Unified Endpoint Management (UEM) Market Size 2026-2030

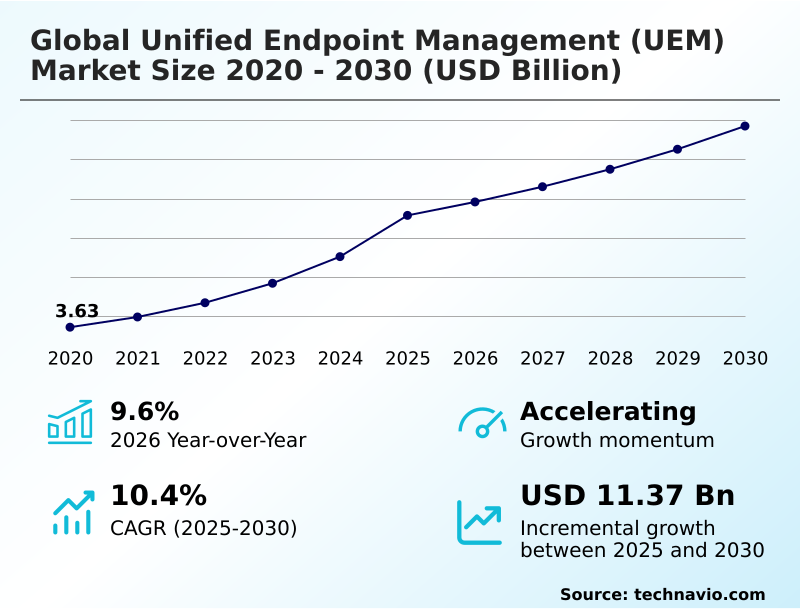

The unified endpoint management (uem) market size is valued to increase by USD 11.37 billion, at a CAGR of 10.4% from 2025 to 2030. Institutionalization of AI and automated self-healing endpoints will drive the unified endpoint management (uem) market.

Major Market Trends & Insights

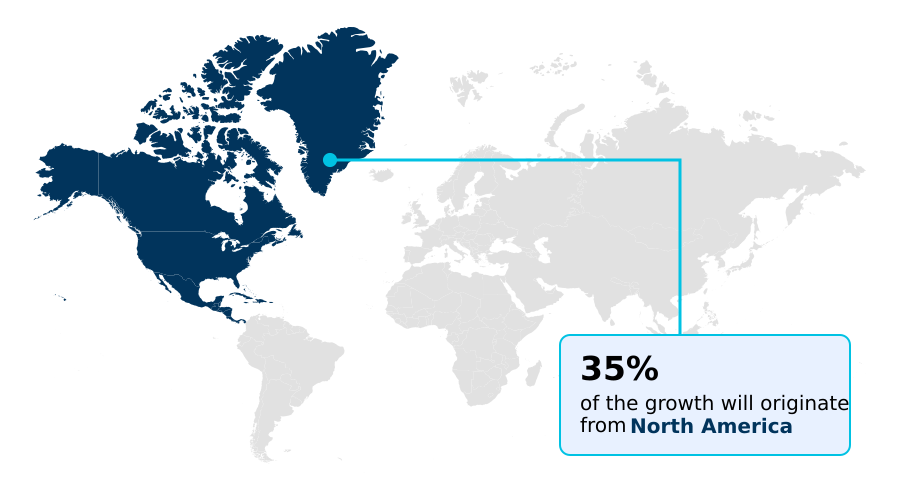

- North America dominated the market and accounted for a 35.1% growth during the forecast period.

