Security Camera Market Size 2026-2030

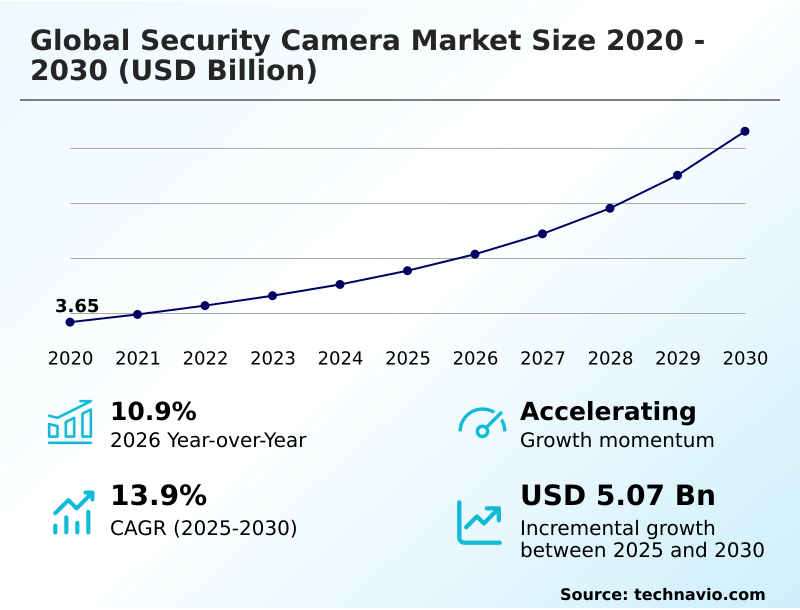

The security camera market size is valued to increase by USD 5.07 billion, at a CAGR of 13.9% from 2025 to 2030. Institutionalization of sovereign cybersecurity standards and regulatory mandates will drive the security camera market.

Major Market Trends & Insights

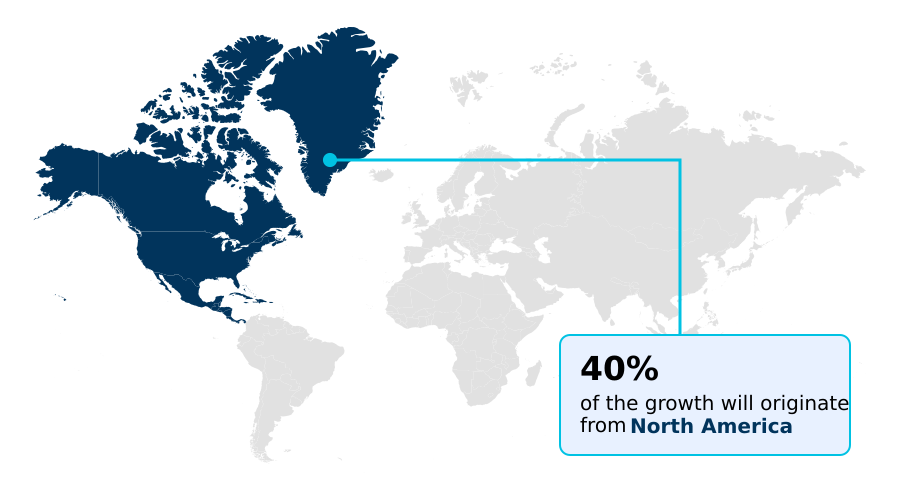

- North America dominated the market and accounted for a 40% growth during the forecast period.

