Robotics Market Size 2026-2030

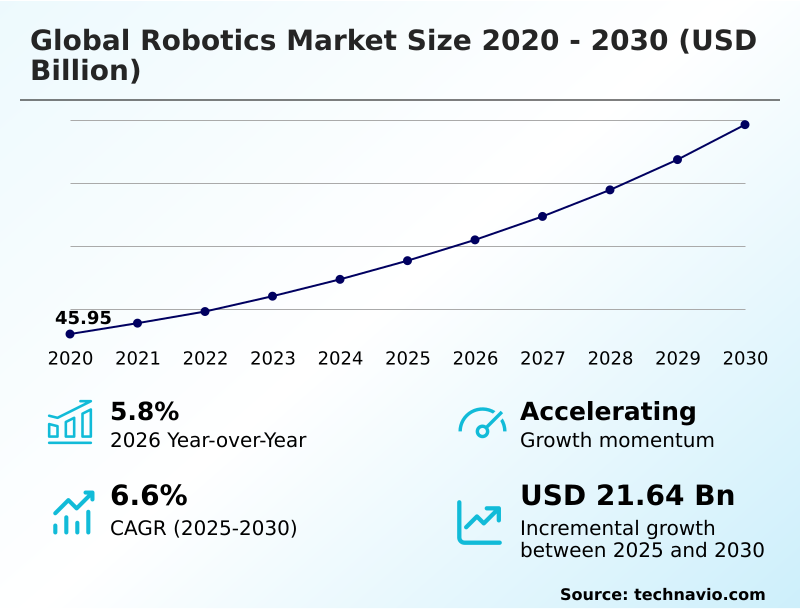

The robotics market size is valued to increase by USD 21.64 billion, at a CAGR of 6.6% from 2025 to 2030. Critical shortages of labor and demographic shifts will drive the robotics market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 56.7% growth during the forecast period.

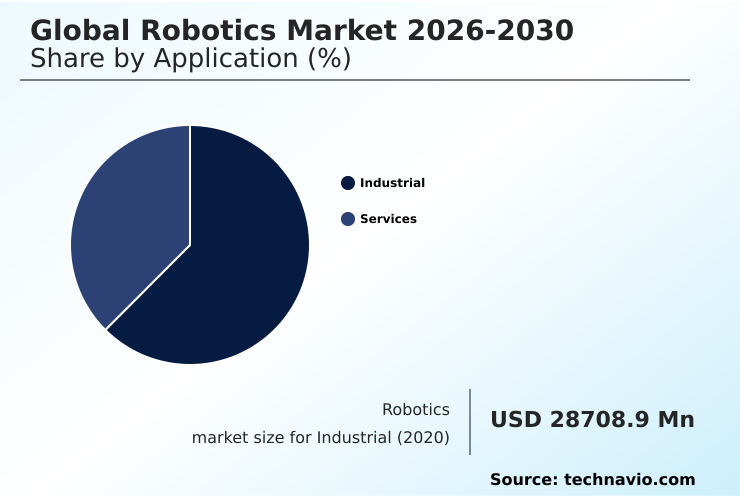

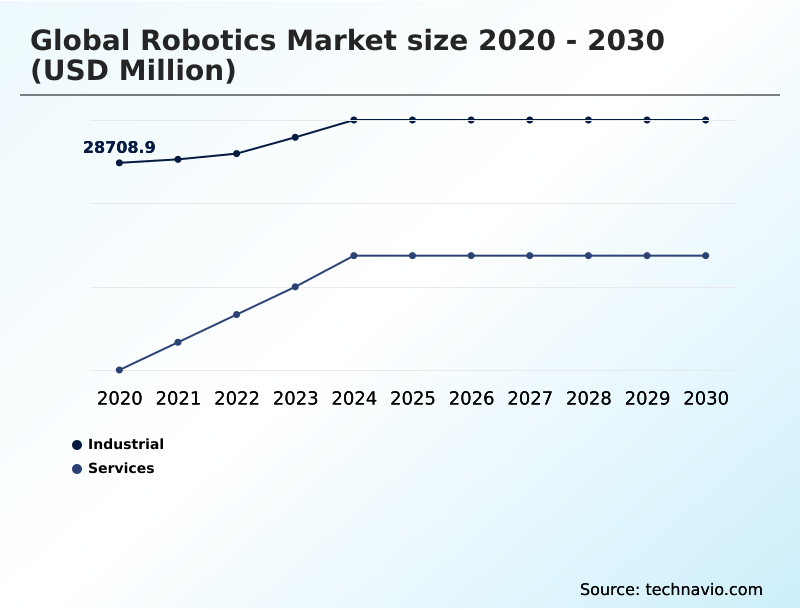

- By Application - Industrial segment was valued at USD 31.08 billion in 2024

- By End-user - Manufacturing segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 33.30 billion