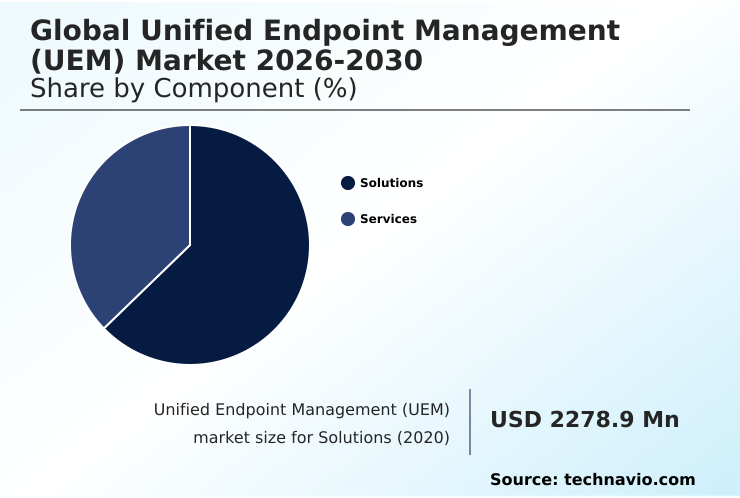

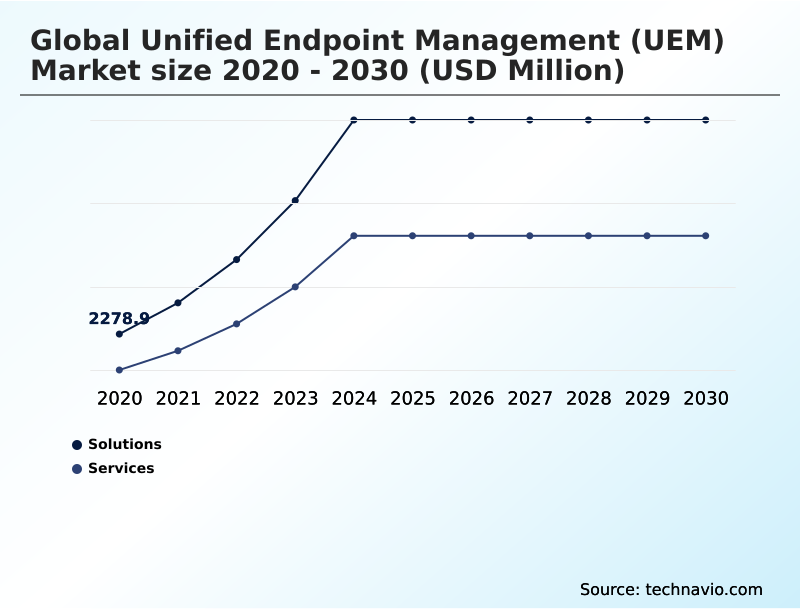

- By Component - Solutions segment was valued at USD 7.80 billion in 2024

- By Deployment - Cloud segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 25.59 billion

- Market Future Opportunities: USD 11.37 billion

- CAGR from 2025 to 2030 : 10.4%

Market Summary

- The unified endpoint management (UEM) market is defined by a convergence of security and operational efficiency, driven by the complexities of the modern digital workplace. This technology provides a consolidated approach to overseeing all enterprise devices, from traditional laptops to an expanding array of IoT endpoints.

- Core market drivers include the push for zero-trust security frameworks and the institutionalization of AI to facilitate automated, self-healing capabilities. A primary trend is the evolution toward unified orchestration of non-traditional endpoints, such as XR devices used in specialized training. For instance, a global logistics firm must manage a diverse fleet of ruggedized handhelds, in-vehicle computers, and back-office workstations.

- A UEM platform allows the firm to apply a single, consistent security policy, deploy software updates, and remotely troubleshoot devices worldwide, ensuring supply chain integrity and operational continuity.

- However, challenges such as the technical complexity of migrating legacy systems and navigating fragmented data sovereignty regulations require strategic planning and significant investment from enterprises aiming to achieve a truly unified and secure endpoint ecosystem.

What will be the Size of the Unified Endpoint Management (UEM) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Unified Endpoint Management (UEM) Market Segmented?

The unified endpoint management (uem) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Solutions

- Services

- Deployment

- Cloud

- On-premises

- Hybrid

- End-user

- Large enterprises

- SMEs

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- North America

By Component Insights

The solutions segment is estimated to witness significant growth during the forecast period.

