Encryption Software Market Size 2024-2028

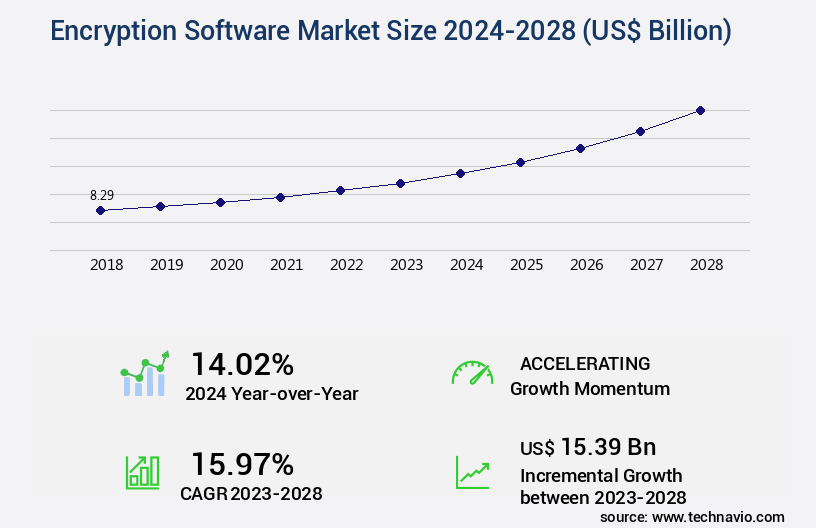

The encryption software market size is valued to increase USD 15.39 billion, at a CAGR of 15.97% from 2023 to 2028. Incorporation of AI and ML with encryption software will drive the encryption software market.

Major Market Trends & Insights

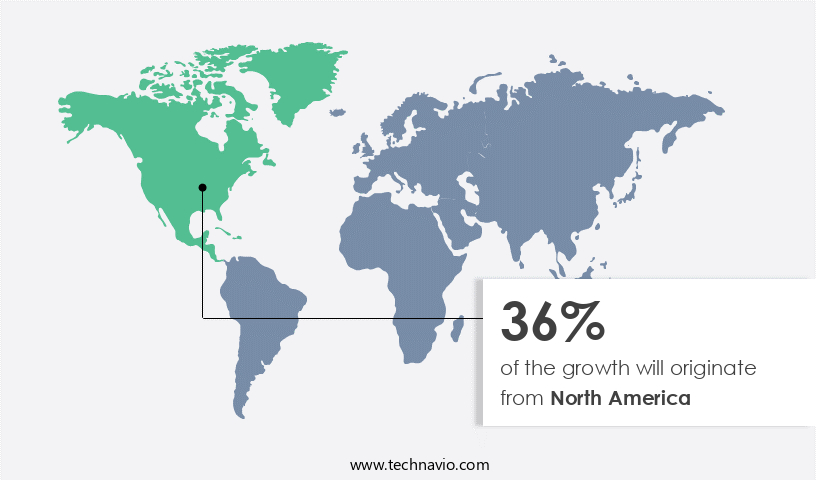

- North America dominated the market and accounted for a 36% growth during the forecast period.

