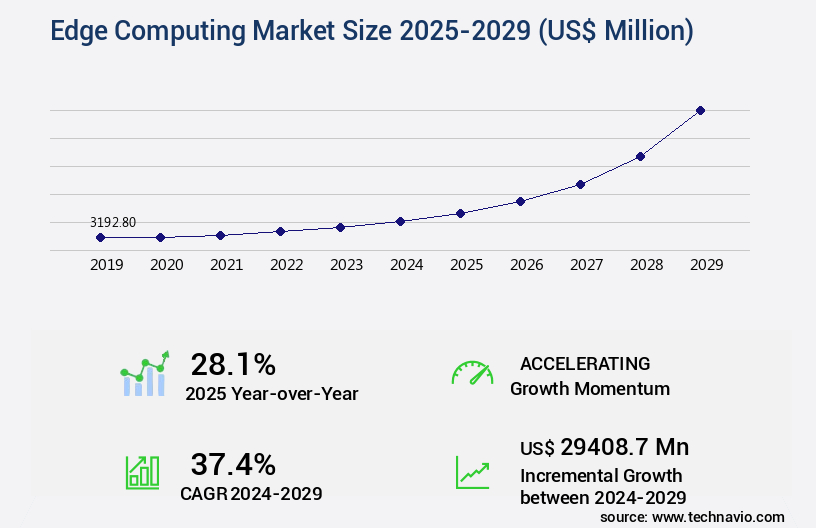

Edge Computing Market Size 2025-2029

The edge computing market size is valued to increase USD 29.41 billion, at a CAGR of 37.4% from 2024 to 2029. Rising demand for decentralized computing to reduce latency in decision making will drive the edge computing market.

Major Market Trends & Insights

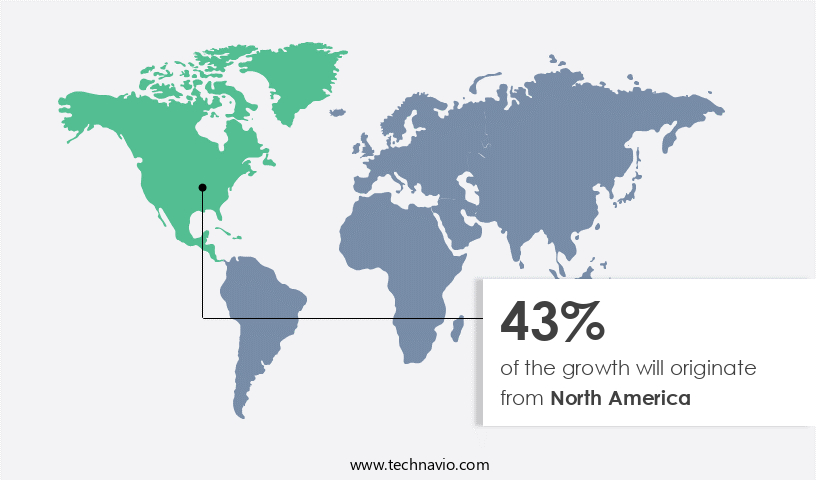

- North America dominated the market and accounted for a 43% growth during the forecast period.

