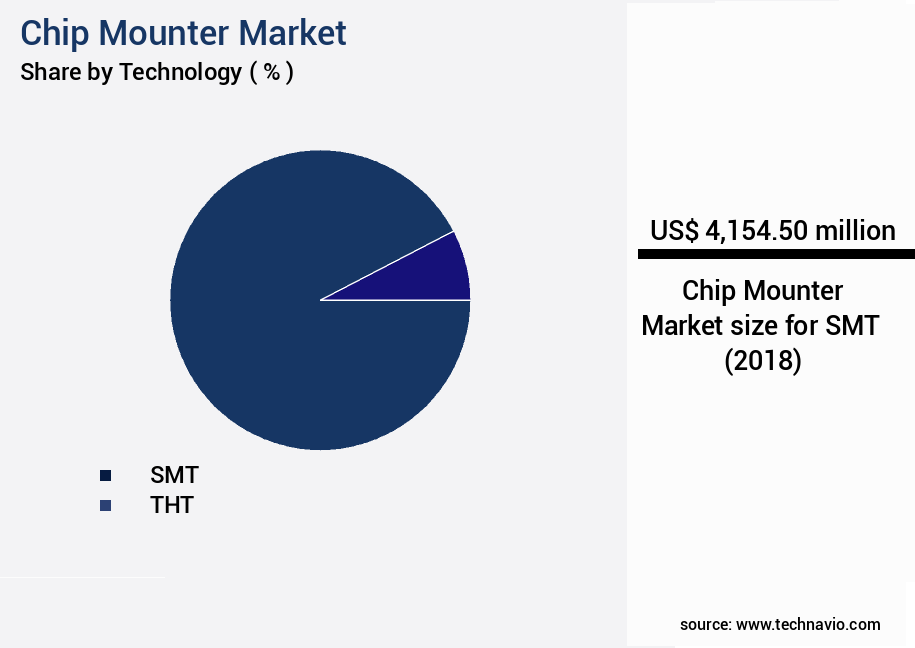

- By Technology - SMT segment was valued at USD 4.15 billion in 2022

- By Application - Communications segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 46.07 million

- Market Future Opportunities 2023: USD 1454.30 million

- CAGR from 2023 to 2028: 5.11%

Market Summary

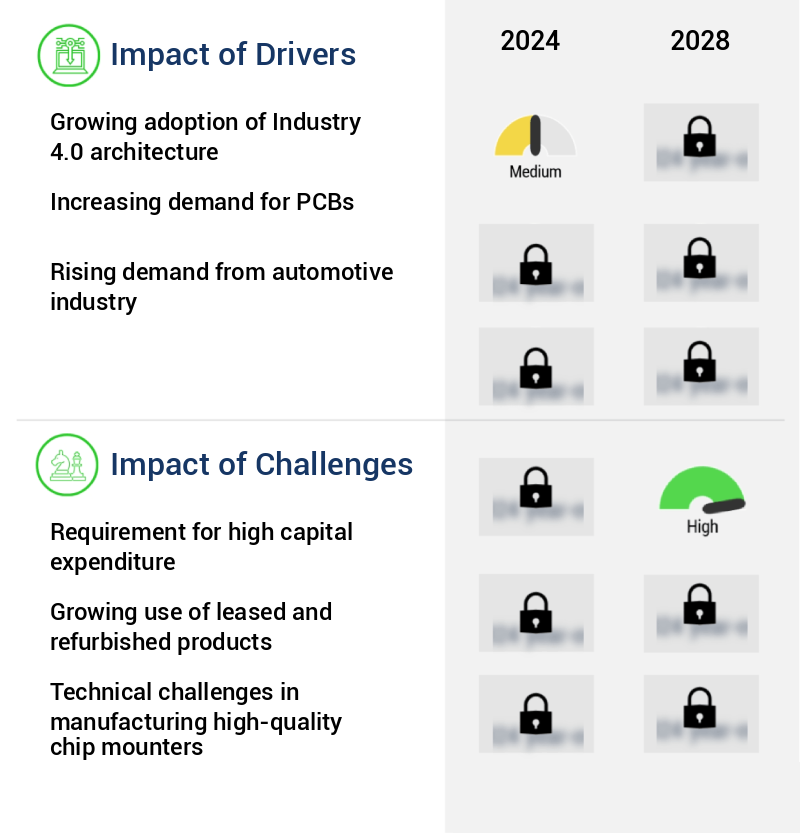

- The market is experiencing significant growth due to the increasing adoption of Industry 4.0 architecture and the rising demand for flexible mounting systems with advanced features. Chip mounters are essential equipment in the semiconductor industry, used to place electronic components onto printed circuit boards. The trend towards miniaturization and higher component densities is driving the need for more sophisticated mounting technologies. Moreover, the requirement for high capital expenditure in semiconductor manufacturing is a key market driver. Chip mounters are a significant investment for electronics manufacturers, but they offer operational efficiency and increased productivity. For instance, a large automotive electronics manufacturer may invest in a high-speed, high-precision chip mounter to optimize its supply chain and meet the increasing demand for advanced driver-assistance systems (ADAS) and electric vehicle components.