The solutions segment is the technological core of the unified endpoint management market, providing frameworks for securing and overseeing diverse hardware assets.

These platforms deliver zero-touch provisioning and employ intelligent policy enforcement to automate application deployment and enforce rigorous security configurations. The integration of user and entity behavior analytics is crucial for modern risk assessment.

By consolidating disparate management silos, organizations can reduce administrative complexity, with some reporting a 40% reduction in critical security vulnerabilities through automated patch management and proactive vulnerability remediation.

This approach to endpoint configuration management supports a secure and efficient digital environment, using AI and automated self-healing to manage corporate-owned personal-enabled devices and ensure robust data loss prevention.

The Solutions segment was valued at USD 7.80 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 35.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Unified Endpoint Management (UEM) Market Demand is Rising in North America Get Free Sample

Geographic dynamics in the unified endpoint management market are distinct, with North America leading innovation and accounting for over 35% of the market's incremental growth.

This region's maturity in cloud-first management strategies drives demand for platforms with predictive analytics for device health.

In Europe, a focus on data sovereignty compliance and localized data storage solutions is paramount, with firms reporting a 20% improvement in audit pass rates after adopting compliant UEM policies.

The APAC region is the fastest-growing, fueled by mobile-first economies that demand scalable mobile application management and containerization technologies.

Across all regions, the push for a single pane of glass management and orchestration-led discipline is universal, as organizations seek to standardize security and operations.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Achieving unified endpoint management cost optimization is a primary goal for modern enterprises. This involves a strategic approach to UEM for industrial internet of things and ensuring zero trust security for mobile devices, which are now critical assets.

- The role of AI in unified endpoint management is expanding, directly impacting the UEM and digital employee experience DEX by enabling proactive support. Effectively managing BYOD policies with UEM is essential, and many organizations are realizing cloud-native UEM platform benefits such as scalability and accessibility.

- Specific sectors have unique needs, leading to the development of UEM solutions for healthcare compliance and the financial services sector. Key technical components include automated patch management in UEM and deep UEM integration with identity providers. Functionally, this extends to remote device management for logistics and the emerging need for securing XR devices with UEM.

- Navigating UEM data sovereignty compliance features is a major challenge for global firms. Many are in the process of migrating from MDM to UEM to handle UEM for ruggedized device environments. Security is enhanced through passwordless authentication for UEM access, while UEM threat detection and response capabilities are crucial.

- Ultimately, improving IT efficiency with UEM is achieved through endpoint analytics for performance monitoring and true cross-platform management with a UEM.

What are the key market drivers leading to the rise in the adoption of Unified Endpoint Management (UEM) Industry?

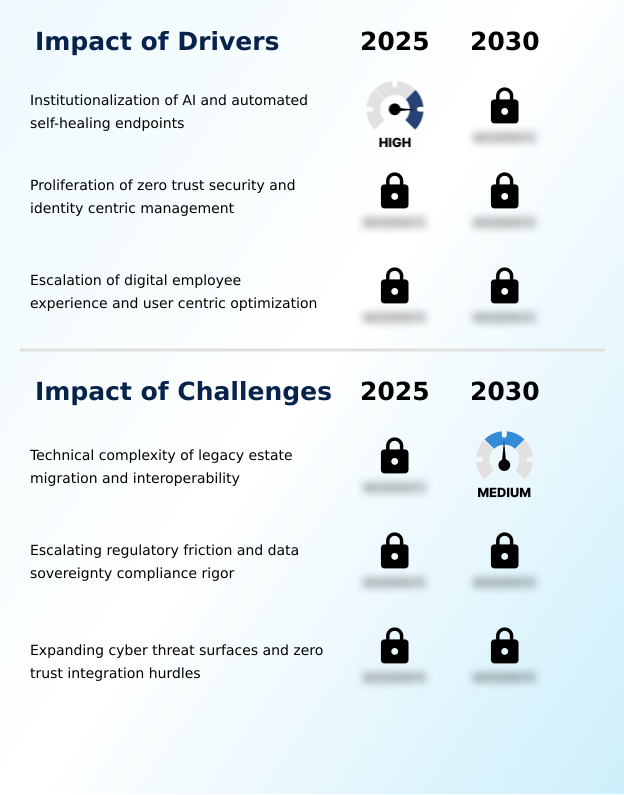

- A key market driver is the institutionalization of AI to enable automated, self-healing capabilities for endpoints, enhancing system resilience and security.