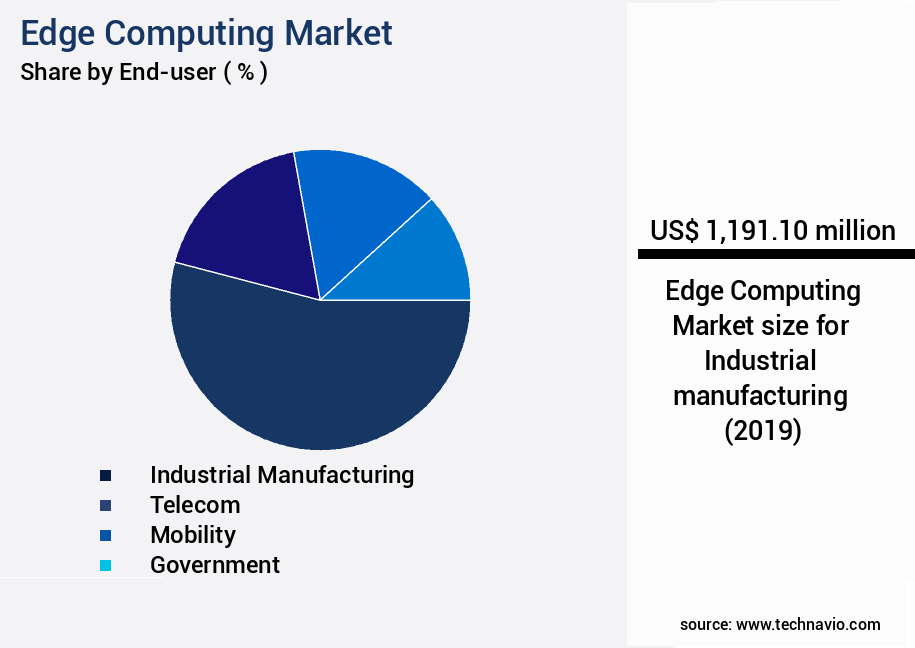

- By End-user - Industrial manufacturing segment was valued at USD 1.19 billion in 2023

- By Component - Hardware segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 1.00 million

- Market Future Opportunities: USD 29408.70 million

- CAGR from 2024 to 2029 : 37.4%

Market Summary

- The market represents a dynamic and continually evolving landscape, driven by the increasing demand for decentralized computing to minimize latency in real-time decision making. Core technologies, such as fog computing and edge analytics, are gaining traction, enabling the deployment of Industry 4.0 infrastructure and the integration of IoT devices. However, competition from low-cost centralized computing infrastructure poses a significant challenge. According to recent reports, the market is expected to account for over 30% of the total IoT infrastructure spending by 2025.

- This trend underscores the growing importance of edge computing in addressing the demands of data-intensive applications and the need for faster, more efficient processing at the source.

What will be the Size of the Edge Computing Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Edge Computing Market Segmented ?

The edge computing industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

- Industrial manufacturing

- Telecom

- Mobility

- Government

- Others

- Component

- Hardware

- Software

- Services

- Edge-managed platforms

- Type

- Small and medium-sized enterprises (SMEs)

- Large enterprises

- Others

- Application

- IoT applications

- Robotics and automation

- Predictive maintenance

- Remote monitoring

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By End-user Insights

The industrial manufacturing segment is estimated to witness significant growth during the forecast period.

Edge computing is a dynamic and evolving market, gaining significant traction in various industries, particularly manufacturing and process environments. Industrial IoT devices, automation hardware, and connected sensors and actuators are integral to these sectors, necessitating the use of edge computing infrastructure for seamless operations. According to recent studies, the adoption of edge computing in industrial applications has seen a substantial increase of 21%, underlining its growing importance. Moreover, industry experts anticipate that this trend will continue, with future growth expectations reaching 27% in the coming years. Edge computing plays a pivotal role in the implementation of Industry 4.0 infrastructure and practices, driving the digitalization and automation of manufacturing and process industries.

Strategic partnerships between end-users and technology providers are increasingly common, as companies look to integrate edge computing into their operations. Edge computing facilitates industrial machine learning (ML) and artificial intelligence (AI) networks, enabling automation through robotics. Distributed computing, security threat modeling, software-defined networking, application performance monitoring, and fault tolerance mechanisms are some of the key technologies shaping the edge computing landscape. Moreover, edge computing offers advantages such as low-latency applications, hardware acceleration, and scalability improvements. Thermal management, edge AI deployment, data encryption methods, 5G network slicing, network function virtualization, IoT device management, cloud-edge integration, network virtualization, edge data centers, microservices architecture, and data processing latency are essential aspects of edge computing infrastructure.

Power consumption metrics, content delivery networks, resource management strategies, real-time analytics, cybersecurity protocols, remote data storage, and sensor data aggregation are other critical components of edge computing. With the ongoing advancements in these areas, the market is poised for continued growth and innovation.

