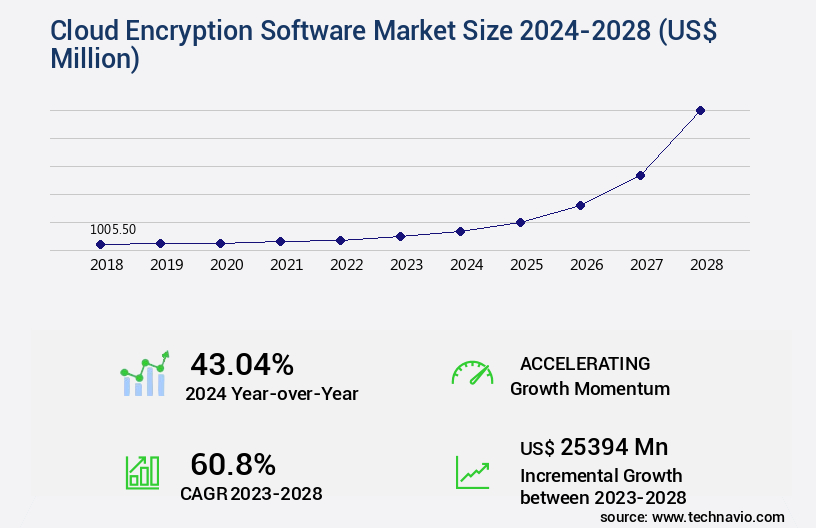

Cloud Encryption Software Market Size 2024-2028

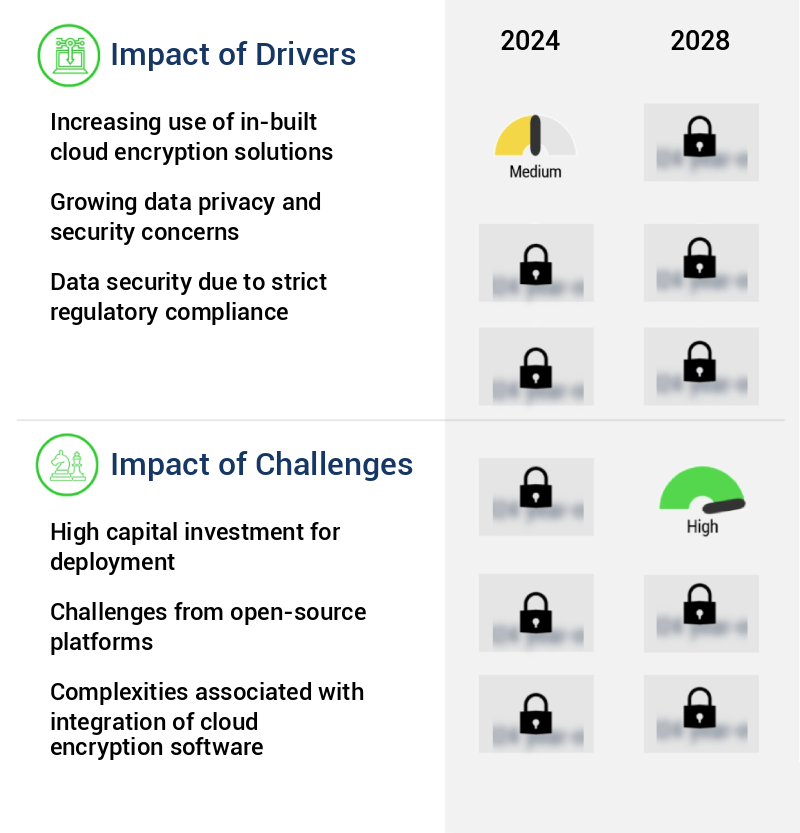

The cloud encryption software market size is valued to increase by USD 25.39 billion, at a CAGR of 60.8% from 2023 to 2028. Increasing use of in-built cloud encryption solutions will drive the cloud encryption software market.

Market Insights

- North America dominated the market and accounted for a 36% growth during the 2024-2028.