- Market growth is significantly propelled by the institutionalization of AI and automated self-healing, which facilitates proactive software-driven maintenance and user-centric optimization. The proliferation of zero-trust security frameworks is another major driver, making identity-centric management a cornerstone of modern IT.

- This has led to an increased focus on the digital employee experience, with platforms using system performance telemetry and non-intrusive background updates to enhance productivity. Organizations implementing these identity-aware frameworks report a reduction in credential-based breaches by over 60%.

- The convergence of management and security into a singular, orchestration-led discipline allows for the consolidation of security agents, reducing system latency and simplifying the overall software stack.

What are the market trends shaping the Unified Endpoint Management (UEM) Industry?

- A key trend shaping the market is the industrialization of zero-trust architecture integration. This involves a fundamental shift from perimeter-based security to a model of continuous verification for every user and device.

- Key market trends are centered on the industrialization of security and management, leading to the deep integration of zero trust architecture integration. This shift away from traditional perimeters is driving demand for solutions with hardware-root-of-trust validation and real-time policy enforcement engine capabilities.

- The evolution toward unified IoT and XR device orchestration is expanding the scope of management to include non-traditional endpoints used for specialized tasks like spatial engineering device management. This comprehensive device visibility is becoming a standard, with platforms that can deploy modular application containers to diverse hardware.

- The adoption of AI-driven spectrum analysis within these platforms has been shown to reduce critical security vulnerabilities by nearly 40% while enhancing the identity-centric security posture.

What challenges does the Unified Endpoint Management (UEM) Industry face during its growth?

- A significant challenge impacting market growth is the technical complexity associated with migrating legacy IT estates and ensuring interoperability across heterogeneous device environments.

- The market faces significant hurdles, primarily the technical complexity of legacy estate migration and achieving interoperability across heterogeneous device environments. This requires extensive use of application programming interfaces and often results in prolonged deployment timelines, with migration projects exceeding budgets by an average of 20%.

- Another challenge is escalating regulatory friction, demanding stringent data sovereignty compliance and localized data storage solutions, which adds an estimated 15% to compliance overhead. The expanding cyber-threat surface, exacerbated by bring-your-own-device practices, makes achieving full zero trust integration difficult. This requires a move toward more resilient security frameworks and away from legacy on-premises client management tools.

Exclusive Technavio Analysis on Customer Landscape

The unified endpoint management (uem) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the unified endpoint management (uem) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Unified Endpoint Management (UEM) Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, unified endpoint management (uem) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

42Gears Mobility Systems Ltd. - Key offerings focus on resilient cybersecurity for devices, data, and access controls, providing a foundation for secure, unified endpoint management.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 42Gears Mobility Systems Ltd.

- Absolute Software Corp.

- Atera Networks Ltd.

- BlackBerry Ltd.

- Citrix Systems Inc.

- IBM Corp.

- Ivanti Software Inc.

- JAMF Holding Corp.

- JumpCloud Inc.

- Matrix42 GmbH

- Microsoft Corp.

- Miradore Oy

- Mitsogo Inc.

- N able Inc.

- NinjaOne

- Open Text Corp.

- Sand Studio

- Sophos Group Ltd.

- Tanium Inc.

- Zoho Corp. Pvt. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Unified endpoint management (uem) market

- In October 2024, 42Gears Mobility Systems Ltd. and SATO Holdings Corp. announced a strategic partnership to provide centralized, remote management for industrial and mobile printers, enhancing their offerings for the logistics and retail sectors.