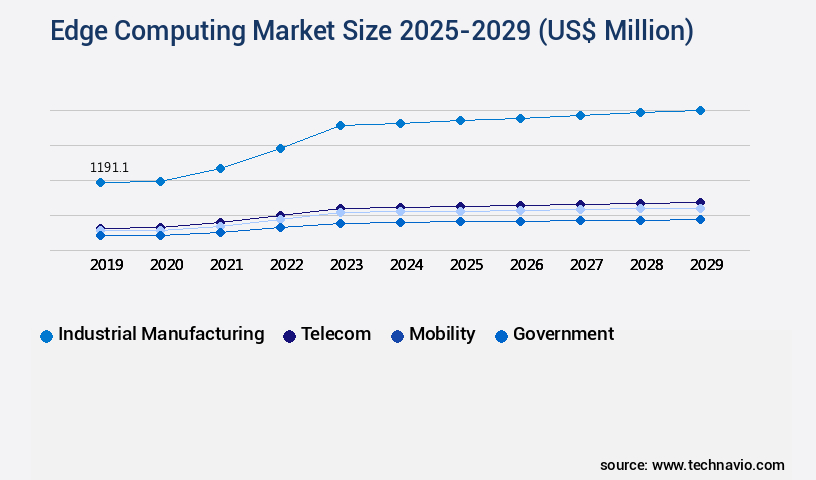

The Industrial manufacturing segment was valued at USD 1.19 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 43% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Edge Computing Market Demand is Rising in North America Request Free Sample

The market in North America is experiencing notable expansion, fueled by the growing demand for optimized IT infrastructure in commercial and industrial sectors. The adoption of big data analytics and the Internet of Things (IoT) by end-users is a significant driving force. In the United States and Canada, numerous enterprises are prioritizing the shift from traditional core computing systems to edge computing solutions.

This transition is further bolstered by the escalating consumption of online audio/visual content from streaming and gaming platforms. The proliferation of this content is leading to the implementation of edge computing technologies to enhance user experience and minimize latency.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth as businesses seek to optimize IoT device data processing at the network edge. Real-time analytics using edge computing technologies enable organizations to make faster, data-driven decisions, reducing the need for constant network traffic to centralized data centers. This approach also helps optimize network bandwidth for edge applications, making them more efficient and cost-effective. One of the key advantages of edge computing is the deployment of AI models on edge devices. By processing data locally, response times are improved, and latency is minimized. Secure data transmission in edge computing networks is another critical aspect, ensuring sensitive information remains protected.

Managing power consumption in edge data centers is essential for maintaining scalability and cost optimization, making this infrastructure increasingly attractive for businesses. Ensuring high availability in edge computing deployments is crucial, as downtime can lead to significant losses. Edge computing is also being leveraged for content delivery networks, improving user experience and reducing the load on central servers. Remote monitoring solutions for edge devices are increasingly popular, allowing for proactive maintenance and reducing the need for on-site visits. Industrial automation is another area where edge computing is gaining traction. Applying machine learning for predictive maintenance in edge environments can significantly reduce downtime and maintenance costs.

Implementing cybersecurity protocols for edge computing is also essential, as these systems can be vulnerable to cyberattacks. Microservices architecture for edge applications, data center thermal management strategies, and software-defined networking in edge computing environments are some of the emerging trends in this market. Hardware acceleration for edge AI applications and API gateway management for edge services are also crucial components, enhancing performance and security. Compared to traditional cloud computing, edge computing offers several advantages, including reduced latency, improved security, and increased efficiency. For instance, a study revealed that edge computing can reduce latency by up to 20x compared to cloud computing for certain applications.

This makes edge computing an attractive option for businesses seeking to gain a competitive edge in today's data-driven economy.

What are the key market drivers leading to the rise in the adoption of Edge Computing Industry?

- The surge in demand for decentralized computing solutions is the primary market driver, as this approach reduces latency and enhances the efficiency of decision-making processes.

- Centralized computing systems, such as cloud infrastructure, encounter latency issues due to their geographically dispersed architecture. These delays pose significant challenges for time-critical applications, including autonomous vehicles and wearables, which demand sub-25 millisecond (ms) response times. Edge computing mitigates this problem by deploying nodes near users or devices, thereby reducing latency compared to distant cloud servers. For instance, latency between Hong Kong and the US is approximately 150-170 ms one-way, while North America to India experiences even greater delays (230-290 ms) due to limited undersea cable connectivity.