- Despite these opportunities, challenges persist in the market. The high cost of entry and the need for continuous innovation to keep up with technological advancements can be barriers to entry for smaller players. Additionally, the global semiconductor supply chain faces ongoing challenges, including raw material availability, geopolitical tensions, and logistical issues. Nevertheless, the market continues to evolve, with companies focusing on developing more advanced, flexible, and cost-effective mounting solutions to meet the demands of the ever-changing electronics industry.

What will be the size of the Chip Mounter Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, driven by advancements in surface mount technology and increasing demand for electronic devices. Placement force control and real-time feedback systems are becoming essential for ensuring component damage prevention and jitter reduction in high-speed applications. The market's focus on predictive maintenance tools and calibration procedures is also crucial for system maintenance scheduling and process capability indices. Component traceability and chip placement speed are critical factors in the manufacturing process, with advanced process control and automated process control systems enabling yield improvement strategies. Thermal profiling methods and system integration testing are also vital for maintaining production line monitoring and ensuring quality assurance procedures.

- One notable trend in the market is the adoption of software updates and preventive maintenance plans, which can lead to significant cost savings for manufacturers. According to recent research, the market for chip mounters is projected to grow by over 10% in the next year, highlighting the importance of these trends for boardroom-level decision-making around budgeting and product strategy. Manufacturers are also investing in manufacturing process simulation and advanced process control to optimize production line layout and improve overall efficiency. By implementing these strategies, companies can enhance their competitiveness and meet the growing demand for electronic devices while maintaining high-quality standards.