- Market Future Opportunities: USD 21.64 billion

- CAGR from 2025 to 2030 : 6.6%

Market Summary

- The robotics market is undergoing a critical transformation, shifting from task-specific automation toward adaptive, software-defined systems. This evolution is driven by the convergence of generative artificial intelligence and high-fidelity physical simulation, enabling robotic platforms to generalize learning from virtual training to unstructured, real-world settings.

- As sectors from logistics to healthcare confront persistent labor shortages and escalating operational costs, demand has expanded beyond traditional automotive assembly into complex domains like precision agriculture and domestic assistance. The industrialization of physical AI is a pivotal development, equipping robots with perception-driven architectures for autonomous decision-making and safer human-robot collaboration.

- For instance, in a modern fulfillment center, a fleet of autonomous mobile robots navigates dynamic layouts to optimize order picking, reducing walk times for human associates by over 60% and directly improving throughput. This technical redirection is supported by the democratization of technology, as falling component costs and flexible Robot-as-a-Service models enable small and medium-sized enterprises to adopt scalable solutions.

- The focus on energy efficiency, lightweight materials, and advanced gripper technology further ensures that automated operations align with global sustainability mandates, cementing robotics as a cornerstone of the modern economy.

What will be the Size of the Robotics Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Robotics Market Segmented?

The robotics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Industrial

- Services

- End-user

- Manufacturing

- Healthcare

- Aerospace and defense

- Media and entertainment

- Others

- Component

- Hardware

- Software

- Services

- Geography

- APAC

- China

- Japan

- South Korea

- Europe

- Germany

- France

- UK

- North America

- US

- Canada

- Mexico

- Middle East and Africa

- Saudi Arabia

- UAE

- Israel

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

By Application Insights

The industrial segment is estimated to witness significant growth during the forecast period.

The industrial segment is defined by the deployment of automated systems in manufacturing. Modern industrial robotics are moving beyond static roles, with perception-driven architectures enabling high-precision assembly and dynamic task handling.

This evolution is central to Industry 4.0 automation, where smart factory environments require seamless human-robot collaboration and adaptability. Innovations in actuators and end-effectors, guided by bionic design principles, allow for greater dexterity.

The integration of robotic process automation with physical systems is becoming critical, though challenges with legacy infrastructure integration remain.

Modular robotics are gaining traction, allowing for scalable high-throughput logistics and production lines, with some systems achieving a 20% reduction in reconfiguration downtime.

The Industrial segment was valued at USD 31.08 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 56.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Robotics Market Demand is Rising in APAC Get Free Sample

The geographic landscape is dominated by APAC, which accounts for over 56% of the incremental growth, driven by massive industrialization and a burgeoning demand for service robotics.

This region is a key testing ground for last-mile delivery solutions using autonomous mobile robots.

In contrast, North America, with a more modest growth rate of 3.5%, leads in innovation, particularly in surgical robots featuring advanced haptic feedback systems and endoluminal systems.

Europe is focusing on sustainable automation and human-robot interaction to support its reshoring manufacturing initiatives. The adoption of robots-as-a-service (RaaS) models is growing globally, lowering entry barriers.

Meanwhile, specialized applications like exoskeletons for rehabilitation and autonomous drone inspection for infrastructure are gaining traction in developed markets.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic deployment of advanced robotics is reshaping industries, with a focus on specialized, high-value applications. The development of robotic systems for hazardous environments is paramount in sectors like energy and defense, mitigating risks to human personnel. In business operations, the integration of AI in robotic process automation is streamlining back-office functions, linking digital workflows with physical execution.