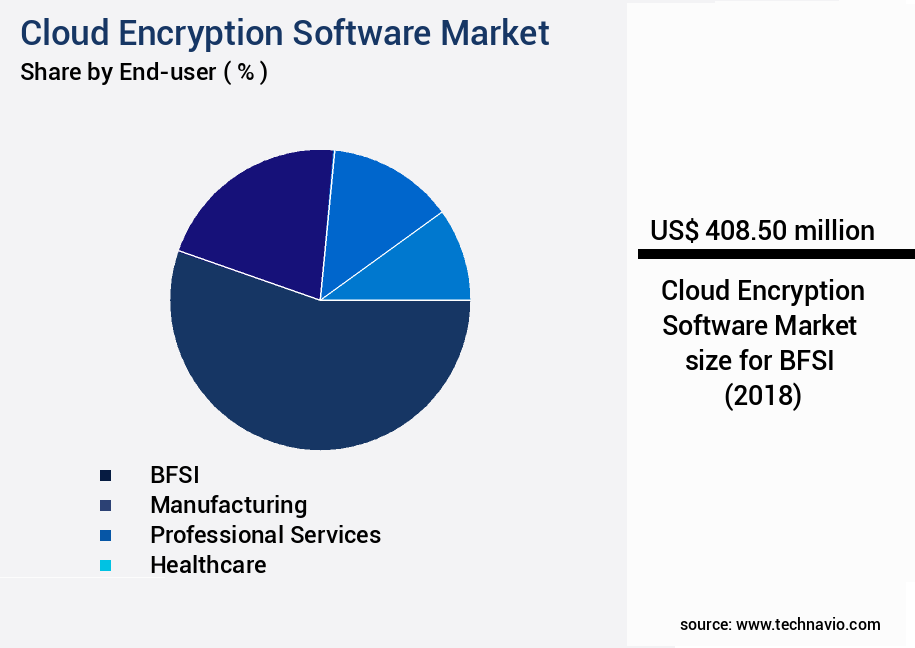

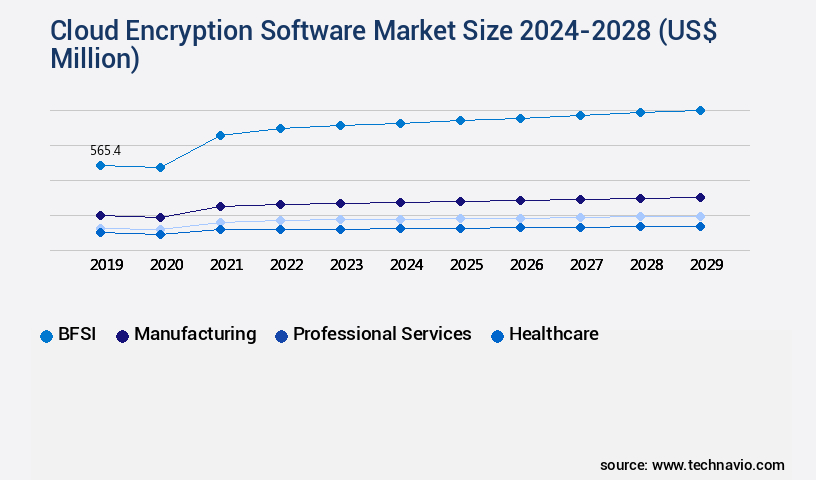

- By End-user - BFSI segment was valued at USD 408.50 billion in 2022

- By Type - Large enterprise segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 2.00 million

- Market Future Opportunities 2023: USD 25394.00 million

- CAGR from 2023 to 2028 : 60.8%

Market Summary

- The market is experiencing significant growth due to the increasing adoption of cloud services and the need to secure data in a digital world. With the rise of Bring Your Own Device (BYOD) policies in organizations, there is a growing requirement for robust encryption solutions to protect sensitive information. In-built cloud encryption solutions are gaining popularity as they offer enhanced security features, ease of deployment, and integration with various cloud platforms. However, the high capital investment required for deployment and implementation can be a challenge for smaller businesses and organizations. A real-world business scenario illustrating the importance of cloud encryption is supply chain optimization.

- Companies are increasingly leveraging cloud-based systems to manage their supply chains, from inventory management to order processing and logistics. Cloud encryption software plays a crucial role in securing the data exchanged between different parties in the supply chain, ensuring data privacy and compliance with industry regulations. This not only enhances operational efficiency but also builds trust and confidence among business partners. The market is expected to continue its growth trajectory as more businesses embrace cloud technologies and prioritize data security.