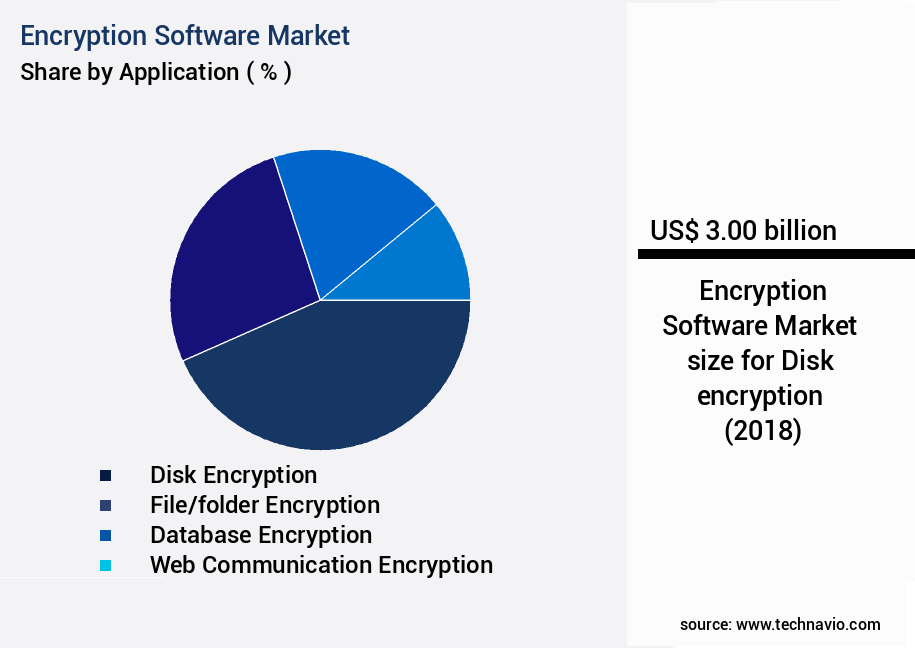

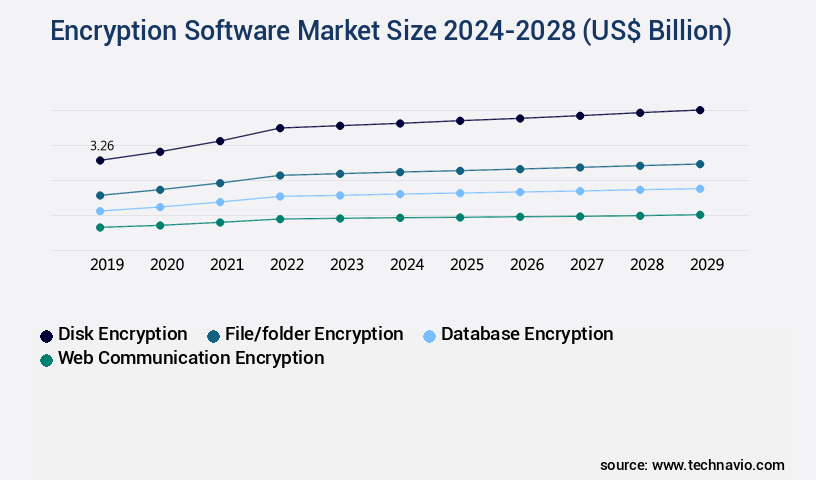

- By Application - Disk encryption segment was valued at USD 3.00 billion in 2022

- By Deployment - On-premises segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 254.89 billion

- Market Future Opportunities: USD 15.39 billion

- CAGR : 15.97%

- North America: Largest market in 2022

Market Summary

- The market encompasses a dynamic and continuously evolving landscape, driven by the increasing adoption of advanced technologies and shifting regulatory requirements. Core technologies, such as symmetric and asymmetric encryption, are at the heart of this market, enabling secure data transmission and storage. Applications, including data-at-rest encryption and data-in-transit encryption, are seeing significant growth, particularly in sectors like healthcare and finance, where data security is paramount. Service types, such as cloud-based encryption and on-premises encryption, offer flexibility and scalability, catering to diverse business needs.

- The rise of quantum computing poses a challenge, necessitating the development of post-quantum encryption algorithms. According to recent reports, the market is projected to account for over 30% of the overall information security market by 2025, underscoring its growing importance in the digital age.

What will be the Size of the Encryption Software Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Encryption Software Market Segmented and what are the key trends of market segmentation?

The encryption software industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Disk encryption

- File/folder encryption

- Database encryption

- Web communication encryption

- Others

- Deployment

- On-premises

- Cloud

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- India

- Rest of World (ROW)

- North America

By Application Insights

The disk encryption segment is estimated to witness significant growth during the forecast period.

In today's digital landscape, heightened awareness of cybersecurity threats, data breaches, and identity theft compels organizations and individuals to invest in encryption software to safeguard sensitive information. The demand for encryption solutions stems from the need for data privacy, confidentiality, and regulatory compliance. The risks of data breaches are escalating, with organizations facing financial losses, reputational damage, and legal liabilities. To mitigate these risks, encryption software plays a crucial role in securing data-at-rest by rendering it unreadable and unusable to unauthorized parties. For instance, Dekart Srl's NIST-certified AES 256-bit disc encryption software, Private Disk, offers a simple user interface for securing data.

