- US,Canada,Germany,UK,China - Size and Forecast 2022-2026")

Enjoy complimentary customisation on priority with our Enterprise License!

The infectious disease diagnostics market share is expected to increase to USD 13.94 billion from 2021 to 2026, and the market's growth momentum will accelerate at a CAGR of 6.7%.

The Infectious Disease Diagnostics Market is witnessing substantial growth attributed to the rising majority of chronic diseases and the growing demand for early diagnostic tests. Key factors driving market expansion include advanced molecular techniques, novel diagnostics, and breakthrough innovations in disease detection and monitoring. Additionally, the market benefits from government initiatives, funding, and support systems aimed at combating infectious diseases. Companies like bioMérieux and Siemens Healthineers AG are at the forefront, offering cost-effective tools and cutting-edge technologies. With a focus on accurate diagnosis and effective treatment, the market presents significant growth opportunities, particularly in regions like the Asia Pacific where infectious diseases are prevalent.

|

Study Period |

2022 |

|

Base Year For Estimation |

2021 |

|

CAGR |

6.7% |

|

Forecast period |

2022-2026 |

|

Fastest Growing Region |

37% of North America |

|

List of Charts and Table |

last_exhibit |

For More Highlights About this Report, Download Free Sample in a Minute

In company offerings, we provide an in-depth analysis of 20 top company profiles, along with other valuable insights comprising:

? Company Overviews

? Key News and Updates

? Products and Services

? Market-leading Offerings

? Focused Segments

Abbott Laboratories - Under the established pharmaceuticals products segment, the company focuses on core laboratory, molecular solutions, point of care solutions, and rapid diagnostics.

Becton Dickinson and Co. - The BD Medical segment offers a range of medication delivery solutions, medication management solutions, diabetes care, and pharmaceutical systems.

The following are the leading companies in the market_name . These companies are adopting various strategies, including strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to strengthen their market presence. Collectively, they hold the largest market share and set industry trends. The market research and growth report also provides detailed analyses of the competitive landscape and information about 15 key market companies, including:

Our segment comprises two primary segments, each with its respective sub-segments for further detailed analysis within specific national markets. Furthermore, our market coverage extends across geographic regions, with comprehensive breakdowns to provide in-depth insights.

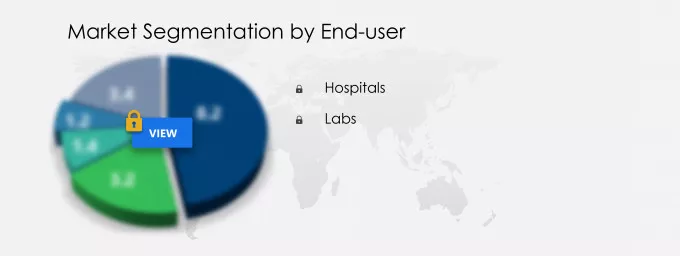

Based on End-user , the infectious disease diagnostics sub-segment dominated the market in 2022 and continue to grow during the forecast period.

The growth is attributed to the increase in the number of patients suffering from different types of diseases, such as AIDS, tuberculosis (TB) meningitis, and COVID-19, globally. The growing presence of the large-, medium-, and small-sized hospitals that procure medical products, including infectious disease diagnostic instruments, in bulk from suppliers and group purchasing organizations (GPOs) will further boost the market growth.

Get a glance at the market contribution of various segments Request Free Sample

The US is the leading contributor to the market in North America, driven by an increasing focus on treating infectious diseases caused by microorganisms. The market is projected to experience steady growth during the forecast period, largely due to the rising prevalence of infectious diseases such as AIDS, TB, meningitis, influenza, and pneumonia. Respiratory tract infections caused by bacteria are among the most common conditions in humans, imposing a high economic burden. For instance, the Centers for Disease Control and Prevention (CDC) reported approximately 85 million infections and 10.75 million deaths in the US in 2021, with 25.6% of US cases with genotype data attributed to recent transmission. These conditions have led to high adoption rates of infectious disease diagnostic instruments, kits, and reagents for accurate diagnosis and treatment.

In Canada, researchers have developed new methods to diagnose bacterial infections. For example, the University of British Columbia, Okanagan campus, and the University of Calgary have developed a diagnostic tool that allows healthcare practitioners to perform on-spot diagnosis of bacterial infections, offering rapid, label-free, and contactless diagnosis while screening for bacterial interactions with antibiotics. Similarly, the University of California San Francisco (UCSF) in the US has developed a radioactively labeled tracer to track bacteria in mice.

The regional infectious disease diagnostics market is expected to accelerate during the forecast period due to the development of new antibacterial drugs and increased funding for new therapies. Organizations like the Biomedical Advanced Research and Development Authority (BARDA) support and fund the development of new anthrax vaccines. Additionally, vendors are expanding geographically through acquisitions, such as Thermo Fisher Scientific Inc.'s acquisition of Mesa Biotech, Inc. to enhance molecular diagnostics at the point of care (POC).