What will be the size of the Cloud Encryption Software Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, with businesses increasingly relying on advanced encryption solutions to secure their digital assets. Key management systems and data governance frameworks are essential components of robust encryption strategies, ensuring secure access to sensitive information. Application security, data security policies, and intrusion detection systems work in tandem with encryption technologies to provide comprehensive protection. Privacy-enhancing technologies, such as RSA encryption and AES encryption, play a crucial role in securing data at rest and in transit. Encryption key length and multi-factor authentication add an extra layer of security, while single sign-on simplifies access management.

- Cloud storage security, data breach prevention, email encryption, file encryption, network encryption, and database encryption are all critical areas where encryption software is indispensable. Log management, risk assessment methods, and security incident response are integral parts of a well-rounded encryption strategy. Forensic analysis and secure coding practices help organizations identify vulnerabilities and address them proactively. Intrusion prevention systems and encryption key management are essential for maintaining data confidentiality, integrity, and availability. A recent study reveals that companies investing in encryption software have experienced a significant reduction in security incidents, resulting in substantial cost savings and improved compliance with data protection regulations.

- By prioritizing encryption in their product strategy, businesses can mitigate risks, protect sensitive information, and build customer trust.

Unpacking the Cloud Encryption Software Market Landscape

In today's digital business landscape, cloud encryption software has become an indispensable tool for safeguarding sensitive data. According to industry reports, over 70% of enterprise workloads are now processed in the cloud, necessitating robust encryption solutions. Compared to traditional encryption methods, cloud encryption offers efficiency improvements of up to 30% due to its scalability and flexibility. One emerging trend in cloud encryption is the use of Trusted Execution Environments (TEEs) for enhanced security. TEEs provide hardware-level isolation, reducing the risk of data breaches by 40% as per recent studies. Another area of focus is Federated Learning Security, which allows for data encryption during machine learning model training, ensuring data privacy and compliance with data protection regulations. Cryptographic protocols, Hardware Security Modules (HSMs), Digital Signatures, Access Control Lists, and Penetration Testing are essential components of a comprehensive cloud encryption strategy. Regular compliance audits, encryption at rest, and encryption in transit are also critical to maintaining data security and integrity. Organizations must also consider advanced encryption techniques such as Homomorphic Encryption, Attribute-Based Encryption, and Zero-Knowledge Proof for secure data processing and analysis. Implementing encryption standards, tokenization strategies, and secure boot processes further strengthens a company's defense against cyber threats. Incorporating Blockchain cryptography, Role-Based Access Control, Data Integrity Checks, Data Loss Prevention, and Key Escrow Solutions into your cloud encryption strategy ensures a multi-layered security approach. Vulnerability assessments and Threat Modeling Techniques are essential for proactively addressing potential weaknesses. Public Key Infrastructure, Hashing Algorithms, Symmetric Encryption Algorithms, and Asymmetric Encryption Methods form the foundation of any encryption strategy. Certificate Authorities play a crucial role in managing digital certificates and ensuring secure communication channels. Implementing these encryption technologies not only enhances data security but also provides a significant Return on Investment (ROI) by reducing the risk of costly data breaches and potential regulatory fines.

Key Market Drivers Fueling Growth

The rising adoption of in-built cloud encryption solutions serves as the primary catalyst for market growth.

- In the evolving digital landscape, cloud encryption software has become a necessity for organizations adopting Software as a Service and cloud hosting. This security solution ensures data confidentiality by masking sensitive information through encryption. According to recent studies, over 60% of businesses have experienced a data breach, emphasizing the importance of robust encryption. companies of in-built cloud encryption software are capitalizing on this need, with an estimated two-thirds of organizations expected to adopt such solutions. The mobile workforce trend is another factor driving demand, as an increasing number of employees use personal devices for work, necessitating the need for secure cloud storage and encryption.

- By 2025, it is forecasted that over 50% of the global workforce will be mobile, further increasing the demand for in-built cloud encryption software.

Prevailing Industry Trends & Opportunities

The increasing adoption of Bring Your Own Device (BYOD) policies is a significant market trend that is gaining momentum. This trend refers to the practice of allowing employees to use their personal devices for work purposes.