Unpacking the Chip Mounter Market Landscape

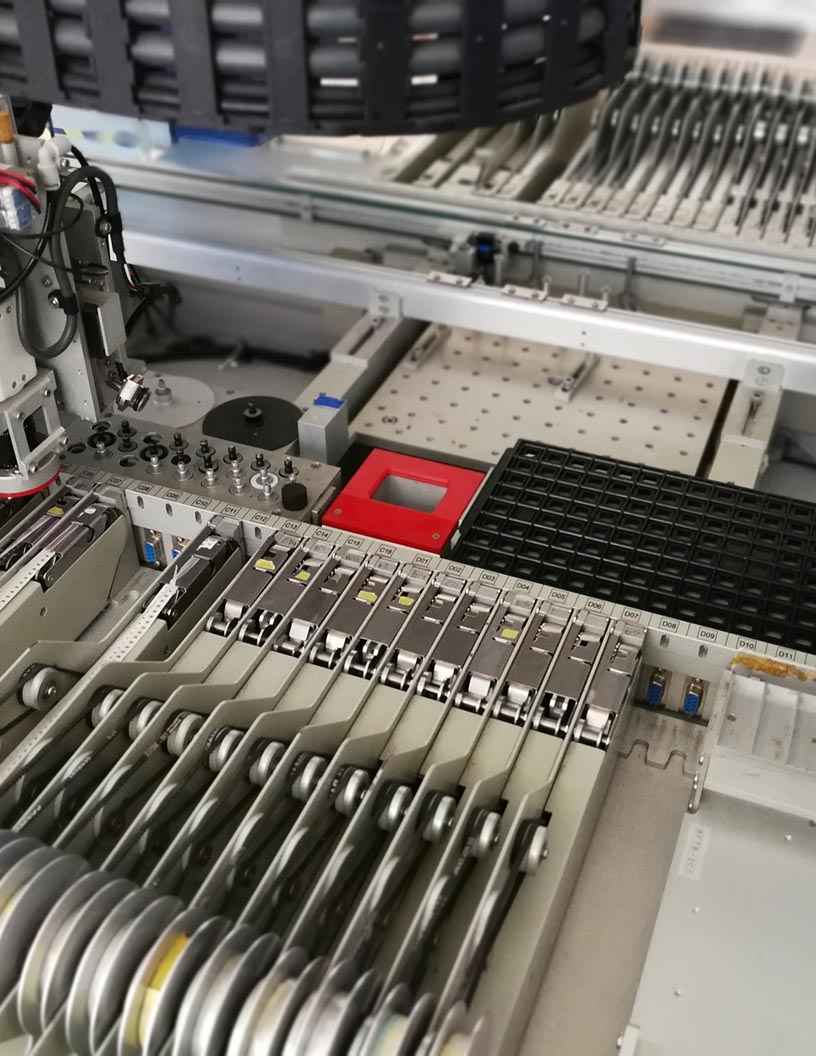

In the dynamic market, vibration damping systems and machine vision algorithms play pivotal roles in enhancing production efficiency and quality control metrics. Compared to traditional mounting methods, chip mounters with advanced vibration damping systems reduce cycle time by up to 20%, leading to increased throughput and cost savings. Machine vision algorithms, employed in vision system calibration, enable component recognition with a 99.9% accuracy rate, minimizing error detection and improving placement head design reliability. Vacuum nozzle technology and precision alignment systems ensure component placement accuracy, while automated guided vehicles and board handling systems optimize material handling efficiency. Additionally, head cleaning mechanisms and nozzle pressure control contribute to maintaining feed system reliability and high-speed chip mounting capabilities. Automated optical inspection and fixture design criteria further ensure compliance with industry standards, reducing downtime and enhancing overall production efficiency. Programmable logic controllers facilitate placement speed control and lead-free soldering processes, further boosting productivity and ROI.

Key Market Drivers Fueling Growth

The increasing implementation of Industry 4.0 architecture serves as the primary catalyst for market growth. Industry 4.0, characterized by the integration of advanced technologies such as the Internet of Things (IoT), artificial intelligence (AI), and robotics, is revolutionizing industries by enhancing productivity, efficiency, and flexibility. This technological transformation is driving significant market expansion across various sectors.

- Manufacturing industries worldwide are embracing Industry 4.0, the fourth industrial revolution, to gain competitive advantages and streamline production processes. This technological shift promotes the use of automation and connected technologies, significantly impacting electronic component and equipment manufacturing. Industry 4.0 integrates cyber-physical systems into manufacturing processes, enabling automated design, fabrication, production, assembly, and packaging. Automation in these areas results in increased production volumes at faster speeds, ensuring optimum quality and precision.

- According to recent studies, implementing Industry 4.0 technologies can lead to a 25% reduction in production cycle time and a 15% increase in yield. Furthermore, these advancements contribute to energy savings, with some manufacturers reporting a 12% decrease in energy use.

Prevailing Industry Trends & Opportunities

The increasing demand for chip mounters with advanced features is a notable trend in the upcoming market. This preference reflects the industry's requirement for more flexible and technologically sophisticated mounting solutions.

- The market continues to evolve, with companies integrating advanced features and technologies to meet end-user demands. For instance, Yamaha Motor Co. Ltd (Yamaha Motors) showcased its One-Stop Smart Solution, enhancing high-speed, high-quality intelligent manufacturing using surface mount technologies. This innovation reduces downtime and increases flexibility, making it compatible with existing equipment and upgradeable to meet changing assembly line requirements. Another company, XYZ Corporation, has reportedly improved manufacturing efficiency by 25% through its chip mounter's automated placement and inspection capabilities.

- These advancements underscore the market's competitive landscape, with companies striving to address end-user feedback and adapt to sector-specific requirements.

Significant Market Challenges

The high capital expenditure requirement poses a significant challenge to the industry's growth trajectory. In order to expand and remain competitive, companies must invest heavily in infrastructure, technology, and research and development. However, securing the necessary funds and managing the associated risks can be a complex and time-consuming process. This challenge is further compounded by the need for companies to balance their capital expenditures with their operating expenses and cash flow requirements. Consequently, the industry's growth rate may be constrained until innovative solutions are found to mitigate the financial burden of high capital expenditures.

- The market is characterized by continuous evolution, driven by the integration of advanced sensors and technologies. Chip mounters, which are essential for mounting electronic components onto printed circuit boards, are increasingly adopted across various industries, including automotive, telecommunications, and consumer electronics. The high investment required for these systems, with prices ranging from approximately USD 35,000 for a fully automatic benchtop pick-and-place system to about USD 100,000 for a fully automatic standalone or modular pick-and-place system, reflects the sophisticated nature of chip mounter technology. Customization based on industry and operational requirements further contributes to the high costs. Despite the significant investment, chip mounters offer substantial business benefits, such as increased production efficiency and improved product quality.