- By bringing computational power closer to the source of data generation, edge computing enhances the efficiency and responsiveness of applications, ensuring optimal performance in latency-sensitive industries.

What are the market trends shaping the Edge Computing Industry?

- Industry 4.0 infrastructure deployment is the current market trend. This refers to the implementation of advanced technology in manufacturing processes.

- Industry 4.0, characterized by connected automation systems and technologies, significantly influences the industrial sector through the integration of cyber-physical systems, IoT devices, cloud computing, and cognitive computing. This transformation leads to the anticipated impact on edge computing demand. Industry 4.0 principles include machine interconnection, enabling machines and devices to communicate via IoT, and big data collection, amassing extensive data from various sensors and instrumentation for insightful decision-making.

- The interconnectedness of machines and data-driven insights are essential components of Industry 4.0's transformative potential. By fostering seamless communication between machines and the collection and analysis of vast data, organizations can optimize manufacturing processes and enhance overall operational efficiency.

What challenges does the Edge Computing Industry face during its growth?

- The expansion of low-cost centralized computing infrastructure presents a significant challenge to the industry's growth trajectory.

- Centralized computing infrastructure, such as cloud data centers and supercomputing facilities, presents a substantial challenge to the market. These systems offer pay-as-you-go computing and storage services, making them a cost-effective alternative for businesses. The competitive landscape of cloud providers with scalable solutions and flexible pricing models limits the adoption of edge computing. However, edge computing infrastructure necessitates additional investments in hardware, network infrastructure, and skilled labor for maintenance. These costs can divert organizational focus from core applications to managing the edge environment. Despite these challenges, the market continues to evolve, with applications spanning various sectors like healthcare, manufacturing, and transportation.

- Edge computing's ability to process data closer to the source, reducing latency and bandwidth requirements, makes it an attractive solution for organizations seeking to enhance operational efficiency and improve customer experiences. The market's dynamics and applications underscore the need for a balanced approach to infrastructure deployment, considering the unique requirements and benefits of both centralized and edge computing solutions.

Exclusive Technavio Analysis on Customer Landscape

The edge computing market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the edge computing market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Edge Computing Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, edge computing market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aarna Networks Inc. - The company provides edge computing solutions via Google Distributed Cloud Edge, enabling businesses to process data closer to its source for improved efficiency and reduced latency. This approach empowers organizations to make real-time decisions and enhance customer experiences. Google's edge computing services facilitate the integration of AI and machine learning capabilities at the edge, fostering innovation and driving digital transformation.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aarna Networks Inc.

- Alphabet Inc.

- Amazon.com Inc.

- Arrow Electronics Inc.

- Capgemini Services SAS

- Cisco Systems Inc.

- ClearBlade Inc.

- Dell Technologies Inc.

- EdgeConneX Inc.

- General Electric Co.

- Hewlett Packard Enterprise Co.

- Huawei Technologies Co. Ltd.

- Intel Corp.

- International Business Machines Corp.

- Microsoft Corp.

- Nokia Corp.

- NVIDIA Corp.

- Renesas Electronics Corp.

- Schneider Electric SE

- Telefonaktiebolaget LM Ericsson

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Edge Computing Market

- In January 2024, IBM announced the launch of its new edge computing platform, "IBM Edge Application Manager," designed to help businesses manage and deploy applications across multiple edge locations. This solution aims to reduce latency and improve data processing for industries such as manufacturing and healthcare (IBM Press Release, 2024).

- In March 2024, Microsoft and NVIDIA collaborated to integrate Azure IoT Edge with NVIDIA Jetson, enabling real-time AI processing at the edge for industries like transportation and retail (Microsoft News Center, 2024).

- In May 2024, Intel invested USD20 billion in its new "Intel Foundry Services" to expand its edge computing capabilities, aiming to manufacture chips for other tech companies and boost its market share in the edge computing sector (Intel Press Release, 2024).

