APAC Automated Material Handling Equipment (Amhe) Market Size and Growth Forecast 2026-2030

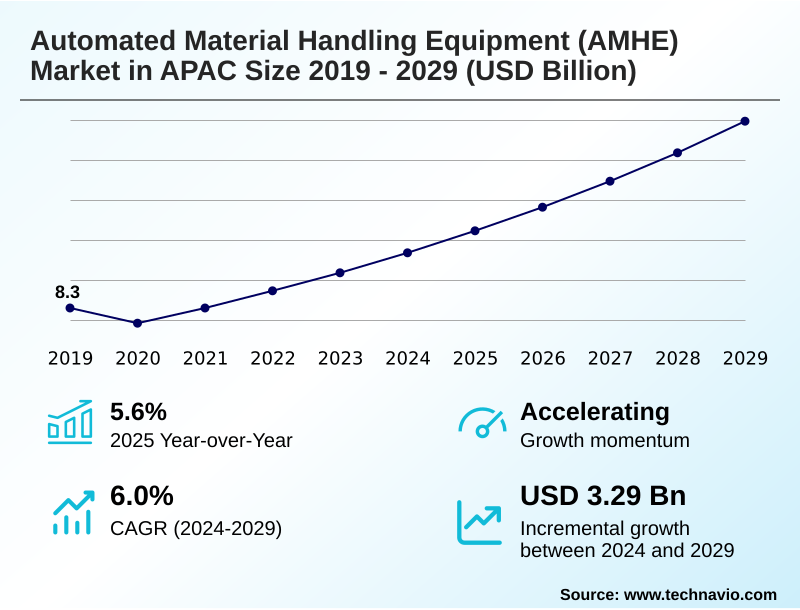

The APAC Automated Material Handling Equipment (Amhe) Market size was valued at USD 10.23 billion in 2025 growing at a CAGR of 6.1% during the forecast period 2026-2030.