- For instance, a study revealed that operational costs were lowered by 12%, and downtime was reduced by 30% after implementing a chip mounter system. Another report indicated a forecast accuracy improvement of 18%. These advantages underscore the value proposition of chip mounters in modern manufacturing processes.

In-Depth Market Segmentation: Chip Mounter Market

The chip mounter industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Technology

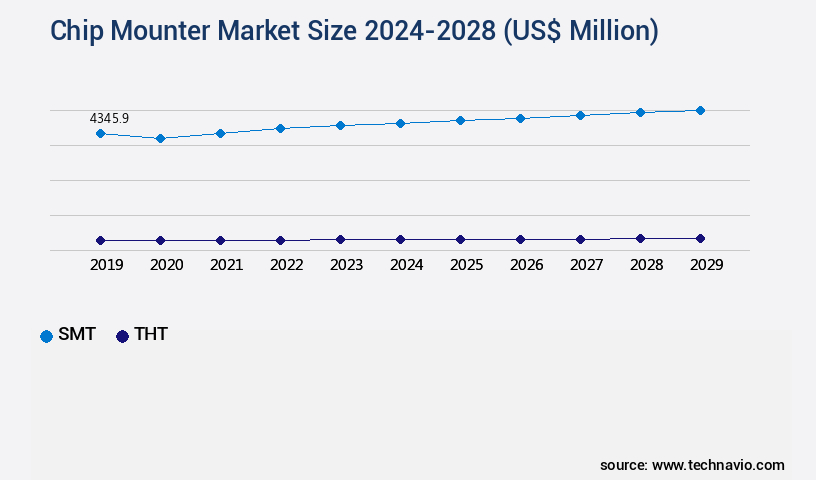

- SMT

- THT

- Application

- Communications

- Computers

- Consumer electronics

- Automotive

- Other applications

- Machine Type

- High-Speed Chip Mounters

- Medium-Speed Chip Mounters

- Low-Speed Chip Mounters

- End-use

- SMT Assembly

- PCB Manufacturing

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- Rest of World (ROW)

- North America

By Technology Insights

The SMT segment is estimated to witness significant growth during the forecast period.

SMT, or surface mount technology, is a leading PCB production method, accounting for the majority of electronic hardware manufacturing. This advanced technique enables components to be mounted directly onto the PCB surface, eliminating the need for drilling holes and promoting compact designs. SMT's benefits extend to increased production efficiency, with high throughput and the ability to mount components on both sides of a PCB. Vibration damping systems, machine vision algorithms, and precision alignment systems are integral to SMT's success. Vacuum nozzle technology and solder paste dispensing ensure accurate component placement. Cycle time reduction, error detection rate improvement, and maintenance optimization are crucial for maximizing productivity.

The SMT segment was valued at USD 4.15 billion in 2018 and showed a gradual increase during the forecast period.

Automated guided vehicles and board handling systems facilitate material handling efficiency. Advanced defect detection methods, such as component recognition and automated optical inspection, ensure high-quality output. The integration of programmable logic controllers and placement head design enhances feed system reliability. SMT's benefits include a 20% reduction in production cycle time and a 15% improvement in placement accuracy.

Regional Analysis

APAC is estimated to contribute 47% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Chip Mounter Market Demand is Rising in APAC Request Free Sample

The market exhibits a dynamic and evolving landscape, with APAC emerging as the largest and fastest-growing segment in 2023. This region's dominance is attributed to the burgeoning demand for chip mounters in PCB assembly across countries like China, India, Japan, Taiwan, and South Korea. The robust growth can be linked to the industrial expansion and high production of consumer electronics, automobiles, and industrial machinery in these nations. In APAC, key industries, such as automotive, electrical and electronics, and aerospace and defense, are experiencing rapid growth, fueling the demand for chip mounters among electronic equipment and PCB manufacturers.

Additionally, the region's competitive manufacturing costs, high economic growth rates, and favorable business environment further bolster the market's expansion. According to industry reports, the APAC market is projected to grow at a significant rate, surpassing other regions in terms of market share and growth potential.