- The logistics sector is being revolutionized by humanoid robots in logistics automation, which promise to navigate spaces designed for people. Meanwhile, collaborative robots for SME manufacturing are lowering the barrier to entry for automation. The evolution of agentic AI for autonomous navigation is making mobile robots more intelligent and adaptable in complex spaces.

- The impact of 5G on industrial robotics is enabling low-latency communication for real-time control and data processing. New robots-as-a-service business models are changing procurement strategies, shifting focus from capital expenditure to operational performance, achieving more than 2x faster technology adoption cycles for some firms. In quality assurance, machine vision for quality control is becoming standard.

- Emerging fields include swarm robotics in precision agriculture for optimized farm management and 3d concrete printing for construction. However, challenges in robotic fleet management and the need for clear interoperability standards for industrial robots persist. The use of vision-language models for robot control is making interaction more intuitive.

- Healthcare is benefiting from the role of exoskeletons in rehabilitation, while edge computing in autonomous mobile robots ensures rapid decision-making. Hardware innovations like force-torque sensors in collaborative robots and bionic gripper technology for delicate handling enhance capability.

- Finally, successfully integrating ROS with legacy factory systems and establishing robust security protocols for connected robots are critical for success, alongside predictive maintenance for robotic arms to ensure uptime.

What are the key market drivers leading to the rise in the adoption of Robotics Industry?

- Critical shortages of skilled labor and ongoing demographic shifts are key drivers propelling growth and investment in the robotics market.

- Key drivers include acute labor shortages and the strategic need for supply chain resilience, which is accelerating reshoring manufacturing efforts. Companies are deploying collaborative robots to augment human workers, boosting productivity in some plants by 25%.

- This human-robot collaboration is central to the smart factory vision of Industry 4.0 automation. Advancements in mechatronics and computer vision have expanded robot capabilities, enabling effective autonomous navigation in dynamic settings.

- The integration of edge computing facilitates real-time data processing for predictive maintenance, which can reduce equipment downtime by 40%.

- This synergy of intelligent software and hardware, promoting better human-robot interaction, is critical for achieving sustainable manufacturing automation and maintaining operational continuity.

What are the market trends shaping the Robotics Industry?

- The proliferation of swarm robotics and decentralized intelligence is emerging as a significant market trend. This is driving the adoption of coordinated, autonomous units across various sectors.

- A key market trend is the shift toward decentralized intelligence through swarm robotics, where coordinated units improve efficiency in logistics and agriculture by over 30% compared to single-robot systems. The integration of agentic AI and vision-language models into the robotic operating system allows machines to interpret complex commands via natural language processing for robots, reducing programming complexity.

- This move toward production-scale physical AI is accelerated by low-code programming interfaces. Digital twin simulation in robotic simulation environments allows for virtual testing, cutting physical deployment times by up to 50%. Advancements in machine vision systems and soft robotics are enabling software-defined automation solutions that are more adaptable to unstructured environments.

What challenges does the Robotics Industry face during its growth?

- Significant interoperability hurdles and conflicts arising from the integration of modern robotics with legacy infrastructure present a key challenge affecting industry-wide growth.

- A primary market challenge is the difficulty of legacy infrastructure integration, which complicates the implementation of a cohesive data-driven operational strategy. The lack of interoperability standards hinders effective robotic fleet management, with over 60% of companies citing integration issues as a major barrier.

- Deploying advanced systems like automated guided vehicles or robots with sophisticated LiDAR sensors and bionic gripper technology in older facilities often requires cost-prohibitive retrofitting. Furthermore, a severe shortage of skilled technicians capable of maintaining specialized hardware for hazardous environment operation or circular economy robotics increases operational costs.

- This talent gap affects even niche applications like automated fiber placement and 3d concrete printing, slowing adoption despite clear efficiency benefits.