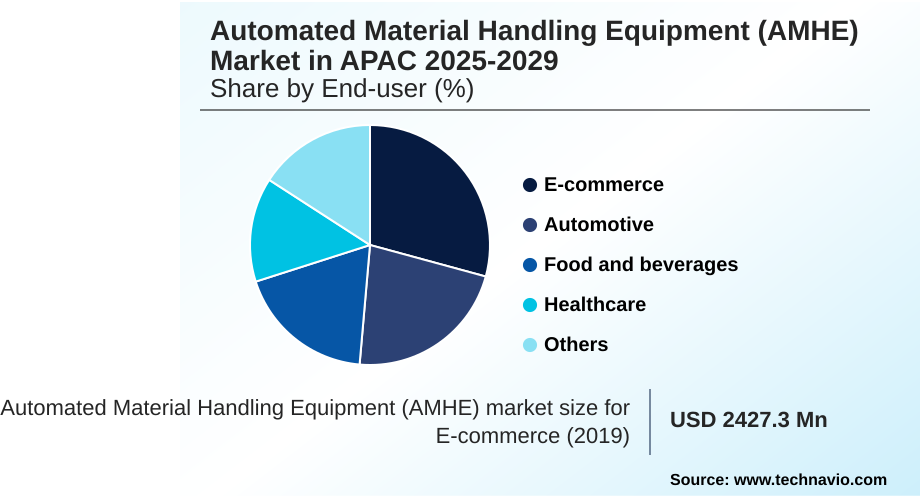

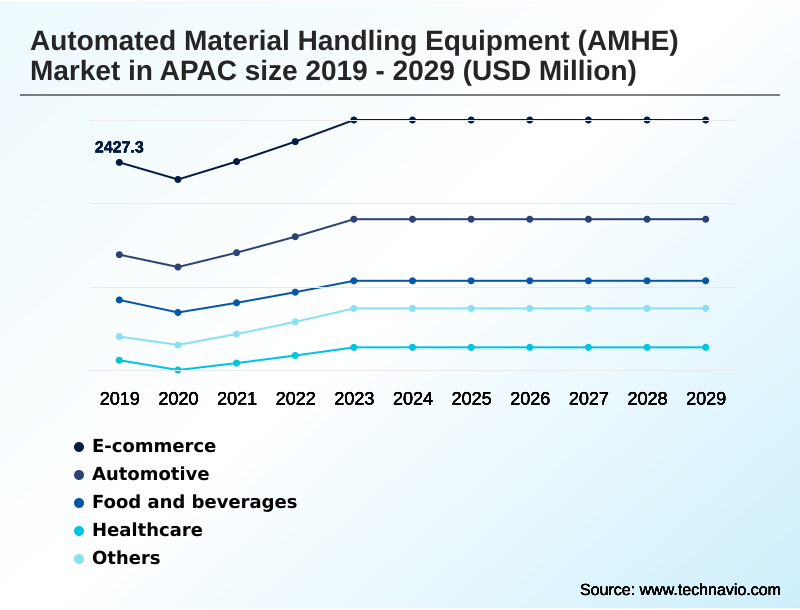

The E-commerce segment by End-user was valued at USD 2.85 billion in 2024, while the Conveyor systems segment holds the largest revenue share by Product.

The market is projected to grow by USD 5.84 billion from 2020 to 2030, with USD 3.54 billion of the growth expected during the forecast period of 2025 to 2030.

Get Key Insights on Market Forecast (PDF) Request Free Sample

APAC Automated Material Handling Equipment (Amhe) Market Overview

The automated material handling equipment (AMHE) market in APAC is expanding, driven by the need for intralogistics workflow automation and labor cost reduction. Industrial modernization and the rise of e-commerce are compelling facilities to adopt automated storage and retrieval systems and integrated sortation technologies to improve operational efficiency. Challenges such as systems integration complexity and high initial capital outlay persist, but the long-term benefits of improved order fulfillment accuracy and enhanced supply chain resilience justify the investment. In a typical third-party logistics facility, the implementation of goods-to-person picking technology combined with high-speed sorters can increase processing capacity by over 30%, a critical factor for handling seasonal demand peaks. This move toward intelligent automation is reflected in the market's year-over-year growth of 5.8%, signaling a persistent shift away from manual processes toward more sophisticated, data-driven material flow control.

Drivers, Trends, and Challenges in the APAC Automated Material Handling Equipment (Amhe) Market

Strategic decisions in the automated material handling equipment (AMHE) market in APAC are increasingly nuanced, moving beyond simple cost-per-unit calculations. For example, a food and beverage distributor planning a new facility must weigh the benefits of different systems.

A high-density automated pallet shuttle offers superior space utilization, potentially increasing storage capacity over 70% compared to conventional racking, a key consideration for automated storage for cold chain environments where energy costs are high.

This decision must also consider compliance with frameworks like the Global Food Safety Initiative (GFSI), which influences the design of conveyor systems for parcel handling and other equipment. Furthermore, the challenge of integrating AMRs with existing WMS requires careful evaluation of AI-optimized inventory management software.

For a separate use case, such as an automotive plant, the focus might be on deploying specialized AGV systems for automotive assembly line-side delivery. The ultimate choice often involves balancing upfront capital with long-term operational flexibility, including the ease of modular automated storage expansions and the capability for robotic goods-to-person picking systems to adapt to changing order profiles.

This complexity underscores the market's shift toward customized, vertically-integrated solutions.

Primary Growth Driver: The proliferation of e-commerce fulfillment centers is a primary market driver, creating significant demand for efficient, scalable, and rapid order processing automation.

The market's momentum is strongly linked to the expansion of e-commerce fulfillment scalability and investments in Industry 4.0.

In China, which commands over 40% of the regional market, the government's push for smart logistics infrastructure has catalyzed large-scale deployments of automated storage and retrieval systems and sophisticated conveyor and sortation systems.

This drive is a direct response to the need for high-velocity order fulfillment, where speed and accuracy are critical competitive differentiators.

The resulting demand for integrated solutions that ensure precise material flow control is compelling operators to invest in technologies that support both greenfield project deployment and the modernization of existing facilities, ultimately enhancing overall supply chain resilience.