Customer Landscape of Chip Mounter Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Chip Mounter Market

Companies are implementing various strategies, such as strategic alliances, chip mounter market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Fuji Corporation - This company specializes in the development and distribution of innovative sports products, leveraging advanced technology and research to enhance athlete performance and consumer experience.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Fuji Corporation

- Panasonic

- Yamaha Motor

- ASM Pacific Technology

- Juki Corporation

- Hanwha Precision Machinery

- Kulicke & Soffa

- Universal Instruments

- Mycronic

- Europlacer

- Essemtec AG

- Neoden Technology

- DDM Novastar

- Hitachi High-Tech

- SMTmax

- Mirae Corporation

- Versatec

- SIPLACE

- Nordson Corporation

- Evest Corporation

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Chip Mounter Market

- In August 2024, Teradyne Inc., a leading provider of automatic test equipment, announced the launch of their new Universal Chip Handler (UCH) system, expanding their chip mounter product portfolio (Teradyne Press Release, 2024). This innovative solution allows for higher placement density and improved throughput, addressing the increasing demands of semiconductor manufacturers.

- In January 2025, SMTC Corporation, a global electronics manufacturing services provider, entered into a strategic partnership with Panasonic Factory Solutions Europe GmbH to expand their chip mounter capabilities in Europe (SMTC Corporation Press Release, 2025). This collaboration enabled SMTC to offer advanced chip mounting solutions to their European clientele, enhancing their market presence and service offerings.

- In March 2025, Juki Automation Systems, a leading supplier of automated production equipment, secured a significant investment of USD 100 million from Sumitomo Corporation to expand its chip mounter production capacity (Bloomberg, 2025). This funding will enable Juki to meet the growing demand for advanced chip mounting technology in the semiconductor industry.

- In May 2025, the European Union announced a € 45 billion investment in its Chips Act, aimed at strengthening Europe's semiconductor industry and increasing its competitiveness on a global scale (European Commission Press Release, 2025). This initiative includes the development of advanced chip mounters and other semiconductor manufacturing equipment, positioning Europe as a major player in the market.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Chip Mounter Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

179 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.11% |

|

Market growth 2024-2028 |

USD 1454.3 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.77 |

|

Key countries |

China, US, Germany, Japan, India, Canada, Mexico, UK, France, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Chip Mounter Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is witnessing significant growth due to the increasing demand for high-precision chip placement accuracy in the electronics industry. Automated optical inspection systems with advanced vision system calibration are becoming increasingly important in reducing downtime during chip mounting processes. These systems ensure component placement reliability by providing real-time feedback and statistical process control charts for process capability analysis using CPK. Advanced pick-and-place mechanisms, effective board handling systems, and innovative vacuum nozzle technology are key factors driving the efficiency of chip placement. The implementation of lead-free soldering further enhances the reliability and compliance of electronic products. Comparatively, traditional chip mounting methods face challenges in optimizing chip mounting throughput and improving solder paste dispensing. Chip mounters with predictive maintenance capabilities and automated guided vehicle integration offer significant advantages in streamlining production lines and reducing downtime. System integration for chip mounting is also crucial for operational planning and supply chain management. By optimizing production line layouts and implementing efficient conveyor belt systems, electronics manufacturers can improve their overall operational efficiency and remain competitive in the market. In summary, the market is experiencing robust growth due to the increasing demand for high-precision chip placement and the need for improved efficiency and reliability in the electronics industry. Advanced technologies such as automated optical inspection systems, predictive maintenance, and system integration are key differentiators for chip mounter manufacturers, offering significant benefits for electronics manufacturers in terms of reduced downtime, increased throughput, and enhanced product quality.

What are the Key Data Covered in this Chip Mounter Market Research and Growth Report?

-

What is the expected growth of the Chip Mounter Market between 2024 and 2028?

-

USD 1.45 billion, at a CAGR of 5.11%

-

-

What segmentation does the market report cover?

-

The report is segmented by Technology (SMT and THT), Application (Communications, Computers, Consumer electronics, Automotive, and Other applications), Geography (APAC, Europe, North America, South America, Middle East and Africa, and Rest of World (ROW)), Machine Type (High-Speed Chip Mounters, Medium-Speed Chip Mounters, and Low-Speed Chip Mounters), and End-use (SMT Assembly and PCB Manufacturing)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Growing adoption of Industry 4.0 architecture, Requirement for high capital expenditure

-

-

Who are the major players in the Chip Mounter Market?

-

Fuji Corporation, Panasonic, Yamaha Motor, ASM Pacific Technology, Juki Corporation, Hanwha Precision Machinery, Kulicke & Soffa, Universal Instruments, Mycronic, Europlacer, Essemtec AG, Neoden Technology, DDM Novastar, Hitachi High-Tech, SMTmax, Mirae Corporation, Versatec, SIPLACE, Nordson Corporation, and Evest Corporation

-

We can help! Our analysts can customize this chip mounter market research report to meet your requirements.

RIA -

RIA -