- In November 2024, Sophos Group Ltd. published a threat report detailing a 40% year-over-year increase in ransomware attacks targeting unmanaged devices, reinforcing the need for unified security policies and integrated threat defense.

- In March 2025, Microsoft Corp. announced a major update to its Intune UEM platform, integrating advanced AI-driven predictive analytics to proactively identify device health issues and security vulnerabilities before they impact users.

- In April 2025, Ivanti Software Inc. acquired a startup specializing in AI for IT operations (AIOps), aiming to integrate autonomous self-healing capabilities into its Neurons for UEM platform to reduce manual intervention.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Unified Endpoint Management (UEM) Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 296 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 10.4% |

| Market growth 2026-2030 | USD 11365.0 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 9.6% |

| Key countries | US, Canada, Mexico, Germany, France, UK, Italy, Russia, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, UAE, Saudi Arabia, South Africa, Israel and Egypt |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The unified endpoint management (UEM) market is undergoing a structural evolution, driven by the convergence of security and IT operations into a framework of autonomous IT operations. The integration of zero-trust security frameworks is no longer an option but a baseline requirement, compelling boardroom decisions on security investment. This shift demands identity-centric management and continuous authentication across all endpoints.

- Advanced platforms now leverage AI-enabled predictive remediation and AI-driven spectrum analysis to preemptively address issues, a transition from reactive to proactive endpoint resilience. The focus on digital employee experience has led to user-centric optimization tools that use system performance telemetry for real-time device posture checks.

- Adopting these advanced systems has enabled organizations to automate up to 70% of their routine remediation tasks. This includes automated patch management and vulnerability remediation. Platforms are incorporating everything from passwordless authentication and remote wipe capabilities to endpoint privilege management and mobile threat defense.

- The challenge remains in achieving seamless context-aware orchestration and cross-platform policy enforcement across heterogeneous device environments, especially with bring-your-own-device practices and the need for zero-touch provisioning and agentless management capabilities for IoT and XR device orchestration.

What are the Key Data Covered in this Unified Endpoint Management (UEM) Market Research and Growth Report?

-

What is the expected growth of the Unified Endpoint Management (UEM) Market between 2026 and 2030?

-

USD 11.37 billion, at a CAGR of 10.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Solutions, and Services), Deployment (Cloud, On-premises, and Hybrid), End-user (Large enterprises, and SMEs) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Institutionalization of AI and automated self-healing endpoints, Technical complexity of legacy estate migration and interoperability

-

-

Who are the major players in the Unified Endpoint Management (UEM) Market?

-

42Gears Mobility Systems Ltd., Absolute Software Corp., Atera Networks Ltd., BlackBerry Ltd., Citrix Systems Inc., IBM Corp., Ivanti Software Inc., JAMF Holding Corp., JumpCloud Inc., Matrix42 GmbH, Microsoft Corp., Miradore Oy, Mitsogo Inc., N able Inc., NinjaOne, Open Text Corp., Sand Studio, Sophos Group Ltd., Tanium Inc. and Zoho Corp. Pvt. Ltd.

-

Market Research Insights

- The market's dynamic is shaped by a strategic shift towards a single pane of glass management, enabling orchestration-led discipline through zero trust architecture integration. This is driven by AI and automated self-healing, utilizing predictive analytics for device health and proactive software-driven maintenance.

- Technologies such as containerization technologies and over-the-air provisioning are essential for mobile application management and supporting corporate-owned personal-enabled devices. The goal is an identity-centric security posture, enforced by a real-time policy enforcement engine that leverages intelligent policy enforcement and user and entity behavior analytics.

- Firms are adopting cloud-first management strategies to handle the expanding cyber-threat surface and implement resilient security frameworks. This approach requires autonomous self-healing capabilities and seamless security operations center integration, moving beyond on-premises client management tools to achieve robust device lifecycle management and effective vulnerability remediation, even for rugged and spatial engineering device management.

We can help! Our analysts can customize this unified endpoint management (uem) market research report to meet your requirements.

RIA -

RIA -