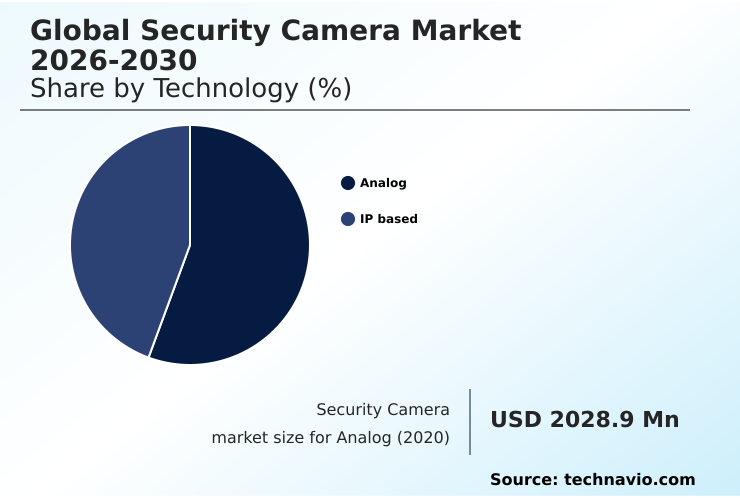

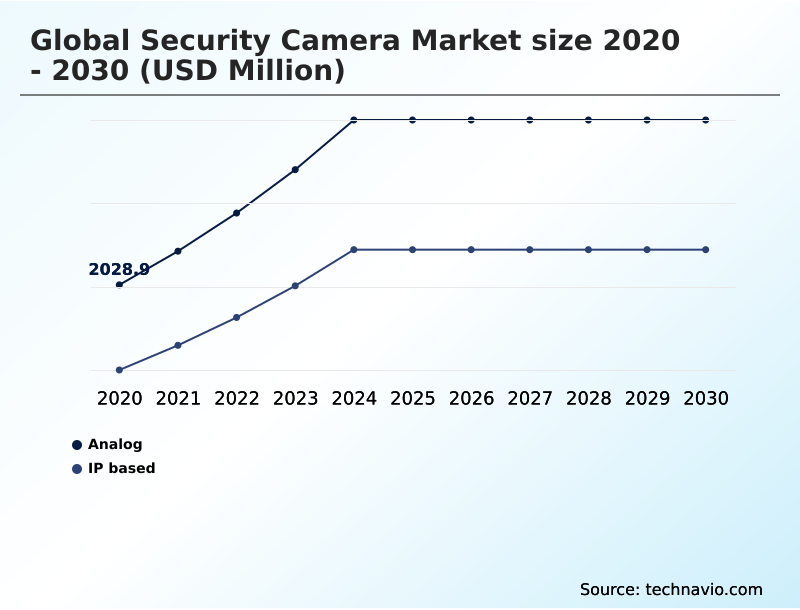

- By Technology - Analog segment was valued at USD 2.82 billion in 2024

- By Product Type - HD and full-HD segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 6.94 billion

- Market Future Opportunities: USD 5.07 billion

- CAGR from 2025 to 2030 : 13.9%

Market Summary

- The security camera market is undergoing a significant transformation, moving beyond passive recording to proactive, intelligence-driven systems. This evolution is driven by the integration of edge-based processing and AI-driven video analytics, enabling devices to perform real-time behavioral analysis and facial recognition.

- The proliferation of high-definition IP systems is fundamental, providing the clarity needed for predictive analytics to be effective in both commercial and public safety applications. For instance, a logistics company can utilize an integrated access control and video system with AI-powered cameras to not only secure perimeters but also monitor operational workflows, identifying bottlenecks and improving efficiency without manual oversight.

- However, this increased connectivity introduces challenges, making cybersecurity resilience and adherence to sovereign cybersecurity standards paramount. As smart city surveillance solutions become more common, the demand for cyber-hardened surveillance solutions that can withstand video data breaches and comply with regulations like GDPR is shaping the industry's trajectory.

- The focus is now on developing zero-trust architectures and tamper-resistant hardware to ensure data integrity and public trust. The convergence with digital twin technology also presents new frontiers for creating sentient space environments where surveillance data informs broader operational intelligence.

What will be the Size of the Security Camera Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Security Camera Market Segmented?

The security camera industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Technology

- Analog

- IP based

- Product type

- HD and full-HD

- Non-HD

- Application

- Commercial surveillance

- Public and government infrastructure

- Residential surveillance

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- India

- Japan

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Technology Insights

The analog segment is estimated to witness significant growth during the forecast period.