Emerging Market Trend: The accelerated adoption of autonomous mobile robots represents a prominent market trend, driven by the need for flexible and scalable solutions in dynamic warehouse environments.

A significant trend is the accelerated adoption of autonomous mobile robots, which offer flexibility for brownfield site integration without the need for major structural changes. This shift is driven by the demand for scalable goods-to-person picking technology that can adapt to fluctuating order volumes, particularly in e-commerce.

Advanced fleet management software enables the coordination of hundreds of robots, optimizing routes and improving warehouse throughput optimization. As adoption grows, system interoperability standards become crucial for ensuring seamless communication between AMRs and existing warehouse management systems.

This trend facilitates workforce augmentation with robotics, where collaborative robots work alongside human employees to increase picking speed and accuracy, addressing both labor shortages and the need for higher productivity.

Key Industry Challenge: High initial capital investment requirements for advanced systems pose a significant challenge, often deterring automation initiatives among small and medium-sized enterprises.

The high upfront capital required for advanced automation presents a primary market challenge, particularly for small and medium-sized enterprises. A comprehensive return on investment analysis is essential but can be complicated by the long-term nature of the benefits, such as labor cost reduction and operational efficiency gains.

The vendor landscape is characterized by high fixed costs, where the criticality of inputs like R&D and capex is high. This financial barrier is compounded by systems integration complexity, which demands specialized expertise and can lead to unforeseen expenses.

Consequently, many potential adopters are exploring phased implementation strategy options and modular designs to mitigate financial risk and manage the total cost of ownership, including lifecycle support services, more effectively.

Explore Full Market Dynamics Analysis Request Free Sample

APAC Automated Material Handling Equipment (Amhe) Market Segmentation

The apac automated material handling equipment (amhe) industry research report provides comprehensive data including region-wise segment analysis, with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

End-user Segment Analysis

The e-commerce segment is estimated to witness significant growth during the forecast period.

The e-commerce segment is a critical end-user category, shaped by imperatives for high-velocity order fulfillment and e-commerce fulfillment scalability. Operators are deploying integrated solutions, including conveyor and sortation systems and advanced robotic picking solutions, to manage surging online retail volumes.

The objective is to achieve reduced order cycle times to meet consumer expectations for same-day delivery. In practice, this involves a strategic blend of automated storage and retrieval systems and autonomous mobile robots to enhance warehouse throughput optimization.

This segment accounts for nearly 30% of the market, reflecting massive capital investment in smart logistics infrastructure to handle peak order seasons and maintain competitive service levels.

The E-commerce segment was valued at USD 2.85 billion in 2024 and showed a gradual increase during the forecast period.

Customer Landscape Analysis for the APAC Automated Material Handling Equipment (Amhe) Market