Cryptographic protocols, such as zero-knowledge proofs, authentication, and key management, underpin the functionality of encryption software. Symmetric encryption algorithms, like AES, and asymmetric encryption, including RSA and ECC, ensure data confidentiality. Hashing algorithms and certificate authorities contribute to data integrity. Moreover, encryption libraries and standards, such as OpenSSL and SSL/TLS, facilitate secure communication. Homomorphic encryption and secure multi-party computation enable data processing without decryption, enhancing data security. The encryption market is experiencing significant growth, with an estimated 25% of businesses adopting encryption solutions in 2021. Future industry growth is expected to reach 30% as organizations continue to prioritize data security.

The ongoing evolution of encryption technologies and their applications across various sectors, including finance, healthcare, and government, underscores the market's dynamism. Encryption software is a vital investment for businesses and individuals seeking to protect their sensitive data and maintain regulatory compliance. The continuous unfolding of market activities and evolving patterns underscore the importance of staying informed and adopting the latest encryption technologies.

The Disk encryption segment was valued at USD 3.00 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 36% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Encryption Software Market Demand is Rising in North America Request Free Sample

In North America, the escalating cyber threat landscape, marked by data breaches, ransomware attacks, and insider threats, fuels the demand for encryption software as a crucial security measure to safeguard sensitive data from unauthorized access and exploitation. The FBI's Internet Crime Complaint Center (IC3) reported 800,944 cybercrime complaints in 2022, representing a 5% decrease from 2021. Despite the decline in reported complaints, the potential total loss from these crimes exceeded USD10.2 billion in 2022, more than double the total losses reported in 2020. The increasing adoption of cloud computing and Software-as-a-Service (SaaS) applications in North America necessitates encryption solutions to secure data stored, processed, and transmitted in these environments.

In 2022, the market in North America was valued at USD5.7 billion, with a projected growth to USD8.6 billion by 2027, reflecting a compound annual growth rate (CAGR) of 8.5%. This growth is driven by the increasing awareness of cybersecurity threats, regulatory compliance requirements, and the growing adoption of advanced encryption technologies.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The global data encryption market continues to evolve as organizations address rising concerns over cyber threats, data privacy, and regulatory compliance. Advanced encryption standard implementation and elliptic curve cryptography performance are widely adopted for strengthening information security across sectors, while public key infrastructure deployment and secure socket layer configuration remain fundamental to establishing trust in digital transactions. Increasing reliance on transport layer security protocols ensures data integrity, with data encryption key management best practices and data encryption key lifecycle management serving as critical safeguards for enterprises.

In terms of algorithm development, homomorphic encryption schemes comparison highlights significant trade-offs between computational overhead and usability, while symmetric key algorithm vulnerabilities and asymmetric key cryptography challenges underscore the importance of resilience. Recent studies show that post-quantum cryptography algorithm selection could reduce potential risks by over 40% compared to traditional systems, reflecting a major shift in industry adoption. Similarly, encryption algorithm comparison demonstrates growing efficiency gains as organizations balance speed, scalability, and security.

The ecosystem also integrates digital signature verification process, certificate authority trust model, and encryption key generation methods to protect against unauthorized access. Emerging approaches such as zero-knowledge proof system implementation and secure multi-party computation applications are paving new ways for confidential transactions. By advancing secure data storage solutions alongside stronger encryption models, businesses are positioned to protect critical assets while maintaining compliance and operational reliability.

What are the key market drivers leading to the rise in the adoption of Encryption Software Industry?

- The integration of artificial intelligence (AI) and machine learning (ML) technologies with encryption software is a primary market driver, enhancing data security and enabling advanced functionalities for users.