The global security camera market segmentation is defined by technology, product type, application, and geography. The technology segment is critically divided between legacy analog systems and modern IP-based cameras.

While analog technology maintains a presence in cost-sensitive applications, the market is decisively shifting toward IP-based solutions that offer superior 4K imaging, scalability, and integration with advanced video management software.

This transition is essential for enabling features such as predictive analytics and AI-driven video analytics. Product types are distinguished by HD and full-HD versus non-HD resolutions, with the former dominating new deployments by over 80%.

Geographically, the market presents diverse regulatory landscapes, such as GDPR-compliant security cameras in Europe, which significantly influence product design and cybersecurity resilience. The application segment includes commercial, public infrastructure, and residential surveillance, each demanding tailored solutions with robust end-to-end encryption.

The Analog segment was valued at USD 2.82 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 40% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Security Camera Market Demand is Rising in North America Request Free Sample

The global security camera market exhibits distinct regional dynamics, with North America and APAC leading in technological adoption and market share, contributing over 66% of the incremental growth.

In North America, the focus is on upgrading legacy analog systems to high-definition IP systems and deploying smart city surveillance solutions, with the region's stringent NDAA regulations influencing supply chains.

Meanwhile, APAC's growth is fueled by large-scale infrastructure projects and government initiatives, driving demand for AI-powered cameras and video management software. Europe's market is heavily shaped by GDPR compliant security cameras, pushing innovation in privacy-enhancing technologies.

In South America and the Middle East, adoption is growing in commercial and industrial sectors, with an increasing interest in integrated access control and video systems.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the security camera market requires a deep understanding of several evolving factors. A key consideration is comparing analog vs IP-based surveillance systems, where the latter offers superior scalability and integration, aligning with modern IT infrastructure.

- As organizations adopt more connected devices, learning how to secure IP cameras from data breaches becomes a critical operational imperative, necessitating robust cybersecurity protocols. The industry is also grappling with the impact of data localization laws on video storage, which forces multinational companies to rethink their cloud strategies.

- For residential and small business markets, there's growing interest in best practices for subscription-free local camera storage. Technologically, innovation focuses on using thermal and radar sensors in surveillance to reduce false alarms and improve detection in adverse conditions. This ties into the broader trend of integrating security cameras with digital twin technology.

- However, the challenges of AI chiplet supply for camera manufacturing pose a significant risk, with supply disruptions affecting production timelines for advanced devices by more than 30% in some cases. The role of cybersecurity standards in surveillance hardware is therefore more important than ever. The ability to deploy GDPR compliant facial recognition systems is now a key differentiator.

- Finally, firms must address how to mitigate risks of legacy security camera firmware, a challenge that requires systematic upgrade and replacement strategies.

What are the key market drivers leading to the rise in the adoption of Security Camera Industry?