The COVID-19 pandemic had a mixed impact on the regional market. The rise in COVID-19 cases in early 2020 led to partial lockdowns, affecting non-urgent pharmaceutical operations. However, the focus on developing vaccines and therapeutics for COVID-19 boosted the market. For instance, in December 2020, the US FDA authorized the emergency use of the COVID-19 mRNA vaccine developed by Pfizer Inc. and BioNTech SE. By June 2, 2022, a total of 579 million vaccines were administered in the US. Additionally, Colorado announced USD173 million in federal funding in July 2021 to expand COVID-19 testing in schools, even after restrictions were lifted.

Since early 2021, relaxed lockdown restrictions have helped revive the pharmaceutical supply chain in the region. The rising prevalence of infectious diseases will continue to drive the growth of the regional infectious disease diagnostics market during the forecast period.

Our researchers analyzed the data with 2023 as the base year, along with the key trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Key Driver

One of the key factors driving the global market growth is the increasing prevalence of infectious diseases.The outbreaks of infectious diseases have increased due to changing lifestyles, which result in reduced immunity.The pattern of infection incidence has also been changing with the evolution of drug-resistant pathogens.As per the Joint United Nations Programme on HIV/AIDS data of 2020, 680,000 people died from AIDS-related illnesses across the world.The prevalence of meningococcal disease, which is caused by the bacterium Neisseria, meningitides, was decreased, owing to the meningococcal vaccines, which were licensed and made available in August 2020 in the US.According to the CDC data for 2021, annually, almost 4,100 cases and 500 deaths occur due to meningococcal disease in the US.The rise in the prevalence of infectious diseases is expected to drive the growth of the market in focus during the forecast period.

Significant Trend

Increase in M&A is one of the key infectious trends that is expected to impact the industry positively in the forecast period.The vendors operating in the market are focusing on pursuing inorganic growth to tap into rapidly growing markets, such as India, Brazil, China, and South Africa.In August 2021, Sanofi S.A acquired Translate Bio Inc., a clinical-stage mRNA therapeutics company, for over USD3 billion.In April 2021, Pfizer Inc. acquired Amplyx Pharmaceuticals Inc., an American pharmaceutical company, with an aim to access the Fosmanogepix (APX001).In May 2020, Novavax Inc., a biotechnology company specializing in next-generation vaccines, spent over USD160 million and acquired Praha Vaccines A.S.A rise in M&A activities across the globe is anticipated to boost the growth of the market in the forecast years.

Key Challenge

One of the key challenges to global market growth is the availability of counterfeit drugs in developing economies.The counterfeit products pose a challenge for global pharmaceutical manufacturers, costing them billions of dollars and negatively affecting their brand reputation.Counterfeit drugs provide a false sense of security to the patients using them while endangering them even more with the contents of the products.The counterfeits are widely available in low-income and developing countries because of insufficient regulations and manufacturing control.The fear of stigma often makes HIV patients buy antiretrovirals through unauthorized retailers.Due to the increase in the prevalence of AIDS in underdeveloped countries, such as India, Brazil, and Iran, counterfeiters may gain profits from the counterfeiting of antiretroviral drugs without easily being noticed.The wide availability of counterfeit drugs may hamper the growth of the market in focus during the forecast period.

The infectious disease diagnostics market thrives on breakthrough technologies like mass spectrometry and next-generation sequencing (NGS), enabling early diagnosis in healthcare settings. Point-of-care testing and molecular techniques offer cost-effective solutions, especially in emerging economies. Joint ventures and mergers facilitate the development of technologically advanced products and expand product lines. Regulatory guidelines and government-funded initiatives drive innovation and ensure the accuracy of diagnostic tools. With a focus on detecting bacterial infections and sexually transmitted diseases, the market addresses the rising incidence of infectious diseases, emphasizing the importance of accurate and timely screening in centralized laboratories.

|

We can help! Our analysts can customize this market research report to meet your requirements.

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Five Forces Analysis

5 Market Segmentation by End-user

6 Customer Landscape

7 Geographic Landscape

8 Drivers, Challenges, and Trends

9 Vendor Landscape

10 Vendor Analysis

11 Appendix

Get lifetime access to our

Technavio Insights

Cookie Policy

The Site uses cookies to record users' preferences in relation to the functionality of accessibility. We, our Affiliates, and our Vendors may store and access cookies on a device, and process personal data including unique identifiers sent by a device, to personalise content, tailor, and report on advertising and to analyse our traffic. By clicking “I’m fine with this”, you are allowing the use of these cookies. Please refer to the help guide of your browser for further information on cookies, including how to disable them. Review our Privacy & Cookie Notice.