Exclusive Technavio Analysis on Customer Landscape

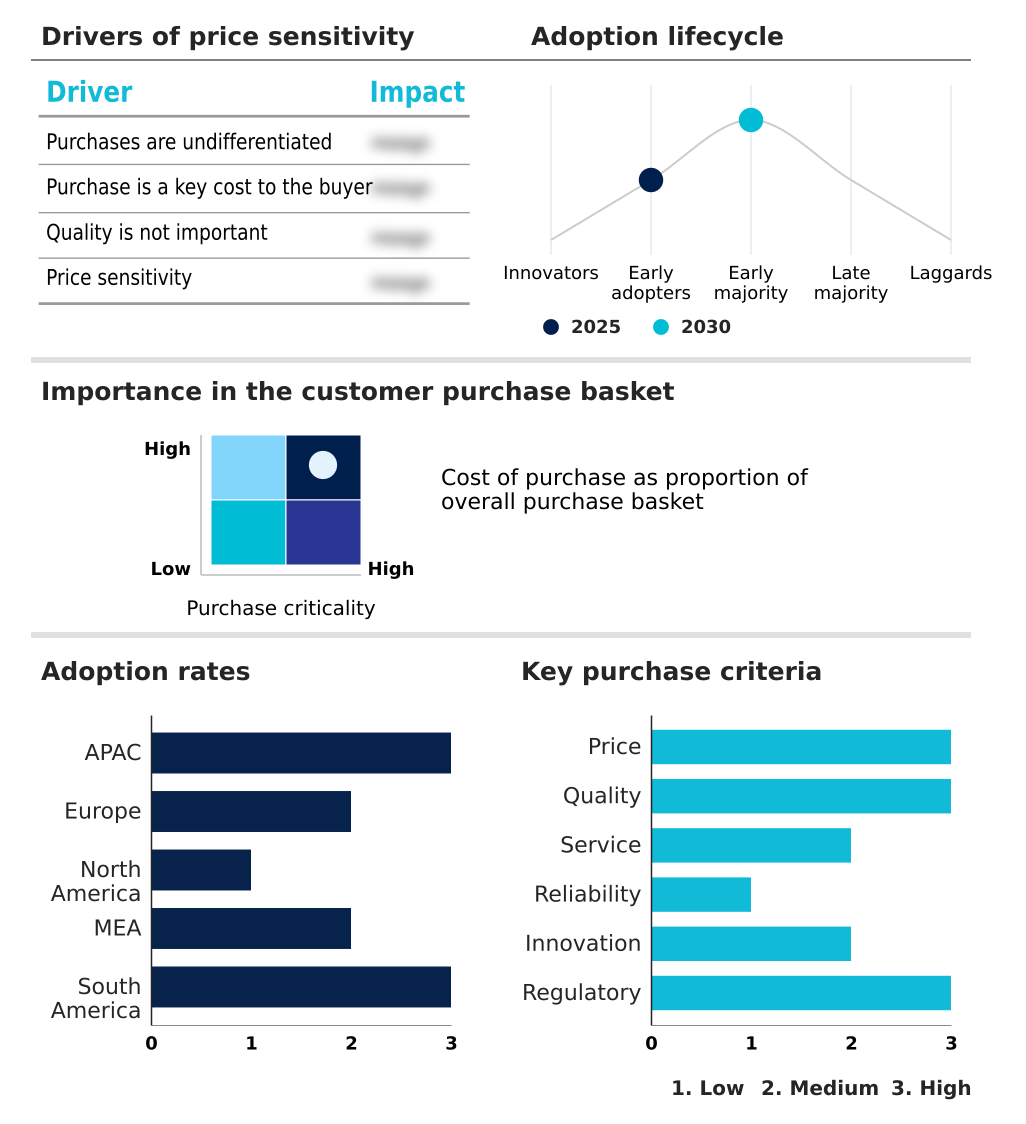

The robotics market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the robotics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Robotics Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, robotics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - Delivers integrated automation solutions, combining high-precision robotics and advanced control systems for complex manufacturing and logistics environments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Agility Robotics Inc.

- Apptronik Inc.

- Boston Dynamics Inc.

- Comau SpA

- DENSO Corp.

- FANUC Corp.

- Grey Orange Pte. Ltd.

- HD Hyundai Robotics

- Intuitive Surgical Inc.

- Kawasaki Robotics USA Inc.

- KUKA AG

- Mitsubishi Electric Corp.

- Nachi Fujikoshi Corp.

- OMRON Corp.

- Seiko Epson Corp.