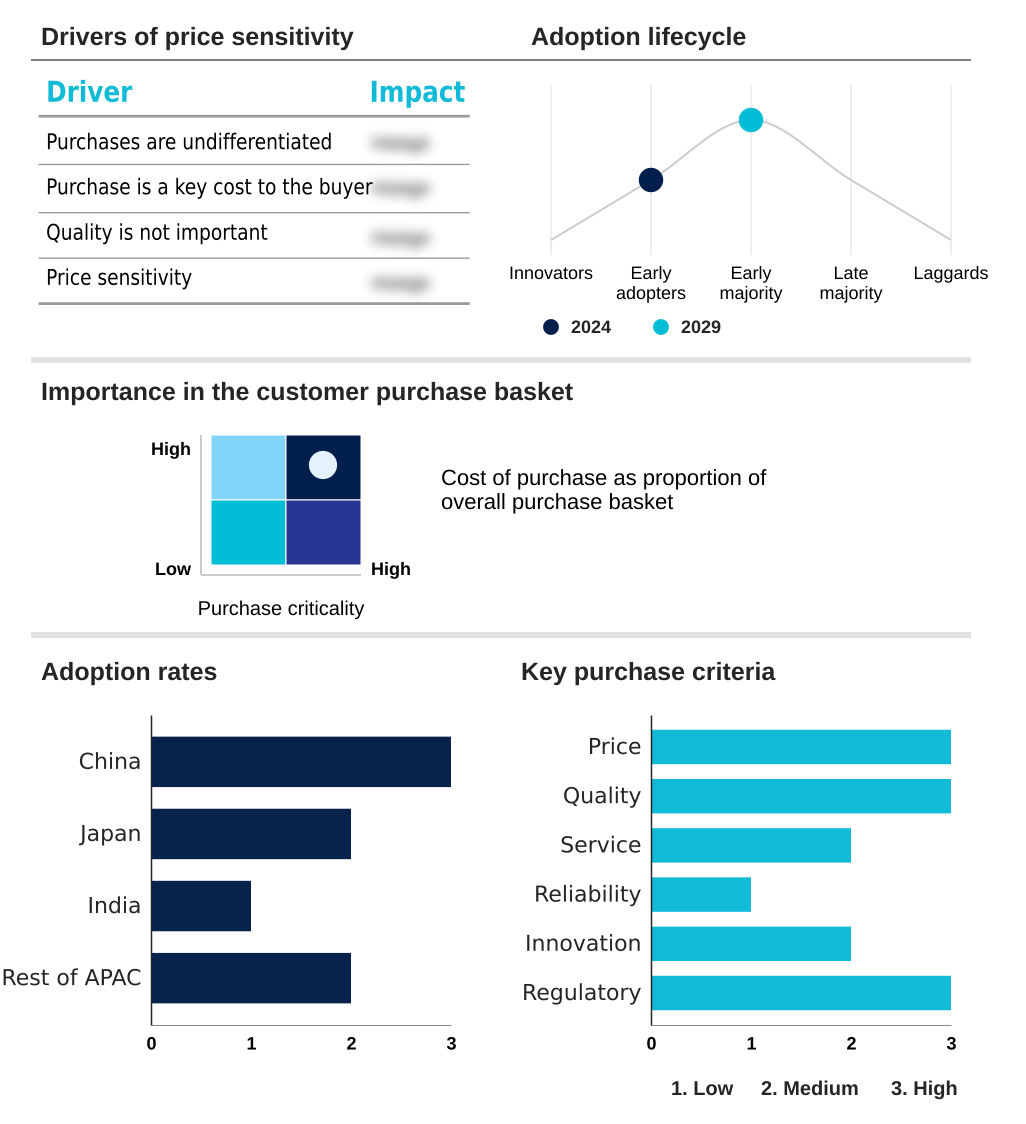

The apac automated material handling equipment (amhe) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the apac automated material handling equipment (amhe) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Competitive Landscape of the APAC Automated Material Handling Equipment (Amhe) Market

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the apac automated material handling equipment (amhe) market industry.

Addverb Technologies Pvt. Ltd. - Offerings include integrated systems for conveying, sorting, and storage, leveraging digital controls to enhance lifecycle performance and throughput efficiency in complex logistical operations.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Addverb Technologies Pvt. Ltd.

- Beumer Group GmbH and Co. KG

- Daifuku Co. Ltd.

- FIVES SAS

- FlexLink Holding AB

- Hanwha Group

- Honeywell International Inc.

- John Bean Technologies Corp.

- Jungheinrich Group

- Kardex Holding AG

- KION GROUP AG

- KNAPP AG

- Mecalux Group

- Murata Machinery Ltd.

- SSI Schafer IT Solutions GmbH

- Swisslog Holding AG

- TGW LOGISTICS GROUP GmbH

- Toyota Industries Corp.

- Wipro PARI Pvt Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments in the APAC Automated Material Handling Equipment (Amhe) Market

- In November 2024, DAIFUKU secured a contract valued at USD 300 million to automate an Alibaba fulfillment hub in Hangzhou, deploying 2000 autonomous mobile robots and high-speed sorters.

- In January 2025, KION Group announced a substantial expansion of its automated material handling plant in Jinan, China, adding advanced unit load handling capabilities and an AI research center.