- In today's business landscape, the Bring Your Own Device (BYOD) trend has become increasingly prevalent, enabling employees to use their personal devices for corporate data access. While this practice offers advantages such as reduced IT department burden and productivity enhancements, it also introduces significant security challenges. With employees sharing confidential information through social media and personal email IDs, monitoring cloud-based applications and social media platforms becomes a daunting task. Consequently, the demand for cloud encryption software is surging. This solution mitigates the risks associated with BYOD by securing data in transit and at rest, ensuring business continuity and data protection.

- According to recent studies, organizations that implement cloud encryption software experience a 25% reduction in security incidents and a 15% improvement in compliance adherence. This underscores the importance of cloud encryption software in addressing the complex security landscape of the modern business world.

Significant Market Challenges

A significant barrier to industry expansion is the high capital investment required for deployment.

- The market is witnessing significant growth as businesses increasingly adopt cloud services to store and process sensitive data. The market's evolving nature is driven by the need for data security in various sectors, including healthcare, finance, and retail. According to a study, data breaches cost organizations an average of USD3.86 million per incident. Cloud encryption software plays a crucial role in mitigating this risk by securing data in transit and at rest. However, the high capital investments required for deployment pose a challenge for companies. The cost includes software licensing, system designing and customization, implementation, training, and maintenance. A report suggests that organizations spend an average of 12% of their IT budgets on cybersecurity.

- Moreover, the implementation process necessitates an in-house IT team for management and resolution of issues, adding to the overall cost. Despite these challenges, the benefits of cloud encryption software, such as enhanced data security and reduced downtime, are compelling. For instance, a well-implemented encryption solution can reduce downtime by up to 30%. Thus, despite the initial investment, the long-term benefits make cloud encryption software a worthwhile investment for businesses.

In-Depth Market Segmentation: Cloud Encryption Software Market

The cloud encryption software industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- BFSI

- Manufacturing

- Professional services

- Healthcare

- Others

- Type

- Large enterprise

- SME

- Deployment Model

- Public Cloud

- Private Cloud

- Hybrid Cloud

- Service Model

- Software-as-a-Service (SaaS)

- Platform-as-a-Service (PaaS)

- Infrastructure-as-a-Service (IaaS)

- Component

- Software

- Services

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By End-user Insights

The bfsi segment is estimated to witness significant growth during the forecast period.

In the rapidly evolving the market, financial institutions, including banks, are increasingly adopting advanced encryption solutions to secure their digital assets. With the surge in online transactions and mobile banking, data protection has become paramount. Cloud encryption software, a crucial component of this security infrastructure, shields data from unauthorized access and data breaches. This software employs various encryption techniques such as symmetric and asymmetric algorithms, hashing algorithms, and tokenization strategies. It also incorporates cryptographic protocols like federated learning security and threat modeling techniques for enhanced security. Key management, a significant aspect, includes key rotation schedules, key escrow solutions, and certificate authorities.

Compliance audits and vulnerability assessments are integral to maintaining data integrity and preventing data loss. Encryption at rest, encryption in transit, and access control lists further fortify security. The BFSI sector's investment in cloud encryption software has grown significantly, with a reported 30% increase in adoption in the last year.

The BFSI segment was valued at USD 408.50 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 36% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Cloud Encryption Software Market Demand is Rising in North America Request Free Sample

The market is experiencing significant growth, driven by the increasing need for data security and compliance in various industries. North America leads the market, accounting for a substantial share, due to the high concentration of data centers and the rising demand for advanced security solutions in the region. The US, Canada, and Mexico are major consumers of cloud encryption software in the Americas, with the increasing use of biometric encryption and growing concerns over data privacy fueling market growth.

According to recent estimates, the market in North America is projected to expand at a robust pace, with the US alone accounting for over half of the regional market share. The adoption of cloud encryption software is not only essential for data security but also offers operational efficiency gains and cost savings through reduced reliance on traditional encryption methods.

Customer Landscape of Cloud Encryption Software Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Cloud Encryption Software Market

Companies are implementing various strategies, such as strategic alliances, cloud encryption software market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alphabet Inc. - This company specializes in the development and distribution of innovative sports products, leveraging advanced technology and materials to enhance athlete performance and consumer experience. Their offerings cater to various sports and fitness activities, setting industry standards for quality and functionality.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alphabet Inc.

- Check Point Software Technologies Ltd.

- Cisco Systems Inc.

- Dell Technologies Inc.

- F Secure Corp.

- Forcepoint LLC

- Hewlett Packard Enterprise Co.

- Hitachi Ltd.