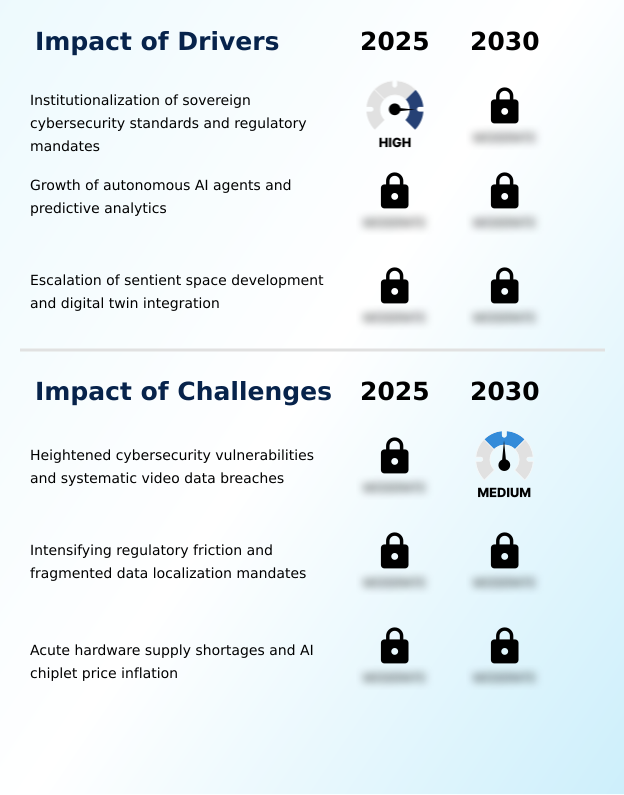

- The institutionalization of sovereign cybersecurity standards and regulatory mandates is a key driver compelling manufacturers to adopt secure-by-design principles.

- Market growth is fundamentally driven by the institutionalization of sovereign cybersecurity standards, which mandate the use of cyber-hardened surveillance solutions and secure-by-design principles.

- This regulatory push, which has reduced vulnerability exploits in certified devices by over 60%, compels manufacturers to prioritize cybersecurity resilience. Concurrently, the growth of autonomous AI agents and predictive analytics in security is transforming cameras into proactive tools.

- This technology enhances operational efficiency for security teams by automating threat detection.

- A third major driver is the escalation of sentient space development and digital twin integration, where surveillance data from high-resolution industrial cameras is used to create virtual models for optimizing city management and industrial processes, improving resource allocation by up to 20%.

What are the market trends shaping the Security Camera Industry?

- The industrialization of edge artificial intelligence processing is a primary market trend. This involves embedding complex algorithms directly onto security hardware for real-time, decentralized video analytics.

- A dominant trend reshaping the security camera market is the industrialization of edge computing in surveillance. This shift involves moving AI-driven video analytics from centralized servers directly onto devices like AI-powered cameras, enabling real-time decision-making.

- The rise of subscription-free security cameras with high-capacity local storage addresses consumer demand for cost-effective, private solutions, with adoption rates in the residential sector increasing by 25% year-over-year. Furthermore, the evolution toward multi-sensory surveillance systems, which integrate thermal imaging for perimeter security with traditional visual feeds, enhances detection accuracy.

- This allows for a 40% reduction in false alarms compared to single-sensor systems. These trends collectively push the industry toward more autonomous, resilient, and user-centric security solutions, including AI-integrated software architectures and advanced video security.

What challenges does the Security Camera Industry face during its growth?

- Heightened cybersecurity vulnerabilities and systematic video data breaches present a key challenge, expanding the attack surface for networked surveillance systems.

- The security camera market faces significant challenges, primarily from heightened cybersecurity risks associated with preventing security camera cyberattacks. The proliferation of IP-based cameras has expanded the attack surface, leading to a 35% increase in reported video data breaches.

- Another major hurdle is regulatory friction from fragmented data localization mandates, which increases operational costs for multinational firms by forcing redundant data infrastructure. A third challenge is the acute AI chiplet shortages and hardware supply chain disruptions.

- This has inflated the cost of high-end smart home cameras by over 30%, delaying large-scale projects and constraining the deployment of advanced predictive analytics capabilities. These factors create a complex environment where innovation must be balanced with security, compliance, and supply chain resilience.