- Staubli International

- UBTECH ROBOTICS CORP LTD

- Universal Robots AS

- Yaskawa Electric Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Robotics market

- In January 2025, Boston Dynamics Inc. unveiled its all-electric Atlas humanoid robot, a platform engineered for a wide range of industrial tasks and initially deployed for application testing with automotive and technology partners.

- In February 2025, HD Hyundai Robotics and KUKA AG announced an expanded collaboration to develop standardized communication protocols, aiming to ensure seamless interoperability for collaborative robots within heterogeneous smart factory ecosystems.

- In March 2025, Intuitive Surgical Inc. began the global rollout of its next-generation da Vinci 5 surgical system, which incorporates integrated force-feedback technology and advanced digital tools to enhance surgeon control in high-precision procedures.

- In April 2025, NVIDIA launched the Nemotron Coalition, a strategic initiative with prominent AI research labs focused on creating open-source frontier models optimized to provide a standardized computational framework for advanced humanoid robotics.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Robotics Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 302 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.6% |

| Market growth 2026-2030 | USD 21636.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.8% |

| Key countries | China, Japan, South Korea, India, Australia, Indonesia, Germany, France, UK, Italy, Spain, The Netherlands, US, Canada, Mexico, Saudi Arabia, UAE, Israel, Turkey, South Africa, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The robotics market is advancing through the integration of agentic AI and computer vision, creating intelligent systems for applications ranging from industrial robotics to advanced service robotics. Core technologies like the robotic operating system (ROS) are enabling complex human-robot interaction and the deployment of collaborative robots. The development of specialized hardware, including high-performance actuators, precise LiDAR sensors, and versatile end-effectors, is crucial.

- We see humanoid robots and autonomous mobile robots transforming logistics, while surgical robots and exoskeletons redefine healthcare. Swarm robotics and soft robotics open new possibilities, with digital twin simulation accelerating development. In manufacturing, automated fiber placement and 3d concrete printing showcase niche applications.

- For boardroom decisions, the shift to robots-as-a-service models impacts capital budgeting, allowing firms to adopt robotic process automation without massive upfront investment, with some achieving a 30% reduction in processing time. Systems now use force-torque sensors, vision-language models, bionic gripper technology, and perception-driven architectures, managed via edge computing for predictive maintenance.

- This landscape includes modular robotics, tactical reconnaissance units, animatronics, automated guided vehicle systems, and advancements in mechatronics for high-precision assembly and autonomous navigation.

What are the Key Data Covered in this Robotics Market Research and Growth Report?

-

What is the expected growth of the Robotics Market between 2026 and 2030?

-

USD 21.64 billion, at a CAGR of 6.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Industrial, and Services), End-user (Manufacturing, Healthcare, Aerospace and defense, Media and entertainment, and Others), Component (Hardware, Software, and Services) and Geography (APAC, Europe, North America, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Critical shortages of labor and demographic shifts, Interoperability hurdles and legacy infrastructure integration conflicts

-

-

Who are the major players in the Robotics Market?

-

ABB Ltd., Agility Robotics Inc., Apptronik Inc., Boston Dynamics Inc., Comau SpA, DENSO Corp., FANUC Corp., Grey Orange Pte. Ltd., HD Hyundai Robotics, Intuitive Surgical Inc., Kawasaki Robotics USA Inc., KUKA AG, Mitsubishi Electric Corp., Nachi Fujikoshi Corp., OMRON Corp., Seiko Epson Corp., Staubli International, UBTECH ROBOTICS CORP LTD, Universal Robots AS and Yaskawa Electric Corp.

-

Market Research Insights

- Market dynamics are increasingly influenced by the convergence of software-defined automation and physical artificial intelligence. This shift enables a data-driven operational strategy where robotic fleet management systems optimize for supply chain resilience, improving on-time delivery rates by up to 25% compared to legacy systems. The adoption of low-code programming interfaces has democratized deployment, reducing implementation time by 40% for SMEs.

- Digital enterprise integration allows for remote robotic monitoring and robotic process orchestration, which are crucial for hazardous environment operation and sustainable manufacturing automation. Advances in natural language processing for robots and decentralized intelligence are facilitating the move toward production-scale physical AI, while circular economy robotics and precision agriculture robotics open new avenues for resource efficiency.

We can help! Our analysts can customize this robotics market research report to meet your requirements.

RIA -

RIA -