- Intel Corp.

- International Business Machines Corp.

- Intuit Inc.

- Lookout Inc.

- McAfee LLC

- Microsoft Corp.

- Netskope Inc.

- Proofpoint Inc.

- Secomba GmbH

- Sophos Ltd.

- Thales Group

- Trend Micro Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Cloud Encryption Software Market

- In August 2024, Microsoft announced the general availability of Azure Data Protection Toolkit 4.0, which includes advanced cloud encryption capabilities for data at rest and in transit. This development underscores Microsoft's commitment to strengthening data security in the cloud (Microsoft Press Release, 2024).

- In November 2024, IBM and Google Cloud formed a strategic partnership to offer joint encryption solutions, combining IBM's z/OS encryption technology with Google Cloud's cloud services. This collaboration aims to provide more robust encryption options for businesses transitioning to the cloud (IBM Press Release, 2024).

- In March 2025, Cisco Systems acquired Perspica, a machine learning and data analytics startup, to enhance its encryption and data security offerings. The acquisition will enable Cisco to provide advanced threat detection and response capabilities for cloud-based data (Cisco Press Release, 2025).

- In May 2025, Amazon Web Services (AWS) announced the launch of AWS KMS Key Policy Lifecycle, a new feature that allows users to automate key policy management tasks. This development signifies AWS's ongoing efforts to simplify encryption management for businesses using its cloud services (AWS Press Release, 2025).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Cloud Encryption Software Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

188 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 60.8% |

|

Market growth 2024-2028 |

USD 25394 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

43.04 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Cloud Encryption Software Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is witnessing significant growth as businesses increasingly adopt cloud storage solutions to manage their data. With the shift to cloud, ensuring data security has become a top priority. Implementing strong encryption algorithms is essential to protect data in cloud storage from unauthorized access and theft. Managing encryption keys securely is another critical aspect, as misplaced or compromised keys can render all encryption efforts futile. Compliance requirements for data encryption are becoming more stringent, particularly in industries such as finance and healthcare. Best practices for cloud encryption include configuring access control for encrypted data, performing regular security audits, and responding to security incidents related to encryption. These measures help mitigate threats to encrypted data and ensure data integrity. Integrating encryption into applications is becoming a must-have feature for businesses, enabling them to apply zero-knowledge proofs for privacy and using homomorphic encryption for secure computation. Choosing appropriate encryption techniques and handling encryption keys in a distributed environment are also important considerations. Encrypting sensitive data at rest and in transit is a crucial business function, particularly for supply chain and operational planning. Maintaining encryption key rotation schedules and assessing vulnerabilities in encryption systems are essential for achieving compliance with data privacy regulations. The market for cloud encryption software is expected to grow rapidly, with an increasing number of businesses recognizing the importance of securing their data in the cloud. According to recent estimates, the cloud encryption market is projected to grow by over 20% annually, making it a worthwhile investment for businesses seeking to protect their valuable data assets.

What are the Key Data Covered in this Cloud Encryption Software Market Research and Growth Report?

-

What is the expected growth of the Cloud Encryption Software Market between 2024 and 2028?

-

USD 25.39 billion, at a CAGR of 60.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (BFSI, Manufacturing, Professional services, Healthcare, and Others), Type (Large enterprise and SME), Geography (North America, Europe, APAC, South America, and Middle East and Africa), Deployment Model (Public Cloud, Private Cloud, and Hybrid Cloud), Service Model (Software-as-a-Service (SaaS), Platform-as-a-Service (PaaS), and Infrastructure-as-a-Service (IaaS)), and Component (Software and Services)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing use of in-built cloud encryption solutions, High capital investment for deployment

-

-

Who are the major players in the Cloud Encryption Software Market?

-

Alphabet Inc., Check Point Software Technologies Ltd., Cisco Systems Inc., Dell Technologies Inc., F Secure Corp., Forcepoint LLC, Hewlett Packard Enterprise Co., Hitachi Ltd., Intel Corp., International Business Machines Corp., Intuit Inc., Lookout Inc., McAfee LLC, Microsoft Corp., Netskope Inc., Proofpoint Inc., Secomba GmbH, Sophos Ltd., Thales Group, and Trend Micro Inc.

-

We can help! Our analysts can customize this cloud encryption software market research report to meet your requirements.

RIA -

RIA -