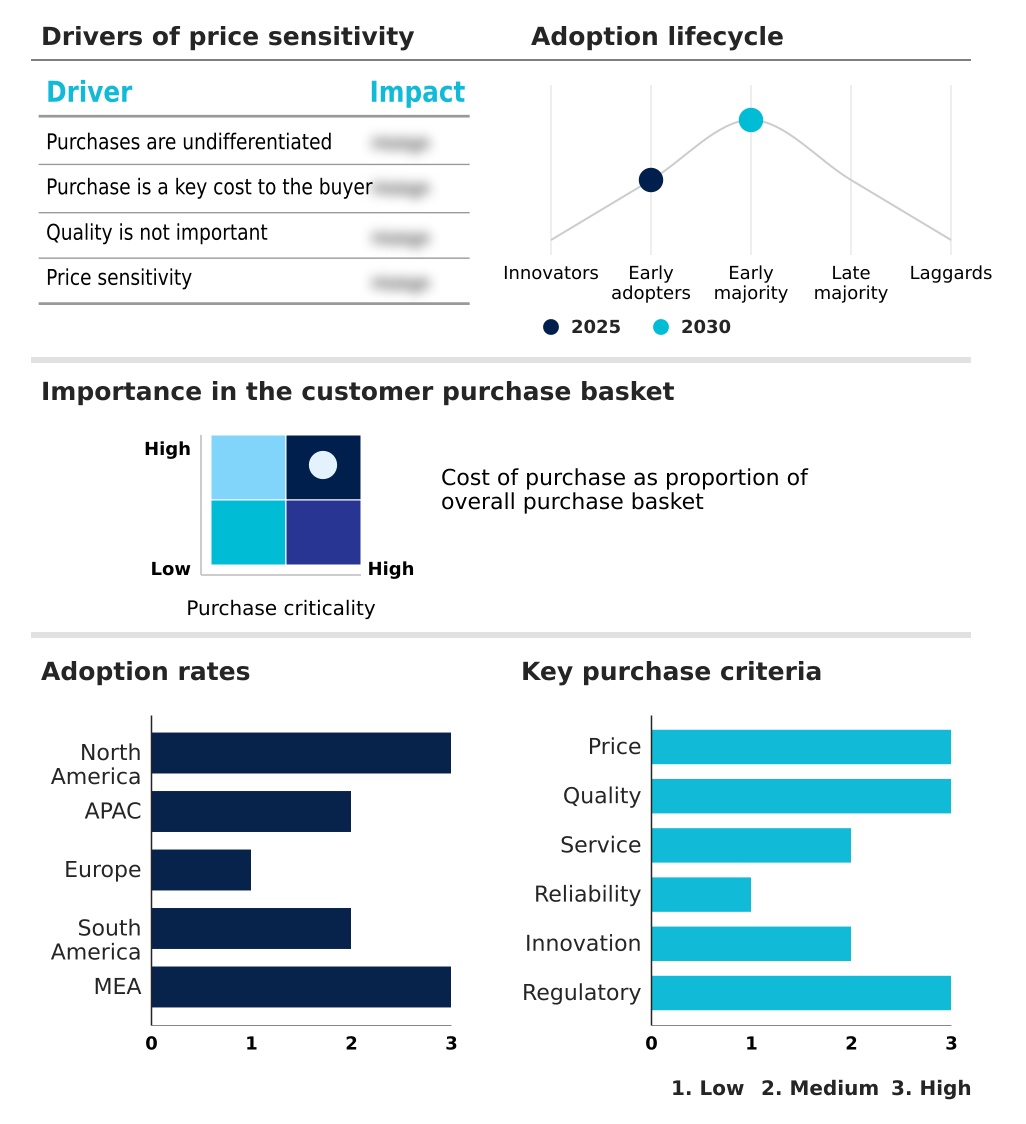

Exclusive Technavio Analysis on Customer Landscape

The security camera market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the security camera market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Security Camera Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, security camera market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Arlo Technologies Inc. - Provides smart, cloud-based wireless security camera systems and video doorbells designed for residential and connected home monitoring use cases.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Arlo Technologies Inc.

- Avigilon Corp.

- Axis Communications AB

- Bosch Sicherheitssysteme GmbH

- Canon Inc.

- CP PLUS International

- GeoVision

- Google LLC

- Hangzhou Hikvision Digital

- Hanwha Vision Co. Ltd.

- Honeywell International Inc.

- Motorola Solutions Inc.

- Panasonic Holdings Corp.

- Pelco Inc.

- Sony Group Corp.

- Teledyne FLIR LLC

- Tiandy Technologies Co. Ltd.

- Zhejiang Dahua Technology

- Zhejiang Uniview Technologies

- ZKTeco Co Ltd

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Security camera market

- In February 2025, Arlo Technologies Inc. announced a strategic partnership with a major US telecommunications provider to bundle its smart home security cameras with high-speed internet packages, enhancing its residential market penetration.