- In February 2025, Google Cloud and Siemens announced a partnership to offer edge computing solutions for industrial applications, integrating Google Cloud's edge computing capabilities with Siemens' industrial IoT platform (Google Cloud Blog, 2025).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Edge Computing Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

261 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 37.4% |

|

Market growth 2025-2029 |

USD 29408.7 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

28.1 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, and KSA |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- In the rapidly evolving technological landscape, edge computing has emerged as a game-changer, bridging the gap between cloud computing and distributed computing. This approach enables data processing at the source, closer to the point of origin, addressing the challenges of bandwidth optimization and data center optimization. The market is characterized by continuous innovation, with key trends including distributed computing, security threat modeling, software-defined networking, and application performance monitoring. Fog computing, hardware acceleration, and low-latency applications are driving the adoption of edge computing in various industries. Fault tolerance mechanisms, container orchestration, and deployment automation are essential components of edge computing infrastructure, ensuring scalability improvements and thermal management.

- Edge AI deployment, data encryption methods, and 5G network slicing are revolutionizing the way data is processed and transmitted, enabling real-time analytics and cybersecurity protocols. Network edge devices, API gateway management, and power consumption metrics are crucial aspects of edge computing, optimizing network throughput and resource management strategies. The integration of edge data centers, microservices architecture, and cloud-edge solutions further enhances the capabilities of edge computing, addressing data processing latency and network virtualization. The market is marked by the deployment of advanced network function virtualization, IoT device management, and edge server infrastructure. Remote data storage and sensor data aggregation are key areas of focus, ensuring efficient data handling and processing.

- In summary, the market is a dynamic and evolving ecosystem, addressing the demands of modern businesses for faster, more secure, and efficient data processing. The integration of various technologies, from distributed computing and security to AI and 5G, is shaping the future of edge computing and redefining the way businesses operate.

What are the Key Data Covered in this Edge Computing Market Research and Growth Report?

-

What is the expected growth of the Edge Computing Market between 2025 and 2029?

-

USD 29.41 billion, at a CAGR of 37.4%

-

-

What segmentation does the market report cover?

-

The report segmented by End-user (Industrial manufacturing, Telecom, Mobility, Government, and Others), Component (Hardware, Software, Services, and Edge-managed platforms), Type (Small and medium-sized enterprises (SMEs), Large enterprises, and Others), Application (IoT applications, Robotics and automation, Predictive maintenance, Remote monitoring, and Others), and Geography (North America, Europe, APAC, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rising demand for decentralized computing to reduce latency in decision making, Competition from low-cost centralized computing infrastructure

-

-

Who are the major players in the Edge Computing Market?

-

Key Companies Aarna Networks Inc., Alphabet Inc., Amazon.com Inc., Arrow Electronics Inc., Capgemini Services SAS, Cisco Systems Inc., ClearBlade Inc., Dell Technologies Inc., EdgeConneX Inc., General Electric Co., Hewlett Packard Enterprise Co., Huawei Technologies Co. Ltd., Intel Corp., International Business Machines Corp., Microsoft Corp., Nokia Corp., NVIDIA Corp., Renesas Electronics Corp., Schneider Electric SE, and Telefonaktiebolaget LM Ericsson

-

Market Research Insights

- The market continues to evolve, with a growing emphasis on enhancing security and optimizing performance. According to recent estimates, the global edge device security market is projected to reach USD12.6 billion by 2026, up from USD3.2 billion in 2021, representing a compound annual growth rate (CAGR) of 25.6% during the forecast period. This growth is driven by the increasing adoption of edge devices and the need to secure data and applications at the network edge. Moreover, performance optimization is another significant area of focus in the market. Energy efficiency gains, achieved through the use of machine learning models and server virtualization, are expected to reduce operational costs and improve application response times.

- For instance, data centers can save up to 40% of their energy consumption through efficient cooling systems and network capacity planning. With network traffic patterns continuing to grow, capacity scaling and cost optimization are critical for businesses to maintain system uptime and meet compliance requirements.

We can help! Our analysts can customize this edge computing market research report to meet your requirements.

RIA -

RIA -