- In February 2025, Geek+ expanded its autonomous mobile robot fleet deployment in JD.com warehouses across China, integrating over 1500 units to improve sorting and transport efficiency.

- In April 2025, Daifuku launched a new manufacturing plant in Hyderabad, India, to quadruple production capacity for automated warehouses, transport vehicles, and conveyors for South and Southeast Asia.

Research Analyst Overview: APAC Automated Material Handling Equipment (Amhe) Market

Procurement decisions are shifting from hardware-centric purchases to holistic investments in integrated intralogistics software platforms and end-to-end logistics automation. Boardroom discussions increasingly focus on total cost of ownership, where predictive maintenance analytics and real-time inventory management capabilities offered by modern warehouse execution software are weighed against upfront capital.

The deployment of autonomous mobile robots and automated guided vehicles necessitates a risk management strategy that addresses compliance with technical standards like ISO 3691-4 for driverless industrial trucks. This standard directly impacts operational protocols and insurance liabilities. A facility deploying robotic picking solutions must also evaluate the robustness of its warehouse control software to prevent bottlenecks.

The robotics systems segment's rapid expansion, contributing significantly to the market's overall 5.8% year-over-year growth, highlights that future competitiveness hinges not just on mechanical capabilities like those of gantry loader systems, but on the intelligence and security of the software that orchestrates them.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled APAC Automated Material Handling Equipment (Amhe) Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 215 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.1% |

| Market growth 2026-2030 | USD 3538.7 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.8% |

| Key countries | China, Japan, India, South Korea and Rest of APAC |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

APAC Automated Material Handling Equipment (Amhe) Market: Key Questions Answered in This Report

-

What is the expected growth of the APAC Automated Material Handling Equipment (Amhe) Market between 2026 and 2030?

-

The APAC Automated Material Handling Equipment (Amhe) Market is expected to grow by USD 3.54 billion during 2026-2030, registering a CAGR of 6.1%. Year-over-year growth in 2026 is estimated at 5.8%%. This acceleration is shaped by proliferation of e-commerce fulfillment centers, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (E-commerce, Automotive, Food and beverages, Healthcare, and Others), Product (Conveyor systems, Automated storage and retrieval systems, Robotics systems, and Automated guided vehicles), Type (Unit load material handling, and Bulk load material handling) and Geography (APAC). Among these, the E-commerce segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers APAC. Country-level analysis includes China, Japan, India, South Korea and Rest of APAC, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is proliferation of e-commerce fulfillment centers, which is accelerating investment and industry demand. The main challenge is high initial capital investment requirements, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the APAC Automated Material Handling Equipment (Amhe) Market?

-

Key vendors include Addverb Technologies Pvt. Ltd., Beumer Group GmbH and Co. KG, Daifuku Co. Ltd., FIVES SAS, FlexLink Holding AB, Hanwha Group, Honeywell International Inc., John Bean Technologies Corp., Jungheinrich Group, Kardex Holding AG, KION GROUP AG, KNAPP AG, Mecalux Group, Murata Machinery Ltd., SSI Schafer IT Solutions GmbH, Swisslog Holding AG, TGW LOGISTICS GROUP GmbH, Toyota Industries Corp. and Wipro PARI Pvt Ltd.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

APAC Automated Material Handling Equipment (Amhe) Market Research Insights

Market dynamics are increasingly shaped by the pursuit of operational efficiency gains and greater supply chain resilience. Decision-makers are focused on warehouse throughput optimization, compelling investment in solutions that promise reduced order cycle times. However, systems integration complexity remains a significant factor influencing procurement, as facilities must ensure new technologies align with existing infrastructure.

Adherence to system interoperability standards, such as those governing communication between robotic fleets and warehouse software, is critical for successful brownfield site integration. As companies seek to balance innovation with financial prudence, a thorough return on investment analysis becomes central to justifying expenditures on smart logistics infrastructure and advanced automation.

We can help! Our analysts can customize this apac automated material handling equipment (amhe) market research report to meet your requirements.

RIA -

RIA -