- In April 2025, Axis Communications AB launched its next-generation line of AI-powered IP cameras featuring on-device deep learning for advanced object detection and behavior analysis, targeting the commercial and smart city sectors.

- In January 2025, Hanwha Vision Co. Ltd. unveiled its 'Trustworthy AI' initiative, committing to new ethical guidelines and privacy-enhancing features in its video surveillance software, addressing growing data security concerns in Europe and North America.

- In September 2024, Motorola Solutions Inc. completed the acquisition of a specialized video analytics software firm, integrating its predictive policing and anomaly detection algorithms into the Avigilon security portfolio to strengthen its public safety offerings.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Security Camera Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 291 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 13.9% |

| Market growth 2026-2030 | USD 5066.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 10.9% |

| Key countries | US, Canada, Mexico, China, India, Japan, South Korea, Indonesia, Australia, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Turkey and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The security camera market is rapidly advancing beyond simple video capture, driven by the integration of edge-based processing and Generative AI into high-definition IP systems. The use of neural processing units within AI-powered cameras allows for sophisticated behavioral analysis and facial recognition at the source, reducing latency.

- This shift supports the development of autonomous surveillance systems and hybrid AI-agent partnerships that can proactively identify threats. Boardroom decisions are increasingly focused on cybersecurity resilience, pushing for the adoption of tamper-resistant hardware, zero-trust architectures, and end-to-end encryption to mitigate the risk of video data breaches.

- Compliance with STQC certification and regulations such as GDPR and NDAA is now a critical product strategy requirement. The industry is also exploring multi-sensory autonomous surveillance by combining bispectral imaging and acoustic sensors. This transition to intelligent, secure systems has demonstrated the ability to reduce false security alerts by over 40%, optimizing resource allocation.

- The integration with digital twin technology is creating sentient space environments, where video management software provides crucial data for broader operational management.

What are the Key Data Covered in this Security Camera Market Research and Growth Report?

-

What is the expected growth of the Security Camera Market between 2026 and 2030?

-

USD 5.07 billion, at a CAGR of 13.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Technology (Analog, and IP based), Product Type (HD and full-HD, and Non-HD), Application (Commercial surveillance, Public and government infrastructure, and Residential surveillance) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Institutionalization of sovereign cybersecurity standards and regulatory mandates , Heightened cybersecurity vulnerabilities and systematic video data breaches

-

-

Who are the major players in the Security Camera Market?

-

Arlo Technologies Inc., Avigilon Corp., Axis Communications AB, Bosch Sicherheitssysteme GmbH, Canon Inc., CP PLUS International, GeoVision, Google LLC, Hangzhou Hikvision Digital, Hanwha Vision Co. Ltd., Honeywell International Inc., Motorola Solutions Inc., Panasonic Holdings Corp., Pelco Inc., Sony Group Corp., Teledyne FLIR LLC, Tiandy Technologies Co. Ltd., Zhejiang Dahua Technology, Zhejiang Uniview Technologies and ZKTeco Co Ltd

-

Market Research Insights

- The security camera market's dynamics are shaped by the convergence of advanced technology and evolving security paradigms. The adoption of AI-driven video analytics and edge computing in surveillance allows for proactive threat detection, improving response times by over 50% compared to traditional passive monitoring.

- Enterprises are increasingly deploying commercial video surveillance systems not just for security but for operational intelligence, utilizing video management for retail to optimize store layouts and customer flow. This shift is driving demand for cyber-hardened surveillance solutions that comply with sovereign cybersecurity standards and data localization mandates.

- The debate over local vs cloud camera storage continues, with hybrid models gaining traction. The integration of thermal imaging for perimeter security and multi-sensory surveillance systems is becoming standard in high-security applications, addressing the limitations of traditional visual cameras.

We can help! Our analysts can customize this security camera market research report to meet your requirements.

RIA -

RIA -