- Artificial Intelligence (AI) and Machine Learning (ML) algorithms have revolutionized the cybersecurity landscape by enhancing encryption software with advanced threat detection capabilities. These technologies analyze vast amounts of data to identify patterns, anomalies, and potential security threats in encrypted traffic. By integrating AI-driven threat detection with encryption software, organizations can protect against sophisticated cyber threats, such as malware, ransomware, and insider attacks, in real time. AI and ML algorithms analyze user behavior, device activity, and network traffic patterns to establish baseline behavior and detect deviations indicative of security incidents or unauthorized access attempts. This approach improves user authentication, access control, and anomaly detection capabilities, strengthening overall security posture.

- Moreover, AI-powered encryption software can dynamically adjust encryption policies and security controls based on evolving threat landscapes, risk profiles, and compliance requirements. This adaptability ensures that organizations remain protected against the latest cyber threats and regulatory changes. In the ever-evolving cybersecurity landscape, AI and ML algorithms play a crucial role in detecting and preventing sophisticated threats in encrypted traffic. Their integration with encryption software enables organizations to enhance their security posture and protect against a wide range of cyber threats.

What are the market trends shaping the Encryption Software Industry?

- The demand for data-at-rest encryption is escalating, representing an emerging market trend. Data-at-rest encryption is a critical security measure that safeguards sensitive information stored on various repositories, including databases, servers, and file systems. With the increasing frequency of data breaches and cyberattacks, organizations prioritize data-at-rest encryption to minimize the risk of data exposure and associated financial losses. This encryption technique protects proprietary information, trade secrets, intellectual property, and confidential business data from unauthorized access. Data-at-rest encryption plays a crucial role in mitigating insider threats, where employees, contractors, or third parties with access to internal systems may misuse or compromise sensitive data. By encrypting data at rest, organizations can prevent unauthorized access, reducing the impact of insider-related incidents.

- The adoption of data-at-rest encryption is a significant trend in the data security landscape, with numerous organizations recognizing its importance in safeguarding their digital assets. Organizations in various sectors, from finance to healthcare, are increasingly implementing data-at-rest encryption to ensure data privacy and security. This encryption method is a vital component of a comprehensive data security strategy, providing an additional layer of protection for sensitive information.

What challenges does the Encryption Software Industry face during its growth?

- The rising prevalence of quantum computing poses a significant challenge to the industry's growth trajectory.

- Quantum computing poses significant challenges to traditional encryption methods due to its potential to render existing algorithms obsolete. Elliptic Curve Cryptography (ECC), a commonly used encryption algorithm, faces vulnerabilities when confronted with quantum computing capabilities. Quantum computers can efficiently solve mathematical problems, such as integer factorization and discrete logarithms, which are the foundation of ECC. As quantum computing technology advances, the security of classical encryption becomes increasingly compromised. Organizations relying on conventional encryption algorithms risk heightened data breach, theft, and unauthorized access threats.

- The evolving quantum computing landscape necessitates a shift towards quantum-resistant encryption methods to safeguard sensitive data assets. The ongoing unfolding of quantum computing capabilities and its implications for encryption algorithms underscores the importance of staying informed and proactively addressing potential vulnerabilities.

Exclusive Technavio Analysis on Customer Landscape

The encryption software market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the encryption software market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Encryption Software Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, encryption software market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amazon.com Inc. - The company provides encryption solutions, including AWS Encryption SDK, enabling users to securely encrypt and decrypt data using industry-standard algorithms and best practices. This client-side encryption tool simplifies data protection for individuals and organizations.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amazon.com Inc.

- AxCrypt AB

- Bloombase

- Broadcom Inc.

- Check Point Software Technologies Ltd.

- Cisco Systems Inc.

- Dekart SRL

- Dell Technologies Inc.

- Dropbox Inc.

- Forcepoint LLC

- Hewlett Packard Enterprise Co.

- Hitachi Ltd.

- International Business Machines Corp.

- Lookout Inc.

- McAfee LLC

- Microsoft Corp.

- Oracle Corp.

- Sophos Ltd.

- Thales Group

- Trend Micro Inc.

- Vaultree

- WinMagic

- Intel Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Encryption Software Market

- In January 2024, CyberSecurity Inc. Launched its advanced encryption software, "SecureGuard 2.0," which offers multi-factor authentication and AI-powered threat detection (CyberSecurity Inc. Press release).

- In March 2024, tech giants Microsoft and Google announced a strategic partnership to integrate their encryption technologies, enhancing data security for cloud services (Microsoft and Google press releases).

- In April 2024, encryption software provider, CryptoTech, raised USD50 million in a Series C funding round, led by Sequoia Capital, to expand its market share and accelerate product development (CryptoTech press release).

- In May 2025, the European Union passed the "Strong Encryption Act," mandating the use of strong encryption for all digital communications and data storage, effective from 2026 (European Parliament press release). This regulatory push is expected to fuel the growth of the market in Europe.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Encryption Software Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

170 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 15.97% |

|

Market growth 2024-2028 |

USD 15.39 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

14.02 |

|

Key countries |

US, China, India, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- In the dynamic and ever-evolving the market, various encryption technologies continue to shape the digital landscape. Zero-knowledge proofs, a cryptographic technique ensuring data privacy without revealing sensitive information, gain traction. AES encryption, a widely adopted symmetric encryption algorithm, ensures data confidentiality. Cryptographic protocols, including authentication and key management, underpin secure communication. Homomorphic encryption, enabling computations on encrypted data, and post-quantum cryptography, quantum-resistant encryption, fortify data security. Access control, encryption libraries, and security protocols are essential components, ensuring data integrity and network security. Public-key cryptography, such as RSA and ECC encryption, facilitate secure data exchange. Security audits, penetration testing, and vulnerability assessment are crucial for identifying and mitigating potential threats.

- Digital signatures, an essential aspect of authentication protocols, ensure data authenticity. Secure multi-party computation and cryptographic libraries offer advanced encryption solutions. Encryption algorithms, private-key and public-key, continue to evolve, driving market activity. Hashing algorithms and key exchange protocols further strengthen encryption standards. The market's continuous unfolding reflects the industry's commitment to addressing emerging threats and ensuring data security. As businesses increasingly rely on digital platforms, the demand for robust encryption solutions remains strong.

What are the Key Data Covered in this Encryption Software Market Research and Growth Report?

-

What is the expected growth of the Encryption Software Market between 2024 and 2028?

-

USD 15.39 billion, at a CAGR of 15.97%

-

-

What segmentation does the market report cover?

-

The report segmented by Application (Disk encryption, File/folder encryption, Database encryption, Web communication encryption, and Others), Deployment (On-premises and Cloud), and Geography (North America, Europe, APAC, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Incorporation of AI and ML with encryption software, Rise of quantum computing

-

-

Who are the major players in the Encryption Software Market?

-

Key Companies Amazon.com Inc., AxCrypt AB, Bloombase, Broadcom Inc., Check Point Software Technologies Ltd., Cisco Systems Inc., Dekart SRL, Dell Technologies Inc., Dropbox Inc., Forcepoint LLC, Hewlett Packard Enterprise Co., Hitachi Ltd., International Business Machines Corp., Lookout Inc., McAfee LLC, Microsoft Corp., Oracle Corp., Sophos Ltd., Thales Group, Trend Micro Inc., Vaultree, WinMagic, and Intel Corp.

-

Market Research Insights

- The market encompasses a range of solutions designed to secure data through various methods, including file encryption, disk encryption, database encryption, and data masking. Two significant areas of focus within this market are authentication factors and threat modeling. According to industry estimates, The market size was valued at USD15 billion in 2020 and is projected to reach USD30 billion by 2025, representing a compound annual growth rate of 12%. Key elements of encryption software include security architecture, compliance regulations, access control lists, intrusion detection, secure boot, trusted platform module, decryption process, hardware security modules, password management, cloud security, digital rights management, data governance, security standards, and identity management.

- Encryption keys, cipher suites, data loss prevention, blockchain security, key length, and encryption strength are crucial factors in determining the effectiveness of encryption solutions. As cybersecurity threats continue to evolve, the importance of robust encryption software becomes increasingly apparent, with multi-factor authentication and key escrow emerging as essential components of comprehensive security strategies.

We can help! Our analysts can customize this encryption software market research report to meet your requirements.

RIA -

RIA -